Over the last couple of weeks, we looked at how mutual funds are taxed. We spoke about indexation benefit being available for long term capital gains in debt funds. What is indexation benefit and how does it make debt funds a superior option to traditional products such as fixed deposits?

In traditional products such as fixed deposits or debentures, the interest on your investment is taxed in your slab rate; that is –whichever tax slab you fall under. With debt mutual funds too, your gains (short-term gains) are taxed at your slab rate if you held them for less than 3 years. But for investments held for over 3 years, you are taxed at 20% with indexation benefit. What does indexation do? It simply brings the cost of your investment to the current value, by considering cost inflation index. In other words, the value of your original investment is increased to the extent of inflation during your holding period.

Thus, by inflating your original cost, the gain (sale – indexed cost) actually comes down and you pay a 20% tax on such gain.

Let us take an example to see how this works:

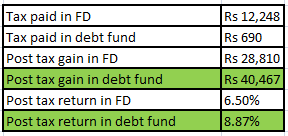

You invested Rs 1 lakh in say January 2012 in a debt fund that delivered 9% annualised return in 4 years. At the same time, you also invested in a deposit returning 9% compounded return. Your deposit would have matured on December 31, 2015. Rs 1 lakh of investment will leave you with Rs 1,41,158 after 4 years. If you are in the 30% tax bracket, deposit money in hand, post tax would be Rs 1,28,810. You would have paid Rs 12,348 as taxes (not considering cess, surcharge etc.)!

Now let us come to the debt mutual fund. Having held the fund for 4 years, if you exit the fund (on the same day as your deposit) you will be allowed indexation benefit.

The indexation would be: your investment costcost inflation index in year of sale/cost inflation index in the year of purchase. So your indexed cost will be Rs 1,00,0001081/785 = Rs 1,37,707. Your long-term gain is therefore 1,41,158-1,37,707= Rs 3,451. Tax on this is 3,451*20/100= Rs 690 and post tax money in hand is Rs 1,40,467.

(click here for cost inflation index table)

The table below makes it obvious how debt funds provide superior post tax returns as a result of indexation, assuming that both FD and debt fund earn the same (which is not the case as debt funds hold higher return potential).

In some cases where the indexed investment amount is greater than your sale price and there is a capital loss for tax purposes. Such loss can be declared and also offset against any other long-term capital gain.

I want to invest Lumpsum amount in one debt mutual fund since the returns are a bit higher than the Bank FD . Can you plzz tell that is it the right time to invest or should I wait . What are the things to be noted b4 investing in Debt Mutual Funds.

Hi Raj,

Debt funds generally do provide returns higher than FDs. If you hold them for more than three years, they also have better tax treatment than FDs (it becomes long-term and thus capital gains are taxed at 20% with indexation benefit). You can always invest in debt funds at any time. Even if the interest rate cycle is now turning down, it will also affect FD returns.

The type of debt fund you invest in will depend on your time horizon. If it is less than 1 year, then go for ultra-short term funds. If its 1-2 years, then go for short-term funds. For a longer period, go for long-term debt funds (both dynamic bond funds and income accrual funds). You can read all about debt funds on these two links:https://blog.fundsindia.com/blog/general/fundsindia-explains-what-are-debt-funds/8982 and https://blog.fundsindia.com/blog/general/fundsindia-explains-how-do-debt-funds-deliver-returns/9021

Next, it depends on your level of risk and how much volatility in your returns you can take. Depending on that, you can choose the correct fund category. For example, if you cannot take risk, then don’t go for funds that have bonds that are low-rated. Similarly, dynamic bond funds will see returns move more than income accrual funds. Hope this helps.

Thanks,

Bhavana

Thanks Madam for such useful and yet simple to understand article .

My query is : How to calculate the capital gain and taxation in debt fund when multiple purchase and sell have been done at multiple point of time ?

Regards

D Prasoon

Fundsindia A/C Holder since 6 years

Thanks Prasoon! The capital gains and whether it is short-term or long-term is calculated based on the first-in-first-out logic – it is assumed that the first unit you sold is the first unit you bought. Here is a blog post on calculating capital gains holding period on multiple purchases and sale:https://blog.fundsindia.com/blog/mutual-funds/fundsindia-explains-how-are-mutual-funds-taxed-part-ii/9153. This should make it clear.

–

Bhavana

Hi Guys,

Could you double check your numbers.

Purchase date is Jan ’12 which implies financial year 11-12.

Thus the CII for purchase date should be 785 and not 852 (Going by your shared link http://ow.ly/g4qa300mQpo)

=> Indexed cost = 1,00,000*1081/785=1,37,707

=> Taxable amount = 1,41,158 – 1,37,707 = 3451

=> Tax: 20% of 3451 = 690

=> Net take away amount = 1,41,158 – 690 = 1,40,467

=> Tax adjusted return = 8.86 %

Apologies for the error.

Hi Harshit, thanks for bringing it to our notice. We have made the necessary changes accordingly.

Hi Bhavana,

I tried posting this from normal comments section as well but it is still in moderation, hence posting from facebook.

I think numbers in your example are incorrect.

January 2012 is the start date of investments which lies in FY 11-12 when CII was 785. Your calculations are based on considering FY 12-13 CII i.e 852.

Actual tax adjusted returns by considering FY11-12 as start year are even better i.e 8.86%.

Please correct if Im missing something here.

hello

Could you also pl. explain sec 112 of the Income tax act applicable to long term debt oriented funds pl

Thanks

Other than long-term debt funds, shall the indexation be applicable for

Short-term,

Ultra short-term

medium term debt funds whose maturity period is less than 3 years.

The portfolio or maturity of the debt fund itself does not matter in taxation. The period for which you hold the fund decides how your capital gains will be taxed. You can hold an ultra-short term fund for more than 3 years and you will get indexation. You can sell a long-term debt fund in less than 3 years and you will pay capital gains tax at your slab rate. At the end of the day, if your sell date is more than 3 years after your buy date for a debt fund, you pay 20% tax with indexation. If your fund sell date is less than 3 years from your buy date, you pay tax at slab rate. What the maturity is of the instruments the fund holds is immaterial. These two articles will explain it in detail: here and here

Thanks,

Bhavana

Thanks Madam for such useful and yet simple to understand article .

My query is : How to calculate the capital gain and taxation in debt fund when multiple purchase and sell have been done at multiple point of time ?

Regards

D Prasoon

Fundsindia A/C Holder since 6 years

Thanks Prasoon! The capital gains and whether it is short-term or long-term is calculated based on the first-in-first-out logic – it is assumed that the first unit you sold is the first unit you bought. Here is a blog post on calculating capital gains holding period on multiple purchases and sale:https://blog.fundsindia.com/blog/mutual-funds/fundsindia-explains-how-are-mutual-funds-taxed-part-ii/9153. This should make it clear.

–

Bhavana

I want to invest Lumpsum amount in one debt mutual fund since the returns are a bit higher than the Bank FD . Can you plzz tell that is it the right time to invest or should I wait . What are the things to be noted b4 investing in Debt Mutual Funds.

Hi Raj,

Debt funds generally do provide returns higher than FDs. If you hold them for more than three years, they also have better tax treatment than FDs (it becomes long-term and thus capital gains are taxed at 20% with indexation benefit). You can always invest in debt funds at any time. Even if the interest rate cycle is now turning down, it will also affect FD returns.

The type of debt fund you invest in will depend on your time horizon. If it is less than 1 year, then go for ultra-short term funds. If its 1-2 years, then go for short-term funds. For a longer period, go for long-term debt funds (both dynamic bond funds and income accrual funds). You can read all about debt funds on these two links:https://blog.fundsindia.com/blog/general/fundsindia-explains-what-are-debt-funds/8982 and https://blog.fundsindia.com/blog/general/fundsindia-explains-how-do-debt-funds-deliver-returns/9021

Next, it depends on your level of risk and how much volatility in your returns you can take. Depending on that, you can choose the correct fund category. For example, if you cannot take risk, then don’t go for funds that have bonds that are low-rated. Similarly, dynamic bond funds will see returns move more than income accrual funds. Hope this helps.

Thanks,

Bhavana

Other than long-term debt funds, shall the indexation be applicable for

Short-term,

Ultra short-term

medium term debt funds whose maturity period is less than 3 years.

The portfolio or maturity of the debt fund itself does not matter in taxation. The period for which you hold the fund decides how your capital gains will be taxed. You can hold an ultra-short term fund for more than 3 years and you will get indexation. You can sell a long-term debt fund in less than 3 years and you will pay capital gains tax at your slab rate. At the end of the day, if your sell date is more than 3 years after your buy date for a debt fund, you pay 20% tax with indexation. If your fund sell date is less than 3 years from your buy date, you pay tax at slab rate. What the maturity is of the instruments the fund holds is immaterial. These two articles will explain it in detail: here and here

Thanks,

Bhavana

Hi Bhavana,

I tried posting this from normal comments section as well but it is still in moderation, hence posting from facebook.

I think numbers in your example are incorrect.

January 2012 is the start date of investments which lies in FY 11-12 when CII was 785. Your calculations are based on considering FY 12-13 CII i.e 852.

Actual tax adjusted returns by considering FY11-12 as start year are even better i.e 8.86%.

Please correct if Im missing something here.

hello

Could you also pl. explain sec 112 of the Income tax act applicable to long term debt oriented funds pl

Thanks

Hi Guys,

Could you double check your numbers.

Purchase date is Jan ’12 which implies financial year 11-12.

Thus the CII for purchase date should be 785 and not 852 (Going by your shared link http://ow.ly/g4qa300mQpo)

=> Indexed cost = 1,00,000*1081/785=1,37,707

=> Taxable amount = 1,41,158 – 1,37,707 = 3451

=> Tax: 20% of 3451 = 690

=> Net take away amount = 1,41,158 – 690 = 1,40,467

=> Tax adjusted return = 8.86 %

Apologies for the error.

Hi Harshit, thanks for bringing it to our notice. We have made the necessary changes accordingly.