TVS Motor Company Ltd. – Shaping Tomorrow’s Mobility, Today

TVS Motor Company Limited, incorporated in 1992 and headquartered in Chennai, is a mobility solutions provider, with operations spanning over 90 countries across Asia, Africa, Latin America, and Europe. The company manufactures a diversified portfolio of motorcycles, scooters, mopeds, and three-wheelers across internal combustion and electric platforms, supported by 5 manufacturing facilities located in India, Indonesia, and the UK. In FY25, TVS Motor sold 4.7 million vehicles globally, making it the fourth-largest two-wheeler manufacturer worldwide. The company’s integrated business model is supported by a pan-India distribution network of over 3,800 touchpoints, and a growing international manufacturing and distribution footprint.

Products and Services

Products offered by the company includes motorcycles & scooters (including electric 2W), 3 wheelers (including electric 3W), mopeds. It is also in the business of providing finance via its retail finance arm TVS Credit Services. Its key brands include Apache, Ronin, Raider, Jupiter, NTorq and Zest, catering to a wide range of customer segments and price points.

Subsidiaries – As of FY25, the company has 24 subsidiaries and 4 associate companies.

Investment Rationale

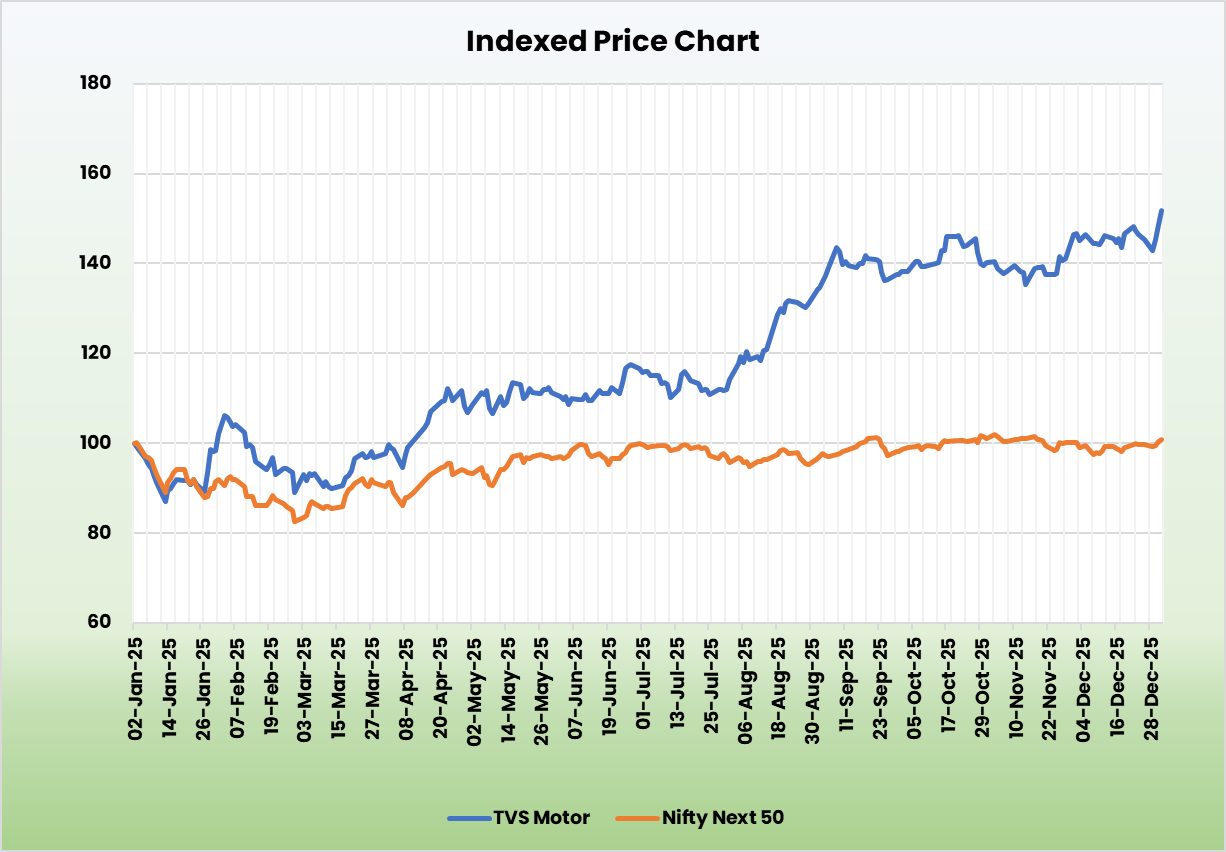

- International Business Driving Consistent Share Gains and Earnings Diversification – The company’s international business continues to scale steadily, with export volumes and revenues growing ahead of industry trends. In Q2FY26, international sales grew 31% versus industry growth of 26%, reflecting sustained market share gains across key geographies. Export volumes crossed 4 lakh units in the quarter, indicating improving scale and operating leverage. Growth in Africa and Latin America remains strong, supported by portfolio strength and expanding distribution, while Asian markets such as Sri Lanka and Nepal are witnessing a gradual recovery. The establishment of a Dubai office strengthens execution capabilities by bringing decision-making closer to key markets. Over time, rising export contribution is expected to improve geographic diversification and reduce dependence on domestic demand cycles.

- EV Portfolio Expansion Enhancing Long-Term Growth Visibility – The company is accelerating its EV strategy with a clear focus on scale and portfolio breadth. EV sales reached a quarterly peak, led by the iQube, which has crossed 700,000 cumulative domestic units, reinforcing its position as a leading electric scooter platform. New launches such as the Orbiter and King Kargo HD EV expand the addressable market across personal and commercial mobility. The company has already achieved ~11% market share in the EV three-wheeler segment, positioning it well as adoption increases. While rare-earth magnet availability remains a near-term constraint, management is pursuing alternative sourcing and technology options.

- Market Share Gains Supported by Volume Growth and Portfolio Premiumisation – The company continues to outperform the domestic industry on volumes, with ICE two-wheeler growth of 21% versus industry growth of 8% in Q2FY26. Market share gains are being driven by a diversified product portfolio spanning mass, executive and premium segments. Strong performance of brands such as Apache, Ntorq, Jupiter and Raider support both volumes and product mix improvement. The planned launch of Norton motorcycles from FY27 adds a long-term premium growth lever, albeit with a gradual ramp-up. Portfolio premiumisation, combined with scale benefits, is expected to support margin expansion over the medium term while sustaining market share momentum.

- Q2FY26 – During the quarter, the company’s sales volume grew by 23%. The company generated revenue of Rs.14,051 crore, which is an increase of 24% compared to Q2FY25. EBITDA grew by 30% YoY to Rs.2,110 crore. The company reported net profit of Rs.833 crore which is an increase of 42% compared to the corresponding quarter of the previous year.

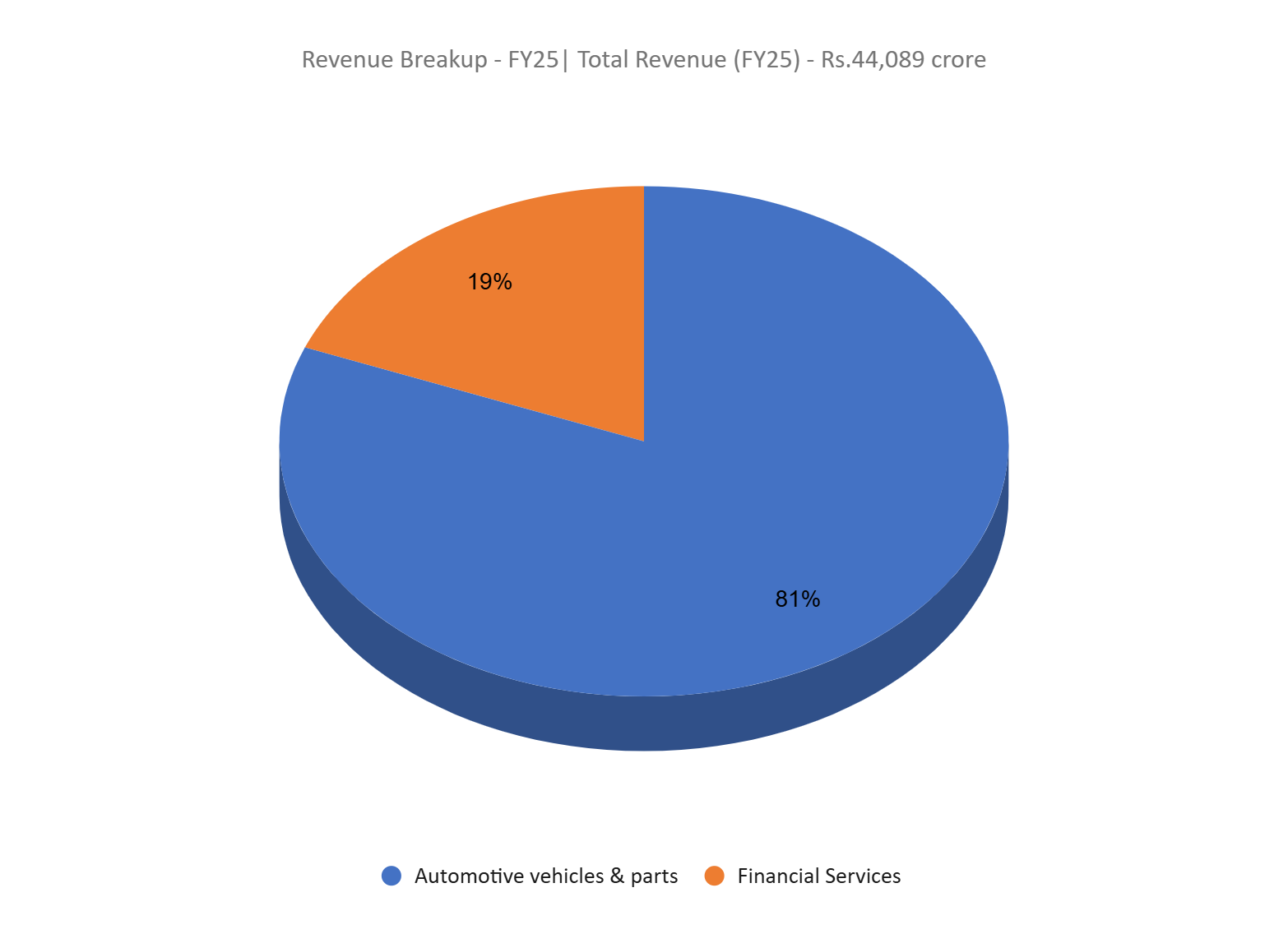

- FY25 – The company generated revenue of Rs.44,089 crore, an increase of 14% compared to FY24 revenue. Operating profit is at Rs.6,575 crore, up by 21% YoY. The company posted net profit of Rs.2,380 crore, a jump of 34% YoY.

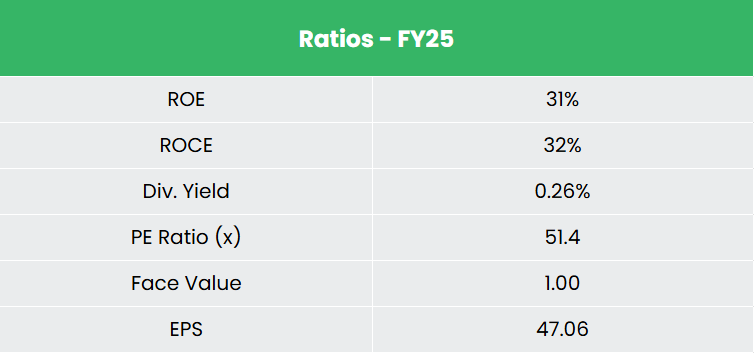

- Financial Performance – The company has generated a revenue and net profit CAGR of 22% and 41% over the period of 3 years (FY23-25). Average 3-year ROE & ROCE is around 27% and 14% for FY23-25 period. The company has a debt-to-equity ratio of 2.08.

Industry

The Indian automobile industry is one of the largest and fastest-growing globally, contributing nearly 6% to India’s GDP and employing over 37 million people directly and indirectly. India is currently the third-largest automobile market globally, with total vehicle sales reaching 25.6 million units in FY25, driven by strong demand across two-wheelers, passenger vehicles, and commercial vehicles. The industry comprises four key segments – two-wheelers, three-wheelers, passenger vehicles, and commercial vehicles with two-wheelers accounting for nearly 76% of total domestic volumes, reflecting India’s preference for affordable personal mobility. India has also emerged as a global manufacturing hub, supported by a strong supplier ecosystem, competitive cost structures, and favourable demographics. The country is now the largest producer of two-wheelers and three-wheelers globally, and a major exporter to emerging markets across Asia, Africa, and Latin America.

Growth Drivers

- The Centre has launched the PM E-DRIVE scheme with a budget of US$ 1.30 billion (Rs. 10,900 crore), effective from October 1, 2024, to March 31, 2026. The initiative aims to accelerate the adoption of Electric Vehicles (EVs), establish charging infrastructure, and develop an EV manufacturing ecosystem in India.

- The automobile sector allows 100% FDI under the automatic route, supported by PLI schemes, EV incentives, and localisation policies that accelerate capacity expansion and technology adoption.

- India’s cost competitiveness and strong supplier ecosystem are driving rising exports, positioning the country as a global hub for two-wheelers and compact vehicles.

Peer Analysis

Competitors: Bajaj Auto Ltd & Hero MotoCorp Ltd, etc.

The company is generating stable return ratios in line with the growth in the sales. This indicates the company’s ability to generate better profits for the capital invested.

Outlook

The company has delivered consistent volume growth across segments, reflecting strong product acceptance and effective execution. We expect medium to long term demand for two-wheelers to remain supportive, aided by improving affordability and higher demand. Backed by robust R&D capabilities, a steady pipeline of new launches and disciplined execution, the company is well positioned to sustain operational momentum. Its expanding product portfolio should continue to support market share gains. Strategic expansion into select international markets has progressed well and is increasingly contributing to growth and diversification. Overall, we expect the company to deliver steady operational and financial performance over the medium term.

Valuations

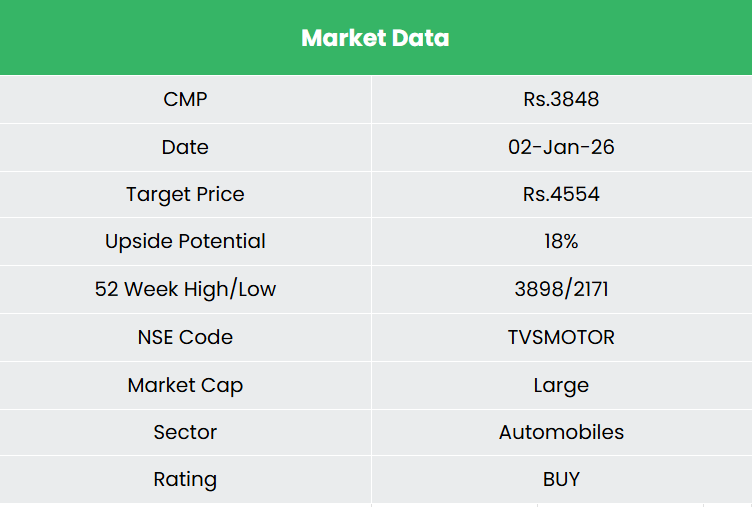

We view the company as an attractive investment, supported by its sustained outperformance versus the industry, strong revenue and profit growth, and a clear strategic focus on EV leadership alongside expansion into higher-margin premium segments. We recommend a BUY rating in the stock with the target price (TP) of Rs.4,554, 47x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

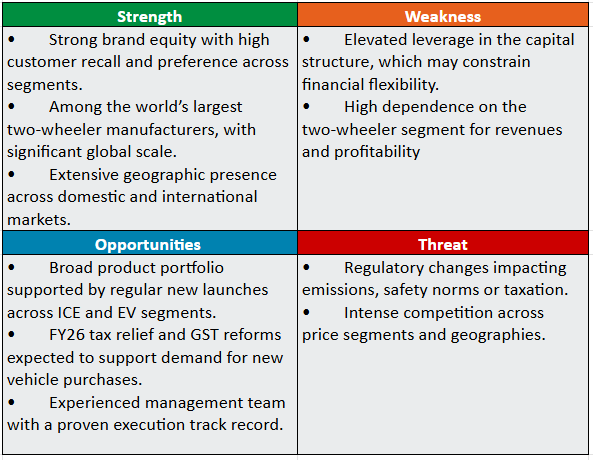

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.