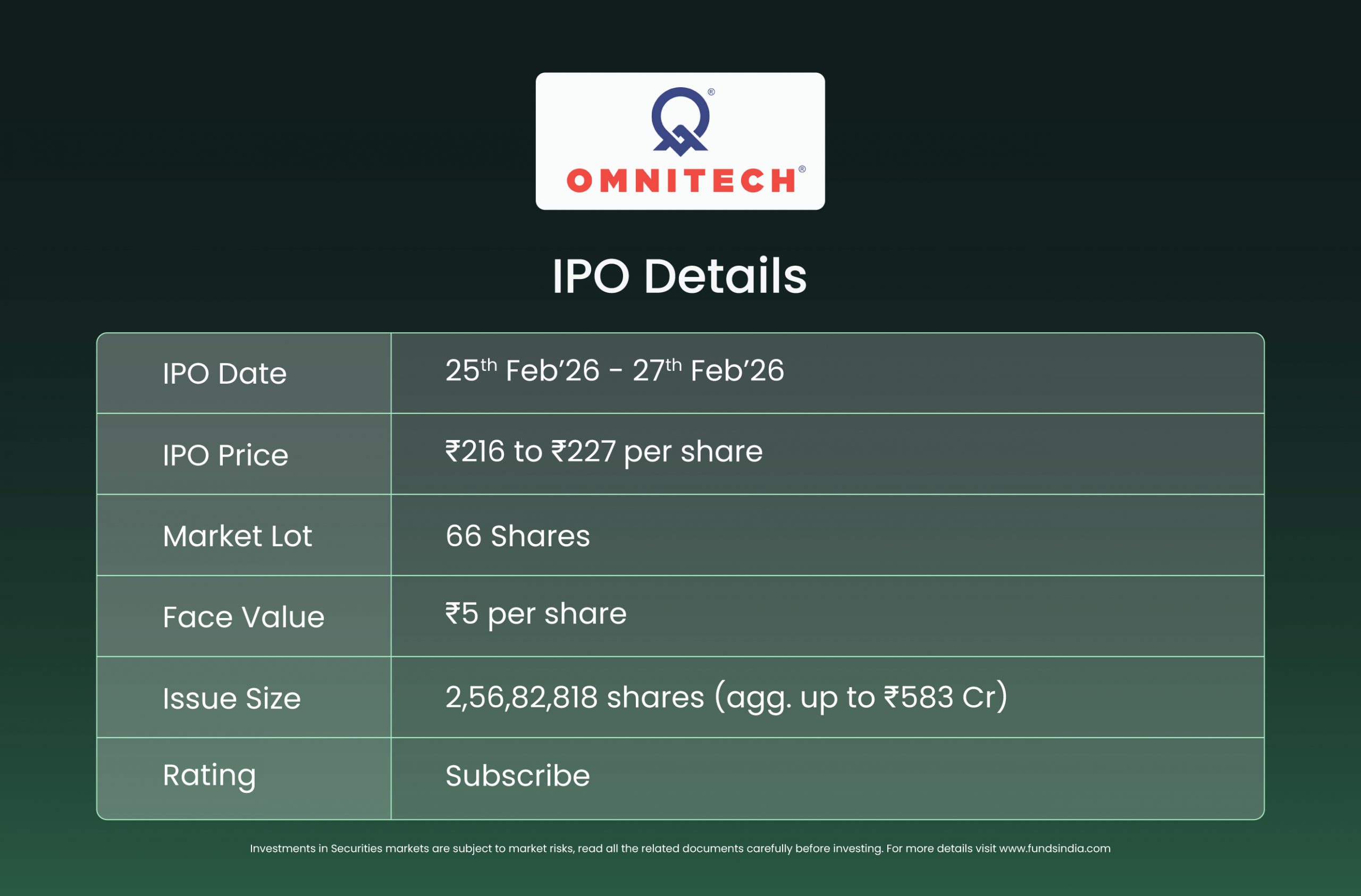

Company Overview

Omnitech Engineering Limited is a manufacturer of high-precision engineered components and assemblies supplied to original equipment manufacturers (OEMs) across energy, industrial equipment, and motion control and automation sectors. The company operates a build-to-specification manufacturing model, producing customised machined components and assemblies for integration into industrial machinery and safety-critical applications. As of September 30, 2025, the company had serviced over 256 customers across 24 countries, primarily serving customers in North America and Europe.

Objects of the offer

The company is carrying out a book-built issue of Equity Shares of face value of Rs. 5 each aggregating up to Rs. 583 crore, comprising a Fresh Issue aggregating up to Rs. 418 crore by the Company and an Offer for Sale aggregating up to Rs. 165 crore by the Selling Shareholders.

The proceeds of the fresh issue are to be utilized towards the following objects:

- Repayment and / or pre-payment, in full or in part, of certain outstanding borrowings of the company.

- Setting up new manufacturing facilities in Rajkot, Gujarat

- Funding capital expenditure towards installation of rooftop solar panels and purchase of equipment and machinery at existing manufacturing facilities.

- General corporate purposes.

Investment Rationale

- Customer stickiness driven by qualification-intensive outsourcing model – Omnitech operates within precision engineered components manufacturing, where supplier onboarding involves lengthy qualification and validation processes before commercial supply begins. The company holds industry certifications including API Spec Q1, API 7-1 and API 5CT, enabling supply of components used in safety-critical energy applications and forming a key prerequisite for vendor approval by global OEM customers. This creates structurally sticky customer relationships once approvals are secured. Repeat customers contributed 96.87% of revenue for the six months ended September 30, 2025, reflecting continued order flow from established OEM relationships. The company has supplied products to over 256 customers across 24 countries, primarily servicing global OEMs in energy and industrial equipment applications, where switching suppliers typically requires requalification and operational revalidation, supporting continuity of demand.

- Export-driven revenue profile linked to global industrial capex cycles – The company derives a majority of its revenue from exports (~79% of revenue was derived from outside India in H1FY26), linking performance to global industrial and energy capital expenditure cycles rather than domestic demand conditions. The global precision engineered goods market was valued at USD 269.1 billion in CY2024 and is expected to grow at a 9.9% CAGR during CY2025–CY2028. Participation in global OEM supply chains positions the company to benefit from ongoing outsourcing trends for specialised precision manufacturing capabilities, and supply chain diversification initiatives (China +1).

- Large order book providing revenue visibility – As of September 30, 2025, the company reported an order book of Rs. 1,764.7 crore, representing approximately 551% of annualised revenue. The order book is predominantly driven by the energy segment (74%), followed by industrial equipment systems (21%) and motion control and automation (3.7%). Exposure to long-cycle industrial and energy equipment programs provides forward visibility, as production schedules and procurement timelines typically extend across multiple reporting periods.

- Operational scale and utilisation – Omnitech’s operational profile reflects established execution capability supported by scaled manufacturing infrastructure and stable capacity utilisation. As of September 30, 2025, the company operated three manufacturing facilities with annualised machining capacity of 24,29,856 machine hours, operating at utilisation of ~73% during H1FY26, and an annualized fabrication capacity of 7,200MTPA. The operational base is supported by a workforce of 1,807 employees, including dedicated production and quality teams, enabling end-to-end execution across machining, fabrication, assembly and testing processes.

- Financial Performance – The company reported consolidated revenue from operations of Rs. 342.9 crore in FY25, reflecting a 92.45% YoY increase from Rs. 178.1 crore in FY24. EBITDA stood at Rs. 117.6 crore in FY25, with an EBITDA margin of 34.31%, compared with Rs. 64.9 crore (36.44% margin) in FY24, representing an 81.2% YoY growth. Profit after tax (PAT) for FY25 was Rs. 43.9 crore, increasing 131.9% YoY from Rs. 18.9 crore in FY24. PAT margin expanded 215 bps to 12.54% in FY25. For H1FY26, the company recorded revenue from operations of Rs. 228 crore, EBITDA of Rs. 70.1 crore, and PAT of Rs. 27.8 crore, with EBITDA margin and PAT margin at 30.72% and 11.74%, respectively.

Key Risks

- Working capital intensive operations and cash flow dependence – The company operates a working capital-intensive business model, with net working capital days at ~282 days in FY25, driven by elevated inventory and receivable cycles typical of precision engineering outsourcing. Long production lead times, extended credit terms, and relatively lower bargaining power with suppliers, result in a prolonged cash conversion cycle where the company effectively finances both production and customer credit simultaneously. The elevated working capital requirement represents a structural feature of the business model, and sustained growth may therefore require continued reliance on prudent working capital management, and external working capital financing.

- Customer concentration risk – The company derives a significant portion of its revenue from a concentrated customer base, with the top 10 customers contributing between ~48% and ~69% of revenue across recent periods. The business model relies on long-term supply relationships with global OEM customers, and while qualification processes create switching costs, dependence on a limited number of customers exposes the company to demand volatility in the event of order reductions, program delays or loss of key customer relationships.

- Operational execution risk linked to customised manufacturing model – The company operates under a build-to-specification manufacturing model, where production is undertaken against customer-specific designs and revenue recognition depends on successful execution, inspection and customer acceptance. Components are often used in safety-critical applications requiring stringent quality validation and adherence to precise specifications. Delays in manufacturing, quality deviations or extended customer approval cycles may defer revenue recognition and lengthen working capital cycles. Given the customised nature of production, inventory and work-in-progress may have limited alternate use.

Outlook

The company’s outlook is supported by a strong order pipeline, ongoing capacity expansion and sustained demand from global OEM customers, with positioning in safety-critical applications and certification-led entry barriers supporting continuity of orders. Growth will depend on successful execution across customised manufacturing programs and effective absorption of incremental capacity. While the business carries structurally high working capital requirements and execution dependence inherent to precision engineering outsourcing, these reflect operating characteristics of the model rather than structural weaknesses, with performance contingent on disciplined working capital management and consistent delivery execution as scale increases.

According to the RHP, the company’s listed peers are PTC Industries Ltd, MTAR Technologies Ltd, Dynamatic Technologies Ltd, and Azad Engineering Ltd, among others. The peer group is trading at an average P/E of 184.9x, with the highest being 428.48x, and the lowest being 56.68x. At the upper price band, the listing market capitalization of Omnitech will be Rs. ~2,807 crore, and the company is demanding a P/E of ~63.94x, based on the post issue market capitalization and FY25 diluted EPS. When compared to its peers, the issue seems to be fairly valued. Based on the above views, we provide a ‘Subscribe’ rating for this IPO.

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.