Va Tech Wabag Ltd. – Global Water Solutions Provider

Incorporated in 1995 and headquartered in Chennai, VA Tech Wabag Limited (WABAG) is a pure-play Indian multinational company focused exclusively on water and wastewater treatment. The company operates in over 25 countries across 4 continents and is recognised among the world’s top three private water operators and the third-largest desalination player globally. Since inception, WABAG has executed more than 1,500 plants (over 6,500 installations globally across legacy operations), supported by 125+ in-house proprietary technologies and dedicated R&D centres in Europe and India, reinforcing its position as a technology-driven global water solutions leader.

Products and Services

WABAG offers end-to-end water and wastewater management solutions across the entire lifecycle from project development and EPC execution to long-term O&M. The company’s offerings spans drinking water treatment, desalination, wastewater treatment, recycle & reuse, effluent treatment, ZLD, sludge treatment & energy recovery.

Subsidiaries: As of FY25, the company has 15 subsidiaries and 2 associate companies.

Investment Rationale

- Capturing the Water Demand from New Age Industries – Beyond its core municipal portfolio, WABAG is strategically aligning with India’s next capex wave across solar PV, green hydrogen, semiconductors, data centres and bio-energy sectors that are inherently water-intensive and require high-purity, reliable and recyclable water solutions. Solar cell and semiconductor manufacturing depend on ultra-pure water (UPW) for wafer cleaning and process stability; green hydrogen requires demineralised and desalinated water as feedstock; while data centres demand large volumes of treated water for cooling with increasing regulatory emphasis on reuse. WABAG’s breakthrough UPW order from RenewSys Solar and the Rs.1,000 crore 100 MLD desalination project for Indosol Solar Private Limited demonstrate proven execution capability across desalination, tertiary RO, effluent treatment and ZLD systems. With India targeting 130 GW solar manufacturing and accelerating hydrogen and semiconductor investments, incremental demand for 100 – 150 MLD of high-purity and recycled water capacity is likely to materialise over the medium term. WABAG’s proven expertise coupled with ongoing engagements and advanced bidding discussions with hydrogen developers, semiconductor fabs and data centre operators positions it as a preferred technology partner rather than a commoditised EPC contractor. These segments offer higher technical entry barriers, recurring O&M potential and superior margin profile, providing a multi-year growth runway and potential valuation re-rating as the company transitions from municipal EPC to a high-value industrial water solutions platform.

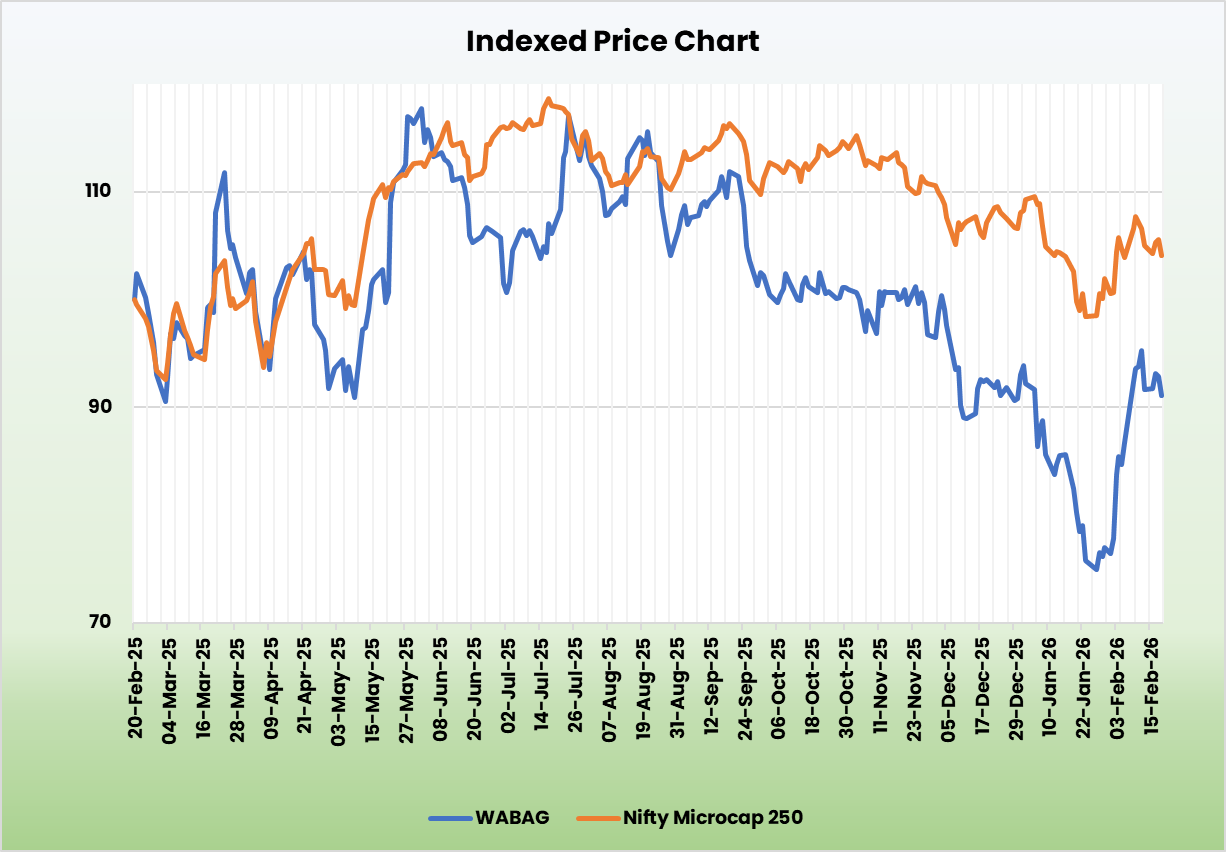

- Robust Order Book with Strong International Diversification – WABAG ended Q3FY26 with a robust order book of Rs.163 billion, offering strong multi-year revenue visibility with a balanced mix of 64% EPC and 36% O&M, supporting both execution growth and annuity stability. International projects contribute ~50% of revenue (YTD) and order backlog, underscoring geographic diversification. The company continues to consolidate its Middle East leadership with the 300 MLD SWA desalination mega project at Yanbu Al-Bahr, KSA, a 50 MLD BWRO plant in Saudi Arabia and preferred bidder status for the Hadda ISTP project. It also secured an ADB-funded DBO order from the Melamchi Water Supply Development Board, Nepal, strengthening its South Asia presence. Multilateral-funded projects such as the JICA-backed 400 MLD Perur desalination plant in Chennai and World Bank/AIIB-supported projects in Bangladesh and Bengaluru enhance counterparty quality. With Rs.1,200 crore order intake in Q3, improved working capital days and debt reduction, WABAG reflects disciplined execution alongside scale expansion.

- Q3FY6 – During the quarter, the company reported consolidated revenue from operations of Rs.961 crore, up 18.5% YoY compared to Rs.811 crore in Q3FY25. EBITDA increased 24.6% YoY to Rs.131 crore from Rs.105 crore, with EBITDA margin improving to 13.6% versus 13.0% in the corresponding quarter last year. Consolidated net profit stood at Rs.92 crore, registering a 30.6% YoY growth from Rs.70 crore in Q3FY25.

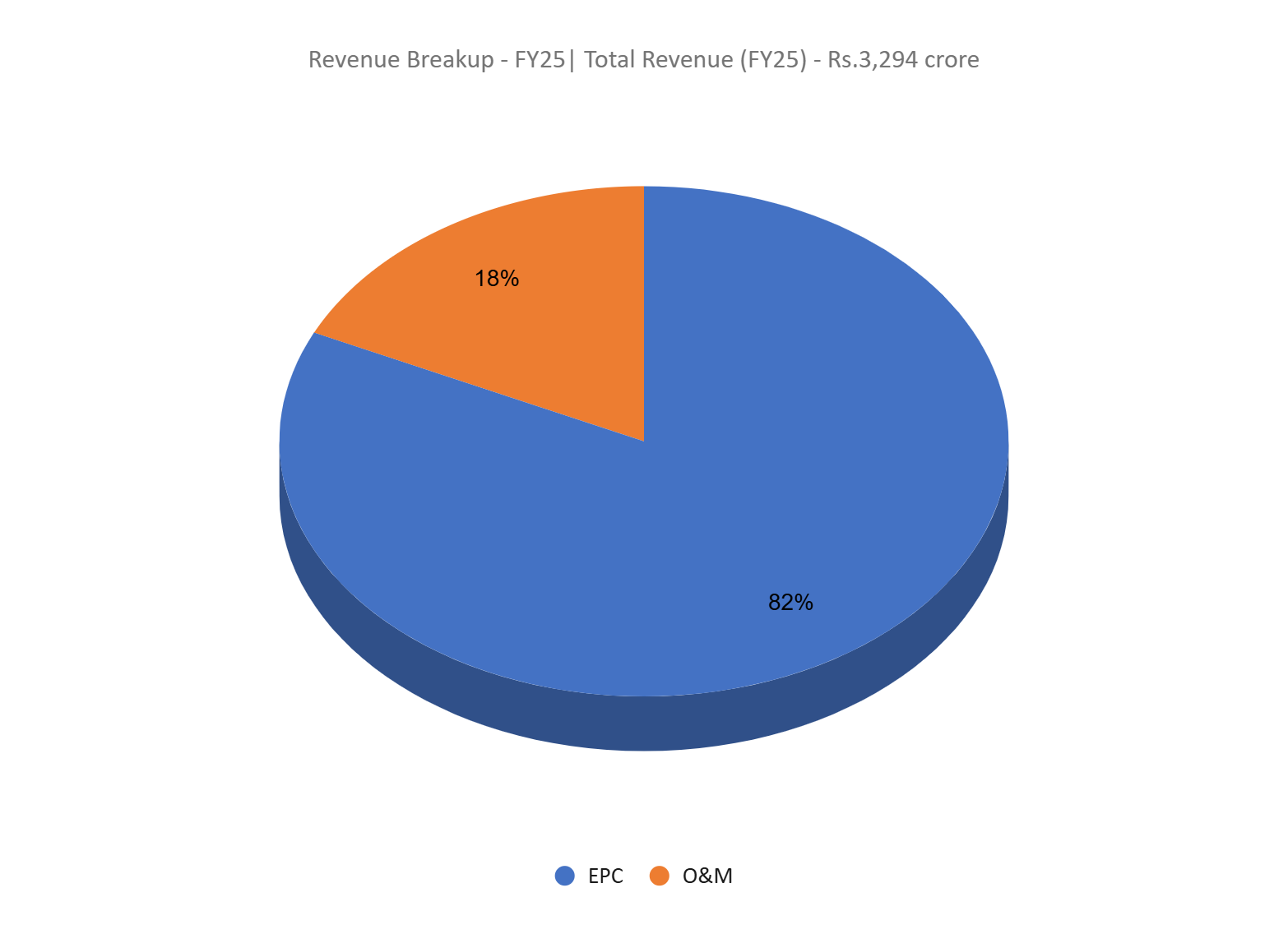

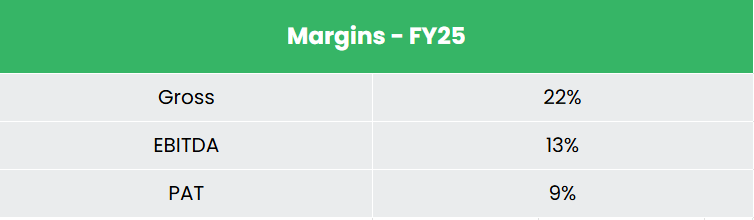

- FY25 – During FY25, the company reported a revenue of Rs.3,294 crore, representing a 15% YoY increase compared to Rs.2,856 crore in FY24. EBITDA stood at Rs.430 crore, up ~14% YoY from Rs.377 crore in the previous year, and net profit was recorded at Rs.295 crore, registering an ~18% YoY growth over Rs.250 crore in FY24.

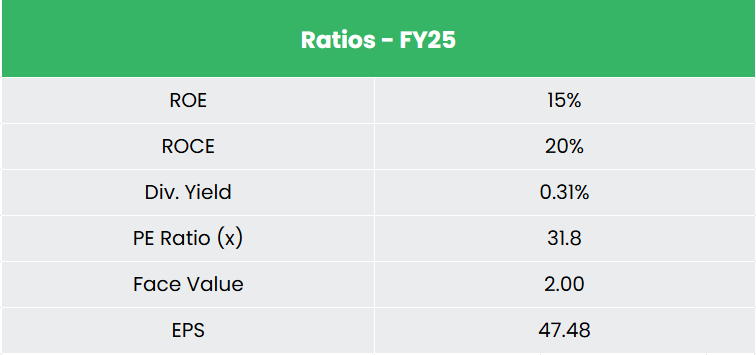

- Financial Performance – The 3-year revenue and net profit CAGR stands at 3% and 32% respectively between FY23-25. Notably, the TTM revenue growth has materially improved to 20%. The company has a debt-to-equity ratio of 0.1, and the 3-year average ROE and ROCE are around 11% and 20% for FY23-25 period.

Industry

The global water treatment industry is witnessing steady structural growth, driven by rising water scarcity, urbanisation and tightening environmental regulations. The global water and wastewater treatment market was valued at approximately US$ 347.9 billion in 2024 and is projected to reach US$ 623.2 billion by 2034, implying a CAGR of ~7.6%, supported by increasing investments in wastewater management, desalination and water reuse infrastructure. Regionally, Asia-Pacific remains the fastest-growing market, expected to expand from US$ 125.6 billion in 2024 to US$ 282.8 billion by 2034 (8.5% CAGR), driven by rapid industrialisation and urban infrastructure investments. Government-led spending continues to underpin demand, including India’s water sector allocation of Rs.99,500 crore and Africa’s Water Investment Action Plan targeting US$30 billion annual investments by 2030, highlighting strong long-term growth visibility for water treatment solution providers.

Growth Drivers

- Policy-led infrastructure spending – Large government programmes such as National Mission for Clean Ganga, AMRUT, AMRUT 2.0, Jal Jeevan Mission and Swacch Bharat Mission and global water security investments are driving sustained project pipelines across municipal and industrial segments.

- Water scarcity and climate stress – Climate models predict that nearly two-thirds of the global population could face water stress by 2030, accelerating adoption of desalination and reuse solutions.

- Industrial water demand – Expansion in refining, petrochemicals, semiconductors and energy sectors is increasing demand for effluent treatment and ultrapure water systems.

- Regulatory tightening and sustainability focus – Stricter environmental norms are driving adoption of advanced wastewater treatment and recycling technologies globally.

Peer Analysis

Competitors – Ion Exchange (India) Ltd, Enviro Infra Engineers Ltd, etc.

Compared to peers, WABAG stands out for its superior cash conversion and balance sheet strength, despite delivering moderate return ratios. The company has reported a CFO/PAT (3yr median) of 1.68x, significantly stronger than ION Exchange (0.15x) and Enviro Infra (-0.27x), indicating materially better earnings quality and working capital discipline. Wabag also maintains a low debt-to-equity ratio of 0.10x, among the lowest in the peer set, supporting liquidity and reducing execution risk inherent in EPC businesses.

Outlook

WABAG is targeting a calibrated expansion in international markets, with a clear strategic focus on the Middle East, Africa, CIS, Southeast Asia and South Asia, where desalination and water reuse demand remains structurally strong. The company continues to follow an asset-light engineering-led model, supporting superior cash generation and healthy return ratios. With EBITDA margins sustaining within the guided 13–15% range and revenue growth of ~18% aligning with medium-term guidance, operational momentum remains intact. A strong liquidity position gross cash of Rs.1,080 crore and net cash of Rs.891 crore as of December 2025 provides flexibility to pursue large and complex projects. Backed by a diversified order book, improving working capital efficiency and strong international tender pipeline, WABAG remains well positioned to deliver steady growth with disciplined capital allocation.

Valuations

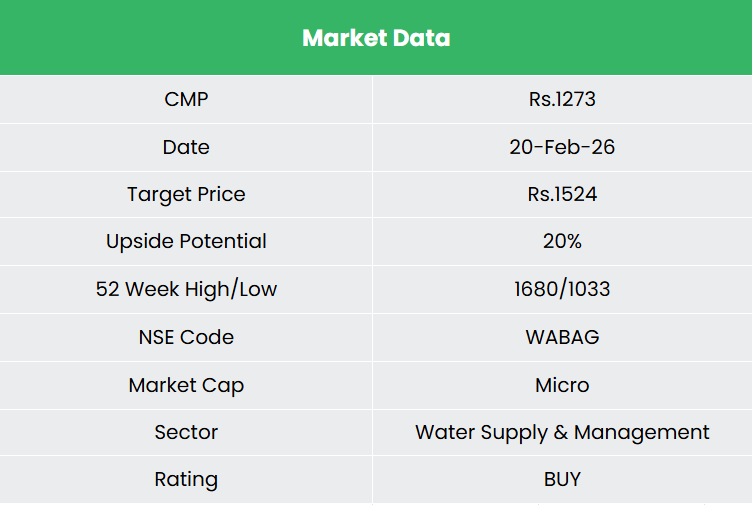

At current levels, we believe the stock offers a compelling play on a globally diversified, asset-light water infrastructure platform with improving margins, strong cash position and multi-year revenue visibility. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,524, 20x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

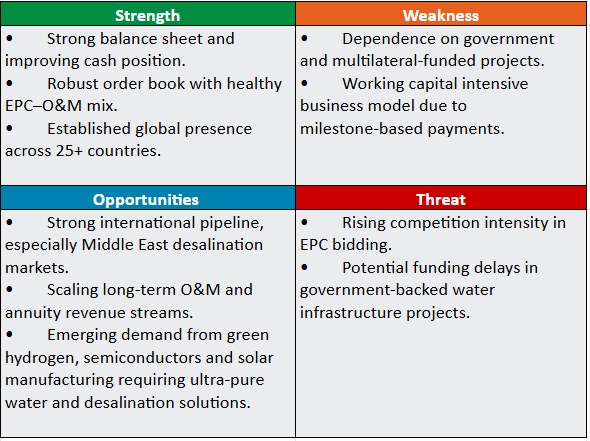

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.