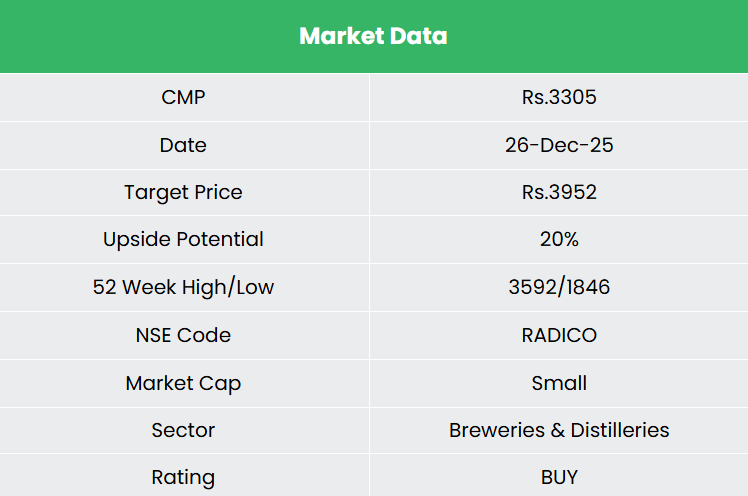

Radico Khaitan Ltd – Spirit of Excellence

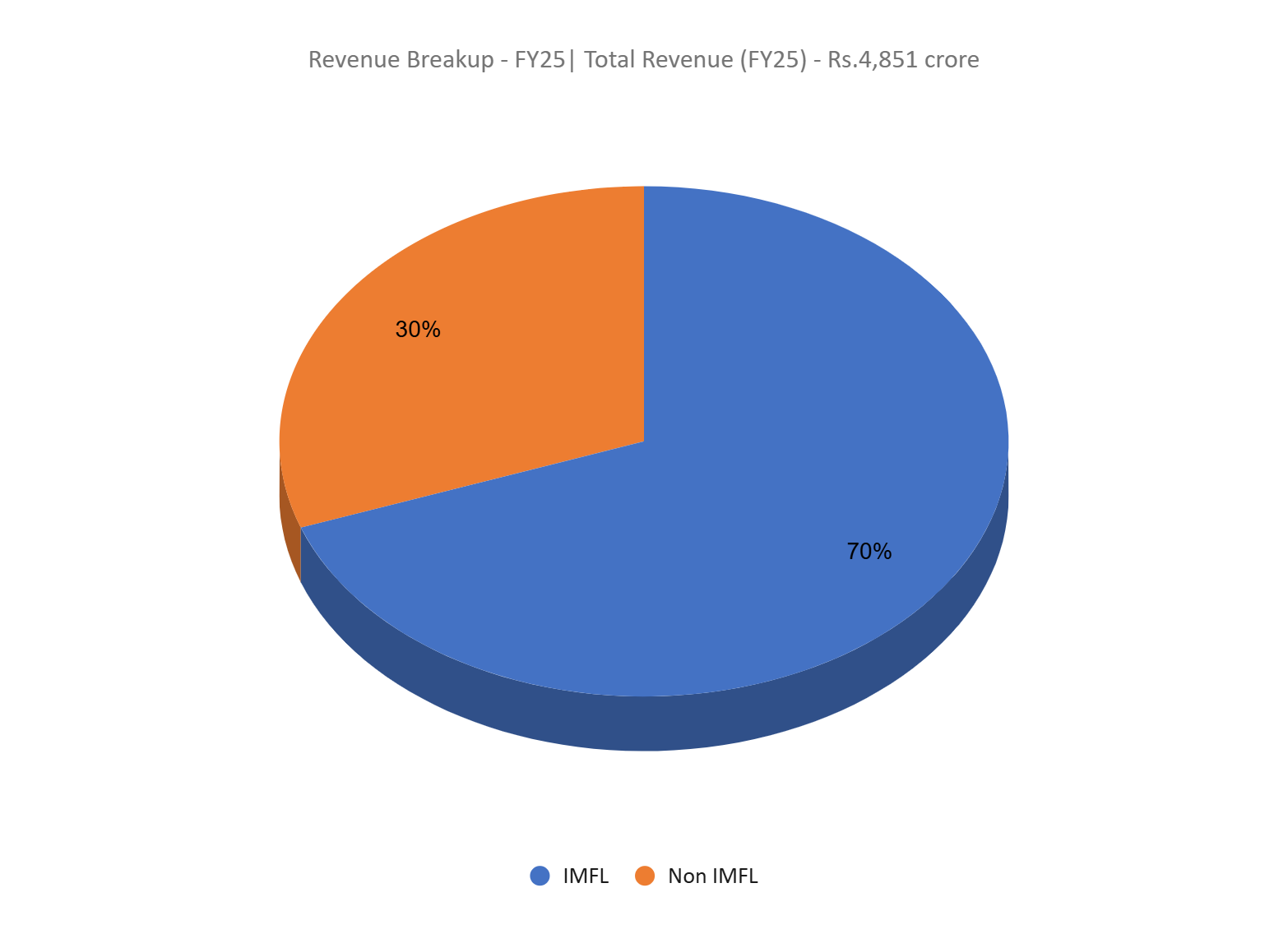

Radico Khaitan Limited, incorporated in 1943 and headquartered in New Delhi, is one of India’s largest Indian Made Foreign Liquor (IMFL) companies, operating 8 distilleries with an aggregate production capacity of 321 million litres per annum across molasses-based, grain-based, and malt-based spirits, supported by 44 bottling units (5 owned, 39 contract and royalty) strategically located pan-India to minimise interstate taxes and logistics costs. The company’s portfolio spans whisky, brandy, rum, vodka, gin, and liqueurs across luxury, premium, and regular price segments, with a focused premiumisation strategy driving 8 brands into the global millionaires’ club (>1 million cases annually). The company distributes through over 100,000 retail outlets and 10,000 on-premises locations across India, and exports to over 100 countries with presence in 35+ travel retail locations globally.

Products and Services

The company’s portfolio includes a range of award-winning spirits across whisky, vodka, gin, brandy, rum and liqueurs, anchored by established mass brands and a growing premium offering. Notable brands include 8PM Whisky, Magic Moments Vodka, Rampur Indian Single Malt Whisky, Sangam World Malt Whisky, and Jaisalmer Indian Craft Gin.

Subsidiaries – As of FY25, the company has 8 subsidiaries and 1 joint venture.

Investment Rationale

- Premium Mix Expansion Strengthens Earnings Quality – Premiumisation remains the key growth and value driver for Radico Khaitan, supported by a favourable demand environment marked by a strong festive season, improving on-trade consumption and rising preference for premium and craft spirits. The Prestige & Above (P&A) portfolio continues to outperform, delivering 15.5% volume growth in FY25 and accounting for 46% of IMFL volumes and 69.4% of IMFL value, underscoring a structurally improving mix. Importantly, management has maintained firm pricing discipline across categories, indicating confidence in brand strength and demand elasticity. Momentum remains visible at the brand level, with Magic Moments Vodka crossing 7 million cases and retaining ~60% market share, while After Dark Whisky scaled to 1.9 million cases, aided by successful premium extensions. The introduction of two luxury brands in Q1FY26 and planned entry into the super-premium whisky segment in Q1FY26 further strengthens the premium ladder, enhancing margin visibility and reinforcing the investment case around sustained earnings growth driven by mix improvement rather than price-led volume expansion.

- Sitapur Capex Strengthens Supply Security and Margin Expansion – The company has completed a strategic capex cycle aimed at strengthening backward integration and supporting long-term growth in its branded spirits portfolio, led by the commissioning of the 350 KLPD grain-based ENA distillery at Sitapur, now operating at ~95% utilisation. The facility secures long-term ENA supply, reduces dependence on external vendors, and supports the company’s accelerating Prestige & Above (P&A) growth, where grain-based ENA is predominantly used. Alongside the Rampur campus, Sitapur is expected to meet branded business requirements for the next 6–7 years, while expanded packaging and PET bottle capacities further enhance operational efficiency. With the capex cycle largely complete, Radico is well positioned to drive premiumisation-led growth, margin expansion, and stronger cash flow generation, aided by a cost-efficient and sustainable energy mix at Sitapur, where the majority of power is generated through captive agro-waste–based sources.

- New Product Launches Expand Growth Opportunities – Recent product launches further reinforce Radico Khaitan’s premiumisation strategy and earnings quality. The launch of Morpheus Super Premium Whisky in Q1FY26 marks the company’s entry into the fast-growing super-premium whisky segment, a structurally higher-margin category where it previously had limited presence. Priced above peer offerings, the brand has seen encouraging early traction with improving tertiary offtake and positive consumer feedback, and is set to expand from three to 10 states in H2FY26, covering ~70% of the category. The Spirit of Kashmyr, a luxury vodka with Natural and Saffron variants, strengthens Radico’s leadership in vodka by addressing a premium white space historically dominated by imports, and is already present in seven states.

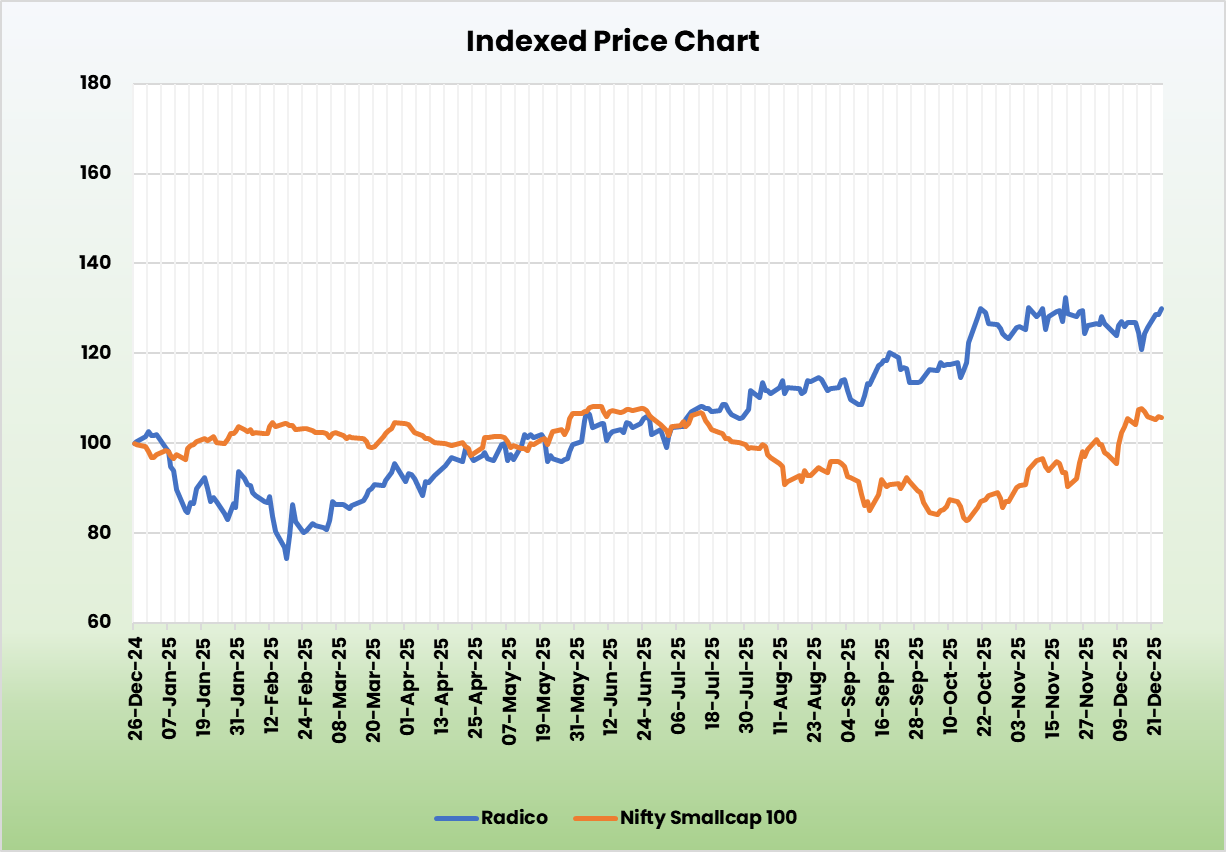

- Q2FY26 – Radico Khaitan delivered a strong Q2FY26, with revenue rising 34% YoY to Rs.1,494 crore, supported by robust volume growth across segments. EBITDA increased 46% YoY to Rs.236 crore, while net profit grew 73% YoY to Rs.140 crore, reflecting operating leverage and favourable mix. The Prestige & Above (P&A) portfolio recorded 22% volume growth and 24% value growth, with realisations improving 2.1% YoY, marking the highest-ever quarterly P&A volumes and reinforcing management’s guidance of sustained double-digit growth in this segment. The regular segment posted a sharp 80% volume rebound, ending a nine-quarter decline, driven by route-to-market changes in Andhra Pradesh. Overall EBITDA margin expanded by 126 bps YoY to 15.8%, underscoring improved operating efficiency and scale benefits.

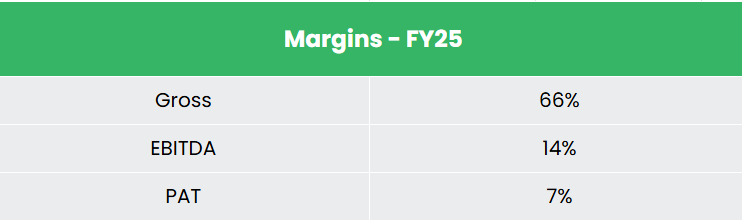

- FY25 – During FY25, the company generated revenue of Rs.4,843 crore, an increase of 18% compared to the FY24 revenue. EBITDA was recorded at Rs.674 crore, up by 33% YoY. The net profit grew by 32% to Rs.346 crore.

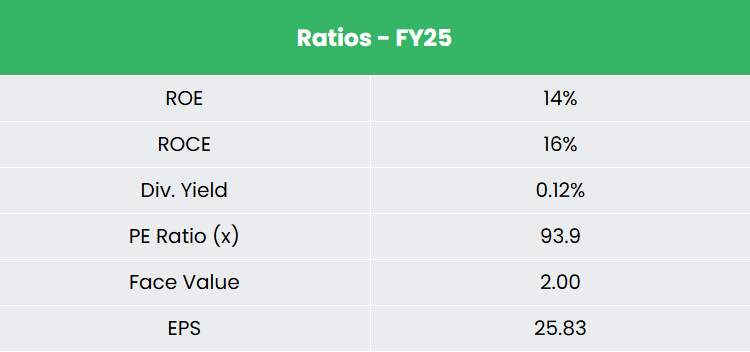

- Financial Performance – The 3-year revenue and net profit CAGR stands at 19% and 10% respectively between FY23-25. Notably, the TTM revenue and net profit growth have improved to 25% and 62%. The 3-year average ROE and ROCE are around 12% and 14% for FY23-25 period. The company has a robust capital structure with a debt-to-equity ratio of 0.21.

Industry

The Indian FMCG sector is one of the fastest-growing segments of the domestic economy, projected to grow at a CAGR of 27.9% from 2021 to 2027, reaching nearly US$ 615.87 billion. Within this, the food and beverage segment accounts for approximately 3% of India’s GDP, while the household and personal care categories continue to witness sustained demand. The FMCG industry provides employment to around 3 million people, accounting for approximately 5% of total factory employment in India. India’s alcoholic beverage (alcobev) industry, a key sub-segment within food and beverages, is projected to record 8–10% revenue growth in FY26, reaching Rs.5,30,000 crore (US$ 61.97 billion), reflecting sustained premiumisation trends and structural demand growth driven by rising disposable incomes and evolving consumer preferences.

Growth Drivers

- India’s FMCG sector is supported by a large, young population, rising disposable incomes, and expanding consumption across urban and rural markets, underpinning steady growth in food, beverages, and personal care.

- Rapid growth in e-commerce and quick commerce, alongside an internet user base expected to surpass 900 million by 2025, is structurally increasing FMCG access, especially for packaged foods and beverages.

- The sector benefits from policy support including 100% FDI allowed in food processing and single-brand retail, alongside targeted schemes such as PLI for food processing that are driving investment and capacity creation.

Peer Analysis

Competitors – United Spirits Ltd, Allied Blenders & Distillers Ltd, etc.

Compared to its peers, the company demonstrates disciplined capital allocation and improving profitability, supported by a growing premium brand portfolio and a focused spirits-led strategy.

Outlook

The company enters FY26 with strong growth visibility, supported by a well-established brand portfolio, improving execution, and consumer-led innovation. With the major capex cycle now complete, the company has sufficient capacity, scale, and integration to support sustained expansion, while management targets strong double-digit growth in the Prestige & Above segment and 20%+ overall volume growth in FY26. Stable ENA and grain pricing expectations, alongside favourable route-to-market changes and policies anticipated in major states, are likely to support profitability, with management guiding to 125–150 bps EBITDA margin expansion. Continued traction in luxury and semi-luxury offerings, with a targeted Rs.500 crore revenue opportunity, is expected to further strengthen earnings quality. Improved cash generation is anticipated to enable a debt-free balance sheet within the next two years, positioning the company for sustained free cash flow generation by FY27.

Valuations

Supported by rising alcohol consumption, a strengthening festive demand cycle, evolving consumer preferences, improving route-to-market dynamics, and a structurally stronger balance sheet, we believe Radico Khaitan presents a compelling investment opportunity at this stage of its growth cycle. We recommend a BUY rating in the stock with the target price (TP) of Rs.3,952, 56x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

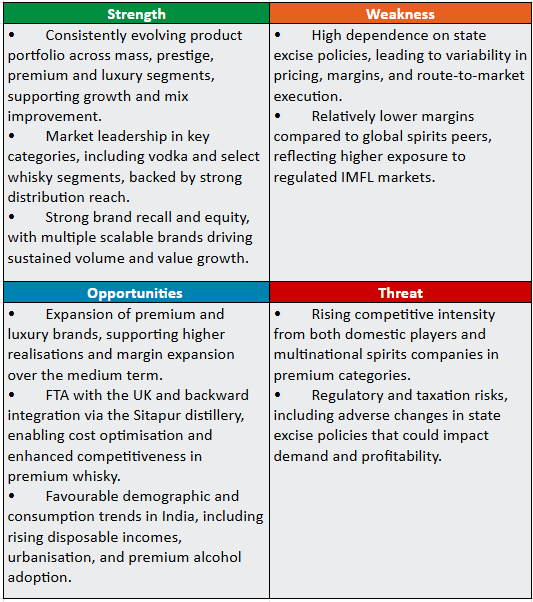

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.