Silver has long been regarded as a store of value, second only to gold in the precious metals hierarchy. But in recent years, silver has moved beyond its traditional role as merely a store of value.

Today, silver plays a dual role: a precious metal and a critical industrial input in sectors such as solar energy, electronics, and electric vehicles. This evolving utility has brought renewed attention to silver as an asset class.

The result? A noticeable rise in silver-focused mutual funds and ETFs, reflecting growing investor interest.

But does silver truly merit a place in your portfolio or is it just a passing trend?

Let’s find out..

The Four Roles of a Core Portfolio Asset

Before adding any asset to your ‘Core Portfolio’, it must serve a clear purpose. Broadly, an asset should deliver on one or more of the following four roles:

- Role 1: Enhance Long Term Returns

- Role 2: Reduce Portfolio Volatility

- Role 3: Act as a Crisis Hedge

- Role 4: Generate Regular Income

Let’s check if Silver delivers on any of these roles

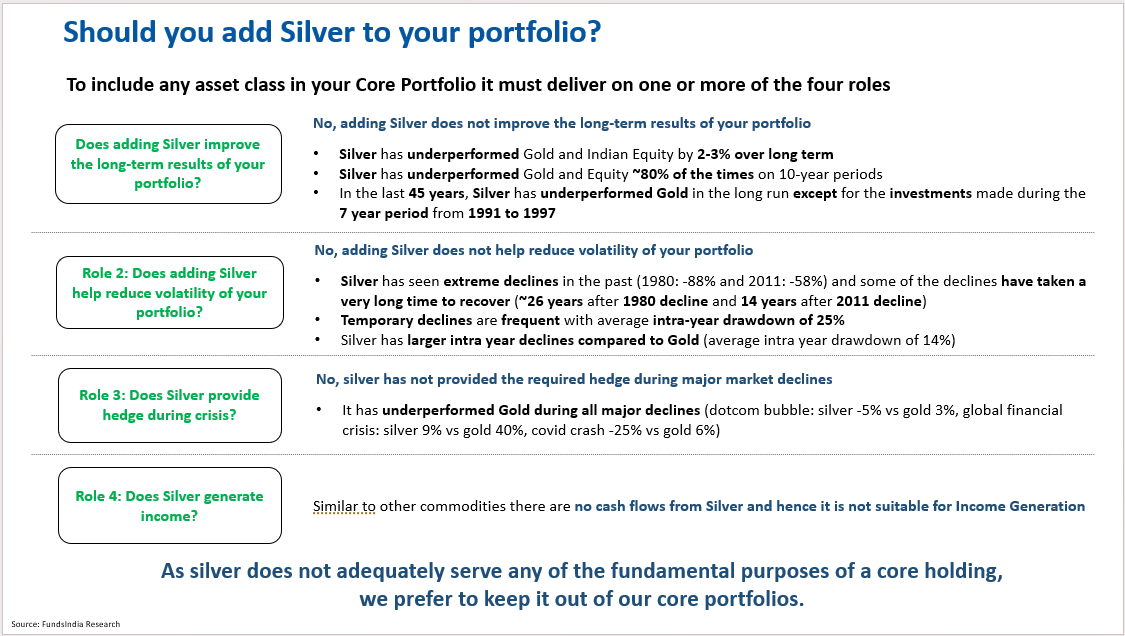

Role 1: Does adding Silver improve the long-term returns of your portfolio?

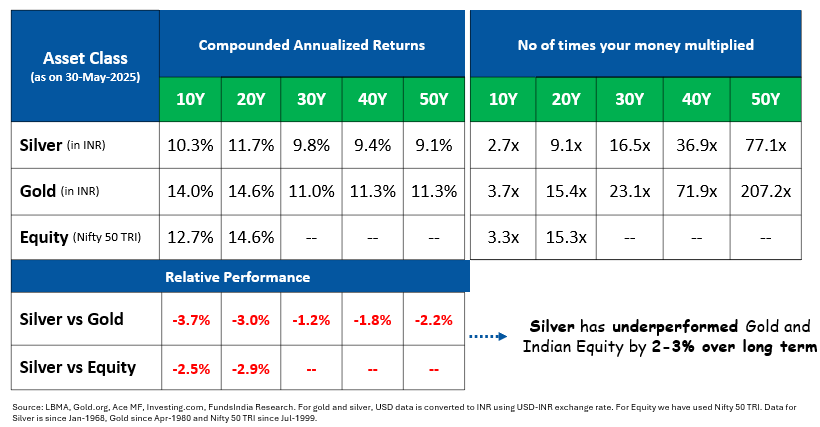

To assess whether silver enhances long-term portfolio returns, we compared its performance against gold and Indian equities (Nifty 50) across different lenses.

1. Annualised Returns Over 50 Years – Silver has delivered lower returns compared to both gold and equity over multi-decade horizons.

- Over the long term, silver has underperformed both gold and equity by 2–3% annually.

- Over a 50 year period, Rs 1 lakh invested in Silver multiplied ~77x i.e. Rs 77 lakh vs Gold at ~207x i.e. Rs 2.07 crores

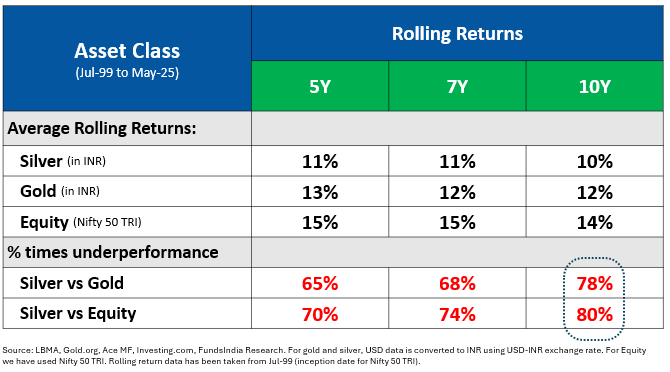

2. Rolling Return Analysis – Silver has rarely outperformed Gold and Equity over 10Y holding periods.

We looked at 5, 7, and 10-year rolling returns to evaluate performance across time, regardless of start date.

- Across all 10-year rolling periods, silver underperformed gold and equity ~80% of the time.

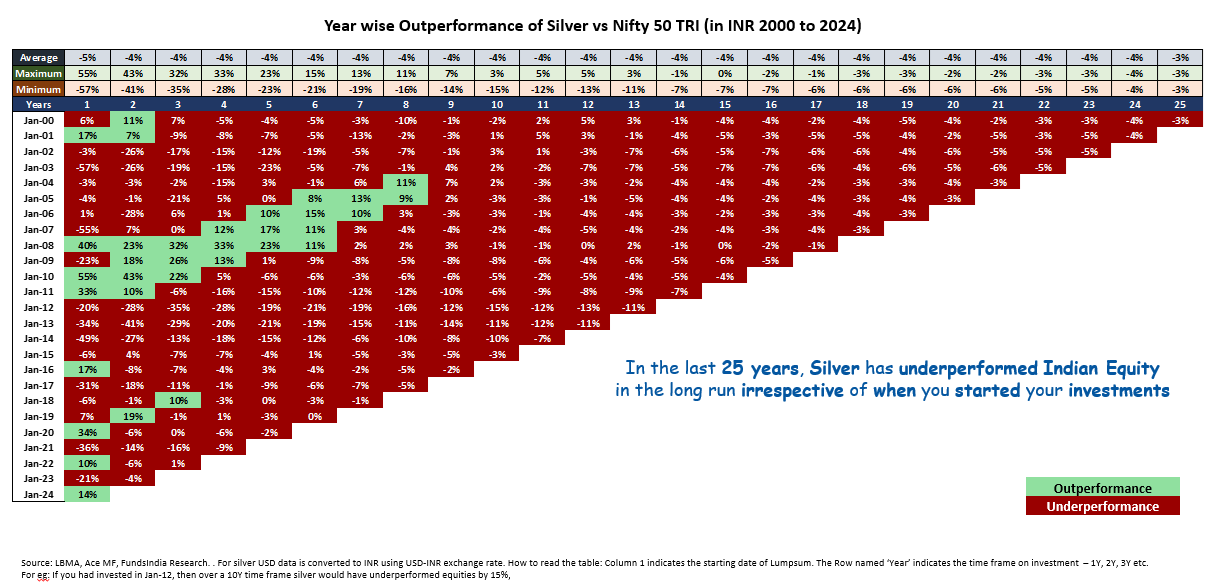

3. Lump Sum Return Matrix – Silver’s historical underperformance has been persistent and widespread.

Another way to look at the long term returns is through the lumpsum matrix given below where green/red indicate outperformance/underperformance of Silver vs Equity and Gold.

The above matrix clearly shows:

- Silver consistently underperformed equity, regardless of investment timing.

- It also lagged gold in most periods – except when you invested in Silver between 1991–1997.

Conclusion

Conclusion

Based on historical return data, silver does not improve the long-term return potential of a portfolio – especially when compared to traditional core assets like equity and gold.

Role 2: Does adding Silver help reduce volatility of your portfolio?

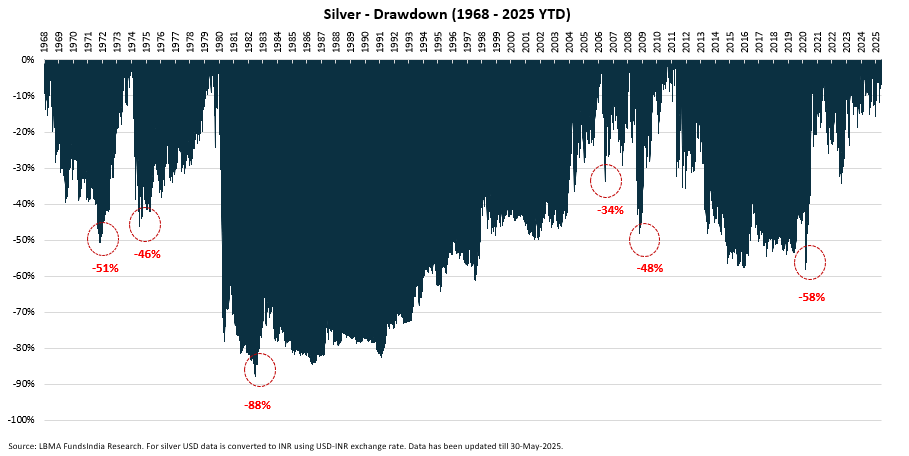

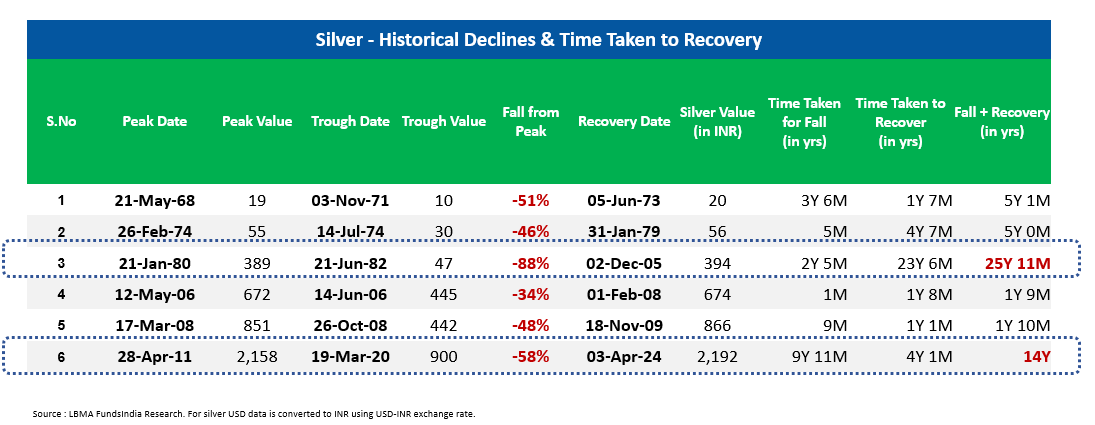

To evaluate silver’s ability to lower portfolio volatility, we examined its historical drawdowns and recovery periods over the past 57+ years (since Jan 1968).

1. Deep Historical Declines – Silver is highly volatile and has historically gone through extreme declines.

Silver has experienced multiple sharp declines, with the most severe decline reaching nearly 88%!

2. Long Recovery Periods – Major Silver drawdowns have taken a decade or more to recover, making it less suitable for portfolios seeking stability.

The depth of silver’s corrections has also been matched by prolonged recovery times:

- 1980 crash: Took ~26 years to recover.

- 2011 peak: Took ~14 years to recover.

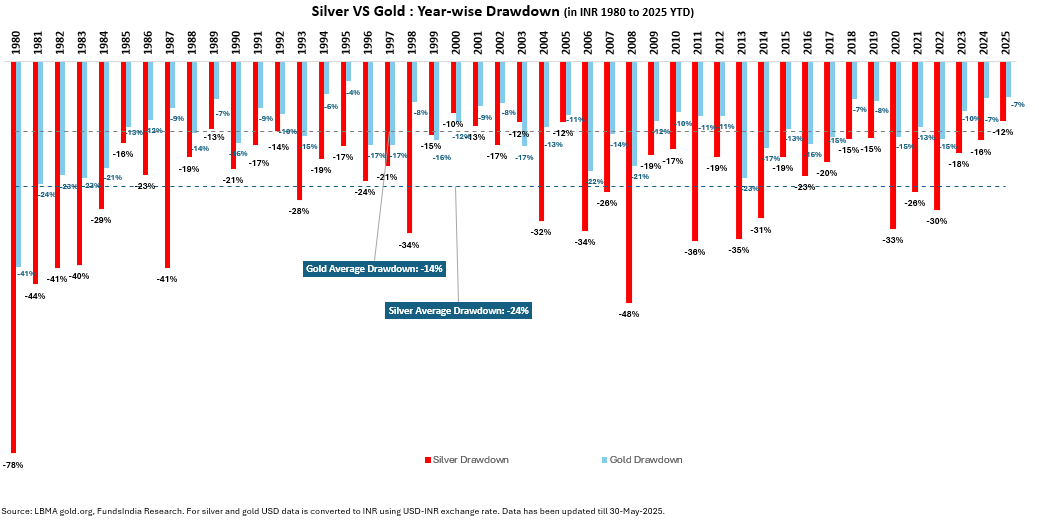

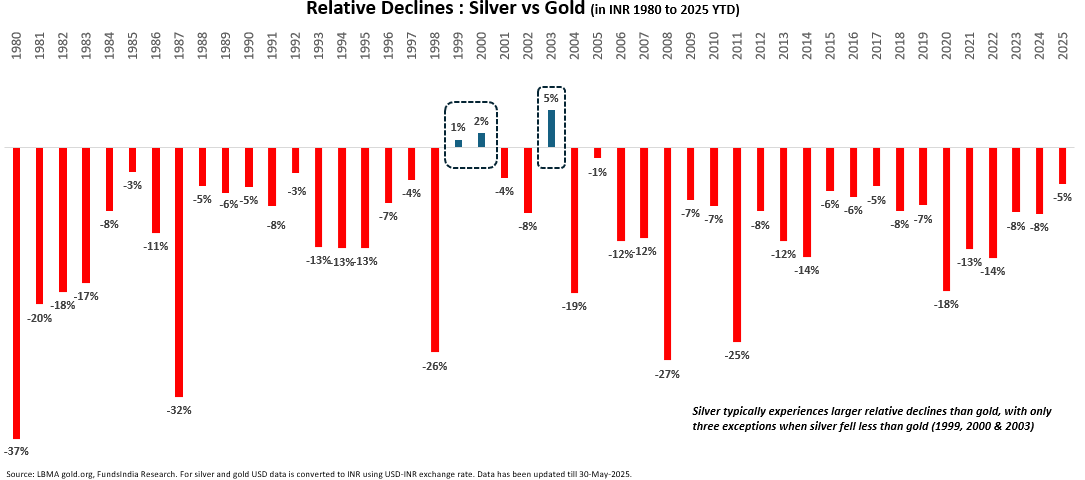

3. Frequent and Severe Intra-Year Declines – Silver tends to exhibit larger and more frequent drawdowns compared to gold.

Average intra-year decline in silver at ~24% is much higher than Gold’s average intra-year decline at ~14%…

Silver fell more than gold in nearly every year – except 1999, 2000, and 2003…

Conclusion

From both depth and frequency of drawdowns, silver introduces more volatility, not less, to a portfolio. It does not serve the role of reducing portfolio risk – unlike assets such as gold or high-quality fixed income

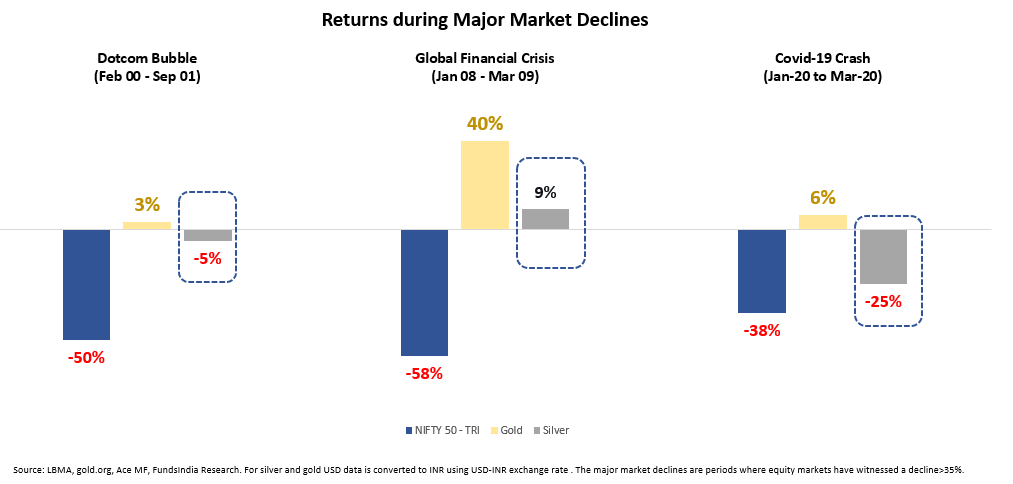

Role 3: Does Silver provide hedge during a crisis?

To evaluate silver’s effectiveness during market stress, we compared the performance of silver, gold, and Indian equities during major equity market declines (drawdowns >35%).

Key Observation – In every major market decline, silver underperformed gold and in many cases, also fell significantly alongside equities.

Conclusion

Silver does not serve as a reliable crisis hedge like Gold. In fact, its tendency to fall during broad equity market declines limits its role as a defensive asset – unlike gold, which has a proven track record of doing well during turbulent times.

Role 4 – Does Silver generate income?

Silver, like most commodities, does not generate any income or cash flows. Unlike assets such as real estate (rent) or bonds (interest), silver offers no yield, dividend, or regular payout.

Conclusion

Silver is a non-income generating asset, making it unsuitable for investors seeking stable cash flows from their portfolio.

Final Verdict: Does Silver Deserve a Place in Your Core Portfolio?

To merit inclusion in a Core Portfolio, any asset must fulfill one or more of the following roles:

| Role | Does Silver Deliver? |

| 1. Improve Returns | ❌ No — Silver has consistently underperformed Gold and Equity |

| 2. Reduce Volatility | ❌ No — Silver adds volatility, not stability |

| 3. Crisis Hedge | ❌ No — Silver fails to act as a reliable crisis hedge |

| 4. Generate Income | ❌ No — Silver generates no income |

While silver may have tactical or thematic appeal, it does not fulfill any of the four core roles required for strategic portfolio allocation.

For most investors, especially those seeking long-term stability and reasonable returns, silver is better suited as a satellite or opportunistic holding – not a core asset.

Visual Summary

While silver may not qualify for a core portfolio, could it still serve as a tactical opportunity?

At first glance, silver’s cyclical nature and potential for sharp rallies make it seem appealing for tactical exposure. However, its high volatility and unpredictable cycles demand precise timing – making the margin for error quite narrow.

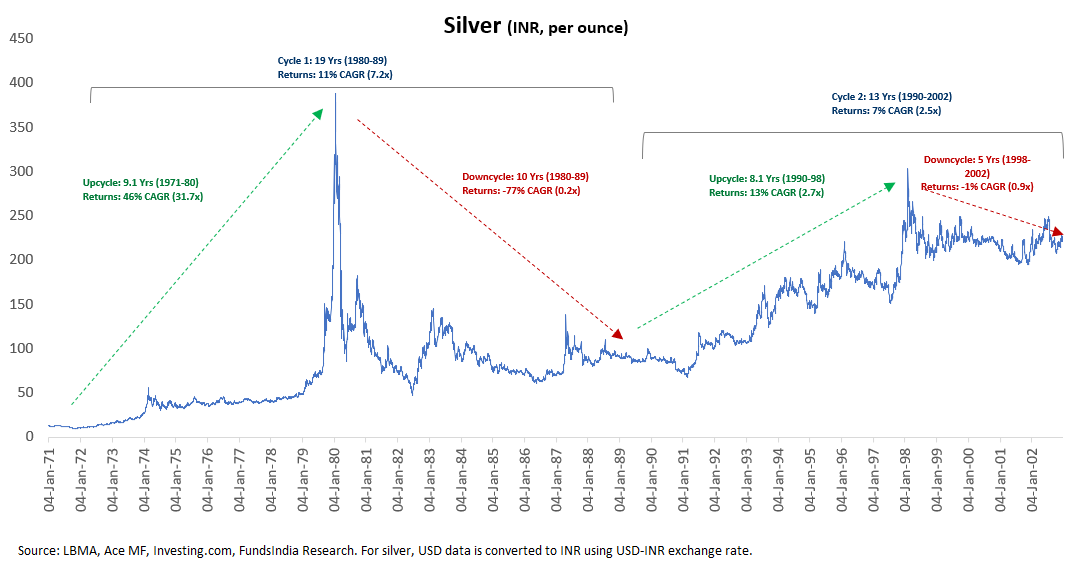

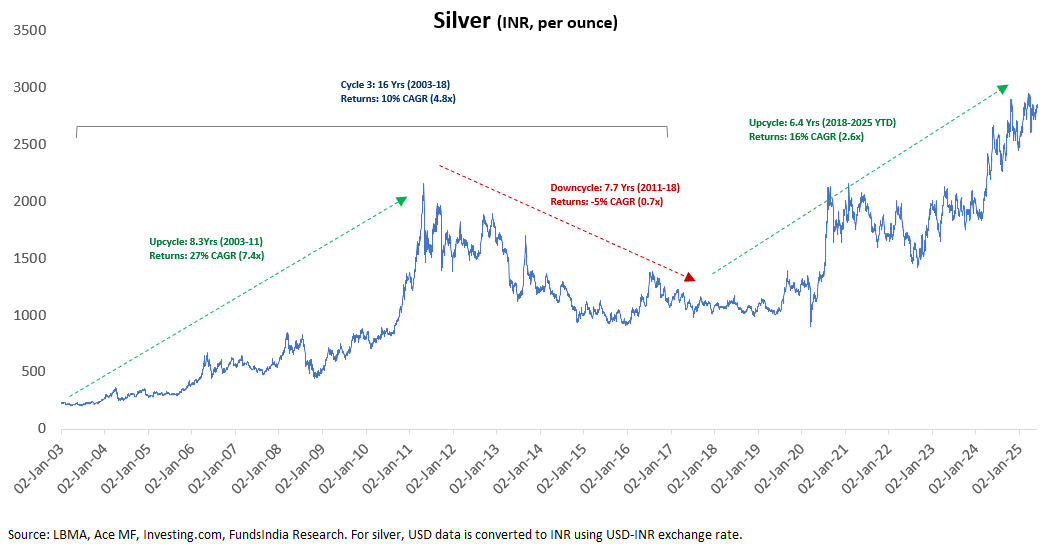

Historical Cycle Analysis (Since Jan 1971)

Historically, Silver has shown a pattern of:

- Upcycles lasting 8–10 years

- Followed by downcycles of 7–10 years

So a poorly timed entry can expose you to steep losses during a downcycle, while a poorly timed exit can erase gains made during the upcycle – leaving overall returns muted or even negative.

If you still wish to explore tactical opportunities in silver…

Two evidence-based indicators can improve timing odds:

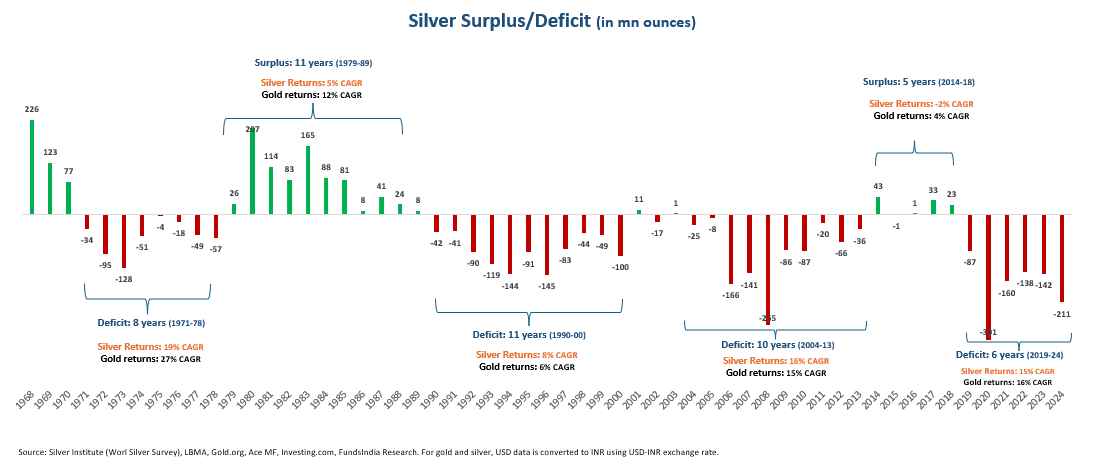

- Indicator 1 – Silver Supply Surplus or Deficit trend:

- Indicator 2 – Silver’s Relative Performance vs Gold

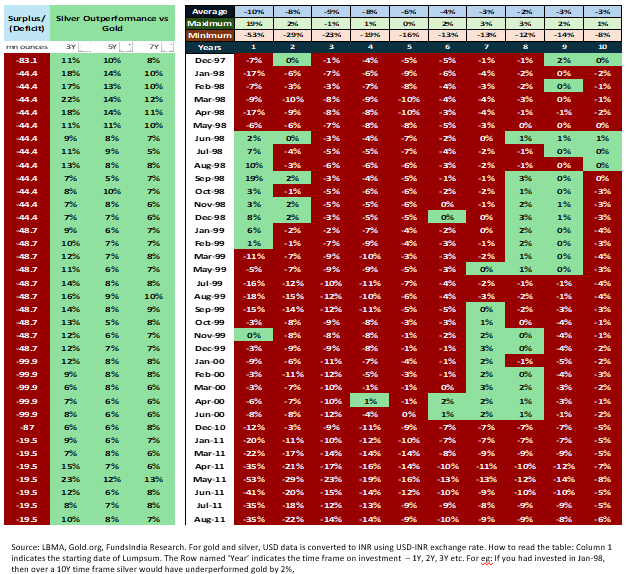

Indicator 1: Silver Supply Deficit or Surplus Trend

- Historical data shows that deficit cycles typically last 8–10 years.

- In the last four deficit phases, silver outperformed gold in only 2 out of 4 – and even then, the outperformance was modest (~1–2% CAGR).

Current Status

- Silver has been in deficit for 6 consecutive years. If historical patterns hold, supply may catch up soon, potentially reversing the deficit and capping further upside.

- Implication: The tailwind from the current deficit cycle may be nearing its end.

Indicator 2: Silver’s Relative Performance vs Gold

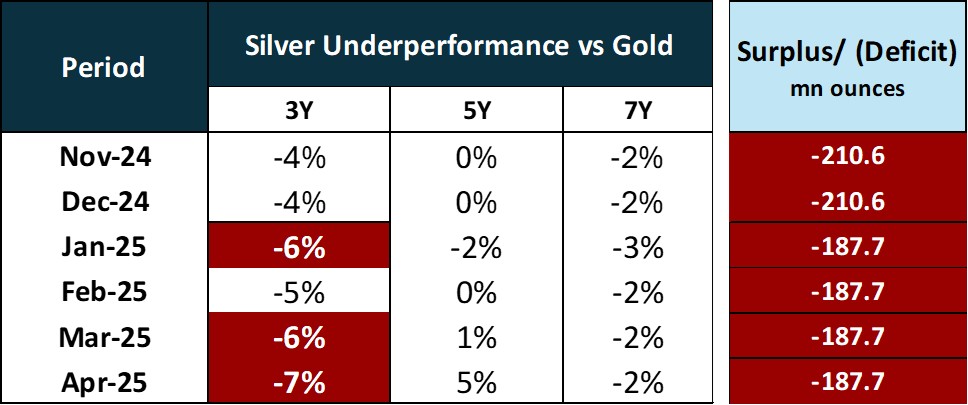

In the chart below we look at the silver deficit/surplus, relative performance over 3Y,5Y,7Y periods and the subsequent outperformance/underperformance.

When Silver significantly underperforms Gold over 3Y, 5Y, and 7Y periods and coincides with a supply deficit, it has historically outperformed Gold in subsequent years.

Conversely, when silver significantly outperforms gold over 3Y,5Y and 7Y periods, it tends to underperform in the periods that follow.

Current Status

- When Silver significantly underperforms Gold over 3Y, 5Y, and 7Y periods and is Supply Deficit – it usually outperforms in the subsequent periods. Currently as seen below, silver underperforms gold over 3Y and 7Y but outperforms over 5Y. Also, the underperformance over the 7Y period is not significant.

Our View: The current indicators do not support a compelling tactical case for silver at this time.

Parting Thoughts

Silver’s dual identity – part precious metal, part industrial commodity – makes it an interesting asset. However, interest alone isn’t a reason to invest.

- As a core portfolio asset, silver fails to deliver on any of the four essential roles: it neither enhances long-term returns, reduces volatility, acts as a crisis hedge, nor generates income.

- As a tactical allocation, silver’s potential is heavily dependent on precise timing – both entry and exit. Current indicators, including a maturing supply deficit and mixed relative performance versus gold, do not present a strong tactical opportunity.

Bottom Line: While silver continues to attract interest and carries a strong narrative, the evidence does not support a meaningful allocation – whether in the core or tactical portfolio.

A disciplined, data-driven approach focused on assets that consistently deliver across cycles will continue to serve you better over the long term.

Happy Investing as always 🙂