Dhanuka Agritech Ltd – Transforming India Through Agriculture

Incorporated in 1985 and headquartered in Gurugram, Dhanuka Agritech Ltd. is one of India’s leading agri-input companies. The company has solutions for all major crops grown in the country including cotton, paddy, wheat, sugarcane, pulses, fruits & vegetables, plantation crops and others. It has international collaborations with 10 leading global agrochemical companies from Japan, US and Europe. As of 31 March 2025, the company has 4 manufacturing units and 41 warehouses in India.

Products and Services

The company’s product portfolio is largely spread across insecticides, herbicides, fungicides, bio-pesticides, bio-simulants, bio-fertilizers, surfactants, precision agriculture tools, and drones.

Subsidiaries: As of FY24, the company has 1 subsidiary.

Investment Rationale

- Bayer AG Acquisition – The company has acquired the international rights to two key fungicides – Iprovalicarb and Triadimenol – as well as the trademark Melody for Iprovalicarb, from Bayer AG, Germany. This strategic move is set to strengthen the company’s global footprint, providing access to over 20 countries across Latin America (LATAM), Europe, the Middle East, Africa (EMEA), and Asia. Iprovalicarb commands a strong global market position with limited generic competition, while Triadimenol holds strategic importance in Brazil, a high-entry-barrier market. Over the next 2 – 3 years, the company plans to shift Iprovalicarb production to its Dahej facility in Gujarat, aiming to boost cost efficiency and scalability. Revenue generation in India is expected to begin in Q1 of FY26, with international markets following, and full-scale operations projected by Q4. The combined total addressable market for both products is estimated at $100 million.

- Growth strategies – The technical manufacturing facility at Dahej, commissioned in FY24, generated Rs.40 crore in revenue during FY25, with Rs.60 crore projected for FY26. The company is planning to expand this plant further and is currently in discussions with Japanese partners for potential contract manufacturing opportunities. It is also preparing to implement a global B2B model, working with both local and international distributors while leveraging its strong domestic network. Dhanuka has recently added new fungicides to its portfolio and is actively pursuing additional insecticides for horticultural crops, as well as herbicides targeted at soybean and groundnut cultivation. A new herbicide was launched in Q1FY26, and the company is also developing innovative fungicides for grapes and other horticultural crops, with launches anticipated in FY26. Two major products introduced in FY25 – LaNevo and MYCORe Super – have already received a positive market response.

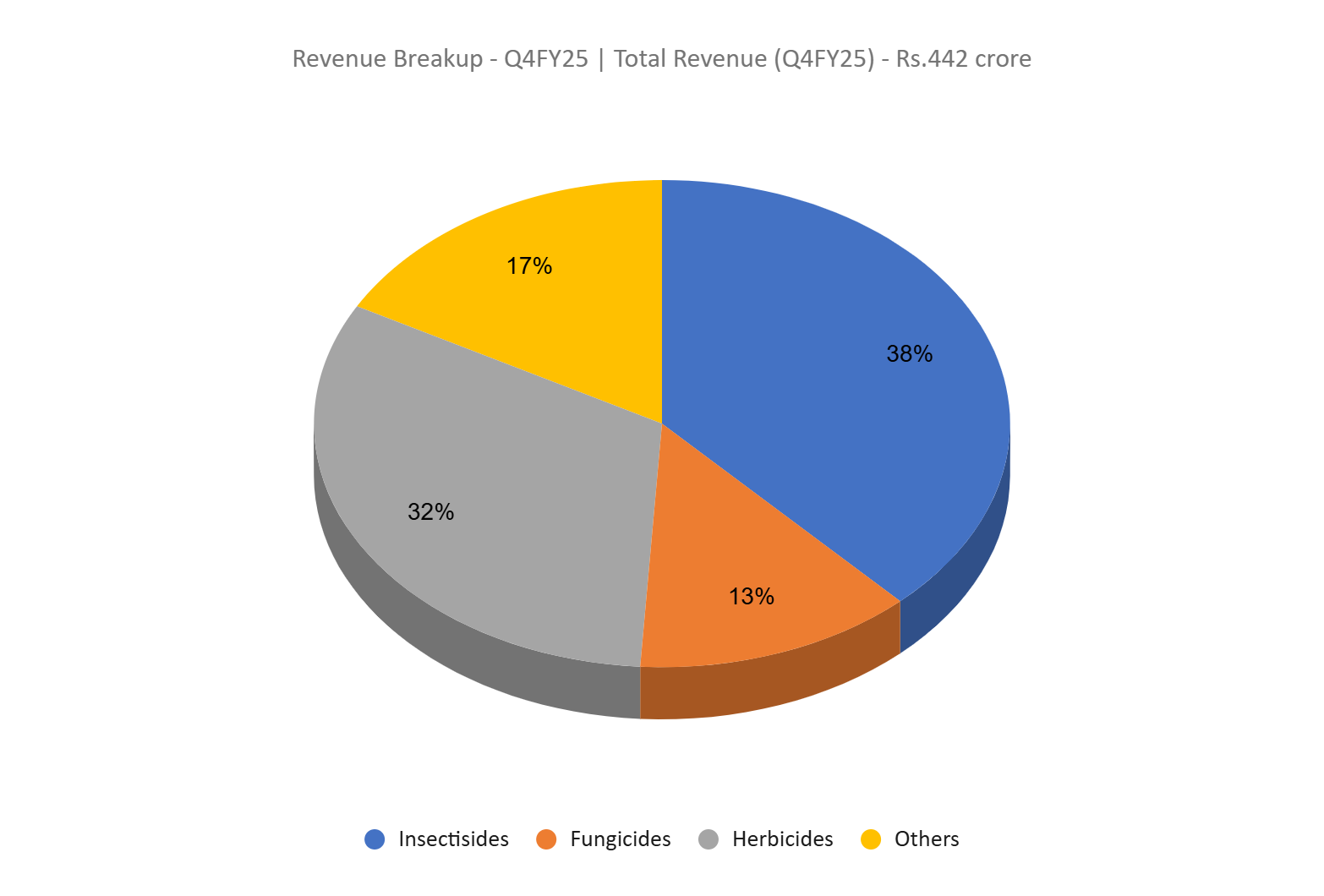

- Q4FY25 – The company achieved a 20% YoY increase in revenue of Rs.442 crore in Q4FY25 compared to the Rs.369 crore of Q4FY24. EBITDA improved from Rs.80 crore in Q4FY24 to Rs.110 crore in Q4FY25, a growth of 38%. The company reported a net profit of Rs.76 crore, an increase of 29% from the Rs.59 crore of Q4FY24.

- FY25 – The company generated revenue of Rs.2,035 crore, an increase of 16% during the year compared to FY24 revenue. Operating profit is at Rs.417 crore, up by 28% YoY. The company reported a net profit of Rs.297 crore, an increase of 24% YoY.

- Financial Performance – The company has generated revenue and net profit CAGR of 11% and 13% over the period of 3 years (FY23-25). TTM sales and net profit growth is at 16% and 25% respectively. Average 3-year ROE & ROCE is around 21% and 28% the FY23-25 period. The company has a robust capital structure with a debt-to-equity ratio of 0.05.

Industry

India’s agriculture sector is a critical pillar of the economy, providing livelihoods to around 55% of the population and holding the second-largest agricultural land area globally. The country is a leading global producer of milk, pulses, spices, and farmed fish, and ranks second in the production and export of food grains, fruits, vegetables, sugar, and cotton. The food processing industry, contributing 32% to the total food market, is one of the largest in India and shows strong growth potential. Increasing investments in irrigation, storage infrastructure, and the adoption of genetically modified crops are expected to enhance productivity. With supportive government policies and rising exports, the sector presents a strong case for sustainable and profitable investment, attracting over Rs.1.11 lakh crore in FDI by September 2024.

Growth Drivers

- Policies like Agriculture Infrastructure Fund and Pradhan Mantri Krishi Sinchayi Yojana are transforming the agriculture sector.

- The importance of effective pest and weed management to reduce the risk of crop yield loss coupled with rising population expansion, increased income levels in rural and urban areas.

- Government initiatives like the promotion of crop protection products and subsidies for fertilizers further support growth.

Peer Analysis

Competitors: Rallis India Ltd, Insecticides India Ltd, etc.

Compared to the above competitors, Dhanuka is a reasonably valued stock with robust returns on the capital invested and healthy growth in sales.

Outlook

The company exceeded both revenue and EBITDA guidance during FY25. For FY26, it has projected strong growth, with revenue and EBITDA expected to rise in the higher double-digit range. Commercialisation of a new fungicide from the Dahej plant is planned during FY26, with a projected revenue contribution of Rs.10 crore. Additionally, the recently acquired Bayer products are expected to generate Rs.110 crore in revenue for the year. Supported by a favourable monsoon outlook and strategic business initiatives, the company is well-positioned to achieve robust financial and operational performance.

Valuation

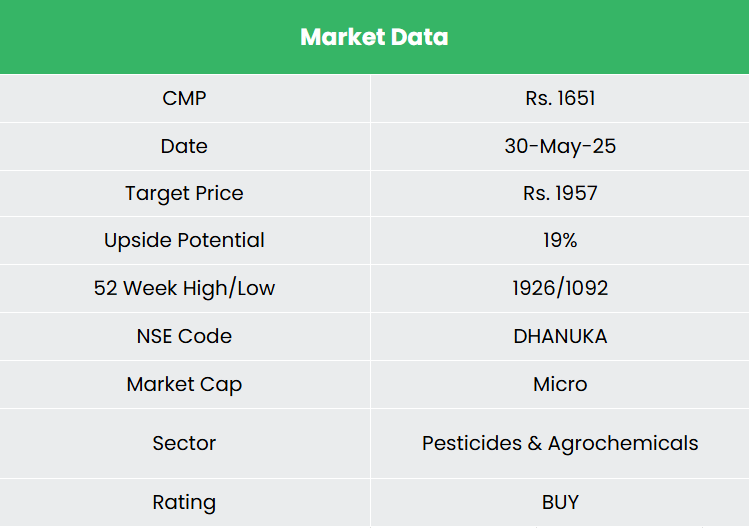

The company’s growth momentum is expected to be sustained through the introduction of innovative, high-margin products, improved utilisation of the Dahej plant, and the continued support of its robust distribution network. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,957, 24x FY27E EPS.

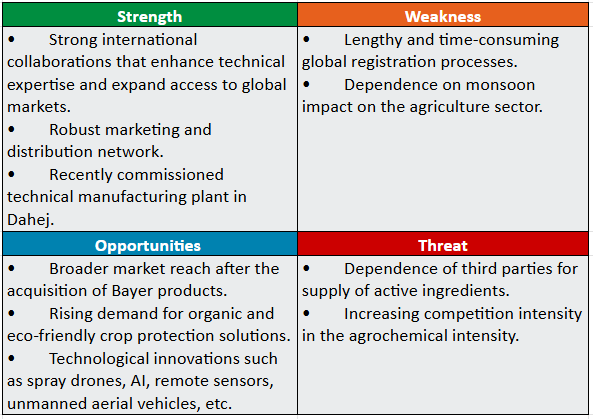

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.