It’s the beginning of the tax season. Likely that your company’s accounts/tax department will start asking you to submit your ‘tax-saving’ proof, if you have to escape or reduce your tax burden.

It’s the beginning of the tax season. Likely that your company’s accounts/tax department will start asking you to submit your ‘tax-saving’ proof, if you have to escape or reduce your tax burden.

A hastily prepared rent receipt and an express visit from an insurance agent and you may think your job is done.

Folks who take the ‘follow the herd’ approach, miss out on smart ways to save tax and earn superior returns. Avoid falling into that groove.

First, know a few facts about the common ways of saving on taxes:

Most people focus on expenses that would fetch them tax deduction. These expenses include children’s education expenses, home loan repayment or payment of insurance premium. These save taxes to some extent alright but it is still money lost, not money gained.

Did you know that you can serve the dual need of saving taxes and building a portfolio with good returns, if you took your Section 80C investment options seriously?

Yes, start looking at the ‘investment options’ that will fetch you medium to long-term superior returns. In this category you have the traditional investment options such as Employee’s provident fund (EPF), Public provident fund (PPF), NSC, 5-year tax-saving deposits and equity-linked savings scheme or ELSS.

ELSS or tax-saving mutual funds as they are called, perhaps offer you the best deal in terms of superior tax benefits and higher returns in the long term. But before that, what exactly are these funds? They are simply diversified equity funds that invest in stock markets and additionally provide a tax deduction on the principal amount you invested, in the year of investment.

Yes, agreed that these investments, like other equity investments, cannot offer guaranteed returns like your fixed income options. But read on to know how they deliver superior results for you:

- Tax-saving funds have a lower lock-in period of 3 years when compared with other investment options such as the 5-year tax-saving bank FD, 5 and 10-year NSC or 15-year PPF.

- That means you get to enjoy more liquidity to take your money out once the 3-year period is over compared with 5,10 and 15 year lock-in periods in other instruments.

- While equity mutual funds by themselves are tax-friendly in nature (as they are exempt from capital gains tax if you hold them for more than 1 year), tax-savings funds provide double benefits. While the upfront benefit you get is the deduction on the principal amount you invest; you also don’t pay taxes on the gains that accrue to you, when you decide to sell the fund anytime after 3 years. This is not the case with, say, a five-year tax saving bank deposit, where the interest income is fully taxable.

Therefore, on a post-tax basis, tax-saving funds turn out to be better options, because of their tax efficiency besides exposure to a better yielding asset class like equities.

Superior yields from tax benefit

Better yields than regular equity funds: As a result of the upfront benefit, tax-saving funds actually deliver you higher yield than regular diversified mutual funds.

Just take an example of a regular diversified equity fund delivering 12% annually over 3 years. Let us suppose there is a similar performing tax-saving fund. Now, the actual yield on this tax-saving fund would be as high as 26% annually if you are in the 30% tax bracket. It would be 20% and 16% if you are in the 20% and 10% tax bracket respectively.

Why is this so? Simply because you save taxes equal to your slab rate in the first year itself. For instance, on Rs 10,000 invested, you save Rs 3000 if your tax rate is 30%. That means your effective outgo in the year of investment is only Rs 7000, net of taxes saved!

This is why tax-saving funds make for good options if you intend to kick-start investments in equities and have not exhausted the limit of Rs 1.5 lakh under Section 80C.

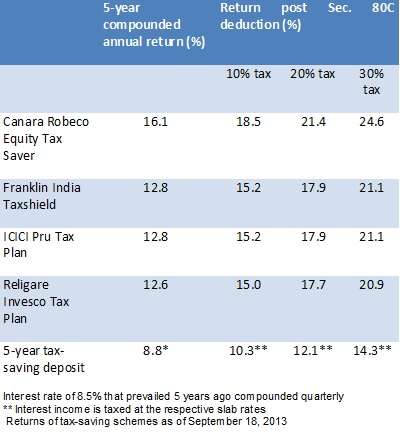

Beat FDs by a mile: The table shows the returns of FundsIndia’s tax-saving scheme recommendations. The returns are post the deduction benefit you enjoy under Section 80C versus similar returns from a tax-saving deposit from a bank.

Although tax-saving mutual funds have only a 3-year lock in, post which you may choose to hold them, we have compared them over a 5-year period as tax-saving FDs have a 5-year lock-in.

The data amply demonstrates how equity tax-saving funds outdid tax-saving deposits in the last 5 years.

While this is not to suggest that you should put all your eggs in one basket, you should consider using the additional tax advantage that comes with ELSS (besides the capital gains tax in all equity schemes) to make the best of your tax-saving investments.

A judicious mix of your company contributed EPF, traditional fixed income instruments and ELSS can form a balanced allocation to deliver optimal returns.

Good Article. Agree with all the explanation provided. Thumbs up again for the explanation 🙂

But at present market condition, few more Tax Saver funds can be added like Axis Long Term Equity and BNP Paribas Tax Saver.

It is advisable to invest in more than one tax saver funds or what can be maximum numbers of tax saver funds like 2 or 3 or 4. Because I am in dilemma that I should invest in one more funds, currently my investment are in SIP mode –

1) Franklin India Tax Shield – 1000.

2) ICICI Pru Tax Plan – 500.

3) Reliance Tax Saver – 1000.

Please recommend.

Hi Ranjan, Axis LT Equity was launched in Dec 2009. That means for 3 yrs after its launch it would have seen no outflows (given the lock-in). So we are waiting for it to complete at least one more year in its open-ended status. BNP Paribas outperformance is more recent. Over a 5-year period, it is not a topper. We will keep watch.

When it comes to choosing funds, the above funds (you mentioned) have different risk-return profiles, although they are all tax-saving funds Use your ‘Ask Advisor’ feature in your activated for us to help you choose. Thanks, Vidya

Thanks a lot for the clarification. 🙂

Hi Vidya,

I invested in Canara robeco ELSS in Dec-2010. Till date the annualised return is around mere 2% since sensex has been hovering in 18-20 K range.

For current year I’m thinking maybe 5 YR FD would be better with 8-9% return before tax, since sensex is around 20K. I’m not sure if ELSS would beat it 3 yrs down the line.

Your comments are appreciated.

Thanks

Hi Kumar, Yes the returns are low unfortunately as your investment was right after the upmarket. Had you invested in tax-saving deposit when would be your exit? In 2015 December right? And you would have locked in to 8.75% then (of course yield will be around 10-15% based on your tax bracket).

Canara Robeco is an excellent performer. All we need is one leg of upmove (which of course will not happen in 2013 but even a year of good market should pull it up) to make up for the lost game. My suggestion would be that you hold it to the time frame that an equity normally needs – which is 5 years (although lock-in is 3 years). But if you are risk averse, then the call is yours. I woudl say for any equities, have a time frame of 5 years. Thanks

Good Article. Agree with all the explanation provided. Thumbs up again for the explanation 🙂

But at present market condition, few more Tax Saver funds can be added like Axis Long Term Equity and BNP Paribas Tax Saver.

It is advisable to invest in more than one tax saver funds or what can be maximum numbers of tax saver funds like 2 or 3 or 4. Because I am in dilemma that I should invest in one more funds, currently my investment are in SIP mode –

1) Franklin India Tax Shield – 1000.

2) ICICI Pru Tax Plan – 500.

3) Reliance Tax Saver – 1000.

Please recommend.

Hi Ranjan, Axis LT Equity was launched in Dec 2009. That means for 3 yrs after its launch it would have seen no outflows (given the lock-in). So we are waiting for it to complete at least one more year in its open-ended status. BNP Paribas outperformance is more recent. Over a 5-year period, it is not a topper. We will keep watch.

When it comes to choosing funds, the above funds (you mentioned) have different risk-return profiles, although they are all tax-saving funds Use your ‘Ask Advisor’ feature in your activated for us to help you choose. Thanks, Vidya

Thanks a lot for the clarification. 🙂

Hi Vidya,

I invested in Canara robeco ELSS in Dec-2010. Till date the annualised return is around mere 2% since sensex has been hovering in 18-20 K range.

For current year I’m thinking maybe 5 YR FD would be better with 8-9% return before tax, since sensex is around 20K. I’m not sure if ELSS would beat it 3 yrs down the line.

Your comments are appreciated.

Thanks

Hi Kumar, Yes the returns are low unfortunately as your investment was right after the upmarket. Had you invested in tax-saving deposit when would be your exit? In 2015 December right? And you would have locked in to 8.75% then (of course yield will be around 10-15% based on your tax bracket).

Canara Robeco is an excellent performer. All we need is one leg of upmove (which of course will not happen in 2013 but even a year of good market should pull it up) to make up for the lost game. My suggestion would be that you hold it to the time frame that an equity normally needs – which is 5 years (although lock-in is 3 years). But if you are risk averse, then the call is yours. I woudl say for any equities, have a time frame of 5 years. Thanks

Thanks for an apt article on ELSS. I had Invested in HDFC Taxsaver Fund .Currently entire HDFC Funds are seeing BLIP in their performance .Can we Invest in This Taxsaver or is it time to shift to FT Taxshield ,Icici Taxsaver or LNT Taxadvantage

Hi Milind, Thanks for writing in. We would be happy to answer fund/portfolio-specific questions if you use our Ask Advisor feature in your FundsIndia account. All activated investors enjoy this feature free of cost and can seek our advisor’s help to build and review portfolio. Thanks, Vidya

Thanks for an apt article on ELSS. I had Invested in HDFC Taxsaver Fund .Currently entire HDFC Funds are seeing BLIP in their performance .Can we Invest in This Taxsaver or is it time to shift to FT Taxshield ,Icici Taxsaver or LNT Taxadvantage

Hi Milind, Thanks for writing in. We would be happy to answer fund/portfolio-specific questions if you use our Ask Advisor feature in your FundsIndia account. All activated investors enjoy this feature free of cost and can seek our advisor’s help to build and review portfolio. Thanks, Vidya

Hello,

I need to invest 78,000/- for the current financial year. I have already invested 15,000/- in 5 years tax saving FD. Plus I am wishing to invest 8,200/- for a Term Insurance.

For the remaining 55,000/-, I wish to invest in ELSS & Post office linked Endowment Policy ( which would give 7% approx. return + Insurance, compared to regular Endowment policy giving approx. 5% return)

Could you help me in selecting the funds for ELSS & Is investing in Post office – Endowment policy would make a balanced portfolio? I am 27 1/2 years old.

Hello Rhythm, Our fund advisory services are available for all our investors free of cost. Request you to activate your FundsIndia account and use the ‘ask advisor’ feature (available in the help tab) to choose funds. You can take a look at our Select funds to choose your ELSS. http://www.fundsindia.com/select-funds Thanks.

Hello,

I need to invest 78,000/- for the current financial year. I have already invested 15,000/- in 5 years tax saving FD. Plus I am wishing to invest 8,200/- for a Term Insurance.

For the remaining 55,000/-, I wish to invest in ELSS & Post office linked Endowment Policy ( which would give 7% approx. return + Insurance, compared to regular Endowment policy giving approx. 5% return)

Could you help me in selecting the funds for ELSS & Is investing in Post office – Endowment policy would make a balanced portfolio? I am 27 1/2 years old.

Hello Rhythm, Our fund advisory services are available for all our investors free of cost. Request you to activate your FundsIndia account and use the ‘ask advisor’ feature (available in the help tab) to choose funds. You can take a look at our Select funds to choose your ELSS. http://www.fundsindia.com/select-funds Thanks.

Hello,

I plan to invest Rs 3000 for investment and tax saving purpose.

I have no idea where to invest and how much. I have not looked beyond bank FD and PPF for tax saving purpose. Need help from you.

Regards,

Gaurav.

Hello Gaurav, As mentioned in the article, tax-saving mutual funds are options in the equity world. They help build wealth and also save on taxes. You can consider the funds mentioned there.If you need help with mutual fund advice, kindly open an account with FundsIndia. it is a free account with one time paper work. You can invest online and also constantly seek our advisory help to choose funds. thanks, Vidya

Hello,

I plan to invest Rs 3000 for investment and tax saving purpose.

I have no idea where to invest and how much. I have not looked beyond bank FD and PPF for tax saving purpose. Need help from you.

Regards,

Gaurav.

Hello Gaurav, As mentioned in the article, tax-saving mutual funds are options in the equity world. They help build wealth and also save on taxes. You can consider the funds mentioned there.If you need help with mutual fund advice, kindly open an account with FundsIndia. it is a free account with one time paper work. You can invest online and also constantly seek our advisory help to choose funds. thanks, Vidya

Hi Vidya,

I fall in the 10% income bracket, does it make sense to utilize my 80C fully given that I already have some 80D investments also. I’m trying to understand if investing the additional money for a 3 year lock-in period with a 10% tax rebate makes more sense or investing it in just normal equity makes more sense.

I understand this article is more about ELCC schemes, but is there some interpolation that can be done with the data to show how tax saving schemes help people not just in the 30% bracket, but also lesser brackets and maybe even those who have no tax liability!

Thanks

Hello Sir,

First get to know from your firm how much tax will be deducted after your other deductions. Multiply it by 10 (since you fall in the 10% tax bracket it will be tax*100/10) to see how much you need to invest. Invest that in ELSS schemes and rest in open-ended diversified equity schemes. thanks Vidya

Thanks Vidya. Makes it very clear…

Hi Vidya,

I fall in the 10% income bracket, does it make sense to utilize my 80C fully given that I already have some 80D investments also. I’m trying to understand if investing the additional money for a 3 year lock-in period with a 10% tax rebate makes more sense or investing it in just normal equity makes more sense.

I understand this article is more about ELCC schemes, but is there some interpolation that can be done with the data to show how tax saving schemes help people not just in the 30% bracket, but also lesser brackets and maybe even those who have no tax liability!

Thanks

Hello Sir,

First get to know from your firm how much tax will be deducted after your other deductions. Multiply it by 10 (since you fall in the 10% tax bracket it will be tax*100/10) to see how much you need to invest. Invest that in ELSS schemes and rest in open-ended diversified equity schemes. thanks Vidya

Thanks Vidya. Makes it very clear…