A Balanced Approach to Equities

If you are starting out on a long-term portfolio or looking for participation in equity, albeit with less volatility, you can consider Tata Balanced Fund. This equity-oriented fund, with about three fourth of its assets in equities and the rest in debt, has a track record of delivering 12.4% annually in the last 5 years. That’s not only a good 4 percentage points higher than the balanced fund category average, but it is also superior to the average returns of diversified equity funds by a similar margin.

Suitability

Tata Balanced has a long track record, having been launched in the last quarter of 1995 and a witness to several market ups and downs.

The fund invests about 70-75% of its assets in equities on most occasions. While peers such as ICICI Pru Balanced reduce their equity holding to 65% levels, Tata Balanced seldom reduced its holding below the 70%-mark in recent years. The benefit of such holding is that the fund outperforms its index and peer groups by a significant margin in up-markets.

In 2007 and 2009, for instance, the fund beat established peers such as HDFC Balanced and ICICI Pru Balanced by a massive 20-30 percentage points. On the flip side though, the fund does fall more than its peers in down markets. Hence, while you can expect this fund to contain declines better than diversified equity funds, if you are more conservative, you will do well to hold the above-mentioned peer funds over Tata Balanced.

Dividend Payout Option: Tata Balanced has a unique option that may help even relatively conservative investors looking for regular payouts. The fund has a monthly dividend payout option. Started in August 2010, this option has been paying dividends every single month since it was launched, although the quantum of dividends varied based on market conditions. Between January and August 2013, for instance, it declared dividend of 3.5% every month (2.5% in September).

Hence, for a retired investor with investments diversified across other fixed income products, this fund could be a good option to take exposure to the equity class.

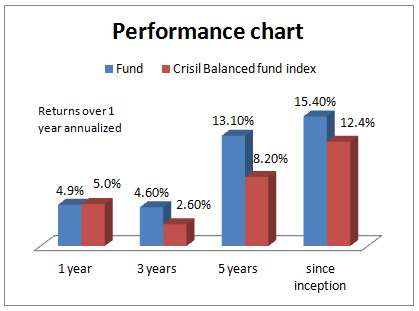

Performance

Had you started a Rs. 10,000-a-month SIP in Tata Balanced 15 years ago, you would have a handsome Rs. 74 lakh today. That’s an annual yield of 17%. The benchmark Crisil Balanced Fund Index, on the other hand, would have fetched just Rs. 42.5 lakh; that’s an IRR of 10.7% annually.

Had you started a Rs. 10,000-a-month SIP in Tata Balanced 15 years ago, you would have a handsome Rs. 74 lakh today. That’s an annual yield of 17%. The benchmark Crisil Balanced Fund Index, on the other hand, would have fetched just Rs. 42.5 lakh; that’s an IRR of 10.7% annually.

The fund also consistently beat its benchmark. On a rolling one-year return basis for the last 3 years, the fund beat its benchmark 86% of the times. Its record would have been better save for the fund underperforming marginally this year. It is noteworthy that the Crisil Balanced Fund Index has a 65% equity (Nifty) allocation and the rest in debt (Crisil Composite Bond). Tata Balanced, on the other hand, holds about 75% in equities. Higher exposure to equities and a relatively higher midcap holding, when compared with the benchmark, are the reasons for such underperformance. Such blips are usually more than made up in a rally.

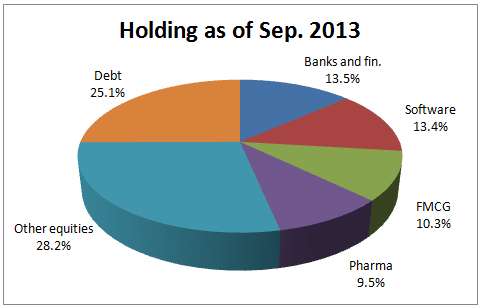

Portfolio

As mentioned earlier, Tata Balanced has mostly sought to hold equities above the 70%-mark, even in down markets such as 2008 and 2011, although its peers reduced their holdings to around 65%. This higher exposure though, delivered handsomely when markets moved to the green. In 2009, for instance, the fund managed a whopping 72% return, a feat achieved only by just a couple of peers which held higher mid-cap stocks.

As of August, close to three-fourth of the fund’s total equity holdings were in large-cap stocks with a market cap of over Rs. 10,000 crore. The rest were in mid and small-cap stocks. Blue Dart Express, WABCO India, Balkrishna Industries, Fag Bearings and Emami were some of the offbeat picks in the mid- and small-cap space.

In the course of the last 8 months, since December, the fund cut back its exposure to the banking and finance space and instead, significantly increased holdings in software.

In its debt portfolio, the fund held a good 11% in gilt instruments (lower than a year ago holding), evidently to keep credit risk of the portfolio at bay. It held about 5.7% in debentures and the rest in money market instruments. But the gilt exposure may have caused some dip in the fund in July.

hello vidya

nice article. i have sip in hdfc prudence of 10000 per month for retirement corpus 20 years later. how does it compare with tata balanced fund?

Hi Sandip, Prudence has more mid-caps then Tata. hence, in a downturn, Prudence underperforms more. If you are comfortable with that, given your long-term tim frame, stay on. Tks

hello vidya

nice article. i have sip in hdfc prudence of 10000 per month for retirement corpus 20 years later. how does it compare with tata balanced fund?

Hi Sandip, Prudence has more mid-caps then Tata. hence, in a downturn, Prudence underperforms more. If you are comfortable with that, given your long-term tim frame, stay on. Tks

Hello Vidya,

I have been following your blog for sometime and would like to thank you for giving un-biased advice to investors.

I invest in stock market directly, so no need for Equity funds.

However I need to include debt in my portfolio so was thinking about dynamic bond funds, but then they can just match inflation over long run, but I need inflation beating returns.

Hybrid funds having equity orientation and some portion of debt would be a better choice in this regard for the next 15 – 20 years. Short-listed some funds – Tata Balanced Fund, HDFC Prudence or Balanced Fund & ICICI Pru Balanced Fund. Please advise. I am a moderate type of investor.

Regards,

Sumeet Sasmal

Hello Sumeet, hope you are aware that balanced equity-oriented funds will invest only about 25-30% in debt. If you are ok with that limited component, you can go for Tata balanced. You may be able to take the mid-cap exposure risk that comes with it, given that you are an equity investor.

Also, you should look at debt from a portfolio perspective rather than individually. Will you portfolio (across asset classes) beat inflation comfortably with soem exposure to debt? Likely it will, if you have a good chunk in equity anyway. The debt component will keep the portfolio from being too volatile. That should be it’s purpose.

In future, kindly use the ‘Ask Advisor’ feature in your account (click help tab) to get response for fund specific queries or portfolio review either through mail or call back. Thanks, Vidya

Hi Vidya,

Currently I have allocated 15% to ICICI Balanced (G) and 10% to ICICI Balanced Advantage Funds through SIPs. I have a 20 year investment horizon. I am in a dilemma whether to make my ICICI Focused Blue Chip + Mirae India Opportunities Funds as Core or the above two Balanced Funds as Core – what do you suggest?

Is there high portfolio duplication between these two Balanced funds? Which one of these Balanced Funds can offer higher returns in 5+ years horizon? Would you recommend any other Balanced Fund as addition or replacement?

Thanks,

Utsav

Hi Utsav, Sorry for the delayed response. In future, Pl. use Advisor support in your FundsIndia account for all portfolio queries to help us serve you faster and systematically, than use the blog. The blog may pl be used as a discussion forum.

The 2 ICICI funds are not comparable. One is a balanced fund, the other is more a hedge against volatility, which uses derivatives. The Balanced advantage fund may underperform in a one-sided rally but help during volatile times. Given your time horizon, a couple of equity funds, one balanced fund and one debt fund can form part of your portfolio. go for pure equity funds but have a balanced fund and add one debt fund such as Templeton India Income Opportunities to form a long-term portfolio. If you are not risk averse then you can have a 70-80% allocation in equities. When you allocate assuem that balanced fudns have a 75% in equity and 25% in debt. thanks, Vidya

Hello Vidya,

I am planning to invest in Balanced fund for my child’s higher education in next 14 years. However, little confused amongst the following funds:

1> Tata Balanced Fund

2> HDFC Balanced Fund

3> HDFC Children’s Gift Fund – Investment plan

Please help me to select the best fund for investment.

Regards,

Sourav

Sourav, Thanks for writing to us. For providing portfolio recommendations, please write to us using the ‘Adivsor appointment’ feature in the help tab of your activated FundsIndia account. The blog is more of a discussion forum and I am constrained from offering individual advice here. thanks, Vidya

Hello Vidya,

I am planning to invest in Balanced fund for my child’s higher education in next 14 years. However, little confused amongst the following funds:

1> Tata Balanced Fund

2> HDFC Balanced Fund

3> HDFC Children’s Gift Fund – Investment plan

Please help me to select the best fund for investment.

Regards,

Sourav

Sourav, Thanks for writing to us. For providing portfolio recommendations, please write to us using the ‘Adivsor appointment’ feature in the help tab of your activated FundsIndia account. The blog is more of a discussion forum and I am constrained from offering individual advice here. thanks, Vidya

Hello Vidya,

I have been following your blog for sometime and would like to thank you for giving un-biased advice to investors.

I invest in stock market directly, so no need for Equity funds.

However I need to include debt in my portfolio so was thinking about dynamic bond funds, but then they can just match inflation over long run, but I need inflation beating returns.

Hybrid funds having equity orientation and some portion of debt would be a better choice in this regard for the next 15 – 20 years. Short-listed some funds – Tata Balanced Fund, HDFC Prudence or Balanced Fund & ICICI Pru Balanced Fund. Please advise. I am a moderate type of investor.

Regards,

Sumeet Sasmal

Hello Sumeet, hope you are aware that balanced equity-oriented funds will invest only about 25-30% in debt. If you are ok with that limited component, you can go for Tata balanced. You may be able to take the mid-cap exposure risk that comes with it, given that you are an equity investor.

Also, you should look at debt from a portfolio perspective rather than individually. Will you portfolio (across asset classes) beat inflation comfortably with soem exposure to debt? Likely it will, if you have a good chunk in equity anyway. The debt component will keep the portfolio from being too volatile. That should be it’s purpose.

In future, kindly use the ‘Ask Advisor’ feature in your account (click help tab) to get response for fund specific queries or portfolio review either through mail or call back. Thanks, Vidya

Hi Vidya,

Currently I have allocated 15% to ICICI Balanced (G) and 10% to ICICI Balanced Advantage Funds through SIPs. I have a 20 year investment horizon. I am in a dilemma whether to make my ICICI Focused Blue Chip + Mirae India Opportunities Funds as Core or the above two Balanced Funds as Core – what do you suggest?

Is there high portfolio duplication between these two Balanced funds? Which one of these Balanced Funds can offer higher returns in 5+ years horizon? Would you recommend any other Balanced Fund as addition or replacement?

Thanks,

Utsav

Hi Utsav, Sorry for the delayed response. In future, Pl. use Advisor support in your FundsIndia account for all portfolio queries to help us serve you faster and systematically, than use the blog. The blog may pl be used as a discussion forum.

The 2 ICICI funds are not comparable. One is a balanced fund, the other is more a hedge against volatility, which uses derivatives. The Balanced advantage fund may underperform in a one-sided rally but help during volatile times. Given your time horizon, a couple of equity funds, one balanced fund and one debt fund can form part of your portfolio. go for pure equity funds but have a balanced fund and add one debt fund such as Templeton India Income Opportunities to form a long-term portfolio. If you are not risk averse then you can have a 70-80% allocation in equities. When you allocate assuem that balanced fudns have a 75% in equity and 25% in debt. thanks, Vidya