What happened to Neil Woodford?

The recent incident involving the iconic and now infamous British fund manager, Neil Woodford (often referred to as Britain’s answer to Warren Buffett) where his funds failed to meet investors’ redemption requests due to insufficient liquidity has brought the focus back on an otherwise ignored topic – liquidity risk. His open-ended funds had made substantial investments in illiquid unlisted companies. When there was a sudden rise in redemptions following a weak performance, the funds were unable to liquidate those investments in time and had to suspend redemptions for investors who wanted to exit.

Thankfully, there have been no major liquidity-related suspensions in India – at least on the equity funds side. However, if something like this can happen in an evolved capital market such as the UK, then India can’t be immune either, and we can’t simply take liquidity in Indian mutual funds for granted.

Small cap funds – Is bigger better?

Liquidity can be a concern especially when you invest in small cap stocks (and by extension in small cap funds) where trading volumes may be extremely low. We define liquidity as the ability of a fund to make timely exits and entries in stocks without impact costs (read as: will the fund be able to buy or sell a stock at a price close to the previously traded price).

Starting in 2015, many small cap funds saw a significant increase in inflows leading to far larger fund sizes. In the past, to cope with their larger size, funds had the flexibility to lower the proportion of small cap stocks (and invest more in large caps) in their portfolio if required.

However post the Oct 2017 SEBI re-categorisation norms, small cap funds have to compulsorily invest at least 65% of their corpus in small cap stocks.

The trend of increasing fund size in a category with relatively lower liquidity and a forced 65% exposure to small caps creates a ripe scenario for liquidity issues to crop up.

Growing pains

Here are three challenges that small cap funds can typically encounter as they grow in size.

- Impact cost

- Constrained Liquidity

- Reduced Flexibility in Portfolio Construction

Impact Cost

Let’s understand this with an example. Suppose the corpus of a small cap fund called ABC Fund grows from ₹1,000 crores to ₹6,000 crores over time. To start with, 5% of the fund’s corpus (₹50 crores) was invested in XYZ, a small cap company. As the fund size grows six-fold, to maintain the 5% weightage, the fund will have to raise its investment in XYZ to ₹300 crores.

Such a large investment in a small cap stock with low trading volumes will have to be staggered over several days. This can push up the stock price and so the fund’s purchase cost. Similarly, when the fund exits the stock, the price may come under pressure.

Constrained Liquidity

If a fund has a large exposure to illiquid small cap stocks, managing risk based on evolving views becomes difficult for the fund manager as reducing/exiting these investments may be difficult if the underlying investment rationale changes. This liquidity issue only gets exacerbated as a fund grows and its exposure to such stocks rises.

In cases of prolonged periods of (and/or sudden) large-scale redemptions, the fund is forced to sell its more liquid holdings sometimes leading to unintended concentration risks in the remaining less liquid stocks.

Reduced Flexibility in Portfolio Construction

A very large fund may not be able to take concentrated exposures in several small cap stocks. It may instead have to invest in a far larger number of small cap stocks to adequately deploy its corpus sometimes leading to several insignificant exposures (less than 1% holding).

This also constrains the fund manager’s ability to make large tactical shifts in the portfolio if required. The fund to address its larger size and to ensure liquidity may also have to invest more in large cap stocks and/or cash holdings (subject to a combined upper limit of 35%) which may dilute the positioning.

How large is too large?

While there is no precise formula to indicate when a small cap fund has become too large, we can get a fair sense of a potential size impact based on the following framework:

- Fund AUM as a % of the Investable Universe – When a small cap fund’s AUM becomes a large percentage of the free-float market cap of the Nifty Smallcap 250 Index constituents, it indicates that its liquidity may become problematic.

- Liquidity of stocks in the fund portfolio – How many stocks (and their weightage in the portfolio) cannot be completely exited by the fund within 30 days? The larger the percentage, the more concerned you must be.

- Large stakes in companies – What percentage of the fund’s AUM is locked in the form of large stakes in a few companies? The greater the proportion of such companies in the portfolio, the lower the fund’s liquidity. This is because as the fund’s stake in a company goes up it becomes tougher for it to exit without impacting the stock price and therefore its returns.

- Reduced flexibility in portfolio construction – A very large AUM may be accompanied by an increase in the number of small cap stocks in the portfolio and reduced tactical flexibility. Alongside, the percentage of the corpus invested in large caps and/or cash holdings may also go up (subject to the upper limit of 35%) indicating potential difficulty in finding new opportunities in the small cap space.

- Restrictions on new investor subscriptions – Whenever the monthly inflows (new subscriptions) cross a certain percentage of the AUM, funds usually consider introducing restrictions on them. Allowing assets to continue to grow may restrict potential investment opportunities.

Evaluating HDFC Small Cap Fund

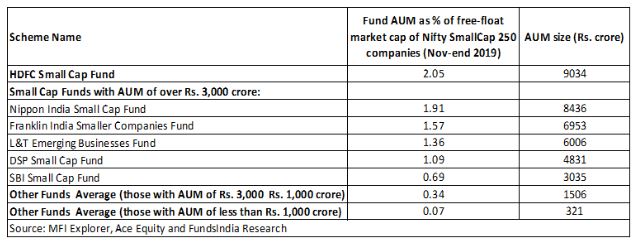

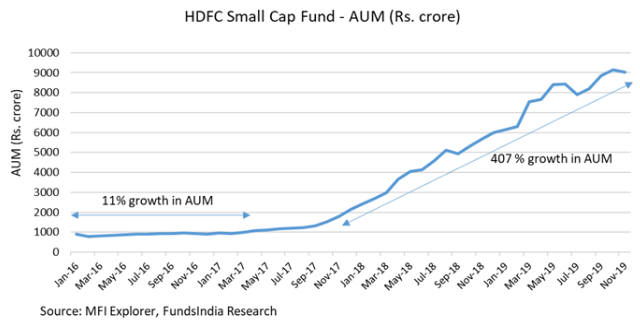

Let’s take the case of HDFC Small Cap Fund and see how it fares on each of these criteria. At an AUM of over ₹9000 crores as of Nov-end 2019, it is the largest small cap fund.

How big?

The fund’s AUM was as much as 2% of the free-float market cap of the Nifty Smallcap 250 companies (₹4.4 lakh crore) in Nov 2019. That is, the fund’s asset base constituted 2% of its investible small cap space. Free-float market cap has been calculated by excluding the promoter and promoter group equity stake from the total market cap of a company.

While 2% may seem small, let’s get some perspective by comparing this with ICICI Prudential Bluechip Fund, the biggest fund in the large cap category. The fund’s AUM of ₹24,640 crore was only 0.42% of the free-float market cap of the Nifty 100 large cap companies of ₹59 lakh crore. It was likewise for Kotak Standard Multicap Fund, the largest in the multi cap category. The fund’s AUM of around ₹29,000 crore was 0.40% of the free-float market cap of the Nifty 500 companies which was ₹73 lakh crore.

HDFC Small Cap Fund’s 2% also appears high when compared with its peers (20 funds). See the table below.

How liquid?

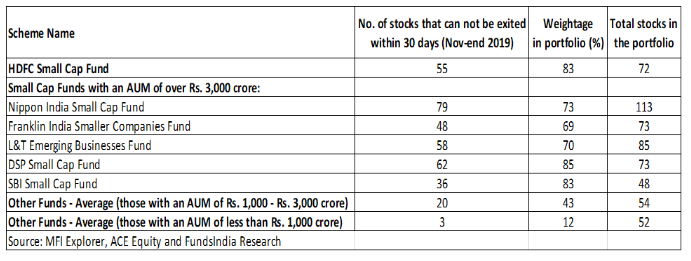

To understand how HDFC Small Cap Fund scores on liquidity, we look at the number of stocks that the fund can’t exit completely in less than 30 days.

The fund would have found it difficult to completely exit 55 out of the 72 stocks held as of Nov-end 2019. These stocks accounted for a whopping 83% of its portfolio, which is fairly high compared to several other funds in this category. See the table below.

These calculations take into account 30% of the daily average combined trading volume of stock on both the NSE and the BSE for 3 months ending Nov 2019 to calculate liquidity (days to exit each stock).

Increasing ownership levels?

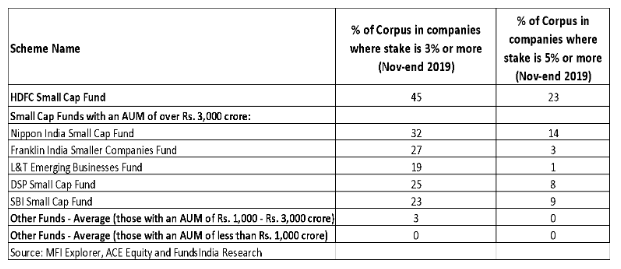

Next, we look at the proportion of HDFC Small Cap Fund’s portfolio that was invested in companies where it held large stakes.

In Nov-end 2017, only 4% of the fund’s corpus was in companies where its stake was 3% or higher. This went up sharply to 45% by Nov-end 2019. Similarly, while in Nov 2017 the fund did not have investments in any company where its stake was 5% or higher, such companies accounted for 23% of its portfolio by Nov 2019.

No other small cap fund had such a significant share of its corpus in companies where its stake was 3% or higher. See the table below.

While such large ownership levels do not conflict with the long-term investment approach of the fund (reflected in low turnover), they could make the fund far less nimble to respond to adverse circumstances (including a significant liquidity event).

Managing its portfolio

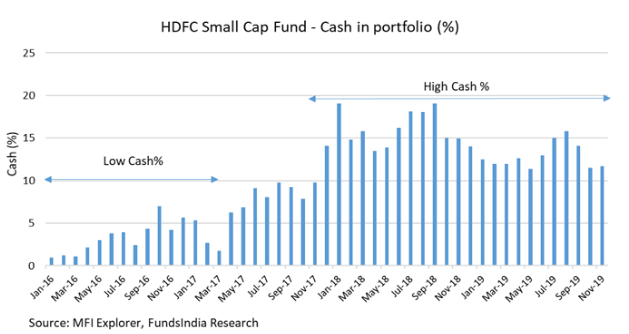

As a fund’s asset base expands beyond a point it can face increasing difficulty in finding opportunities in the small cap space. It can deploy the additional funds (subject to the upper limit of 35%) in large caps stocks and/or raise its cash holdings. In the case of HDFC Small Cap Fund, this has been in the form of a sharp rise in its cash holding.

For example, between Jan 2016 and Mar 2017, the fund’s AUM grew 11%. During this period the fund’s cash holdings as a percentage of its portfolio stayed mostly in low single-digits. Then, between Nov 17 and Nov 19, the fund size more than quintupled to ₹9034 crores. During this period, the cash holdings averaged 14%. See the charts below.

One way to deal with sudden large inflows is to allow cash build-up in the portfolio. This gives the fund manager time to put the new money to work, but it also dilutes the performance of the rest of the portfolio in a rising market.

The relatively high proportion of cash seems to indicate the above issue, as the fund house has historically not taken cash calls otherwise.

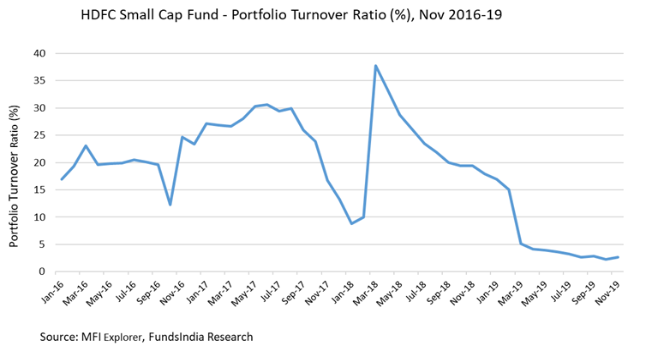

The fund’s portfolio turnover ratio (PTR), an indicator of how much it churns its portfolio – however, is low – at 3% in Nov 2019. This has been so in the past too (chart below). The low PTR has worked in the fund’s favour by helping it manage its portfolio despite its growing asset size.

Also, while the fund’s Top 20 Stock Concentration has remained relatively stable at 41% to 50% for the last 2 years, the share of insignificant stocks (individually accounting for less than 1% of the portfolio) has risen. In Nov 2017, such stocks comprised only 10% of the fund’s portfolio. This went up to ~16% by Nov 2019.

Saying no to new inflows?

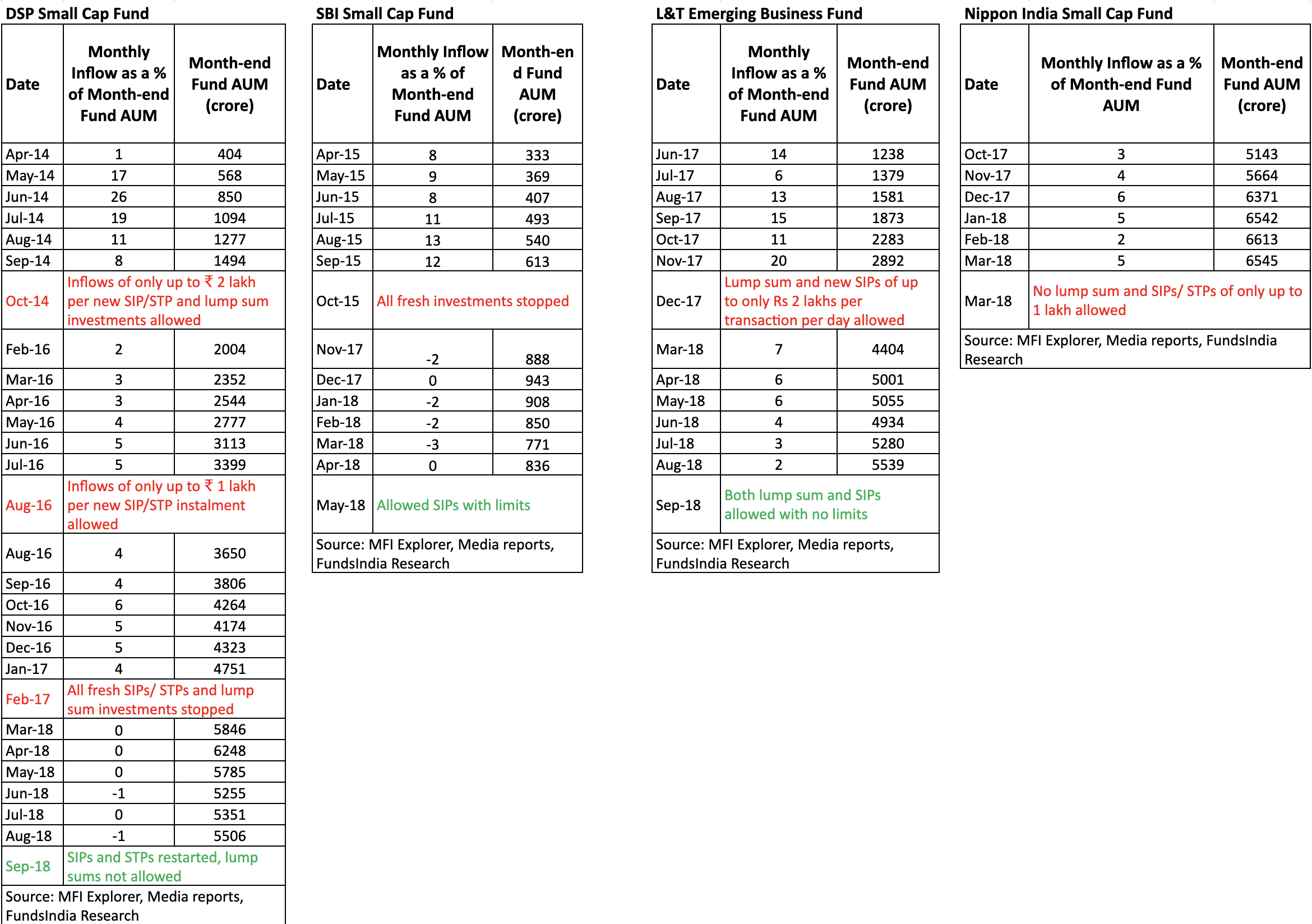

However, despite its growing size, HDFC Small Cap Fund has never imposed restrictions on new subscriptions/inflows, unlike other large small cap funds. Let’s look at a few funds to see at what stage such restrictions were introduced.

We see many funds have imposed restrictions on new subscriptions whenever the monthly inflow as a percentage of the fund’s AUM rose to 4-5% or higher for a few months at a stretch. Once the surge eased, funds eased the restrictions.

HDFC Small Cap Fund, however, hasn’t introduced any restrictions despite receiving significant inflows over several months in the past.

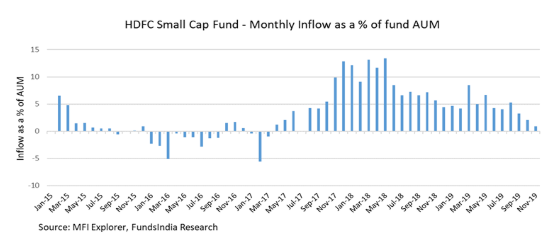

What’s worth noting is that the surge in inflows (chart below) happened at a time when small cap stocks were at their all-time highs in 2018. Unsurprisingly, as the fund’s corpus expanded rapidly from Oct 2017, its cash holdings also shot up given the lack of investment opportunities in the expensively valued small cap space.

Now if the cash holdings were a market-timing call given the valuation concerns, we would have preferred the fund to have restricted inflows rather than accepting them and keeping it as cash.

Summing it up

Taking into account all the above factors, there are initial indications that the liquidity profile of HDFC Small Cap Fund appears to have become tighter on several fronts.

-

Weakening Liquidity:

The fund has a significant proportion of its corpus invested in stocks that can’t be exited in less than a month. Other funds are relatively better off on this count.

-

Increasing ownership stakes in portfolio companies:

The percentage of the fund’s corpus in companies where its stake is large (3%/ 5% or higher) has expanded significantly over the years. Here too, other funds are better placed in terms of a smaller percentage of the corpus invested in companies where their stakes are high.

-

Increase in Cash:

The fund’s expanding asset base has been accompanied by a growing percentage of cash holdings. Whether this is the result of a deliberate strategy or a lack of choice is hard to tell.

But the fact that HDFC AMC historically has never taken cash calls and has explicitly stated its preference for always staying in the market is something to be noted. -

No restrictions despite sizable inflows:

In addition, despite the expanding asset base, the fund hasn’t restricted new subscriptions. The call on whether the fund is facing size constraints, therefore, rests with the investor unlike in the case of other funds where the restrictions on new subscriptions signal the same for investors.

-

Low Portfolio Turnover helps manage large size to an extent:

The fund’s low portfolio turnover ratio has however helped it manage its large corpus to a certain extent. The portfolio concentration in the top 20 stocks too has remained stable.

-

Robust Performance Track record:

We would like to highlight that the fund has a robust performance track record and benefits from a highly experienced longstanding manager and a proven investment approach. We retain our high conviction on the fund manager Chirag Setalwad.

That being said, however, given our concerns around the fund’s current liquidity profile, we find it prudent to recommend our investors to stop incremental exposure towards the fund while continuing with their existing exposure. We will continue to monitor the situation closely and suggest any further steps, if necessary. Updates will be provided accordingly.

Admittedly, there are a lot of what-ifs but we prefer to err on the side of caution.

A few others such as Nippon India Small Cap Fund, Franklin India Smaller Companies Fund and L&T Emerging Businesses Fund are also slowly becoming large. While there are no immediate concerns, one needs to watch out for such ‘large’ small cap funds given the risk associated with their growing asset size as highlighted.

This article was authored by Arun Kumar and Maulik Madhu.