This article was originally published in financial express. Click here to read it

Do you have a home loan outstanding or are you planning to take a home loan?

If ‘Yes’, do you really understand the nuances of how a home loan EMI works?

Let’s find out.

Try and answer these 3 questions.

Assume you have taken a home loan of Rs 50 lakhs at 8.50% interest for a tenure of 20 years with an EMI of Rs 43,391.

Question 1: In the first 5 years you would have paid a total EMI of ~Rs 26 lakhs (read as more than 50% of your original loan amount). How much of your principal loan amount have you repaid?

Option A – 30% to 40%

Option B – 20% to 30%

Option C – less than 15%

Question 2: For the 20 year home loan, how long does it take to repay 50% of the loan amount (principal)?

Option A – 10 years

Option B – 12 years

Option C – 14 years

Question 3: For the loan of Rs 50 lakhs, what is the total EMI amount that you pay over 20 years?

Option A – Rs 70 lakhs to Rs 80 lakhs

Option B – Rs 80 lakhs to Rs 90 lakhs

Option C – more than Rs 1 cr

Now let’s check if you got them right!

The correct answers are,

Question 1: In the first 5 years you would have paid a total EMI of ~Rs 26 lakhs (read as more than 50% of your original loan amount). How much of your principal loan amount have you repaid?

Correct Answer – Option C (less than 15%) – its actually 12%!!

Question 2: For the 20 year home loan, how long does it take to repay 50% of the loan amount (principal)?

Correct Answer – Option C (14 to 15 years)

Question 3: For Rs 50 lakhs home loan, what is the total EMI amount that you pay over 20 years?

Correct Answer – Option C (more than 1 cr) – its 1.04 crs

Surprised!

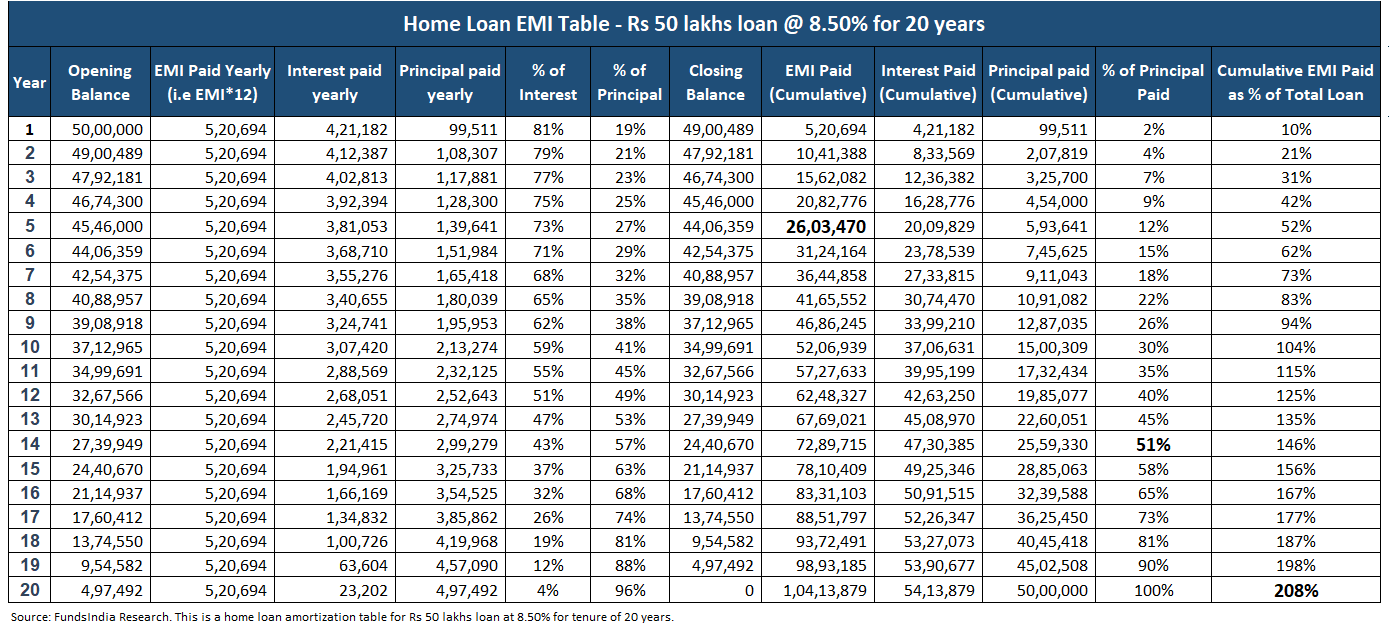

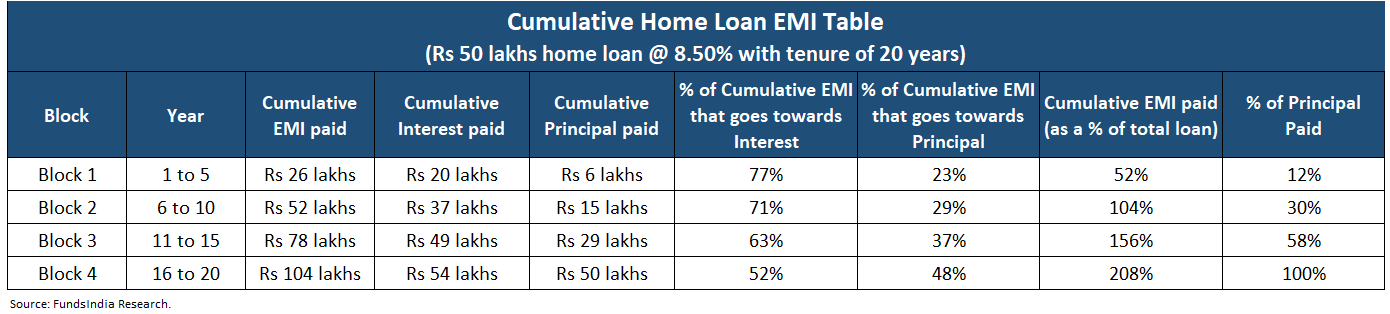

Here is the evidence – the Detailed Home Loan EMI table which shows the 20 year journey

*You can refer to the annexure section of the blog to understand the various columns

How does a home loan really work: 3 Surprising Insights!

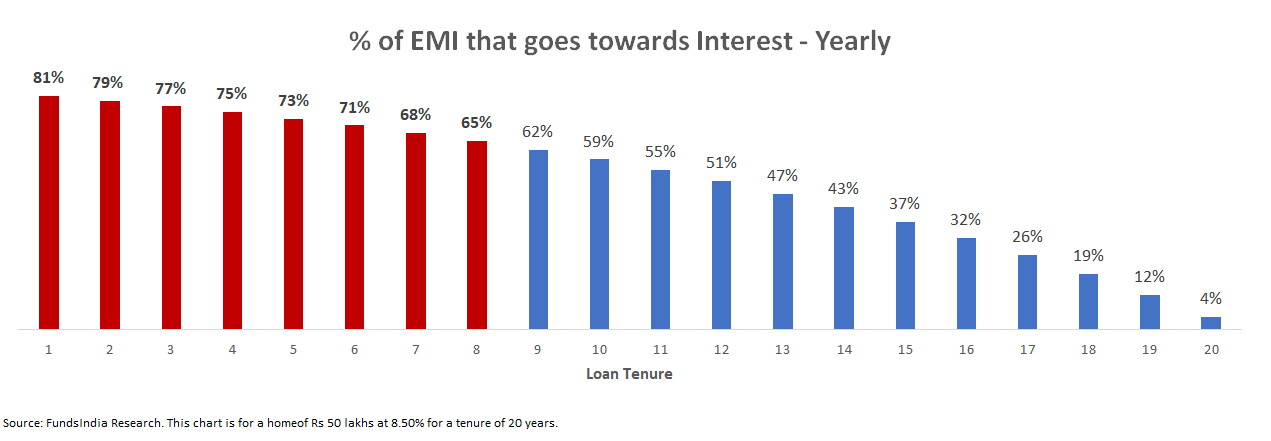

INSIGHT 1: During the initial years, most of your EMI goes only for interest payments!

Sample this.

For a Rs 50 lakhs home loan for 20 years at 8.5% interest rate…

- In the first year, out of Rs 5.20 lakhs that you paid as EMI, Rs 4.2 lakhs goes only towards Interest – a massive 81% of your yearly EMI!.

- 5 years later, the total cumulative EMI amount is Rs 26 lakh, out of which Rs 20 lakhs (77% of cumulative EMI) were only interest payments!

Why does this happen?

As seen from the chart below, a large percentage of your EMI in the initial years goes only towards Interest.

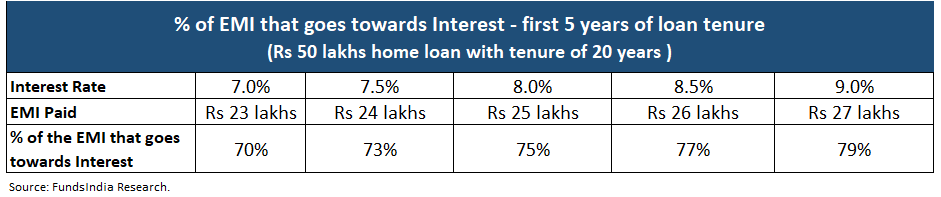

Does this hold true for different loan rates?

Yes it does. Historically, in India interest rates have been around 7% to 9%.

Assuming 7-9% home loan rates, around 70%-80% of the EMI that you pay in the first 5 years goes only towards Interest!

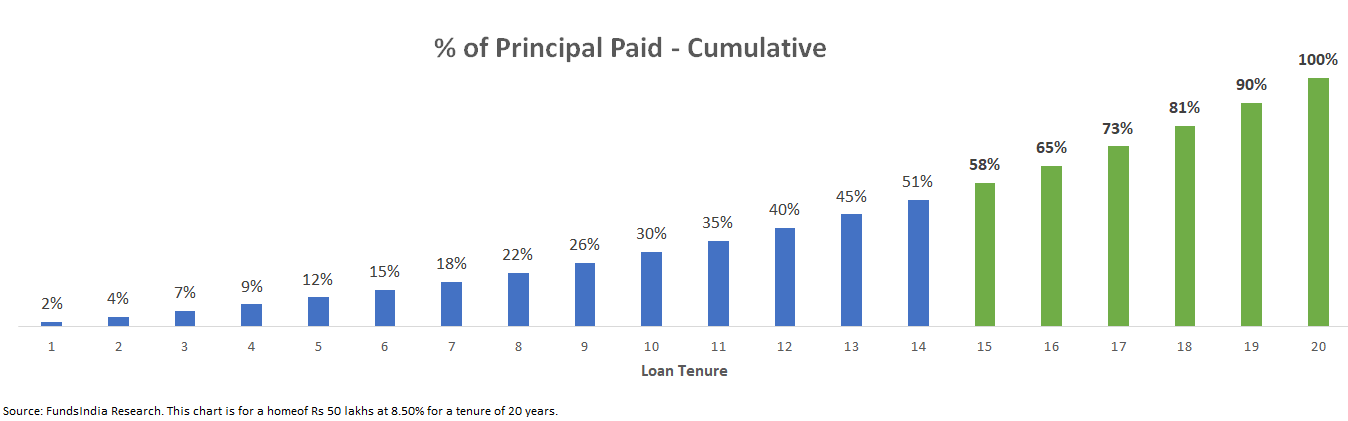

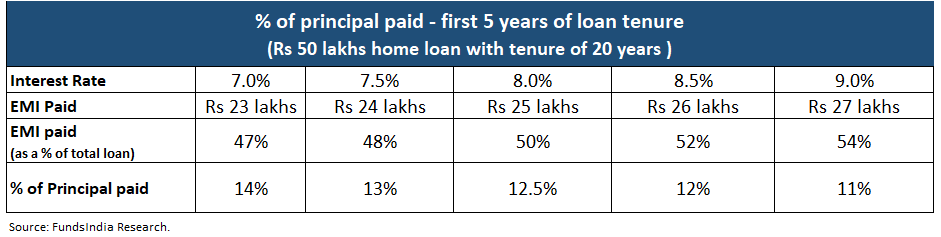

INSIGHT 2: While you pay off almost HALF of the loan amount as EMIs in the first five years, only 10-15% of the loan is paid off!

During the initial years of the loan tenure the contribution of EMI towards the Principal is low which means the loan amount (principal) repaid is also low.

In the chart below, for the same example of a Rs 50 lakhs home loan for 20 years at 8.5% interest rate, you can see how much of the original loan gets repaid cumulatively after every year.

Here comes the shocker…

In the first 5 years the principal repaid is only 12% despite paying off 50% of the home loan as EMIs!

Let’s check if this holds true for different interest rates (7% to 9%).

As seen above, this holds true across different home loan rates between 7%-9%.

Only 10-15% of the loan gets paid off the first 5 years despite paying off almost half the loan amount (45%-55%) as EMIs.

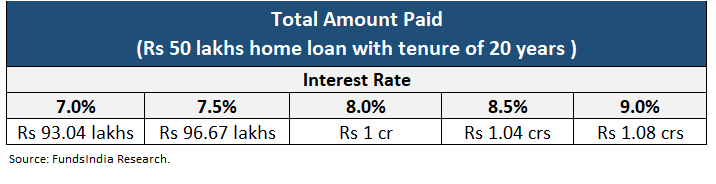

INSIGHT 3: You almost end up paying TWICE the original loan amount as EMIs for a 20-year home loan

While we regularly track the EMIs, Interest and Principal, what we usually overlook is the total amount that we have to pay for the home loan over the entire tenure.

For a Rs 50 lakhs home loan at 8.5% interest, you end up paying Rs 1.04 cr over 20 years – this is almost 2 times the loan amount!

Interest is more than the loan amount i.e. Rs 54 lakhs!

In the table below you can see that even at different home loan rates (7-9%), you still end up paying almost 2 times the original loan amount.

Understanding all the above 3 nuances of how a home loan really works, is important to ensure that you don’t get frustrated in the initial years.

3 Ideas to manage your home loan better

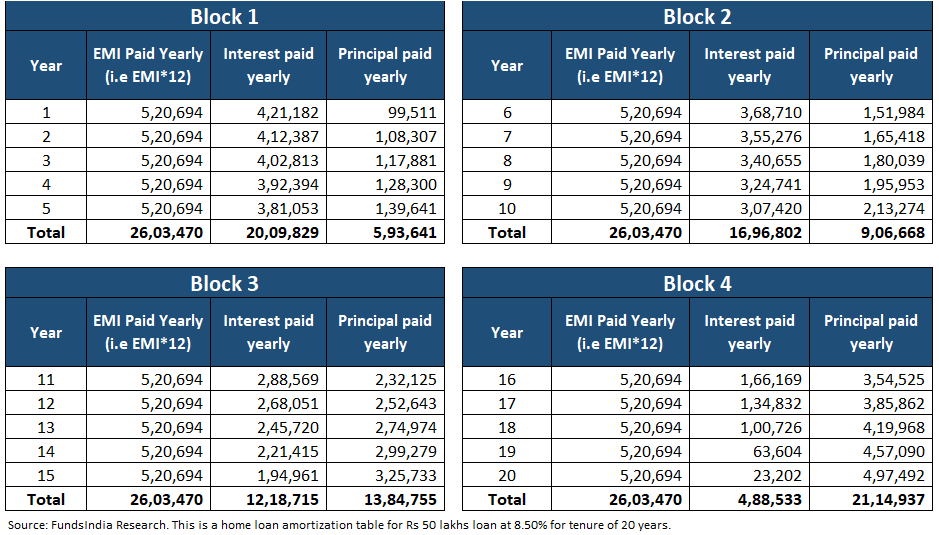

IDEA 1: Use 5 year cumulative blocks to understand how your home loan EMI is split across Interest and Principal

Assume you have a loan tenure of 20 years. To make it simpler, divide this into 5 year blocks (4 in this case) and summarize the cumulative totals.

This makes it easier and simple to understand the proportion of EMI that goes towards Principal vs Interest.

To calculate this, you can use the home loan EMI calculator here.

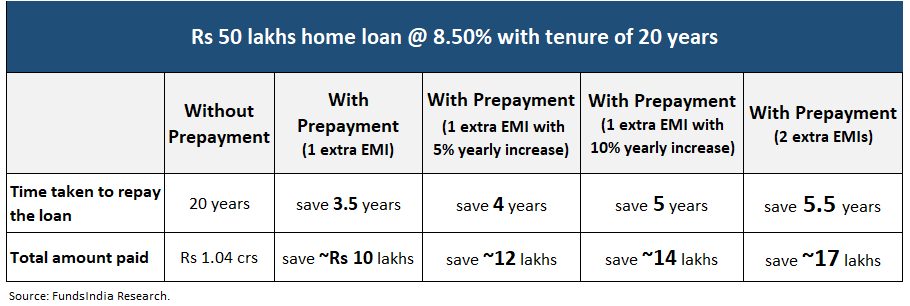

IDEA 2: Try to prepay in early years and increase your EMI every year in line with your salary increase

Since in the early years of loan tenure the majority of EMI goes towards interest, it is better to prepay some of your home loan in the initial years of the loan tenure which will help reduce the total amount paid (over the tenure for the loan) and shorten the loan tenure. Home loan prepayments simply mean you pay a certain portion of your loan amount earlier than the planned repayment period.

This can be done in two ways

- Increasing your EMI every year as your salary increases

- Prepay whenever you receive any lumpsum amount or bonus

How much of a difference does it really make?

- If you prepay 1 extra EMI every year, then your total EMI payments (over the loan tenure) reduce by almost 20% of the original loan amount.

- If you prepay 1 extra EMI and also increase this by 5% every year, then your total EMI payments reduce by almost 25% of the original loan amount.

- This gets even better if you are able to prepay more/increase the EMI.

In the table below we have compared the Rs 50 lakhs home loan assuming no prepayment, with prepayment and with yearly increase in prepayment.

IDEA 3: If home loan rates go up, don’t forget to increase EMI or Prepay to keep tenure constant

While taking a home loan we usually keep the prevailing home loan rate in mind and do not plan for situations like an increase in home loan rates. When interest rates go up, while your EMI remains the same, the banks increase the tenure of your loan.

So, whenever your home loan rates increase, don’t forget to increase your EMI or prepay – to keep your loan tenure the same.

Summing it up

- Understand these 3 nuances of a home loan EMI

- During the initial years, most of your EMI goes only for interest payments

- While you pay off almost HALF of the loan amount as EMIs in the first five years, only 10-15% of the loan is paid off

- You almost end up paying TWICE the original loan amount as EMIs for a 20-year home loan

- Use these 3 ideas to manage your home loan better

- Use 5 year cumulative blocks to simplify and understand how your home loan EMI is split across Interest and Principal

- Try to prepay in early years and increase your EMI every year in line with your salary increase

- If home loan rates go up, don’t forget to increase EMI or Prepay to keep tenure constant

Annexure:

Home Loan EMI table Glossary:

Opening Balance = loan outstanding at the start of the year

EMI paid yearly = yearly EMIs paid (monthly EMI * 12)

Interest paid yearly = from the yearly EMI, the amount that goes towards interest

Principal paid yearly = from the yearly EMI, the amount that goes towards principal

% of interest and % of principal = the proportion of EMI that goes towards interest and principal

Closing Balance = loan outstanding at the end of the year

EMI paid cumulative = total EMI paid till date

Interest paid yearly = total interest paid till date

Principal paid yearly = total principal paid till date

% of Principal paid = total principal paid till date as a proportion of loan outstanding

Cumulative EMI paid as % of total loan = total amount paid till date as a proportion of loan outstanding