The equity markets expressed its disappointment on Monday over the Bihar results, but recovered quite well from its lows on market close. If one observed, the markets may have been factoring this well ahead – suggested by a 4.2% fall in Sensex from the close of October 25 until November 6. Not much happened in the markets to trigger a fall in those 10 days but for the impending poll results.

Once again, this simply reiterates that markets are mostly proactive and not too reactive. That also means, as investors, instead of being reactive, we would do well to see if we can answer the ‘what next?’ question to ensure we are not behind the markets, even if we do not stay ahead of it.

So what would be the impact of the Bihar assembly elections on the market, and what should be your course of action?

No doubt, in the near term, the Bihar assempbly election results would have a near-term impact on market sentiments simply because it was expected to change the pace of reforms that could come about through legislations. It was expected to strengthen the ruling government’s count in the upper house (Rajya Sabha) of the parliament. However, on hindsight, it appears that the tally may not have been reached any which way unless the ruling alliance swept other upcoming polls such as West Bengal and Uttar Pradesh (in 2016 and 2017 respectively). The peculiar election process for the Rajya Sabha, and the mathematical difficulty of the ruling party to enjoy majority in Rajya Sabha means that it has to work outside of legislations for various reforms where key non-monetary bills are stymied by opposition.

Work-in-progress outside Parliament

The ruling government appears to be already on its way to do this, if recent events are anything to go by.

– Large-scale project clearances worth Rs. 4 lakh crore (over the past 6 months) clear up grounds to improve the pace of activity needed for an economic revival

– PSU bank recapitalisation (Rs. 70,000 crore), although not a panacea for public banks, provided the needed relief to recover from their immediate woes of NPAs

– The recent power distribution reform – Project UDAY – is a classic example of how the central and state governments can jointly address key pain points in the economy outside of parliament

– According to reports, the One-Rank-One Pension scheme will inject about $2 billion each in 2016 and 2017 (source BofAML), setting the pace for a consumption recovery

– The above could further be butressed by the Seventh Pay Commission; both of these consumption triggers being expected to directly boost GDP by 0.3%-0.5% (which is the payout expected as a percentage of GDP on account of pay hike) in 2016

Aside of the above, there have been reforms on the FDI front, besides other reforms such as coal auction; suggesting that while the government’s hands may be tied in passing bills, action outside the parliament has moved at a steady state.

The recent uptick in industrial production in September and October 2015 (October IIP was at a 3-year high of 6.4%) is also evidence to the fact that small-ticket reforms may be working in favour of reviving production. That of course is a key economic metric and boosts long-term recovery sentiments.

But the game of politics isn’t over yet. The ruling party would be more keen now than before to do all it can to clinch the large vote bank of Uttar Pradesh. Towards this, a rural stress may be inevitable, and it already appears to be moving its cards towards this aim. The Centre already hiked MSP for wheat by 5% last week and may well implement the Swaminathan Formula of hiking MSP ahead of Punjab and UP elections in 2017. The politics behind this notwithstanding, this could help consumption in rural regions.

While the work outside legislation may yield its results, key bills such as the GST and the land acquisition bill can continue to be dragged as opposition could well spoil the Winter Session of the parliament. This, together with the likelihood of the US Federal Reserve’s rate hike in December could be further near-term sentiment draggers for the market. Less significant sentiment dips in the form of the Swachh Bharat cess on service tax could also dampen market sentiments.

Meanwhile earnings numbers post the December quarter, and a possible rate cut in the Monetary Policy in February 2016, if the RBI’s CPI-target of under 6% is met in January, could be events that the market will watch with caution.

Take a look at the calendar of key events that the market would watch for and react over the next few months leading to the close of the fiscal.

Act when the market watches

As the above events unfold you would likely have more opportunities to average your long-term portfolios. As reiterated by us in our call on September 8(how to invest in a falling market) and September 23 (When the market gives you more time grab it), the time between September and February-March would provide ample opportunities to invest in a sideways moving market.

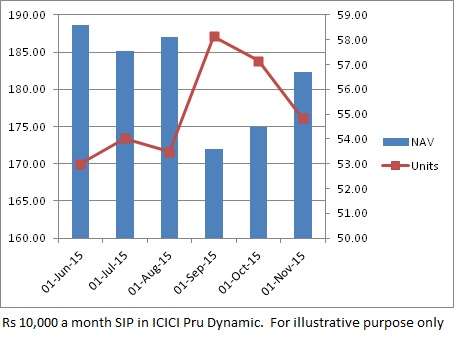

We had laid out strategies to invest in such markets in our September 8 call and would urge you to follow those. Just to illustrate how SIPs help accumulate more units in this market (the fund given below is for illustrative purpose only), take a look at the graph below.

Quite a few investors have expressed concern that their SIP returns (expressed in IRR) appear worse than one-time returns in the present market. In other words, the SIP portfolio suggests a steeper fall when annualised. Do note that it is merely because of your having bought units at much lower prices and the market not delivering yet.

Once the uptick happens, your SIP, as a result of lower cost, is likely to sport higher returns.

Be that as it may, if you look at it in absolute returns (without annualising), you will still note that the absolute SIP returns in the above fund illustrated, between June 1 and now would be 0.05% as against -3.7% if you had invested lump sum on June 1.

So this Diwali, while gold might seem to glitter under the cover of so many seemingly attractive government and private schemes, do know that true bargain hunting is where it glitters the least – and that is in equities now.

Happy Diwali and here’s wishing more bang for your buck!

A bright and prosperous Diwali to Team Fundsindia.

This is a well-timed, yet timeless article on the benefits of long term investing strategies. The analysis of the effects on the Bihar elections is pertinent in the current political and economic scenario . The article rightly illustrates how it makes sense to sow when the soil is ready, nurture the crop and gather the harvest when it matures. A farmer is uncertain about many outcomes yet he never ceases to sow and remain optimistic against all odds. Like agriculture, equity investing revolves around the virtues of seizing the opportunity, being persistent & patient, and reaping the rewards when it is ready. The article should be of immense value to those who are confounded by the election results.

A bright and prosperous Diwali to Team Fundsindia.

This is a well-timed, yet timeless article on the benefits of long term investing strategies. The analysis of the effects on the Bihar elections is pertinent in the current political and economic scenario . The article rightly illustrates how it makes sense to sow when the soil is ready, nurture the crop and gather the harvest when it matures. A farmer is uncertain about many outcomes yet he never ceases to sow and remain optimistic against all odds. Like agriculture, equity investing revolves around the virtues of seizing the opportunity, being persistent & patient, and reaping the rewards when it is ready. The article should be of immense value to those who are confounded by the election results.