Whenever you see your portfolio run up in a year such as the present one, your immediate reaction could be to remove some profits from the table.

However, if you randomly choose to sell funds based on the returns generated, and worse still, if you don’t reinvest them effectively, you may be doing more harm to your portfolio than you know. Here are a couple of things to keep in mind when you see your mutual fund portfolio run up.

Weed out erstwhile underperformers

We are consciously using the term ‘erstwhile’ because it is likely that the funds that were underperforming until early 2014 would now have bounced back and may seem healthy; so, you would no longer view it as an underperformer.

If you had funds that were falling steeply during the 2013 or 2011 market falls, or funds whose performance kept swinging from good to bad, or those funds whose strategy or objective no longer suits you, then a rallying market is a good point to weed out such funds. However, be careful with the following:

– First, make sure you have identified the weak link. Else, seek your advisor’s help (At FundsIndia, you can always email or call your advisor to seek a portfolio review). This is because usually, the first impulse would be to sell funds that currently seem mediocre, but are actually consistent performers.

Just to give an example, a large-cap fund that is usually a consistent performer might seem to lag some of your diversified or mid-cap funds at this point. That does not mean you exit it. While in a rallying market mid-cap funds may seem to outperform, you need the support of large caps in a volatile market and also over the long term. Hence, make sure you are exiting the fund for the right reasons.

– Second and more importantly – REDEPLOY. Unless you intended to take out money in any case, or you need the money badly, you could do much harm to your goal and to your portfolio by removing money midway.

This is very true if you have a long-term portfolio. If you remove even a fifth of your money and do not reinvest it, if it earns about 12 per cent annually, you could easily manage 25 per cent more corpus than what you ended with, had you left the money invested for five years.

Look at portfolio allocation, not just portfolio returns

When you have an asset allocation: If you have a well constructed portfolio without any dud funds, but you feel your portfolio looks inflated, then give it a proper check. Do not simply go by how much your portfolio returned – it could be up by 30 per cent, or 40 per cent, or even more. But that does not automatically mean your portfolio is inflated.

If you have your money allocated across equity and debt, then the right thing to do would be for you to see how much your equity has run up against the other asset classes you hold – debt or gold. For instance, if you started out with a 70:30 allocation to equity funds and debt funds and the proportion now is say 72:28. Your overall allocation has not been disturbed much. In other words, your equity is not as inflated as you think it is. In general, a change of 5 percentage points or more can be a base for you to reallocate money.

So what should you do if the change in allocation is indeed high? The most desirable thing for you to do would be to not disturb the existing portfolio, but bring in more money to ensure that the allocation is back to where it was.

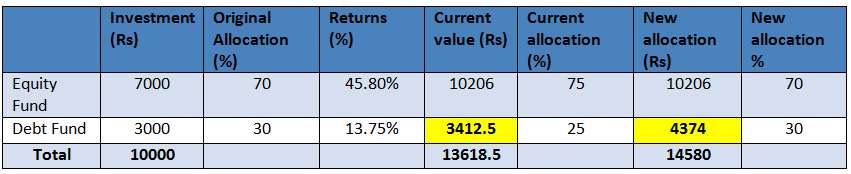

For instance, if you had a 70:30 allocation (say Rs 1 lakh) in equity and debt, and that has climbed to say 75:25. Then, you would have to deploy more money in the undervalued asset class (debt in this case) to ensure the original allocation.

See the illustration below. In this case, you additionally invest only about Rs 1,000 in debt to ensure that you rebalance. But if you cannot plough fresh money, then you would have to book some profits in equities and redeploy the rest in the debt fund.

That would mean having the same Rs 13,618 as your current value of investment. Of course, this may entail capital gains when you try to sell equity funds in less than a year. This is why it is desirable to bring in more money if you wish to rebalance a portfolio that is too young.

If you find that too complicated, you have FundsIndia’s offerings such as Smart Solutions, which will not only help you do the math, but will ensure you rebalance in the right funds.

When you do not have an asset allocation: If you are a long-term investor, why should you be bothered about your ‘fund’ running up? Let’s get this straight: When stocks run up sharply and appear overvalued, it does make sense to book some profits as the upside potential may be limited and you may miss out on opportunities elsewhere.

But a mutual fund is not a single stock. It is a portfolio of stocks and the fund manager knows too well when stocks do run up. That means, he/she is constantly keeping an eye on valuations and upside potential, pruning/booking profits, and looking for new opportunities.

In other words, the fund manager is constantly doing the job of booking profits and redeploying. So, why would you want to replicate what the fund manager is doing, especially if you think you have a well-managed fund?

If the idea of your taking profits off the table is to reallocate to other asset classes (which we just discussed above), then fine. Otherwise, if you are invested in an equity fund to get ‘equity’ exposure for the long term (more than five years), and the fund does that for you, you have little reason to bring it to cash.

Remember, funds themselves move some of their assets to cash when they either find the market overvalued or turbulent. So they still do the job for you. More importantly, chances are, they know better than us to redeploy them quickly when the opportunity arises.

This being the case, the best thing to do if you have a long-term time frame without any need for the money, is to let your portfolio be. But if you feel like the entire equity market has run up and there could be very little opportunities for fund managers to deploy your money effectively, then you may consider selling a part of your fund’s holding and moving to some short-term debt fund. If you are savvy enough, redeploy them on equity market dips. But we would not bet on this strategy.

To sum up:

– Use the run up to exit the poor performers in your portfolio, and reinvest them right away in the other good funds you have. Remember, you do not run the ‘timing’ risk if you redeploy immediately as you are shifting from one equity fund to another one – it is the same asset class. You face the risk of ill-timing if you postpone.

– Look at your asset allocation change and not just the returns on your portfolio before deciding whether your equity or debt fund has run up too much.

– If you do hold only equity funds and have no use for the money in the near to medium term, unless you can find an asset class that can deliver superior returns, booking profits would only mean losing out on returns and disrupting compounding of wealth.

– With falling interest rates in traditional debt options such as fixed deposits, you run the reinvestment risk by booking out from equities, unless you need the money over the course of the next one year.

Hi Vidya

Very good blog on staying invested for a long term despite the volatility with the power of compounding. I think this blog will be very useful for investors like me who are investing in mf’s with the long term financial goals either in large cap or large and midcap that does’nt make big difference, one should stick to disciplined way of investing through SIP without bothering the volatility.

Hi Vidya

Very good blog on staying invested for a long term despite the volatility with the power of compounding. I think this blog will be very useful for investors like me who are investing in mf’s with the long term financial goals either in large cap or large and midcap that does’nt make big difference, one should stick to disciplined way of investing through SIP without bothering the volatility.