With the tax-saving season in, we’d like to highlight two funds that are good to have in your tax-saving portfolio. But before we do that, here are a few things worth taking note of to ensure you make smart choices.

What you need to know this tax-saving season

Increase in limit: You can now claim Rs 1.5 lakh as deduction from your total income under Section 80C of the Income Tax Act, instead of the earlier limit of Rs 1 lakh. That means, if you come under the 30 per cent tax bracket, you can save about Rs 15,000 more. The new ‘maximum’ that you can save under 80C is thus Rs 45,000. Make the most if it.

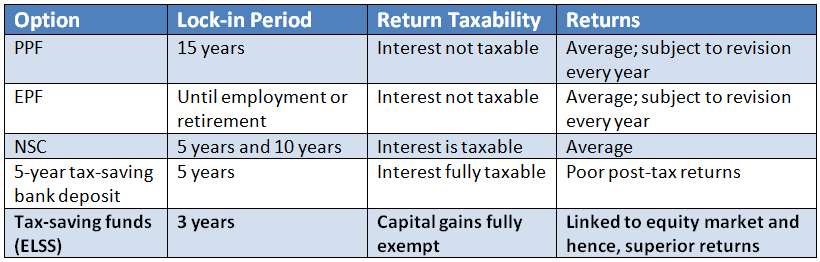

For those of you looking at traditional options of investing the additional limit now allowed, here’s what you need to know about how they work for you, before you decide to increase those investments.

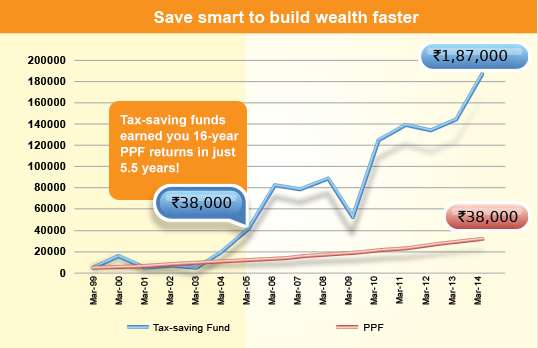

Traditional options are also not great wealth builders, if you look at historical performance. Here’s an illustration that will tell you how efficiently you build wealth with a tax-saving fund, instead of traditional options such as PPF.

In the illustration, you will see Rs 10,000 invested in a PPF and in the ICICI Pru Tax Plan. Rs 38,000 built over 16 years in a PPF took just 5.5 years to accumulate with ICICI Pru Tax Plan!

Actual rates of PPF taken. ICICI Pru Tax Plan was launched in August 1999. Past returns are not indicative of future performance. PPF is a 15-year investment product but earns interest up to its 16th year. Hence, investment comparison has been done on a similar basis.

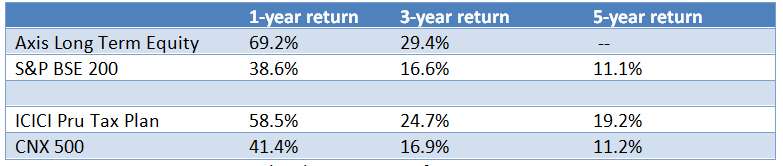

The table and graphics earlier will tell you enough about how tax-saving funds compare with traditional options. Here are two funds that we chose based on their consistent performance and quality of portfolio.

Launched in 2010, this fund delivered the best risk-adjusted returns in the last three years. Ability to contain volatility, willingness to quickly increase cash when markets are turbulent and readiness to also up mid-cap exposure a bit in rallying markets such as the present one has made Axis Long Term Equity among the most noticeable funds in the tax-saving space.

Axis Long Term Equity has an enviable record of beating its benchmark, S&P BSE 200, 100 per cent of the times on a daily rolling one-year return basis over the past three years.

Such consistency was possible with a two-pronged approach. One, holding a reasonably defensive sector strategy that contained volatility; two, very adept stock picking that stemmed from a pure bottom up investing approach.

Apart from high exposure to banking and finance, the fund has, over the course of the last one year, continued to prefer relatively defensive sectors such as IT and pharma. That it managed to hold to this strategy and still deliver at a time when cyclical sectors outperformed, speaks of its stock-picking prowess.

For instance, in the mid and small-cap segment, stocks such as Symphony, Speciality Restaurants and Astra Microwave Products have worked well for the fund, although none of these would quality as sector calls.

The fund is managed by Jinesh Gopani.

Returns over 1-year are annualised. Returns as of November 7, 2014

Had you put Rs 1 lakh in this fund 10 years ago, your money would have grown over 7 fold – to Rs 7.25 lakh. This is a classic example of how a tax-saving fund can help build wealth in the long term. Since there are not too many tax-saving funds with a 10-year plus record, you may not have realised the power of compounding in these funds.

ICICI Pru Tax Plan is a more aggressive fund compared with relatively less flashy ones such as Franklin India Taxshield. But like Axis Long Term Equity, this fund too sport a large-cap tilt; in fact, close to three fourth of its assets are currently in large-cap stocks.

But ICICI Pru Tax Plan is known to take exposure to mid-cap segments in earlier bull markets. Its overall correlation to the broad markets is therefore higher than Axis Long Term Equity.

The fund is best suited for longer periods or for investments through SIPs. In fact over a 10-year SIP, the fund scores the best among funds with a similar long-term track record.

Unlike Axis Long Term Equity, ICICI Pru Tax Plan has overweight exposure to cyclical sectors such as energy. It is, therefore, suitable for those looking for more aggressive exposure to the equity market.

Tips for investing in tax-saving funds:

– Unless performance sags, continue with the same fund for your tax-saving need every year. There is no need to add new funds every financial year.

– While the lock in for tax-saving funds is only three years, view them as any other equity fund and hold them for not less than 5 years, or until you actually need the money for any goal.

– If you are at the beginning of your career, use an SIP to invest in tax-saving funds. They will serve you the purpose of saving tax and building wealth for the long term, if you do not have too much surplus to invest separately.

Is it advisable for an individual in mid 50s to invest in ELSS to save tax?

Hello sir, it depends on your risk appetite. If you can afford to hold the money for at least 5 years and are ok with equity risks, you should do fine. thanks, Vidya

Thank you madam for the reply. I think it is better to invest in ELSS than to invest in real estate to save tax

Is Aviva I Growth ULIP plan is good to invest, I have invested 3000 rs/ month SIP in it, just want to know if it is good for the better returns and tax saving if not then where I can invest this amount. Please advise.

Hello Nitin, I do not analyse ULIPs to comment on individual ULIP performance. Having said that, we are also not fans of ULIPs as we think investment and risk cover should be separate. if you have access to the returns that this ULIP has made and know how much goes out as charges and how much of your money is invested (you can ask your agent to disclose all this), then compare it with MF and see where it stands. A simple tax-saving fund (ELSS) where the investment and NAV and portfolio is transparent is a good choice if you want to use equity for 80C tax-saving purpose. regards, Vidya

hi madam, thanks for your article …..i came across ur blog few days back while searching for some good blogs on ELSS

i have a query regarding dividend options on ELSS. Actually i want to invest 80000rs in ELSS as a lump sum investment to save my taxes for this financial year and I’m confused between dividend and growth option in ELSS, and my point (please correct me if I’m wrong) is as the market is very much high no one can say where it will go in future 3-5 years and more likely it will correct itself to some lower level than today so dividend option should be better as it is paid on regular basis every year and i have seen the records that most of the ELSS funds have given dividend in last 10 years regularly . So if market corrects then also i will get some money atleast that will give me some encouragement while in growth plan , my capital will be eroded if market corrects yo lower level as happened in 2008 & again in 2011

…however returns will be same for both so difference is only of mental peace here. I have pretty bad experience with hdfc taxsaver growth taken in 2011 that gave me almost negative return when i redeemed it after 4 years while during the same period canara robeco equity tax saver dividend provided positive return with 565 rs dividend paying every year during that period.

So please guide me regrading my dilemma… I have read ur blog on growth vs dividend march 2013 and i have started SIP of 3000/- each in reliance tax saver fund and Axis long term equity tax saver for the next financial year..

I am extremely sorry as the post is getting very much lengthy and boring.

thanks once again

.

Hello Anuj,

Appreciate the time taken for posting on our blog. A few things:

1. dividend payout and growth are not the same. Yes, the scheme and performance is the same and websites show the returns to be the same. But since you take the dividend out and do not invest, you do not allow compounding to happen. To that extent you do lose. Growth helps compounding while dividend payout helps take some profits off the table. If you prefer to take out money and not wait for compounding to work over long term, then dividend payout can be your choice.

2. While ELSS has a 3-year lock in, like all other equity products it is meant for the long term. In our opinion, you should treat such funds as long-term equity and hold for not less than 5 years. If investors are willing to hold products like PPF for 15 years, then for superrior yielding products, holding long provides more benefits. If the market volatility troubles you, start SIPs in ELSS in the early part of the financial year so that you invest enough for your tax-saving purpose.

3. If you had invested lump sum amount in the said ELSS in 2011 and redeemed after 4 years..you must have redeemed sometime now. We checked the returns over that period. It is not negative. In fact it is in double digits. It is possible you took the NAV post dividend payout to calculate the returns.

Thanks,

Vidya

Hi Vidya,

This is Ram and my age is 29.

Actually, I am planning to invest 1 lakh into ELSS fund per every year (more than 10 yrs).

Can i invest into two funds or maintain one fund?

1. ICICI Pru Tax plan (G) — 70K

2. Reliance Tax saver (G) — 30K

Could you please suggest me apart from these funds if above funds aren’t right choice.

My proposed portfolio:

PPF – 75K

ELSS – 1Lakh

Please let me know, whether my portfolio is fine or not?. Thanks.

Regards

Ram

Hi Ram, Sorry my response was posted under a wrong id.

the 2 fund choice looks fine. But review your fund choice every year, esp Reliance TAx Saver is an aggressive fund and during market falls may be hurt. I hope you are aware that you will invest Rs 1.75 lakh for tax purposes, although you get benefit for Rs 1.5 lakh. If you are ok because it is still an investment fine. In future, kindly write to us through the advisor appointment feature when yo click the help tab in your account. This will help us track your query and respond promptly. Since you are investing as lump sum , do not panic if there are short-term dips. Also although ELSS lock in is 3 years, have a 5 year view at least before you redeem any part of the amount. regards, Vidya

Hi Vidya,

Thanks for your response.

Actually, I have account in your FundsIndia portal and also started investing in ICICI Pru Tax plan (ELSS) in your portal.

Thanks.

Ram

Hello Ram, Yes, I did check that :-); which is why I wanted you to write to us through your account, so that your queries will be tracked and responded sooner than in a blog, which is a public forum 🙂

regards, Vidya

One can also consider Quantum Tax Saving Fund. It has VRO rating of 3. It has low expense ratio. Though the returns are less as compared to Axis long term equity and ICICI Pru tax, conservative investors can consider adding it to their portfolio.

Hi Vidya, Myself Pankaj. My approximate salary upto march 2015 would be rs 4,50,000 INR. I wanted to invest in somewhere to secure my future with good returns. Which one will be the best according to you ???

Hello Pankaj,

Mutual funds are good options for long-term investments. Please open your FundsIndia account, to allow us to help you with palnning your investments. Yo can ask our advisor any query once you finish the account opening. thanks, Vidya

Hi Vidya,

This is a very nice article. Tax saving mutual funds are really good and better than any other guaranteed investment options for a long term. People are really interested these days to invest in mutual fund.

Hi Vidya,

This is a very nice article. Tax saving mutual funds are really good and better than any other guaranteed investment options for a long term. People are really interested these days to invest in mutual fund.

Is it advisable for an individual in mid 50s to invest in ELSS to save tax?

Hello sir, it depends on your risk appetite. If you can afford to hold the money for at least 5 years and are ok with equity risks, you should do fine. thanks, Vidya

Thank you madam for the reply. I think it is better to invest in ELSS than to invest in real estate to save tax

Is Aviva I Growth ULIP plan is good to invest, I have invested 3000 rs/ month SIP in it, just want to know if it is good for the better returns and tax saving if not then where I can invest this amount. Please advise.

Hello Nitin, I do not analyse ULIPs to comment on individual ULIP performance. Having said that, we are also not fans of ULIPs as we think investment and risk cover should be separate. if you have access to the returns that this ULIP has made and know how much goes out as charges and how much of your money is invested (you can ask your agent to disclose all this), then compare it with MF and see where it stands. A simple tax-saving fund (ELSS) where the investment and NAV and portfolio is transparent is a good choice if you want to use equity for 80C tax-saving purpose. regards, Vidya

Hi Vidya,

This is Ram and my age is 29.

Actually, I am planning to invest 1 lakh into ELSS fund per every year (more than 10 yrs).

Can i invest into two funds or maintain one fund?

1. ICICI Pru Tax plan (G) — 70K

2. Reliance Tax saver (G) — 30K

Could you please suggest me apart from these funds if above funds aren’t right choice.

My proposed portfolio:

PPF – 75K

ELSS – 1Lakh

Please let me know, whether my portfolio is fine or not?. Thanks.

Regards

Ram

Hi Ram, Sorry my response was posted under a wrong id.

the 2 fund choice looks fine. But review your fund choice every year, esp Reliance TAx Saver is an aggressive fund and during market falls may be hurt. I hope you are aware that you will invest Rs 1.75 lakh for tax purposes, although you get benefit for Rs 1.5 lakh. If you are ok because it is still an investment fine. In future, kindly write to us through the advisor appointment feature when yo click the help tab in your account. This will help us track your query and respond promptly. Since you are investing as lump sum , do not panic if there are short-term dips. Also although ELSS lock in is 3 years, have a 5 year view at least before you redeem any part of the amount. regards, Vidya

One can also consider Quantum Tax Saving Fund. It has VRO rating of 3. It has low expense ratio. Though the returns are less as compared to Axis long term equity and ICICI Pru tax, conservative investors can consider adding it to their portfolio.

One can also consider Quantum Tax Saving Fund. It has VRO rating of 3. It has low expense ratio. Though the returns are less as compared to Axis long term equity and ICICI Pru tax, conservative investors can consider adding it to their portfolio.

Hi Vidya,

Thanks for your response.

Actually, I have account in your FundsIndia portal and also started investing in ICICI Pru Tax plan (ELSS) in your portal.

Thanks.

Ram

Hello Ram, Yes, I did check that :-); which is why I wanted you to write to us through your account, so that your queries will be tracked and responded sooner than in a blog, which is a public forum 🙂

regards, Vidya

hi madam, thanks for your article …..i came across ur blog few days back while searching for some good blogs on ELSS

i have a query regarding dividend options on ELSS. Actually i want to invest 80000rs in ELSS as a lump sum investment to save my taxes for this financial year and I’m confused between dividend and growth option in ELSS, and my point (please correct me if I’m wrong) is as the market is very much high no one can say where it will go in future 3-5 years and more likely it will correct itself to some lower level than today so dividend option should be better as it is paid on regular basis every year and i have seen the records that most of the ELSS funds have given dividend in last 10 years regularly . So if market corrects then also i will get some money atleast that will give me some encouragement while in growth plan , my capital will be eroded if market corrects yo lower level as happened in 2008 & again in 2011

…however returns will be same for both so difference is only of mental peace here. I have pretty bad experience with hdfc taxsaver growth taken in 2011 that gave me almost negative return when i redeemed it after 4 years while during the same period canara robeco equity tax saver dividend provided positive return with 565 rs dividend paying every year during that period.

So please guide me regrading my dilemma… I have read ur blog on growth vs dividend march 2013 and i have started SIP of 3000/- each in reliance tax saver fund and Axis long term equity tax saver for the next financial year..

I am extremely sorry as the post is getting very much lengthy and boring.

thanks once again

.

Hello Anuj,

Appreciate the time taken for posting on our blog. A few things:

1. dividend payout and growth are not the same. Yes, the scheme and performance is the same and websites show the returns to be the same. But since you take the dividend out and do not invest, you do not allow compounding to happen. To that extent you do lose. Growth helps compounding while dividend payout helps take some profits off the table. If you prefer to take out money and not wait for compounding to work over long term, then dividend payout can be your choice.

2. While ELSS has a 3-year lock in, like all other equity products it is meant for the long term. In our opinion, you should treat such funds as long-term equity and hold for not less than 5 years. If investors are willing to hold products like PPF for 15 years, then for superrior yielding products, holding long provides more benefits. If the market volatility troubles you, start SIPs in ELSS in the early part of the financial year so that you invest enough for your tax-saving purpose.

3. If you had invested lump sum amount in the said ELSS in 2011 and redeemed after 4 years..you must have redeemed sometime now. We checked the returns over that period. It is not negative. In fact it is in double digits. It is possible you took the NAV post dividend payout to calculate the returns.

Thanks,

Vidya

Hi Vidya, Myself Pankaj. My approximate salary upto march 2015 would be rs 4,50,000 INR. I wanted to invest in somewhere to secure my future with good returns. Which one will be the best according to you ???

Hello Pankaj,

Mutual funds are good options for long-term investments. Please open your FundsIndia account, to allow us to help you with palnning your investments. Yo can ask our advisor any query once you finish the account opening. thanks, Vidya