Within the past week, I had at least three questions on funds’ Net Asset Values (NAVs) from investors. I knew we were back to the 2006-07 days of people viewing mutual funds like stocks when it came to buying and selling them. If you are a new investor, or if you’ve been misguided into believing that mutual fund NAVs are to be viewed like stock prices, here are three myth busters that will help you choose wisely and invest optimally in mutual funds.

Within the past week, I had at least three questions on funds’ Net Asset Values (NAVs) from investors. I knew we were back to the 2006-07 days of people viewing mutual funds like stocks when it came to buying and selling them. If you are a new investor, or if you’ve been misguided into believing that mutual fund NAVs are to be viewed like stock prices, here are three myth busters that will help you choose wisely and invest optimally in mutual funds.

Myth #1: Lower NAV is better than higher NAV – The first question some people ask, when you tell them about a fund is – “What is its NAV? Is it lower than XXX fund?” This is the last thing that should matter.

A fund’s NAV could be lower than its peer for two reasons: one, it is a more recent fund compared with the peer; two, it has not performed as well as the peer. In rare cases, the face value may have changed. But it ends there.

Let us look at an example. There are two funds – one with an NAV of Rs 20, and the other with an NAV of Rs 50. Suppose you had Rs 10,000 to invest. You would have got 500 units of the former and just 200 units of the latter.

If you thought you were poorer with the second fund, hold on. If both the funds delivered 20 per cent in a year’s time, the first fund’s NAV would have grown to Rs 24 and the second fund to Rs 60. Now, multiply the units under each fund by their NAVs and your money would stand at Rs 12,000 either which way.

Then there are others who will argue that more units would mean more dividends. This is also a myth. First, mutual funds are not required to declare dividends regularly. Two, the dividend is only stripped from your own NAV (your gains) and given. So a higher NAV fund may provide you with a high dividend per unit than the lower NAV fund. Hence, that argument does not hold water.

Now, the above explanation is something you can come across when you simply research online. It is more important for you to understand the reason why the value of the NAV does not matter.

A mutual fund’s NAV, unlike a stock’s NAV, does not reflect the underlying fundamentals / valuations of a company. Rather, its gain is reflective of the overall performance of the stocks in its portfolio.

Also remember, when a fund feels it has gained sufficiently from a stock and sees limited upside, or feels that a stock’s prospects are stunted, it books profits / sells those stocks and moves to other stocks in its universe. Hence, the NAV is not reflective of how cheap or expensive the stocks in its portfolio are.

What matters to you in a fund’s NAV is the gain you made, irrespective of the price at which you entered. And need I say, the longer you stay invested, the better the chances of gains that will build your wealth. NAV and units should simply be viewed as a convenient way to segregate investors’ money and disclose the gains for each investor from the overall pool.

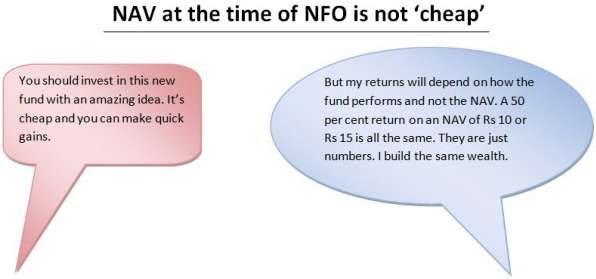

Myth #2: NFOs provide quick gains – It follows from the above points that an NAV of Rs 10 does not make a New Fund Offer ‘cheap.’ But just as NAV prices are wrongly equated to stock prices, NFOs are seen as stock IPOs. Initial Public Offers (IPOs) are companies that are listed in the stock market for the first time. Hence, their value would not have been discovered by stock market forces until then.

Institutional investors and retail investors participate in the IPO, in what results in a sort of price discovery for the company. At the time of listing, when investors perceive value in such companies, there could be more demand, causing the stock to rise sharply. This, many perceive as quick gains (though in reality, most retail investors enter late and do not gain much).

Such a story is simply not possible with NFOs. Why? Because there is no track record, no fundamentals of underlying portfolio and no investment in companies at the time of the NFO.

When a fund comes out with an NFO, it is simply collecting money from you, pooling it for the purpose of investing in stocks or debt instruments. The fund’s Scheme Information Document states an objective and a specific strategy it seeks to follow to achieve such an objective; nothing more.

Except in the case of a fund of fund where the underlying parent fund may have a track record to check, none of the NFOs have any track record of performance to look for.

The Rs 10-NAV is simply a starting point to allot units to you. There is no ‘underlying value’ to the Rs 10; unlike a stock, where the offer price can be related to a ‘valuation’ that investors are willing to give it.

Long story short, a Rs 10-NAV is simply a price to start with. Where the fund will invest in, and how they perform would speak of actual performance. And remember, the money would be deployed in stocks that are already in the stock or debt market. Hence, there are no ‘quick gain’ opportunities that are exclusive to the NFO.

As an investor, see if the theme or strategy of the NFO is unique, or if you find new potential (that is not available in existing funds) in it, or like the fund manager’s track record. These should be the factors you consider and not the NAV of the fund.

Myth #3: A fund that pays dividend is better – Some of you may think that you’ve got a bang for your buck when you get a dividend as soon as you buy into a fund. In reality, what happens is that a part of your money is returned soon after you invest.

This is one among the many misconceptions surrounding a fund when it comes to dividend and the fund’s NAV. For one, many investors believe dividends are the actual returns from a fund, like the way interest is to a deposit. Hence, higher the dividend, the better it is. This is a misconception.

Dividends are nothing but a part of the gains in your NAV that is given back to you in the form of cash (payout), or units (dividend reinvestment). That means you are not getting anything over and above what your fund has earned. No free lunches here.

In fact your NAV falls to the extent of the dividend that is given out. In the case of debt funds, the dividend distribution tax is also reduced from the NAV.

Two, some investors believe that the NAV under dividend option is cheaper. It follows from the first point above that the NAV falls after every dividend is declared. Hence, the NAV will seem low compared with the growth option where the profits of the fund are added to your NAV and not stripped.

Three, funds are not mandated to pay regular dividends. Some funds may pay out more if they think markets have run up a bit and others may strive to give periodic gains by way of dividends. But remember, dividend pay outs, especially when it comes to equity funds, do not allow you to build wealth efficiently as it simply sits in your savings account and does not redeployed.