For all those who think equities are too risky to handle, or who think it cannot deliver enough, here’s why your portfolio cannot do without equities, if you have to beat inflation, build a decent corpus for the long term and be tax efficient. I am going to take the approach of debunking your notions about other asset classes when it comes to their risks and return.

Your Savings

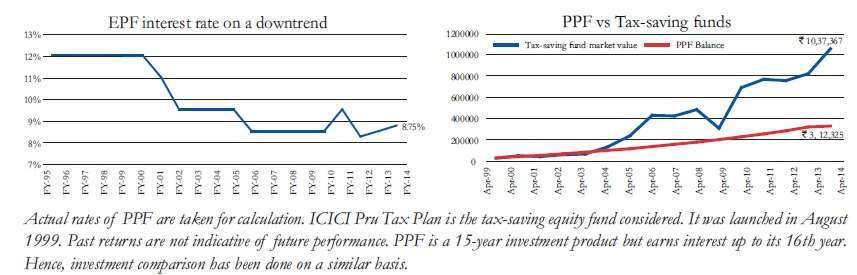

EPF and PPF: For most salaried individuals, your Employee’s Provident Fund (EPF) would be your compulsory saving. A few of you may also add the Public Provident Fund (PPF) as a part of your tax-saving investment and believe these two should take care of your non-income earning future.

While these can be great saving habits, sadly, they will simply not suffice to build you a decent investment kitty in your retirement years. For one, the interest rates on EPF have been on a steady decline over the past 20 years, hardly keeping pace with inflation, especially in recent years.

For instance, annual Consumer Price Inflation (industrial workers) was 9.5 per cent on an average over the last five years. That means, except in FY-11 when EPF rates were 9.5 per cent, for the rest of the years, you would actually have earned real negative returns (that is adjusted for inflation, your returns are negative)!

Your PPF rates too have been on a similar downtrend. The accompanying graphic shows how much Rs 10,000 invested every year in PPF would have delivered as compared to a similar investment in a tax-saving fund – ICICI Pru Tax Plan. The difference is stark, enough for you to realise how little you build with traditional options.

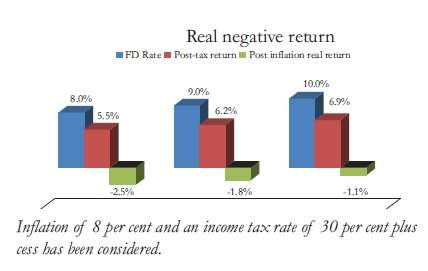

Deposits: When it comes to other voluntary savings that you make, bank deposits are likely to be on the top of your list. Not only are deposits tax inefficient, they are also likely to give you real negative returns – that is not give you anything over inflation.

The accompanying graph shows the three scenarios of Fixed Deposit (FD) returns – with an interest rate of 8, 9 and 10 per cent per annum. We have assumed a tax slab of 30 per cent and inflation of 8 per cent. You will see that the FD does not beat inflation even with a rate as high as 10 per cent.

The accompanying graph shows the three scenarios of Fixed Deposit (FD) returns – with an interest rate of 8, 9 and 10 per cent per annum. We have assumed a tax slab of 30 per cent and inflation of 8 per cent. You will see that the FD does not beat inflation even with a rate as high as 10 per cent.

Your Investments

Property: Multi-baggers in real estate are not uncommon to hear. You may have probably heard of people saying that their property value doubled or tripled.

But very likely the person who sold it would not have told you over what period the money doubled. So what, equities hardly make that, you might think. They probably delivered just 15 percent compounded annual returns in five years.

Did you convert that into money terms? It means your money actually more than doubled in five years! So often times, the notion of returns in real estate is partly overdone.

Also, remember, your confidence in real estate stems from not knowing information as compared to an overload of information with equities.

Just in case you wish to know the short-term returns of real estate, go to the National Housing Bank (NHB) website and see the property price index called Residex.

If you take the average returns from property in the top 15 cities over the past three years (ending March 2014), it’s a mere 5.3 per cent annually! Surprised? An investment in any top quartile equity fund over the same period (which was among the worst period for equities) would have delivered 12 per cent annually!

You’re better off not knowing too much information on your property price isn’t it? Try it with equities too!

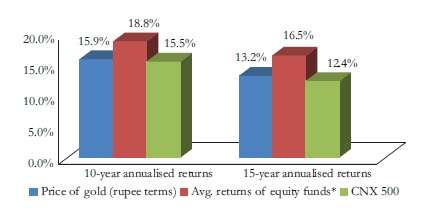

Gold: Agreed almost the whole of last decade was a period of extraordinary returns for gold, with the yellow metal delivering as much as 15.8 per cent annually (MCX prices). But then, do remember, almost seven out of those 10 years were periods of global turmoil and slow recovery, which is when gold is perceived as a safe haven and more takers flock to it, thus pushing up price.

Still, take a look at how gold prices stacked up against the return of equity funds.

Still, take a look at how gold prices stacked up against the return of equity funds.

Remember, gold too goes through cycles and if the last one year’s indications are anything, it may be going through low patches.

Your Wealth Creator

Equities: Ok, I am not going to again draw a chart showing you the returns made by equities in the long run. You would have seen it everywhere, but they may have seldom convinced you.

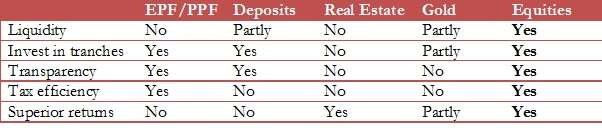

Unless you have hit a jackpot, which asset class can provide you with liquidity, convenience of investing small sums, transparency, tax efficiency and of course, superior returns as equities? And if risks become marginal by holding over the long term (we have discussed this in our earlier publications), then are short-term pains that hard to bear?

No pain, no gain!

M’m, I am very much unknown to stocks or equities, but for last few months I have been watching the market trends and see that banking sector (SBI, AXIS, YES BANK) is the safest one to invest in. Their stock prices are almost doubled in one year period. Madam, I want to know your view whether I can invest in any of these or other stocks. Thank you.

Hello Mr Sampat, I am afraid I am not qualified to give stock calls. I track mutual funds at FundsIndia. Vidya

Thanks for your response, M’m.

M’m, I am very much unknown to stocks or equities, but for last few months I have been watching the market trends and see that banking sector (SBI, AXIS, YES BANK) is the safest one to invest in. Their stock prices are almost doubled in one year period. Madam, I want to know your view whether I can invest in any of these or other stocks. Thank you.

Hello Mr Sampat, I am afraid I am not qualified to give stock calls. I track mutual funds at FundsIndia. Vidya

Thanks for your response, M’m.