KPR Mill Ltd. – Key player in the textiles industry.

Incorporated in 2003 and headquartered in Coimbatore, KPR Mill Ltd. is one of the largest vertically integrated apparel manufacturing companies in India. With state-of-the-art production facilities in Tamil Nadu and a global footprint spanning 60 countries, the company’s diversified business is spread majorly across yarn, fabric, garments, and white crystal sugar. As of 31 March 2023, KPR has a capacity to produce 1,00,000 MTPA of Cotton yarn & 4,000 MTPA Viscose vortex yarn, 40,000 MTPA fabrics and 157 million readymade knitted apparel per annum. The company has also ventured into branded retail segment via the launch of its in-house brand FASO.

Products and Services

KPR has a diverse range of product portfolio comprising readymade knitted apparel, fabrics, compact, melange, carded, polyester, combed yarn etc. Additionally, the company is also in the business of producing white crystal sugar, ethanol and power generation.

Subsidiaries: As of FY23, the company has 7 subsidiaries.

Key Rationale

- Robust track record with solid client base – The company has export relationship with various leading international brands such as Primark, Marks & Spencers, H&M etc. Further, cementing its proven track record of catering to major players, the company recently added Walmart as customer for US exports, and GAP to the US and Europe customer list. The new client additions are expected to give strong volume traction to the company. During Q3FY24, KPR pulled off an all-time high garment order book of Rs.1,100 crore.

- Consistent capex expansions – The company is expanding its processing capacity with an outlay of Rs.250 crore along with solar power plant at a Rs.100 crore capex spend (capacity of 25MW) taking the solar and wind capacity to 100 MW. It recently completed setting up of vortex spinning mill at a capital outlay of Rs.100 crores, roof top solar power plant with an investment of Rs.50 crore and ethanol capacity expansion at existing sugar mills at a capital outlay of Rs.150 crores. With this the capacity of existing sugar mill ethanol capacity has increased from 120 KLPD to 250 KLPD. It also completed the greenfield processing & printing expansion at Rs.50 crores to match the processing capacity to meet the existing garment capacity.

- Sugar/Ethanol segment – The ethanol production is expected to take a hit given the government-imposed restrictions on using sugarcane juice to produce ethanol. Even though ethanol production from B-Heavy molasses and C-Heavy molasses will continue as usual, the company has estimated a 40% reduction in ethanol production converting into a Rs.200 crore revenue dip during the season. It is aiming to compensate this loss from the slightly improved sugar prices from last year. Additionally, higher than expected sugar yield might result in government relaxing the restrictions currently imposed. The company has given a production guidance of 7 – 8 crore litres of ethanol and 2 lakhs tonnes for sugar for the current year.

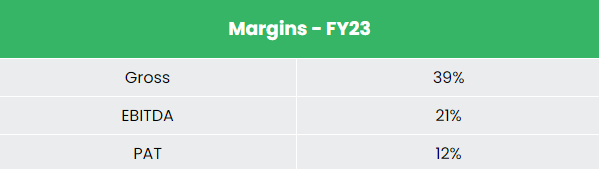

- Q3FY24 – During the quarter, revenue declined by 12% from Rs.1,445 crore of Q3FY23 to Rs.1,269 crore of Q3FY24. Operating profit improved marginally by 1% to Rs.272 crore from the Rs.269 crore of Q3FY23. Net profit improved by 7% to Rs.187 crore. During the quarter, the company had to take the impact of fall in sugar price and consequent fall in price of yarn, margin cut in yarn due to subdued demand in international markets, garment shipment delay due to cyclone in Tamil Nadu and the government ban on using sugar cane juice for ethanol manufacturing. Segment-wise margin achieved by the company is as follows – Yarn & Fabric margin – 15%, Garment – 27%, Sugar – 27%.

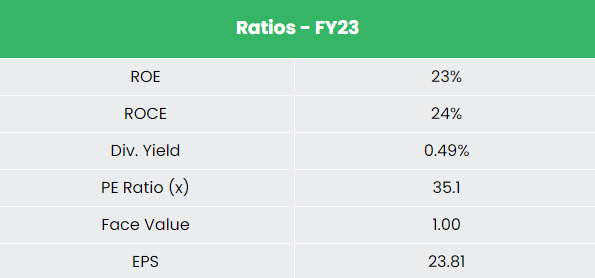

- Financial performance – KPR has generated a revenue and PAT CAGR of 23% and 30% over the period of 3 years (FY20-23). Average 3-year ROE & ROCE is around 26% and 27% for FY20-23 period. The company has strong balance sheet with a robust debt-to-equity ratio of 0.21.

Industry

The fundamental strength of the textile industry in India is its strong production base of a wide range of fibre/yarns from natural fibres like cotton, jute, silk and wool, to synthetic/man-made fibres like polyester, viscose, nylon and acrylic. India is one of the largest producers of cotton and jute in the world. With 4.6% share of the global trade, India is the world’s largest producer and third largest exporter of textiles and apparel in the world. India ranks among the top five global exporters in several textile categories, with exports expected to reach US$ 65 billion by FY26. Cotton production in India is projected to reach 7.2 million tonnes by 2030, driven by increasing demand from consumers. India enjoys a comparative advantage in terms of skilled manpower and in cost of production, relative to major textile producers. Increasing demand for online shopping is also expected to aid the growth of textile manufacturing market.

Growth Drivers

- 100% FDI is allowed under automatic route in textile industry.

- Rs.4,389.24 crore (US$ 536.4 million) total allocation for textile sector in Union Budget for FY23-24.

- Various government schemes such as the Scheme for Integrated Textile Parks (SITP), Technology Upgradation Fund Scheme (TUFS) and Mega Integrated Textile Region and Apparel (MITRA) Park scheme.

Competitors: Page Industries Ltd, Gokaldas Exports Ltd etc.

Peer Analysis

In comparison to the above competitors, KPR Mill is the most undervalued mid-cap stock with better returns on the capital employed and stable growth in sales.

Outlook

The future of the Indian textiles industry looks promising, buoyed by strong domestic consumption as well as export demand. The company expects to achieve increase in sales volumes by virtue of increase in capacity across garments, spinning, sugar and ethanol divisions. It is eyeing a growth of 10% to 12% growth in garments segment. Besides consistent capacity additions in the core textiles business, strategic investments in the sugar/ethanol business will help sustain the growth momentum. The company is anticipating a scale up to a range of Rs.10 crore per month run rate from FASO.

Valuation

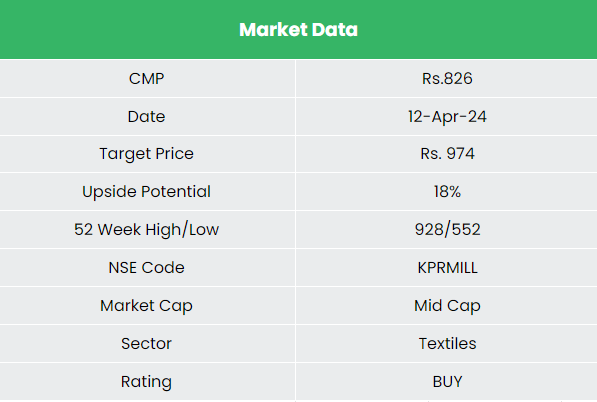

We expect a steady pick up in volumes and realisations for KPR Mill Ltd given the company’s significant market share in the demand driven industry and capacity expansions. However, we expect the sugar/ethanol division to remain under pressure due to head winds. We recommend a BUY rating in the stock with the target price (TP) of Rs.974 34x FY25E EPS.

Risks

- Centralised manufacturing facilities – All of the company’s manufacturing facilities are located in Tamil Nadu. Any unprecedented movements or unanticipated climate conditions in this region might pose a hindrance for the continuation of operations.

- Forex Risk – The company has significant operations in foreign markets and hence is exposed to forex risk. Any unforeseen movement in the forex market can adversely affect the company.

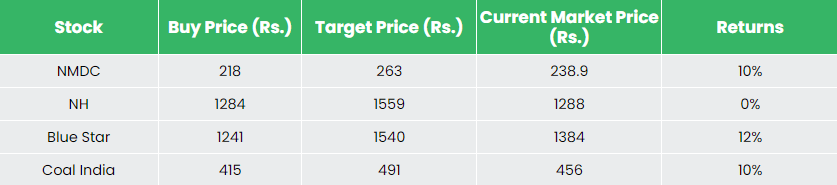

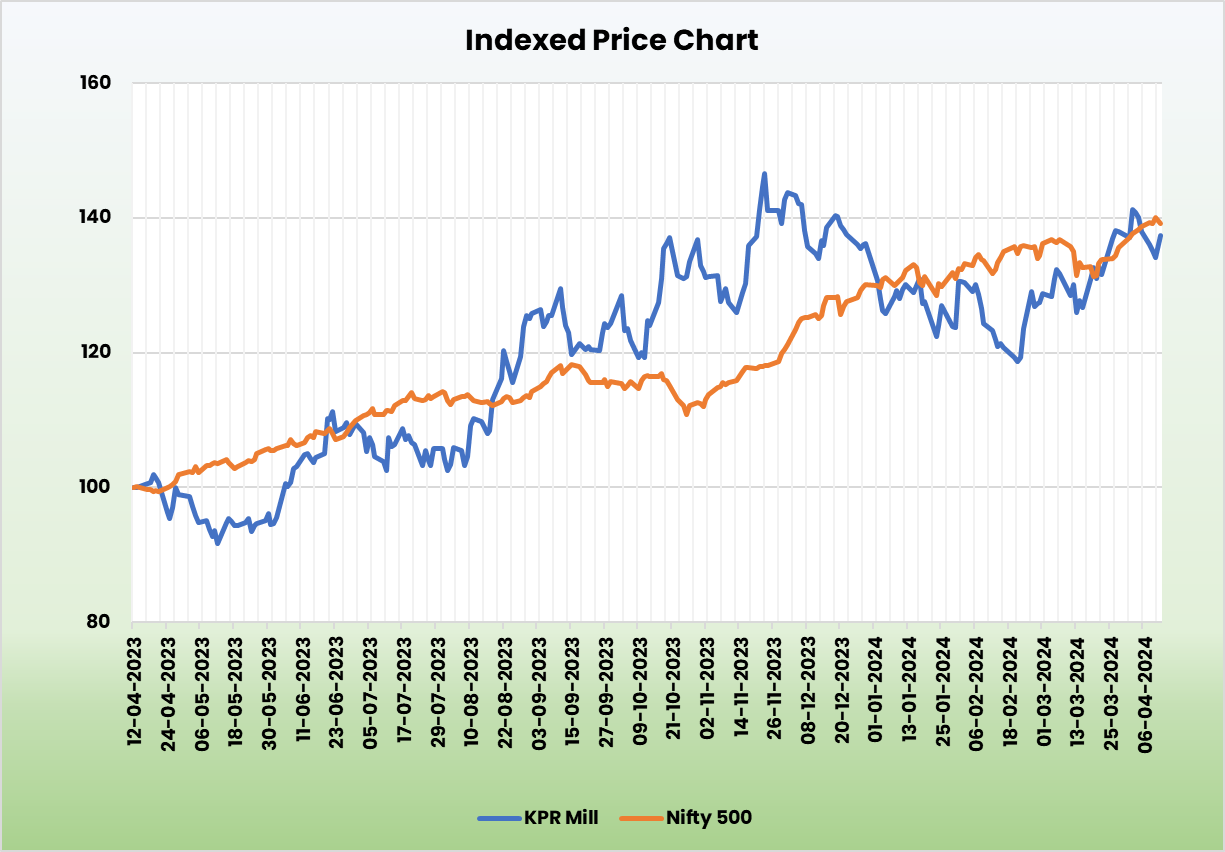

Recap of our previous recommendations (As on 12 Apr 2024)