Blue Star Ltd. – Built on Trust

Incorporated in 1943 and headquartered in Mumbai, Blue Star Ltd. is India’s leading Heating, Ventilation, Air Conditioning and Commercial Refrigeration (HVAC&R) company. It is also a major player in the Mechanical, Electrical, Plumbing, and Firefighting (MEP) space offering turnkey solutions for buildings, factories, data centers, infrastructure, heavy industry and water distribution projects. Currently Blue Star exports its products to 18 countries in the Middle East, Africa, SAARC, and ASEAN regions. As of 31 March 2023, the company has 7 state-of-the-art manufacturing facilities across Himachal Pradesh, Dadra, Ahmedabad, and Wada, including the company’s 100% subsidiary Blue Star Climatech Limited’s Sri City facility.

Products and Services

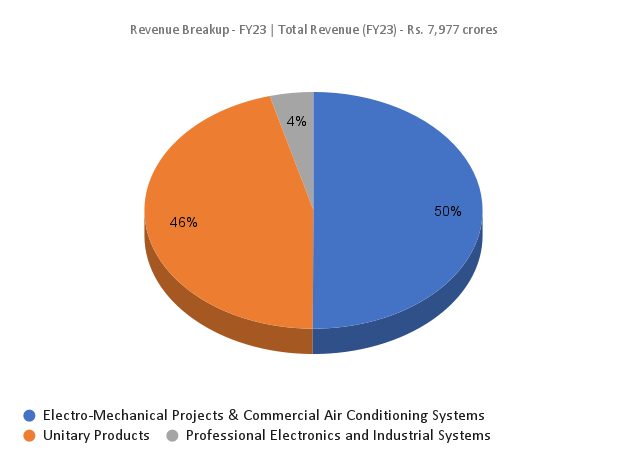

The company operates majorly in 3 business segments – Electro-Mechanical Projects and Commercial Air Conditioning Systems, Unitary Products & Professional Electronics and Industrial Systems. It offers wide range of products such as inverter split AC, window AC, air cooler, air purifier, portable AC, water purifiers, VRF V plus system, screw & scroll chiller, storage water cooler, bottled water dispenser, ice lined refrigerator, freezers, cold rooms etc.

Subsidiaries: As of FY23, the company has 9 subsidiaries and 2 joint ventures.

Key Rationale

- Established position – Blue Star has a market share of 13.75% in the industry. The Unitary segment has displayed a very strong growth ahead of the industry performance during the quarter. The company has given a margin guidance of 8% to 8.5% for the segment. It aims to deliver highly reliable products which are world-class while also entering the affordable segment. Even within affordable segment, the company produces products that are superior in terms of market trends and customer preferences.

- Expanding manufacturing capacities – The company is strategically investing in capacity expansion. With an investment of around Rs.130 crore, the new cutting-edge manufacturing facility at Wada caters to the production of deep freezers and water coolers. It can produce 2,00,000 deep freezers and 1,00,000 storage water coolers per annum. The company’s wholly owned subsidiary, Blue Star Climatech Limited has set room air conditioner manufacturing facility in Sri City equipped with several Industry 4.0 automation techniques and IoT tools. With an investment of Rs.350 crores in the first phase, it has a capacity to produce 3,50,000 room air conditioners. The facility will be scaled up to 16,00,000 room air conditioners in a phased manner.

- Q3FY24 – Revenue for the quarter was Rs.2,241 crore compared to Rs.1,794 crore during Q3FY23, representing a growth of 25%. EBITDA was at Rs.155 crore an increase of 48% compared to the Rs.105 crore of Q3FY23. The company reported net profit of Rs.100 crore marking a surge of 72% compared to the Rs.58 crore of the corresponding quarter in the previous year. During the quarter, the company was able to achieve significant growth due to festive demand and increased demand from Tier-3, 4, 5 towns. The carryforward order book stood at a record Rs.6,038 crores.

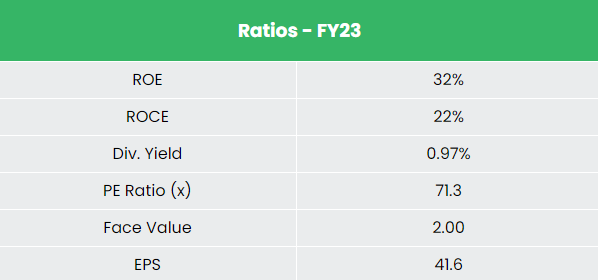

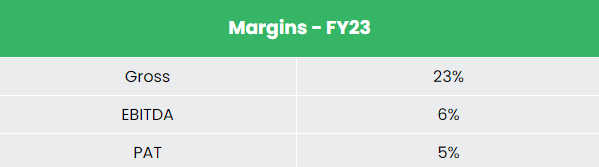

- Financial performance – The 3-year revenue and profit CAGR stands at 14% and 24% respectively between FY20-23. The company has strong balance sheet with debt-to-equity ratio of just 0.37. Average 3-year ROE and ROCE is around 17% and 19% for FY20-23 period.

Industry

White goods or consumer durables industry encompass significant household appliances including air conditioners, LED lights, refrigerators, dishwashers, freezers, coolers etc. The White Goods market is estimated to cross $21 Bn by 2025 expanding at a CAGR of 11%. Domestic manufacturing contributes nearly $4.6 Bn on an average to this industry. Air conditioner Market in India to increase to $9.8 Bn by FY26 from $3.8 Bn in FY21 at a CAGR of 20.8%. The cumulative share (by volume) of four and five-star inverter RACs is expected to increase to 30-40% in FY25 from 20-23% in FY22. AC exports increased at a CAGR of 9% from $165 Mn in 2018 to $233 Mn in 2022.

Growth Drivers

India allows 100 percent foreign direct investment (FDI) under the automatic route into the consumer durable goods manufacturing industry. Between April 2000-September 2023, electronic goods attracted FDI inflows of US$ 4.42 billion. Blue Star is participating in the Production Linked Incentive for White Goods (PLIWG) scheme for components and sub-assemblies for room ACs. The Production Linked Incentive Scheme for White Goods (PLIWG) proposes a financial incentive to boost domestic manufacturing and attract large investments in the White Goods manufacturing value chain.

Competitors: Whirlpool & Johnson Controls – Hitachi.

Peer Analysis

Among the above competitors, Blue Star has better return ratios and stable revenue growth than the other two, indicating the company’s financial stability and its efficiency to generate income and returns from the invested capital.

Outlook

The two new plants, one each in Sri City and Wada, have been added to augment Blue Star’s manufacturing scale to gear up for the next phase of growth. The Sri City plant is strategically located closer to a couple of Southern Indian Sea ports which will enable speedy and efficient logistics management. The company also plans to explore export opportunities in countries like USA and Europe. Blue Star continues to invest in expanding manufacturing capacity, accelerating R&D and digitalization as a part of its growth plan and profitability improvement programs. The company is able to maintain moderate net borrowing due to prudent cash management and healthy debt-to-equity ratio. It currently has an order book of Rs.6,000 crores to be executed in 24 months.

Valuation

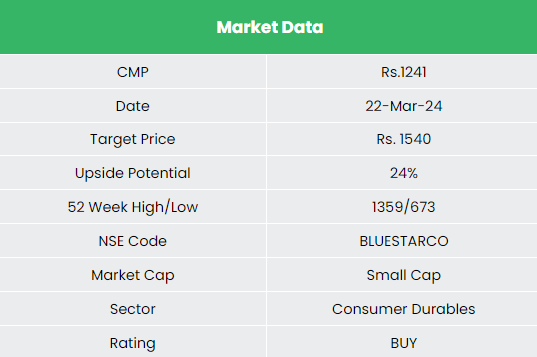

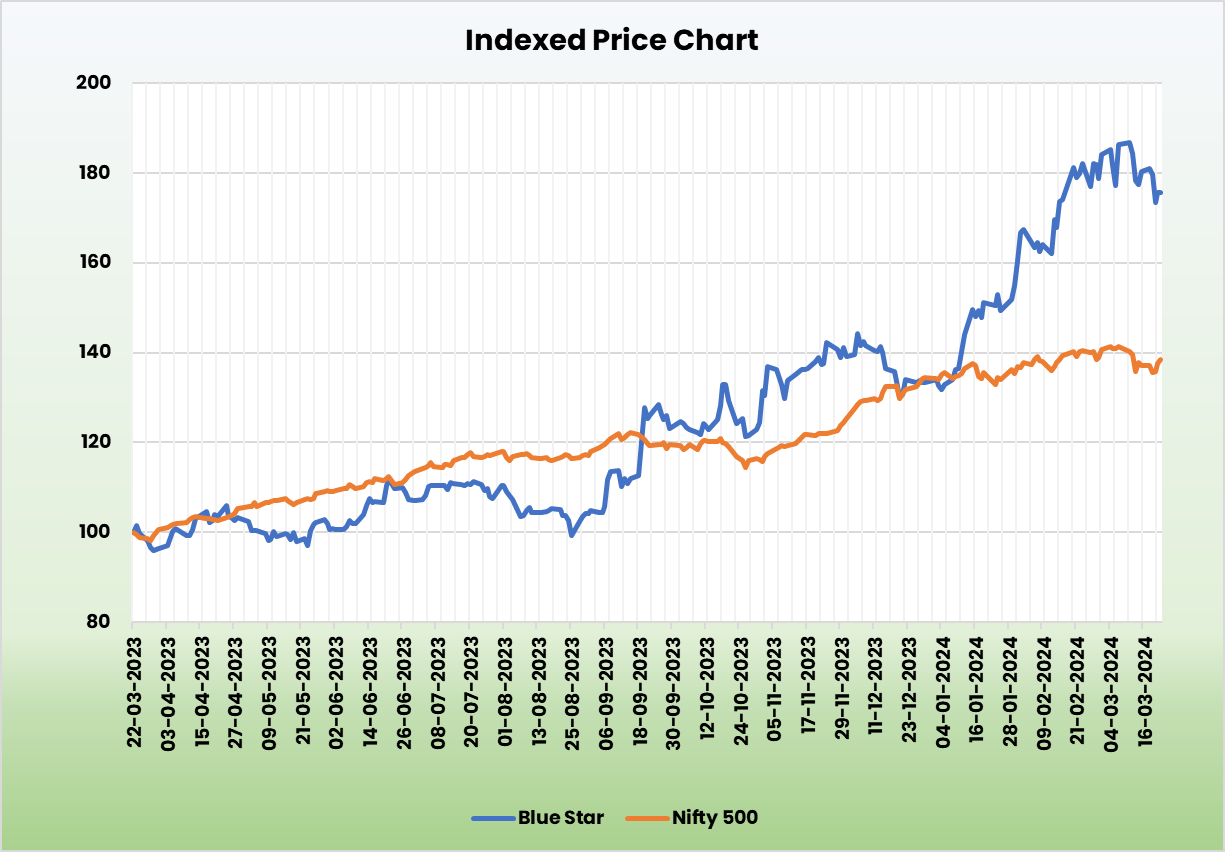

With a focus on total cost management initiatives, product portfolio optimization and scale benefits, the company is aiming to achieve significant growth in profits and a market share of 15% by FY25. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,540, 59x FY25E EPS.

Risks

- Seasonality Risk – Majority of the products sold by the company is seasonal in nature. Unforeseen weather patterns such as extended winter, pleasant summer, less than normal monsoon, excess monsoon, or any kind of disruptions during the peak selling seasons may lead to either a stock-out or excess inventory situation and impact revenue growth.

- Competition risk – Several Indian and global players in the air conditioning business are in the process of setting up or expanding their own manufacturing facilities in India to tap the underpenetrated market. This might put pricing pressure on the company resulting in dilution of margins and profitability.

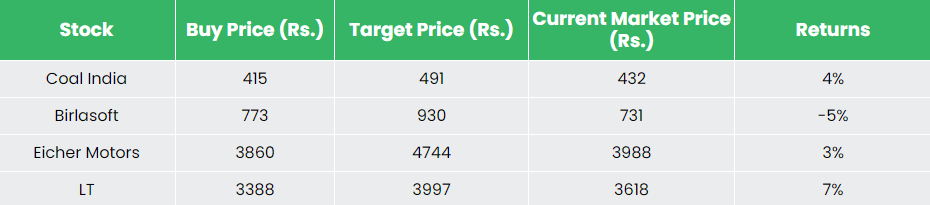

Recap of our previous recommendations (As on 22 Mar 2024)