Close in the heels of the REC tax-free bond issue comes HUDCO’s tax-free bonds. Only this time, thanks partly to higher 10-year gilts (which act as a reference rate), the coupon rates of HUDCO are marginally higher than that of REC. For instance, the 10-year rate is at 8.39% (for retail investors with less than Rs 10 lakh investment) for HUDCO as against 8.26% offered by REC.

The 15-year bonds come with an interest rate of 8.76% per annum while the 20-year tenure will pay 8.74% a year. Investors can go with the 10 or 15-yer bond, based on their capital requirements. Interest is paid out annually.

What are tax-free bonds

Tax-free bonds are non-convertible debentures on which the interest income does not suffer tax throughout the tenure of the bond. There is no tax benefit (such as 80C) on the principal. Most debt options, barring the PPF and EPF suffer tax on the interest component. Your FDs, post office schemes and corporate deposits are no exceptions.

The coupon rate of the tax-free bond is actually the post-tax return for you. This makes this class of bonds attractive for most tax payers.

Added to this, government security yields saw a sharp rise after the recent hike in interest rate by RBI. As a result, long-term bond yields are high, providing scope for you to lock into them using these bonds.

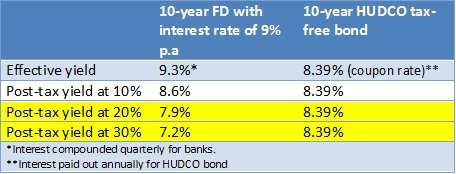

The table below also illustrates how the bonds score over fixed deposits for those in the 20% and 30% tax bracket at this juncture.

HUDCO tax-free bonds can be bought by NRIs as well. They can be held in physical or demat form. Holding in demat form will provide the option of selling it in the market.

However, given that the liquidity in these instruments may not be high and you should know about yield movements before you decide to sell, the bonds are best suited for retail investors as a hold-till-maturity option.

About HUDCO

HUDCO is a public financial institution under the Companies Act and also registered as a housing finance company under NHB. It is a 100% government of India undertaking that seeks to provide long-term financing for social housing and urban infrastructure development projects.

The current issue of HUDCO has an AA+ rating from Care Ratings. That is one notch below the top rating but still considered low risk and investment worthy. REC’s bonds enjoyed higher rating.

HUDCO’s rating is slightly lower as a result of high exposure to sectors such as power and real estate, which are considered vulnerable in the current situation. Nevertheless, that it is a government company having healthy capitalization levels and access to low-cost funding provides comfort.

Hence, the slightly lower rating need not act a deterrent. The company had net profits of Rs 700 crore as of March 31, 2013, on total income of Rs 2923 crore.

whether the interest is paid annually, please inform.

Hello Punnam, yes it is paid out annually. thanks.

This Vs long term Debt funds. Which one do you recommend, given the fact that with indexation, LTCG will probably be nil with debt funds.

Hi Apporv, Yes, income funds (not gilt funds) can be good options if the idea is long-term wealth building. But if someone is looking for steady income, then debt funds cannot guarantee it the way these bonds can. Thanks

Thanks Vidya. If you invest in these funds every year, then after 10 (or 15 years), these will start maturing and you will get some income every year. Is that what you meant by “steady income”?

Hi Apporv, No, the bond has only an annual payout option ( I already added this point on the blog, realising your ques. may pertain to that). Tax-free bonds, in general, do not have cumulative option at all.

That means unless you reinvest the interest paid out every year, you cannot meaningfully build wealth with this bond. hence it is a good source of income. thanks.

whether the interest is paid annually, please inform.

Hello Punnam, yes it is paid out annually. thanks.

This Vs long term Debt funds. Which one do you recommend, given the fact that with indexation, LTCG will probably be nil with debt funds.

Hi Apporv, Yes, income funds (not gilt funds) can be good options if the idea is long-term wealth building. But if someone is looking for steady income, then debt funds cannot guarantee it the way these bonds can. Thanks

Thanks Vidya. If you invest in these funds every year, then after 10 (or 15 years), these will start maturing and you will get some income every year. Is that what you meant by “steady income”?

Hi Apporv, No, the bond has only an annual payout option ( I already added this point on the blog, realising your ques. may pertain to that). Tax-free bonds, in general, do not have cumulative option at all.

That means unless you reinvest the interest paid out every year, you cannot meaningfully build wealth with this bond. hence it is a good source of income. thanks.

Hi,

I am in a tax bracket of 30 % , can you pl suggest which one tax saving option is better :-

ICICI TAX SAVER

HUDCO TAX SAVER

i have pan to invest by 10 yrs .

Vivek

Hi Vivek,

You have to first decide whether you are looking for tax deduction under Section 80C or you are simply looking for tax-free annual income (no exemption under 80C). The ICICI PRu TAx Plan fund is a tax-saving scheme that will provide tax deduction from your total income for investments up to Rs 1 lalkh in the year of investment. HUDCO tax-free bond is a bond, where the interest income earned every year is tax free. The 2 are not the same and hence not comparable at all. What you choose will depend on your requirement. Thanks

Hi,

I am in a tax bracket of 30 % , can you pl suggest which one tax saving option is better :-

ICICI TAX SAVER

HUDCO TAX SAVER

i have pan to invest by 10 yrs .

Vivek

Hi Vivek,

You have to first decide whether you are looking for tax deduction under Section 80C or you are simply looking for tax-free annual income (no exemption under 80C). The ICICI PRu TAx Plan fund is a tax-saving scheme that will provide tax deduction from your total income for investments up to Rs 1 lalkh in the year of investment. HUDCO tax-free bond is a bond, where the interest income earned every year is tax free. The 2 are not the same and hence not comparable at all. What you choose will depend on your requirement. Thanks

Respected Madam

I have not understood the meaning of the line written as” Investors can go with the 10 or 15-yer bond, based on their capital requirement”

I do not understand what is my capital requirement from my investment point of view.

Pl elaborate for my understanding.

Hello sir,

Since the capital will be locked in for 10 years or 15 years, based on when you require your capital back, you may choose the time frame of your investment. Thanks.

Respected Madam

I have not understood the meaning of the line written as” Investors can go with the 10 or 15-yer bond, based on their capital requirement”

I do not understand what is my capital requirement from my investment point of view.

Pl elaborate for my understanding.

Hello sir,

Since the capital will be locked in for 10 years or 15 years, based on when you require your capital back, you may choose the time frame of your investment. Thanks.

Good Day Madam,

From above detailed study, I know that the interest payable annually will be tax free.

Can you kindly confirm what about maturity amount after 20 years. i.e. if I purchase HUDCO bond of Rs. 5 L for 20 year. I will get interest that will be tax free, But after 20 years, at the time of maturity, what amount will I get? Is it tax free or it will be counted as my additional income at that time?

Hello tejas, the principal amount will not be taxed when you get back the money after 20 years. Remember, the principal amount does not enjoy any tax deductions (like 80C) at the time of investing. hence no question of taxation at the time of redemption. Thanks

Good Day Madam,

From above detailed study, I know that the interest payable annually will be tax free.

Can you kindly confirm what about maturity amount after 20 years. i.e. if I purchase HUDCO bond of Rs. 5 L for 20 year. I will get interest that will be tax free, But after 20 years, at the time of maturity, what amount will I get? Is it tax free or it will be counted as my additional income at that time?

Hello tejas, the principal amount will not be taxed when you get back the money after 20 years. Remember, the principal amount does not enjoy any tax deductions (like 80C) at the time of investing. hence no question of taxation at the time of redemption. Thanks

I am the accountholder of “Funds India” and I always read your articles with interest. Thanks for your explanation.

I am the accountholder of “Funds India” and I always read your articles with interest. Thanks for your explanation.

Hi,

Can you please explain how to buy this bond as an individual. What is the minimum amount an individual can buy.

Thanks

Hello Raj,

You can buy online through FundsIndia, if you have an account with us or through any authorised distributor. Minimum investment is Rs 5000. Thanks

Hi,

Can you please explain how to buy this bond as an individual. What is the minimum amount an individual can buy.

Thanks

Hello Raj,

You can buy online through FundsIndia, if you have an account with us or through any authorised distributor. Minimum investment is Rs 5000. Thanks

Is buying these bonds similar to buying stock out equity funds in terms of fees charged?

Hi Hari, No there is no fee or brokerage charged from the customer for tax-free bonds at the time of initial offer. Only if you choose to trade them from your demat account will brokerage kick-in. Thanks, Vidya

Hi Vidya,

Appreciate ur quick reply, also another query. From better rating, higher returns perspective which is better (10yr/15yr option), HUDCO or IIFCL ?

Hi Anand, the risk profile difference is very marginal. If you can spare money for the long haul, consider 15-yr HUDCO. Thanks.

Hi,

Is demat account mandatory to buy HUDCO tax-free bonds ?

or optional ?

Hi Anand, At FundsIndia, in order to have paperless, online transactions, the bonds are allotted through demat account that is either with FI or any demat you may have outside. Otherwise, tax-free bonds can also be bought physically outside. thanks.

Hi Vidya,

Appreciate ur quick reply, also another query. From better rating, higher returns perspective which is better (10yr/15yr option), HUDCO or IIFCL ?

Hi Anand, the risk profile difference is very marginal. If you can spare money for the long haul, consider 15-yr HUDCO. Thanks.

Thank you !

Hi, I have a mutual funds account with FI , but not a demat account, will I be able to buy vis FI then? Or is it necessary to have a demat account ?

If you wish to buy tax-free bonds through FI, then you need demat account either with FI or outside. We have this to avoid delay in paper work (physical mode will require investors to sign and also provide proof of address and identity separately for the bond issuer). thanks

Hi Vidya,

I purchased these bonds through FI. Is there anyway to confirm allotment status now?

Hello Santosh, I have requested our support team to look into this and get back. thanks, Vidya

The remittance of the interest will be annually in the form of tax free income. ?

Yes Jatin, it will be tax-free annual interest payout. thanks, Vidya

is it worth instead of buying hudco tax-free bonds invest Rs. 1 lakh in ppf a/c, because interest rate is almost same & i can get tax benefit on invested amt. also & tax benefit on interest income also.

Hello Vinayak,You would have to keep your PPF account alive every year by investing. Also, investment is restricted to Rs 1 lakh a year. More importantly, PPF rates change every year and your PPF balance will get only the changed rate every year. Hence, it’s not fixed for the 15-year period. PPF rates, have been on the decline over the past decade. With tax-free bonds, you lock into rates. Also, tax-free bonds is ideal for people looking for some annual cash flow. PPF is more for saving for the long term. thanks, Vidya

Hi, I have a DMAT account what should I search for in order to buy the HUDCO or any other bonds.

Hello Harmeet, Unless you buy durng the IPO, bonds can be bought in the secondary market through your broker, provided the said bond is frequently traded. You can specifiy the name of the bond and ask your broker to place the trade. However, pl. note that while buying in secondary market (that is after IPO), you should be careful about buying it at the right price. thanks, Vidya

Thank you so much for the reply, this helps a lot.

The remittance of the interest will be annually in the form of tax free income. ?

Yes Jatin, it will be tax-free annual interest payout. thanks, Vidya

is it worth instead of buying hudco tax-free bonds invest Rs. 1 lakh in ppf a/c, because interest rate is almost same & i can get tax benefit on invested amt. also & tax benefit on interest income also.

Hello Vinayak,You would have to keep your PPF account alive every year by investing. Also, investment is restricted to Rs 1 lakh a year. More importantly, PPF rates change every year and your PPF balance will get only the changed rate every year. Hence, it’s not fixed for the 15-year period. PPF rates, have been on the decline over the past decade. With tax-free bonds, you lock into rates. Also, tax-free bonds is ideal for people looking for some annual cash flow. PPF is more for saving for the long term. thanks, Vidya

Hi Vidya,

I purchased these bonds through FI. Is there anyway to confirm allotment status now?

Hello Santosh, I have requested our support team to look into this and get back. thanks, Vidya

Hi, I have a DMAT account what should I search for in order to buy the HUDCO or any other bonds.

Hello Harmeet, Unless you buy durng the IPO, bonds can be bought in the secondary market through your broker, provided the said bond is frequently traded. You can specifiy the name of the bond and ask your broker to place the trade. However, pl. note that while buying in secondary market (that is after IPO), you should be careful about buying it at the right price. thanks, Vidya

Thank you so much for the reply, this helps a lot.

Thank you !

Hi, I have a mutual funds account with FI , but not a demat account, will I be able to buy vis FI then? Or is it necessary to have a demat account ?

If you wish to buy tax-free bonds through FI, then you need demat account either with FI or outside. We have this to avoid delay in paper work (physical mode will require investors to sign and also provide proof of address and identity separately for the bond issuer). thanks

Hi,

Is demat account mandatory to buy HUDCO tax-free bonds ?

or optional ?

Hi Anand, At FundsIndia, in order to have paperless, online transactions, the bonds are allotted through demat account that is either with FI or any demat you may have outside. Otherwise, tax-free bonds can also be bought physically outside. thanks.

Is buying these bonds similar to buying stock out equity funds in terms of fees charged?

Hi Hari, No there is no fee or brokerage charged from the customer for tax-free bonds at the time of initial offer. Only if you choose to trade them from your demat account will brokerage kick-in. Thanks, Vidya