Early this month, we carried an article on whether you should invest in gilt funds or not:

Should you invest in gilt funds? In the same article, we had suggested that the gilt rally may have limited upside in the course of the next one year, concluding that high-risk investors looking for active debt exposure should probably look at long-dated income fund portfolios which have higher exposure to corporate bonds and debentures and even state development loans.

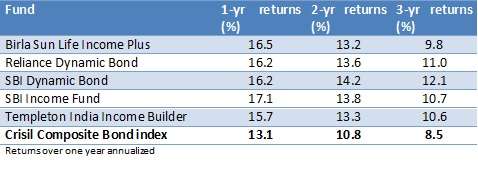

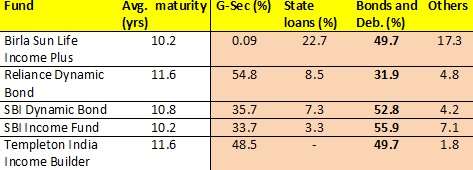

While we sifted through income funds, we came across some such interesting portfolios held by funds such as Birla Income Plus, SBI Income Fund and SBI Dynamic Bond. Funds that had good exposure to corporate bonds but almost a 50% exposure to gilt funds were Templeton India Income Builder and Reliance Dynamic Bond. Here’s a quick review on these funds.

Suitability

The funds mentioned above are suitable only if you are looking to maximize the benefit from the interest rate fall over the course of the next one year. The time frame for holding these funds would be about a year.

In other words, these funds are meant for more tactical holding. You would have to be an active debt investor who can exit the fund once you see interest rate falls approaching an end. The funds would also require relatively higher risk appetite.

We would not recommend these funds for an investor’s core portfolio, especially for those with a long-term horizon. Why is this so? Over a longer term, many other income funds, such as Birla Dynamic Bond or IDFC SSI Medium Term score better on a risk-adjusted basis. That means you can hope to earn well with lower risks in the long term.

Criteria

We scouted for funds that have a long average maturity with a high exposure to corporate bonds or state loans rather than G-Secs. This choice was done to take advantage of rallies in corporate bonds as the spread between corporate bonds and gilts narrow with falling interest rates.

A long track record of reasonable returns and majority holding in AAA-rated instruments were other key criterions used to select the funds.

Portfolio and returns

In the last 2 years, the funds mentioned above delivered high double-digit returns, aided by rally both in the G-Sec and corporate bond segments. Their dynamic shift across various tenures, in line with interest rate movements helped these funds deliver superior returns.

But our analysis suggests that other income funds with lower average portfolio maturity have fared well over a three-year period on a risk-adjusted basis. For instance, Birla Sun Life Dynamic Bond fund’s sharpe ratio (for a period of 3 years) was better than Birla Sun Life Income Plus. Templeton India Income Opportunities, similarly, outperformed Templeton India Income Builder on the same parameter.

It is for this reason of high risk not compensated by high returns in the long term that some of these funds would not receive high fund rating in portals such as Value Research Online.

In the accompanying table, while the SBI funds have a good proportion exposed to private and public sector bonds, Birla Sun Life Income Plus’ portfolio has a good dose of state development loans. They provide better scope for a price rally when compared with Central government bonds. But they are not risk free. State development loan repayments are monitored by the RBI. Yet, if a state’s financial condition is shaky, then such an instrument will carry higher risk.

For those preferring to take exposure to Central government securities than state-run ones, Templeton India Income Builder and Reliance Dynamic Bond may offer a good dose of government securities, even as they invest a reasonable proportion in corporate bonds.

Hi Vidya,

Is there any scheme that does all the activities you mentioned above? Like balancing based on interest fluctuation etc., Could you please suggest few schemes which are doing well.

Rgds

Hari

Hi Hari,

Most of the funds in the income fund category try to play the interest rate cycle well but within their given internal mandates. For instance, Birla Dynamic Bond simply cannot push its portfolio maturity beyond say 4-5 years and hence cannot mimic a Birla Income Plus. But at the same time, Birla Dynamic Bond can reduce its tenure when rates rise. Hence it does balance well.

Similarly, some funds cannot take too short a duration when rates increase.

But as we mentioned in this article, if you are a long-term holder, it will suffice to hold regular income funds (refer our select funds – http://www.fundsindia.com/select-funds for choice of income funds) to play the interest curve well. Tks, Vidya

Hi Vidya,

Is there any scheme that does all the activities you mentioned above? Like balancing based on interest fluctuation etc., Could you please suggest few schemes which are doing well.

Rgds

Hari

Hi Hari,

Most of the funds in the income fund category try to play the interest rate cycle well but within their given internal mandates. For instance, Birla Dynamic Bond simply cannot push its portfolio maturity beyond say 4-5 years and hence cannot mimic a Birla Income Plus. But at the same time, Birla Dynamic Bond can reduce its tenure when rates rise. Hence it does balance well.

Similarly, some funds cannot take too short a duration when rates increase.

But as we mentioned in this article, if you are a long-term holder, it will suffice to hold regular income funds (refer our select funds – http://www.fundsindia.com/select-funds for choice of income funds) to play the interest curve well. Tks, Vidya

I am 50 years old and have 15 lacs to invest. i am planning to invest bsl dynamic bond fund, sbi dynamic bond fund, hdfc mip ltp and reliance mip and would like to withdraw Rs 15000 every month from next year. My total withdrawal would be Rs 180000 per year. I have no other source of income. My question is should i pay any tax ? as my withdrawal would be below the taxable limit.

Hello Madam,

If you withdraw 1 year after investment, you will have long-term capital gains. If you have nil source of income then this Rs 1,80,000 falls within the overall tax slab limit. In that case there will be no tax. But this is so, provided you have no other taxable income such as FD interest etc. Pl. ensure that.

As for the funds you have chosen, the MIPs will carry some risk as they invest some portion in equities. Since you have a short holding period, hope you are game for such risk. Ideally, SWPs should be done in such funds after holding for at least 2 years. Our suggestion would be that you split the Rs 15 lakh across other fixed sources of income such as fixed deposits as well. Thanks, Vidya

Is there any downside risk once the pure debt fund is appreciated?

Hello Prema, If the funds do not make tactical shifts soon after the rate falls or when interest rates start rising, there is even risk of negative returns. Gilt funds as well as dynamic bond funds that had a long average maturity suffered some losses in 2009 when such a scenario played out. That is the downside risk of holding fund with average portfolio maturity of 8 or more years, Thanks, Vidya

In that case can i take sip route for 12 months and do swp after 24 months?

Hello Madam,

If you can hold only for 2 years in total, then you might as well go for a lump sum investment, hold for 2 years and then start SWP. SIPs are useful only if you wish to do either do long-term wealth building (in which case you do SIPs for not less than 3 years) or short-term savings (like investing in liquid or short-term debt for a short-term goal like vacation or for an insurance premium). Thanks, Vidya

I am 50 years old and have 15 lacs to invest. i am planning to invest bsl dynamic bond fund, sbi dynamic bond fund, hdfc mip ltp and reliance mip and would like to withdraw Rs 15000 every month from next year. My total withdrawal would be Rs 180000 per year. I have no other source of income. My question is should i pay any tax ? as my withdrawal would be below the taxable limit.

Hello Madam,

If you withdraw 1 year after investment, you will have long-term capital gains. If you have nil source of income then this Rs 1,80,000 falls within the overall tax slab limit. In that case there will be no tax. But this is so, provided you have no other taxable income such as FD interest etc. Pl. ensure that.

As for the funds you have chosen, the MIPs will carry some risk as they invest some portion in equities. Since you have a short holding period, hope you are game for such risk. Ideally, SWPs should be done in such funds after holding for at least 2 years. Our suggestion would be that you split the Rs 15 lakh across other fixed sources of income such as fixed deposits as well. Thanks, Vidya

Is there any downside risk once the pure debt fund is appreciated?

Hello Prema, If the funds do not make tactical shifts soon after the rate falls or when interest rates start rising, there is even risk of negative returns. Gilt funds as well as dynamic bond funds that had a long average maturity suffered some losses in 2009 when such a scenario played out. That is the downside risk of holding fund with average portfolio maturity of 8 or more years, Thanks, Vidya

In that case can i take sip route for 12 months and do swp after 24 months?

Hello Madam,

If you can hold only for 2 years in total, then you might as well go for a lump sum investment, hold for 2 years and then start SWP. SIPs are useful only if you wish to do either do long-term wealth building (in which case you do SIPs for not less than 3 years) or short-term savings (like investing in liquid or short-term debt for a short-term goal like vacation or for an insurance premium). Thanks, Vidya

Hi Vidya,

First of all u deserve kudos for such well researched and informative articles, which at the same time are concise and summarize your investment ideas very well.

I had invested in two gilt funds eleven months back (motilal oswal and axis), which are averaging around 12% absolute returns till date. I shall be redeeming them as soon as 12 months are over so as to attract LTCG with indexation benefits. (I am in the 30% tax bracket)

My question is out of the 5 funds researched in your article above, which fund in your view would give the best returns going forward with a one year investment horizon. I am ok with a high risk approach as far as debt funds go.

Rgds,

Piyush

Hi Piyush,

Thank you.

If I could hit the bull’s eye that easily, I would have actually mentioned the ONE fund that would manage top returns 🙂

All. I can say is that given the risk-reward ratios of the portfolio, the Birla fund with higher state loans is something that I would expect to deliver more. But then, I have to stop there because if some of the state loans become a little shaky or their liquidity is not adequate in the debt market (which is quite often the case), my guesstimate will go for a toss. But yes, on a pure risk-reward (and risk-punishment) basis, I would keep an eye there. Thanks, Vidya

Haha i knew i was taking a chance with trying to get you to predict a clear winner!

But point duly noted on the birla fund with its risk-reward trade off.

Thank you once again and keep the articles flowing.

Rgds

Hi Vidya,

First of all u deserve kudos for such well researched and informative articles, which at the same time are concise and summarize your investment ideas very well.

I had invested in two gilt funds eleven months back (motilal oswal and axis), which are averaging around 12% absolute returns till date. I shall be redeeming them as soon as 12 months are over so as to attract LTCG with indexation benefits. (I am in the 30% tax bracket)

My question is out of the 5 funds researched in your article above, which fund in your view would give the best returns going forward with a one year investment horizon. I am ok with a high risk approach as far as debt funds go.

Rgds,

Piyush

Hi Piyush,

Thank you.

If I could hit the bull’s eye that easily, I would have actually mentioned the ONE fund that would manage top returns 🙂

All. I can say is that given the risk-reward ratios of the portfolio, the Birla fund with higher state loans is something that I would expect to deliver more. But then, I have to stop there because if some of the state loans become a little shaky or their liquidity is not adequate in the debt market (which is quite often the case), my guesstimate will go for a toss. But yes, on a pure risk-reward (and risk-punishment) basis, I would keep an eye there. Thanks, Vidya

Haha i knew i was taking a chance with trying to get you to predict a clear winner!

But point duly noted on the birla fund with its risk-reward trade off.

Thank you once again and keep the articles flowing.

Rgds

If I want to get an regular income of Rs 30000 pm how should invest my retirement corpus.

HEllo sir, Pl. use this calculator from our retirement solutions to know how much corpus you need as well as how much you need to save monthly. The calculator will consider future value of your current expenses, taking in to account inflation: http://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=4

Calculator is to your right on the screen. Thanks,Vidya

Hi Vidya, Your article came a bit too late for me. Recently invested in IDFC Dynamic Bond Fund. Would love to hear your opinion on the same.

Hello Yogesh, The said article lays out a high-risk strategy for very active investors. who want to ride one wave of the rate cycle. If you are a long-term (3 plus years) investor, your choice of fund is quite judicious. Tks, Vidya

Hi!Vidya,

I want to allocate 10 lacs each( present value) for my daughter’s and son’s education . I have 3 years and 7 years respectively to achieve that. Should i go for debt or equity funds or combination.

3 years –

My present allocation is SIP of 5500 out of which 2000 goes to SBI Dynamic Bond fund, 2000 in SBI FMCG and 1500 in SBI emerging Bsuiness. I also have 10,000 per month RD (All Started in Oct.2012 for 3 years)

5 years –

I also started an SIP of 5000/ month during the same period in ICICI Pru. Discovery fund . I plan to run it for 5 years and redeem it in the 6th year. Meanwhile run a bank RD in the final 2 years.

Reading your article, I feel I should have put the entire SIP in Debt funds.

Please advise me how to go about it?

Rgds

Hello sir,

Three years is not a good enough period to expose entirely in equities. Use a good proportion of say 60-70% in debt and rest in equities. For a 7-year period, you can certainly have 60-70% in equities and rest in debt. Debt is very unlikely to beat equities over such time frames. Hence, you need not worry about not taking too much exposure to debt funds. Have a portfolio of about 2 equity funds and a debt fund for your 7-year goal.

We prefer to address Specific portfolio/fund advice queries through the ‘Ask Advisor’ feature available to all our investors through their FundsIndia account. It is free of charge.

You may wish to take a look at our Smart Solutions for education: http://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=2

of course, you should have a min. 5-year time frame for this as education is a medium to long-term goal.

Thanks,

Vidya

Thank you very much for the advise.

Ajith

Yet another wonderful article…

FYI, i have already started my investment in BSL Dynamic Bond Fund , give my inability to exactly identify interest rate cycles, i have left that work for the professional.

However, i have liked the statement “You would have to be an active debt investor who can exit the fund once you see interest rate falls approaching an end”.

Now, how do we identify the rate cycle, i can say by my knowledge that we are in middle of the decresing rate cycle. However, we never know, this can go either way from here (depends on many factors).

My take on this is, Funds India having such a wonderful reserch team, why can’t they suggest the starting and ending of Interest rate cycles, may be by a mail for their users atleast (with a disclosure though 🙂 ).

let the investors take teir bet on.

I feel this way, because, you are equipped with the knowledge and data to identify the rate cycles more than what we can do (a normal investor).

I hope this point will be taken into consideration.

Thanks in Advance,

Sunil.

Hi Vidya,

I have invested in equity portfolio till now (apart from EPF/PPF) and want to diversify to Debts moving corpus from FDs. How would breakup the amount of say 4L in income and other debt funds considering time frame between 1-3 yrs and aggressive risk appetite (age 30 yrs) ?

Will be great if you suggest funds as well.

Thanks,

Nimesh

Hi Nimesh,

You could invest 30% in a short-term debt fund and rest in income funds. For this pick funds in the 1-1.5 years category for short-term debt fund and about 2 income funds from the Debt-long-term category from our Select funds list: http://www.fundsindia.com/select-funds

Request you to use the Ask Advisor feature (available when you click the help tab in your FundsIndia Account) so that we can cater to your specific queries through mails or scheduled calls by our advisors. We can provide specific funds in that forum as it caters specifically to our investors.

Thanks,

Vidya

Out of 2 income funds- Would I be better of choosing one from the list you have mentioned in this blog because they do not seem to appear in the Select-funds list ?

Hi Nimesh,

The funds mentioned in this article are not part of our Select funds because they are tactical funds (funds meant for certain time periods) and considered risky. As mentioned in the article, they are only for high risk investors and should not ideally form part of a core wealth-building portfolio. Hence, if you are looking for regular funds for long-term investment you should pick from the select funds list. If you are agreeable to the conditions mentioned in the article (for suitability), then you may go for one of the high-risk funds.

thanks,

Vidya

Hello Vidya,

Any commentson my “Comment”?

Hello Sunil,

Your suggestion is well taken. But since you would like a comment here it is: 🙂

Tracking macro economic cycles, such as interest rate is certainly no easy task for fund analysts and certainly not so for lay investors. This is the case with sector funds too, where one needs to know the cycles. But some investors do have their views and take such calls. These are ideally meant for them.

Hence, while I can make no promises, if we are confident about the timing of such calls, we will certainly put them out. But otherwise, we would provide sufficient information so that investors can make informed decisions themselves. We would rather err on the side of caution when we do not have conviction in market calls; our first priority in such a scenario would be to manage risk.

Remember, these funds will seldom form part of our mainstream portfolio calls (in our select funds or Smart Solutions or ready-to-go portfolios) for a core portfolio. Tactical calls typically require investors to be active too 🙂

I commented enough 🙂 Thanks again for your open suggestions. Rgds, Vidya

🙂 Thanks Vidya.

I wanted a comment, as i m under impression that my suggestion was missed.

Thanks for Clarifying.

In that case Dynamic Bond Funds will b etaking care of this problem for investors who wants to invest in Debt Funds?? – Am i right?

Hello Sunil, Not all dynamic bond funds behave alike. Like we mentioned in the article, some of them (funds mentioned in the box) take higher risks while few others such as those from Birla, IDFC or UTI are more stable performers and fit an all-season portfolio. This is where fund choices become important based on one’s risk profile and time frame. You may look at debt-long term category in our Select funds list for such funds: http://www.fundsindia.com/select-funds

Tks

vidya

Thanks Vidya.

Hi,

You have not mentioned about the expense ratios for the recommended funds. Over a 1year period, the expense ratio of say 2% shaves off the returns by that amount straight away. In percentage terms it is not a small amount for debt funds. That gives rise to another question: Why some of the debt funds charge such large expense ratios (similar to equity funds)? Are they charging based on returns?

Regards,

Hi Shirish,

The nav disclosed is only after expense ratio. Hence the returns one calculates on NAV is always post expenses. Since the returns are quite good post such expenses, the expense ratio should not worry investors. Only when returns lag benchmark should one take note of expense. Also, these funds have regular expense ratios. The expense ratios for most debt funds is lower. In the funds we mentioned in this article it ranges between 1.5-1.7% Thanks, Vidya

Yet another wonderful article…

FYI, i have already started my investment in BSL Dynamic Bond Fund , give my inability to exactly identify interest rate cycles, i have left that work for the professional.

However, i have liked the statement “You would have to be an active debt investor who can exit the fund once you see interest rate falls approaching an end”.

Now, how do we identify the rate cycle, i can say by my knowledge that we are in middle of the decresing rate cycle. However, we never know, this can go either way from here (depends on many factors).

My take on this is, Funds India having such a wonderful reserch team, why can’t they suggest the starting and ending of Interest rate cycles, may be by a mail for their users atleast (with a disclosure though 🙂 ).

let the investors take teir bet on.

I feel this way, because, you are equipped with the knowledge and data to identify the rate cycles more than what we can do (a normal investor).

I hope this point will be taken into consideration.

Thanks in Advance,

Sunil.

Hi Vidya, Your article came a bit too late for me. Recently invested in IDFC Dynamic Bond Fund. Would love to hear your opinion on the same.

Hello Yogesh, The said article lays out a high-risk strategy for very active investors. who want to ride one wave of the rate cycle. If you are a long-term (3 plus years) investor, your choice of fund is quite judicious. Tks, Vidya

Hi!Vidya,

I want to allocate 10 lacs each( present value) for my daughter’s and son’s education . I have 3 years and 7 years respectively to achieve that. Should i go for debt or equity funds or combination.

3 years –

My present allocation is SIP of 5500 out of which 2000 goes to SBI Dynamic Bond fund, 2000 in SBI FMCG and 1500 in SBI emerging Bsuiness. I also have 10,000 per month RD (All Started in Oct.2012 for 3 years)

5 years –

I also started an SIP of 5000/ month during the same period in ICICI Pru. Discovery fund . I plan to run it for 5 years and redeem it in the 6th year. Meanwhile run a bank RD in the final 2 years.

Reading your article, I feel I should have put the entire SIP in Debt funds.

Please advise me how to go about it?

Rgds

Hello sir,

Three years is not a good enough period to expose entirely in equities. Use a good proportion of say 60-70% in debt and rest in equities. For a 7-year period, you can certainly have 60-70% in equities and rest in debt. Debt is very unlikely to beat equities over such time frames. Hence, you need not worry about not taking too much exposure to debt funds. Have a portfolio of about 2 equity funds and a debt fund for your 7-year goal.

We prefer to address Specific portfolio/fund advice queries through the ‘Ask Advisor’ feature available to all our investors through their FundsIndia account. It is free of charge.

You may wish to take a look at our Smart Solutions for education: http://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=2

of course, you should have a min. 5-year time frame for this as education is a medium to long-term goal.

Thanks,

Vidya

Thank you very much for the advise.

Ajith

🙂 Thanks Vidya.

I wanted a comment, as i m under impression that my suggestion was missed.

Thanks for Clarifying.

In that case Dynamic Bond Funds will b etaking care of this problem for investors who wants to invest in Debt Funds?? – Am i right?

Hello Sunil, Not all dynamic bond funds behave alike. Like we mentioned in the article, some of them (funds mentioned in the box) take higher risks while few others such as those from Birla, IDFC or UTI are more stable performers and fit an all-season portfolio. This is where fund choices become important based on one’s risk profile and time frame. You may look at debt-long term category in our Select funds list for such funds: http://www.fundsindia.com/select-funds

Tks

vidya

Hello Vidya,

Any commentson my “Comment”?

Hello Sunil,

Your suggestion is well taken. But since you would like a comment here it is: 🙂

Tracking macro economic cycles, such as interest rate is certainly no easy task for fund analysts and certainly not so for lay investors. This is the case with sector funds too, where one needs to know the cycles. But some investors do have their views and take such calls. These are ideally meant for them.

Hence, while I can make no promises, if we are confident about the timing of such calls, we will certainly put them out. But otherwise, we would provide sufficient information so that investors can make informed decisions themselves. We would rather err on the side of caution when we do not have conviction in market calls; our first priority in such a scenario would be to manage risk.

Remember, these funds will seldom form part of our mainstream portfolio calls (in our select funds or Smart Solutions or ready-to-go portfolios) for a core portfolio. Tactical calls typically require investors to be active too 🙂

I commented enough 🙂 Thanks again for your open suggestions. Rgds, Vidya

Thanks Vidya.

Hi Vidya,

I have invested in equity portfolio till now (apart from EPF/PPF) and want to diversify to Debts moving corpus from FDs. How would breakup the amount of say 4L in income and other debt funds considering time frame between 1-3 yrs and aggressive risk appetite (age 30 yrs) ?

Will be great if you suggest funds as well.

Thanks,

Nimesh

Hi Nimesh,

You could invest 30% in a short-term debt fund and rest in income funds. For this pick funds in the 1-1.5 years category for short-term debt fund and about 2 income funds from the Debt-long-term category from our Select funds list: http://www.fundsindia.com/select-funds

Request you to use the Ask Advisor feature (available when you click the help tab in your FundsIndia Account) so that we can cater to your specific queries through mails or scheduled calls by our advisors. We can provide specific funds in that forum as it caters specifically to our investors.

Thanks,

Vidya

Out of 2 income funds- Would I be better of choosing one from the list you have mentioned in this blog because they do not seem to appear in the Select-funds list ?

Hi Nimesh,

The funds mentioned in this article are not part of our Select funds because they are tactical funds (funds meant for certain time periods) and considered risky. As mentioned in the article, they are only for high risk investors and should not ideally form part of a core wealth-building portfolio. Hence, if you are looking for regular funds for long-term investment you should pick from the select funds list. If you are agreeable to the conditions mentioned in the article (for suitability), then you may go for one of the high-risk funds.

thanks,

Vidya

Hi,

You have not mentioned about the expense ratios for the recommended funds. Over a 1year period, the expense ratio of say 2% shaves off the returns by that amount straight away. In percentage terms it is not a small amount for debt funds. That gives rise to another question: Why some of the debt funds charge such large expense ratios (similar to equity funds)? Are they charging based on returns?

Regards,

Hi Shirish,

The nav disclosed is only after expense ratio. Hence the returns one calculates on NAV is always post expenses. Since the returns are quite good post such expenses, the expense ratio should not worry investors. Only when returns lag benchmark should one take note of expense. Also, these funds have regular expense ratios. The expense ratios for most debt funds is lower. In the funds we mentioned in this article it ranges between 1.5-1.7% Thanks, Vidya

If I want to get an regular income of Rs 30000 pm how should invest my retirement corpus.

HEllo sir, Pl. use this calculator from our retirement solutions to know how much corpus you need as well as how much you need to save monthly. The calculator will consider future value of your current expenses, taking in to account inflation: http://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=4

Calculator is to your right on the screen. Thanks,Vidya