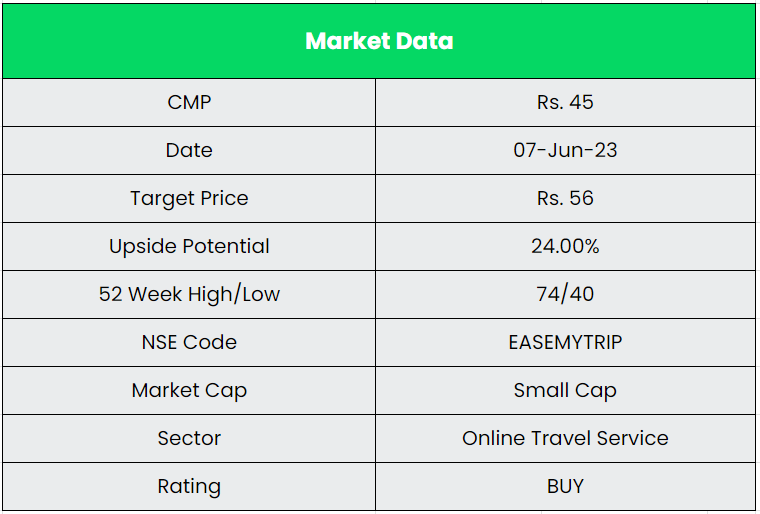

Easy Trip Planners Ltd. – Profitable Travel Agency

Incorporated in 2008, Easy Trip Planners or Easemytrip.com (EMT) was founded as a B2B2C portal providing travel agents access to its website to book domestic travel airline tickets. Subsequently, the company diversified into the business to customer (B2C) distribution channel in 2011 by primarily focusing on the growing Indian middle class population’s travel requirements. EMT now offers a comprehensive range of travel-related products and services for end-to-end travel solutions like online ticket bookings as well as ancillary value-added services such as travel insurance, visa processing and tickets for activities and attraction.

EaseMyTrip provides its users with access to more than 400 international and domestic airlines, over 2 million hotels as well as train/bus tickets and taxi rentals for major cities in India. EaseMyTrip has offices across various Indian cities, including Noida, Bengaluru, and Mumbai. Its international offices (as subsidiary companies) are in the Philippines, Singapore, Thailand, UAE, UK, USA, New Zealand and London.

Products & Services:

The company’s products and services are organized primarily in the following segments.

- Airline tickets – It includes sale of airline tickets as well as airline tickets sold as part of the holiday packages.

- Hotels and holiday packages – It consist of standalone sales of hotel rooms as well as travel packages (which may include hotel rooms, cruises, travel insurance and visa processing)

- Other services – It consists of rail tickets, bus tickets, taxi rentals and ancillary value-added services such as travel insurance, visa processing and tickets for activities and attractions.

Subsidiaries: As on 31st Mar 2023, the company has a total of 11 subsidiaries.

Key Rationale:

- Strong Market Position – Easy Trip’s focused, Asset-light, low-cost, and no-frills approach sets it apart from rest of the online travel agency (OTA) business, in terms of profitability and cash flow. The company’s zero convenience charge policy is a game-changer putting its unprofitable competitors in a difficult situation. Its near-monoline focus (air bookings) and simple strategy have kept it grounded in a very competitive world. The underlying airline business is quite concentrated, more manageable, and thus more profitable for EaseMyTrip. The company’s mantra from the very beginning has been to follow an extremely asset-light, lean cost structure and focus more on technology. This has enabled the company to remain profitable even in challenging times, especially when peers (including industry leaders) have suffered losses. EMT has never reported a single quarter of loss and it proves the company’s stickiness to its strategy. EMT’s market share is more than 10% in the travel market and over 20% in the online travel market.

- Airline Ticket Segment – The company provides airline tickets for domestic travel within India, international travel from and to India and international travel from and to other countries. EMT earns from the airline tickets booked by customers through its platforms in the form of commissions and incentives. Commissions and incentive payments, such as performance linked bonus, are primarily received from GDS (Global Distribution System) service providers, certain airlines as well as credit card companies on a periodic basis, and are generally based on volume of sales generated by the company. In addition, EMT also earns revenue from convenience fee, cancellation service charges, rescheduling charges and advertisement revenue that it may charge along with travel booking. Air Segments booking Volumes were up by 56% YoY with 32 lakhs in Q4FY23 and 62% YoY in FY23 with 1.14 crore. The company has launched an industry-first, free of charge, full refund medical policy through which customers can claim a complete refund on domestic air ticket cancellations caused due to medical emergencies.

- Other Segments – After establishing a key foothold in the air segment, the company focused on expanding its non-air businesses where it has strengthened its hotels business by achieving a whopping 112% during the FY20-FY23 period in terms of room nights. This was achieved as the company strategically gained inorganic growth by acquiring innovative companies across diverse travel segments and evolving into a complete travel ecosystem. Hotel nights booking in FY23 was up by 121% to 3.4 lakhs from 1.5 lakhs in FY22. The company’s Train, Buses & Other segment in FY23 together have seen a booking of 6.2 Lacs up by 10% from 5.6 Lacs in FY22. It also grown at a CAGR of 49% between FY20-23. The Dubai business has continued to thrive, crossing the Rs.100 crs milestone in Gross Booking Revenue in the first year of its operation.

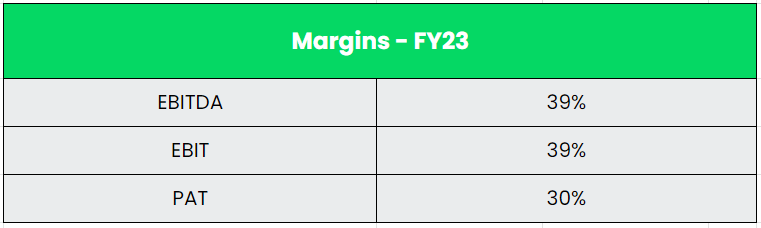

- Financial Performance – The company’s Gross booking revenue reported a massive growth of 117% in FY23 to Rs.8051 crs vs. Rs.3716 crs in FY22. The company’s net revenue posted a growth of 91% YoY in FY23 with an EBITDA growth of 32% YoY to Rs.176 crs. The reported Profit after Tax had a growth of 27% YoY. The company has generated a consolidated Revenue and PAT CAGR of 47% and 60% between FY20-23. The company’s Debt-to-equity ratio stands very low at 0.2x. The average ROE and ROCE of the company for the past 4 years is around 38% and 47%.

Industry:

The Indian Tourism sector ranks among the fastest-growing economic sectors in the country. The industry significantly impacts employment and drives regional development, while also creating a multiplier effect on the performance of related industries. In 2021, the travel & tourism industry’s contribution to the GDP was US$ 178 billion. In light of India’s G20 Presidency and the India@75 Azadi ka Amrit Mahotsav celebrations, the Ministry of Tourism has designated 2023 as the ‘Visit India Year’ to promote inbound travel. The total travel market in India is around Rs.2770 bn in FY23 and it is expected to reach Rs.4045 bn in FY27E at a CAGR of 10%. The total online travel market is around Rs.1865 bn and it expected to grow at a CAGR of 12-13% to reach Rs.2980 bn by FY27E. The Indian domestic passenger volumes in Aviation in nearing pre covid levels with 136 mn in FY23 and it is expected to 1.6x to 220 mn by FY27E.

Growth Drivers:

- In the hotel industry, customers from tier-II and tier-III cities are expected to start booking rooms online on account of the convenience offered by online services.

- In Budget 2023-24, US$ 2.1 billion is allocated to Ministry of Tourism as the sector holds huge opportunities for jobs and entrepreneurship for youth.

- Increased air connectivity to Tier II and III cities at fairly competitive fares, particularly offered by low-cost carriers, prompted Indian consumers to consider air travel as a viable option along with business and leisure travel to such cities, which also had a positive effect on online bookings.

Competitors: Thomas Cook, Make My trip (Unlisted), etc.

Peer Analysis:

In the Listed space, it is clear that East trip easily wins over Thomas cook in terms of Fundamentals. In the overall space (Both listed and unlisted), EMT has the highest gross booking revenue growth CAGR of 24% Between FY20-23 while comparing with its competitors (Makemytrip have grown only at 3% CAGR for the same period). Despite entering the industry at a later stage Easy Trip has a greater number of hotels as compared to the market leader – Make My Trip.

Outlook:

Easy Trip Planners is the fastest growing and profitable company in OTA space in India and is ranked second in the domestic air ticketing space. “Lean cost model” and “No convenience fee strategy” remain key pillars supporting such rapid, profitable growth. This has also led to stickiness by customers with healthy repeat transaction rate of ~86% in the B2C channel. The management believes this is the best time for travel and tourism in India due to the strong pent-up demand. With the anticipated new airports and aircraft, OTAs are becoming increasingly popular compared with direct captive websites or travel agents. Furthermore, the management expects that the OTA industry would benefit from COVID-19 in the long term as customers are being used to doing things online rather than visiting travel agents. Contrary to that, the company is also opened two new offline stores recently in Patna and Surat for the customers who prefer the old school way of “Meet and Greet”.

Valuation:

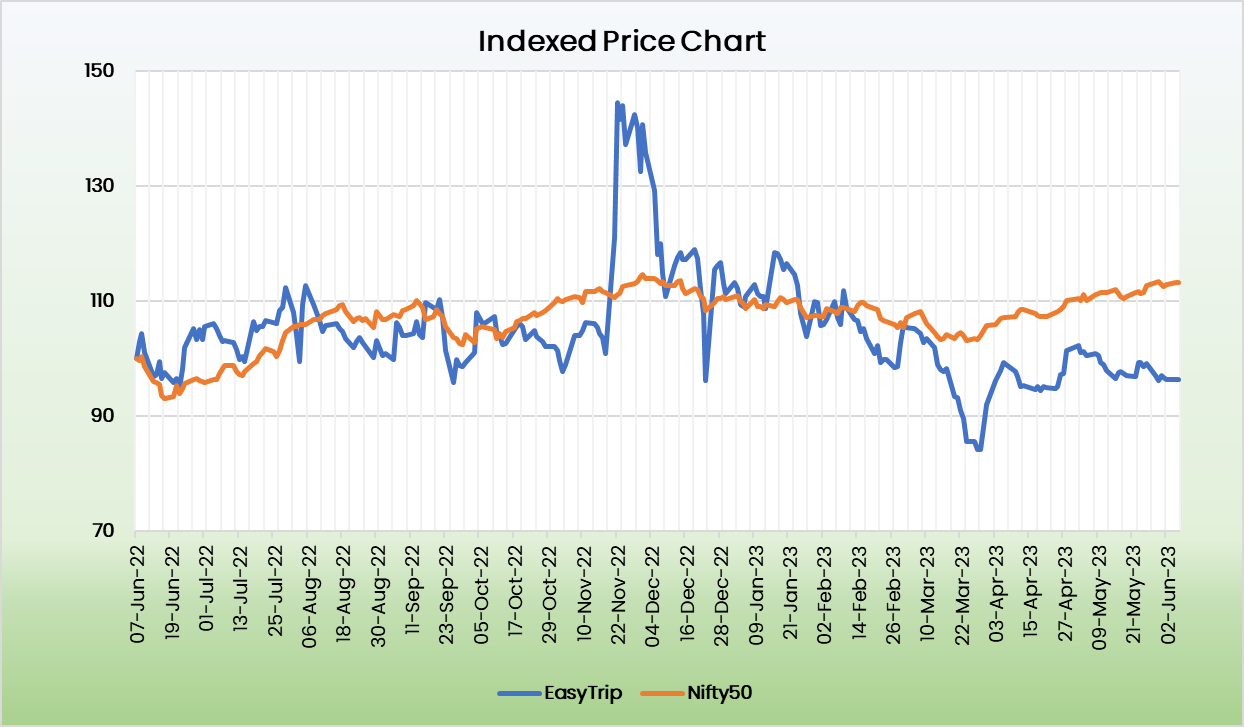

We believe Easy Trip remains a best play in the Travel & Hospitality space supported by its low-cost model and strong balance sheet. At CMP, the stock trades at 33x of FY25E EPS. We recommend a BUY rating in the stock with the target price (TP) of Rs.56, 40x FY25E EPS.

Risks:

- Competitive Risk – The current competitive situation is most benign with the company occupying the second spot in the domestic air ticketing space. However, entry of new players like Flipkart/Amazon having larger pool of 12-14 crore online shoppers compared to ~1+ crore registered customers of EMT will lead to intense competition.

- Profitability Risk – Higher discounts and promotional activity can drive healthy growth but may lead to fall in margins and profitability. The competitors may adopt aggressive discounts/promotions to drive their market share. If the company also chooses to pedal on growth through promotions/discounts, the profitability may get affected.

- Consumer behaviour Risk – The company is highly dependent on factors that affect consumer spending. Prolong muted consumer sentiments can have a huge impact on the company.