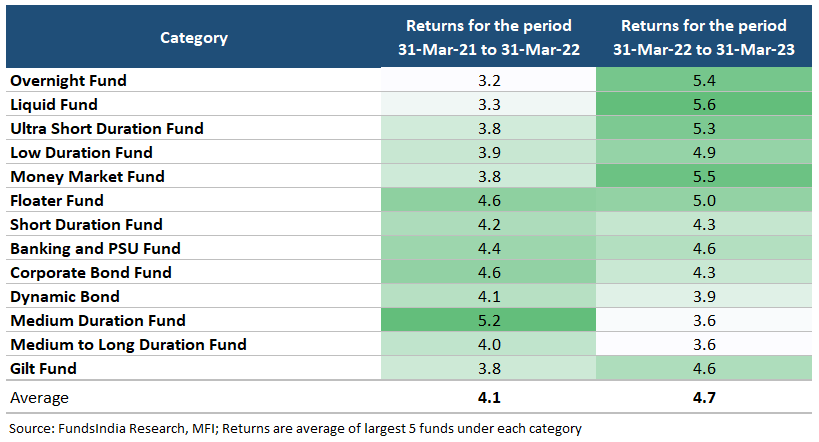

Here are the returns of debt funds in recent years…

One look at this table tells us that the past returns are not great!

And with the recent change in taxation of debt funds, the indexation benefits are also gone.

Does it make sense to invest in debt funds now?

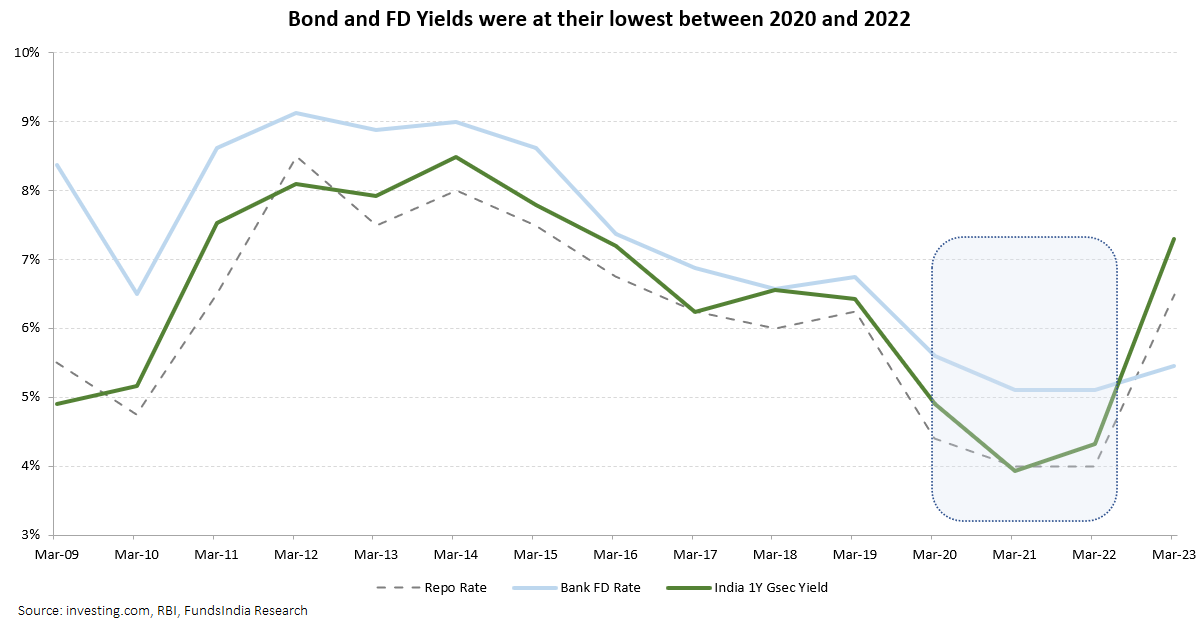

Why are the past returns weak?

For the good part of the last four years, we were in a low interest rate environment. And for the two years between May-2020 and Apr-2022, the repo rate was at a pandemic-led all-time low of 4%.

This low interest rate environment resulted in lower yields across bonds as well as fixed deposits.

However, things have changed drastically in the last 18 months.

RBI has increased the repo rate from 4% to 6.5% in order to curtail high inflation. This has led to bond yields rising across the board.

The rise in yields, while positive for future returns, led to a temporary near term fall in bond prices (refer to our earlier blog here to understand why this happens). This further dampened the past returns of debt funds.

What about future returns?

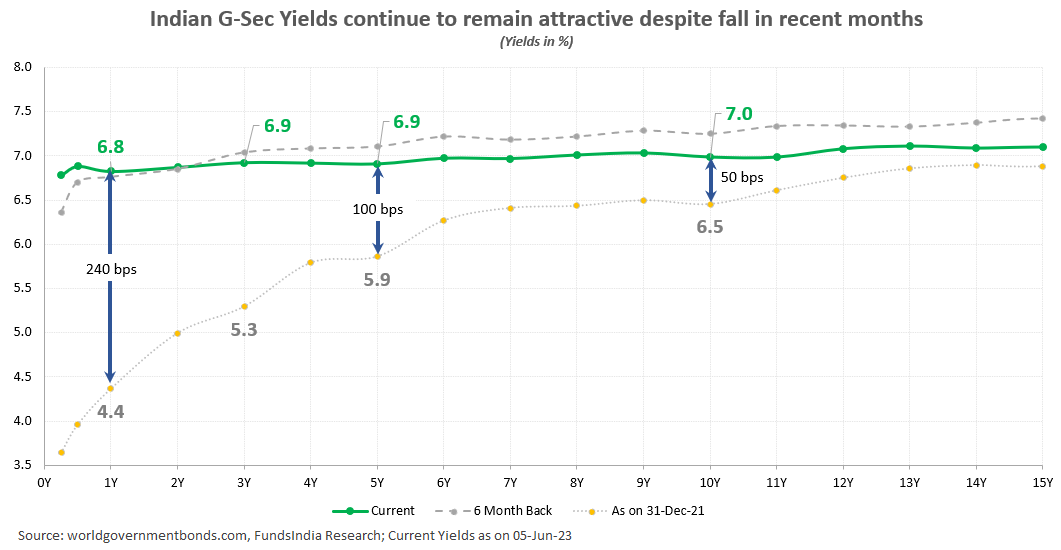

As said earlier, bond yields have increased significantly in the recent past.

To give you some context, between Jan and Nov 2022, the 10-Year bond yields have increased 1.0% and the 1Y bond yields have increased 2.6%.

Though the yields have marginally declined in the last few months, the 3-5 year bond yields (GSec/AAA) still remain attractive (at around 6.9%).

Given the easing inflation scenario in India & US and concerns over global slowdown, yields are unlikely to rise substantially from hereon.

We expect the Indian bond yields to stabilise at the current levels and eventually come down over time.

Any further fall in yields could result in bond prices going up leading to extra returns from your debt fund portfolio (over and above existing yields).

Simply put, future returns from debt funds are likely to be higher than past returns.

But given the recent change in taxation, are debt funds still attractive over FDs?

Before we get into this topic, here is some quick background on the taxation change.

Capital gains from new investments in Debt Funds are now taxed as per your individual slab rates irrespective of the holding period. Previously, Debt Funds had a taxation advantage over FDs (gains from debt funds held for 3+ years were taxed at 20% post indexation).

This change has put the taxation of Debt Funds at par with FDs. Therefore, the choice between Debt funds and FDs going forward will primarily be made on merit of the product vs the taxation rate differential.

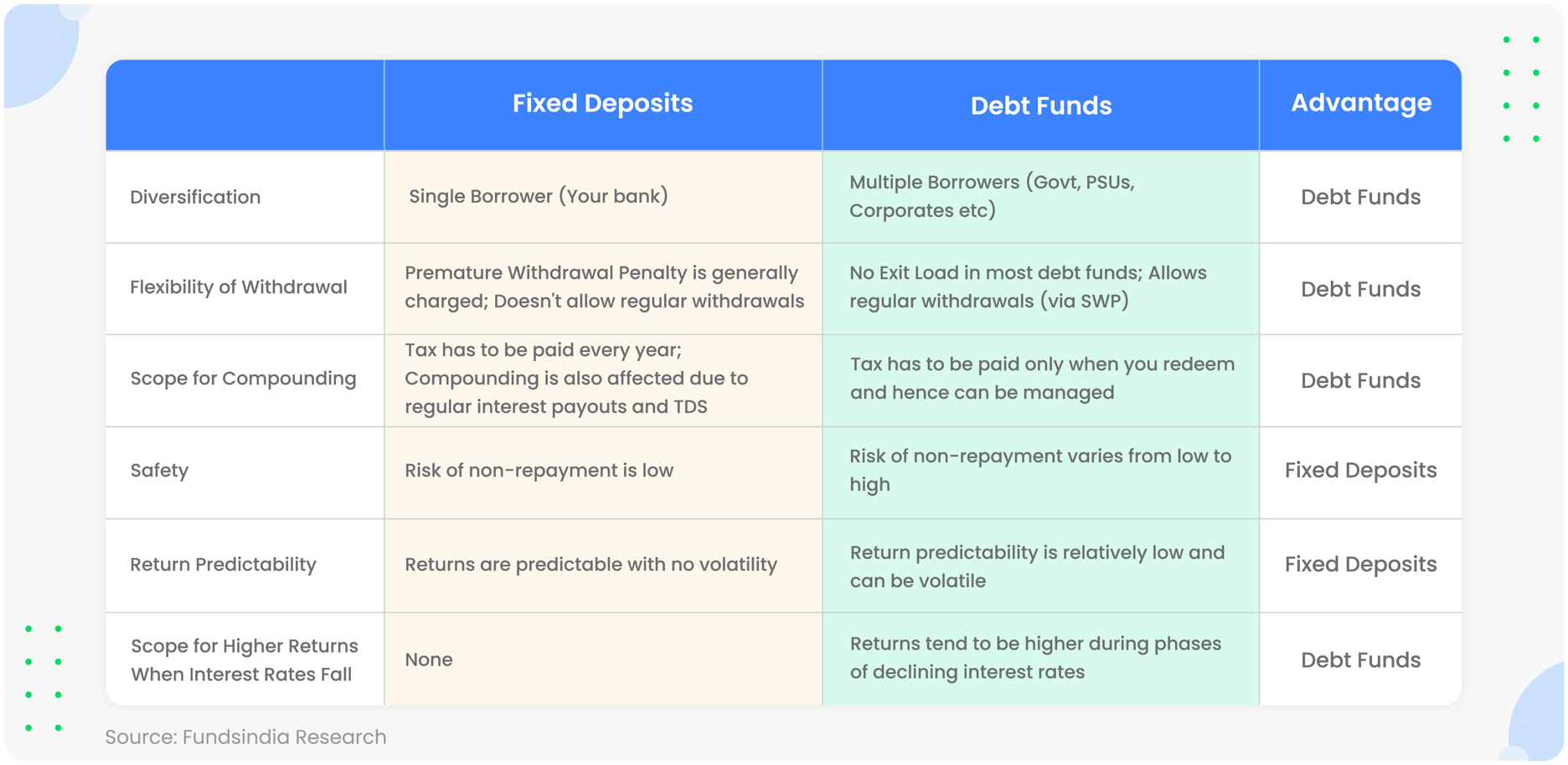

Now, let’s compare Debt Funds to Fixed Deposits and see which one fares better.

Diversification

FD: When you invest in a fixed deposit, you are essentially lending money to a single borrower i.e. your bank.

Debt Funds: When you invest in a debt fund, your money is split and loaned to multiple borrowers. Eg: Central & State Governments, PSUs, Banks and Corporates. This leads to much better diversification.

Advantage: Debt Funds

Flexibility of Withdrawal

FD: A premature withdrawal penalty is generally charged if you want to exit your investments early. It is also not possible to systematically withdraw money from your FDs.

Debt Funds: In most debt funds, the money can be withdrawn anytime without any exit penalty. Further, you have the option to automate your money withdrawals every month by setting up an SWP (Systematic Withdrawal Plan).

Advantage: Debt Funds

Scope for Compounding

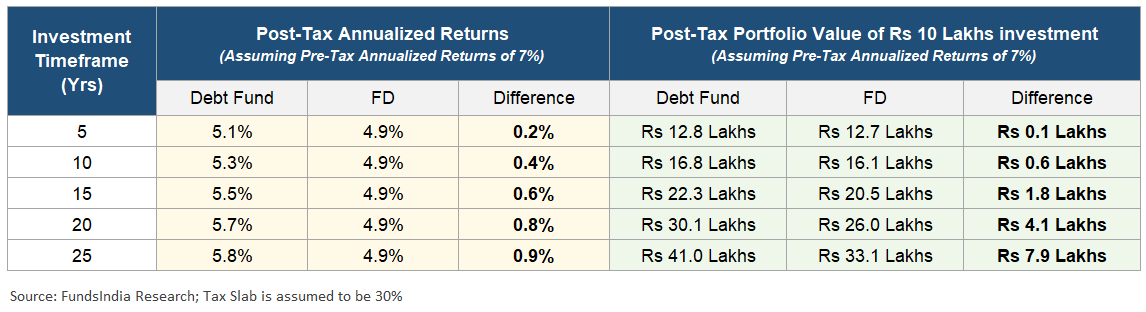

FD: FD returns are taxed EVERY financial year. This is regardless of whether you choose to receive interest every year or on maturity.

For example, let’s say you invest Rs 10 lakhs in a 5-year FD at 6% interest. Here you will have to pay at least Rs 18,000 in tax (assuming 30% slab) every year.

Plus, the regular interest payouts and TDS deduction in FDs also affect compounding.

Debt Funds: Unlike FDs, debt fund gains are taxed only when you redeem. This allows better compounding of returns over the long term.

In debt funds, you also have the option to plan your redemptions in such a way that your tax outlay is reduced. You can lower the tax amount to as much as zero if you use debt funds for post-retirement goals (similar to EPF).

All these result in better compounding outcomes in case of debt funds.

Advantage: Debt Funds

Safety

FD: In fixed deposits, the credit risk (read as the chance of not getting your money back) generally tends to be low especially for large banks. Moreover, the overall bank deposits up to Rs 5 lakhs are insured – which adds to comfort.

Debt Funds: Here the credit risk varies from low to high. But this risk can be minimised to a large extent by choosing debt funds with high credit quality.

Advantage: Fixed Deposits

Return Predictability

FD: The returns are predictable and can be known at the time of investment. There are no fluctuations in your returns unless the bank faces some issues.

Debt Funds: There can be some fluctuations in your returns due to yield movements. The return predictability is therefore lower compared to FDs. However, this has also been addressed to a large extent by Target Maturity Funds.

Advantage: Fixed Deposits

Scope for Higher Returns When Interest Rates Fall

FD: The returns are fixed.

Debt Funds: Debt funds provide scope for higher returns if interest rates fall and vice versa. Bond prices rise when yields fall (positive for debt fund returns) and bond prices fall when yields rise (negative for debt fund returns).

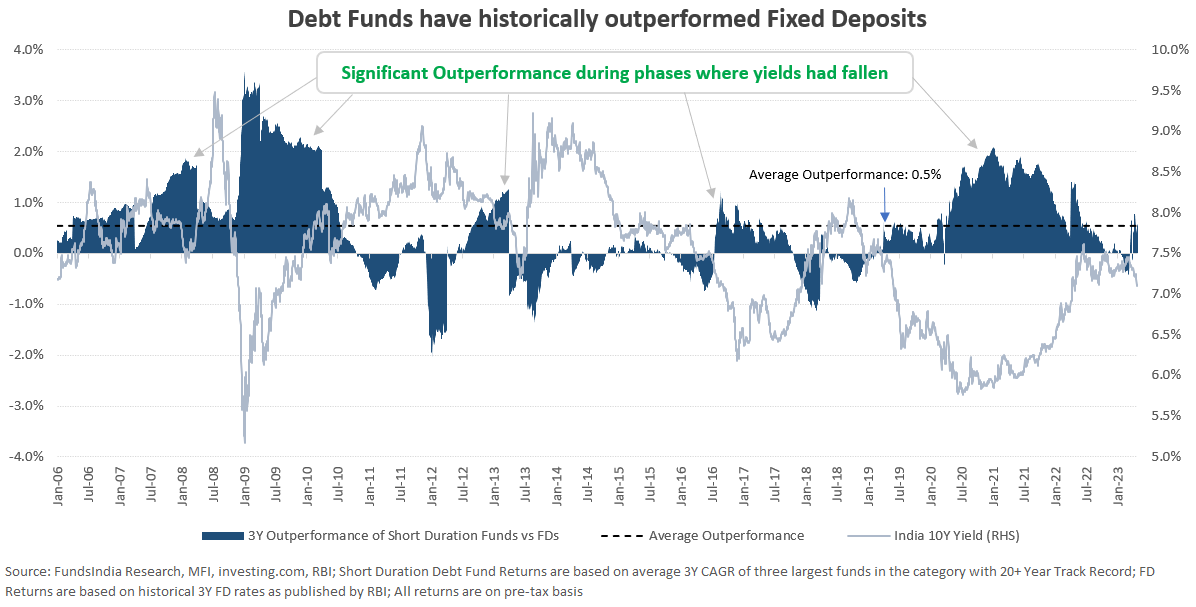

In the last two decades, debt funds have largely outperformed FDs over 3 year periods with an average outperformance of 0.5%.

This outperformance has been much more significant during phases where yields have declined.

And as mentioned earlier, we believe that we are close to peak yield levels of the current interest rate cycle. Any fall in yields could lead to better returns from your debt funds in the near term.

Advantage: Debt Funds

Here is a quick summary of the above…

Verdict

If fixed returns at little to no volatility is your priority, then you can go for fixed deposits.

But if you are willing to tolerate mild volatility, Debt funds are clearly better than FDs despite the taxation changes.

This is because Debt funds provide the potential for extra returns when interest rates fall, better compounding as returns are taxed only during withdrawal, flexibility to withdraw anytime without penalties, and better diversification.

So, how to invest?

We prefer debt funds with

- HIGH CREDIT QUALITY (>80% AAA exposure)

- SHORT DURATION (investing in 1-3 year segment) or TARGET MATURITY FUNDS (investing in 3-5 year segment)

Investors who do not mind slightly higher volatility can also prefer Arbitrage Funds and Equity Savings Funds which enjoy Equity taxation.

Innovative funds or newer categories with 35-65% Gross Equity Exposure may emerge in the coming months as this bucket will continue to enjoy 20% tax post indexation when held for 3+ years. This has already begun with Edelweiss AMC launching Edelweiss Multi Asset Allocation Fund – a debt fund equivalent which holds approximately 50% Arbitrage and 50% Debt.

Summing it up

Debt fund returns in the recent past have been low due to the low-interest rate environment.

But with yields rising significantly in the last 18 months, the future returns are likely to be better than the past. Plus, there could be additional returns from your debt portfolio if yield comes down in the next 1-2 years.

Though the taxation has changed, Debt Funds still hold several advantages over FDs including scope for extra returns when interest rates fall, better compounding as returns are taxed only during withdrawal, flexibility to withdraw anytime without penalties, and greater diversification. If you are planning to invest, prefer High Credit Quality Short Duration Debt Funds or Target Maturity Funds.

An abridged version of this article was originally published in Financial Express. Click here to read it.