Century Plyboards Ltd. – Toughest in the Market

Century Plyboards India Ltd was incorporated in January 1982 by Mr. Sajjan Bhajanka and Mr. Sanjay Agarwal. The company’s manufacturing facilities are located in Joka (West Bengal), Guwahati (Assam), Kandla (Gujarat), Chennai (Tamil Nadu), Karnal (Haryana) and Hoshiarpur (Punjab). The units in Roorkee (Uttarakhand), Myanmar, Laos and Gabon (Africa) are managed by the Company’s subsidiary companies.

The Company’s distribution network comprises of more than 2,700+ dealers who service more than 19,100 retail and sales touch points which are located across 600+ cities and towns in the country. Its proprietary infrastructure also comprises of 28 pan-India marketing offices for the support of trade partners.

Products & Services:

It manufactures plywood, veneer, laminates, medium density fibre (MDF), particle board and allied products.

- Plywood – This is the main segment of the company which has several brands namely Centuryply Club Prime, Centuryply Bond 710, Centuryply WIN MR, Centuryply Blackboard, etc.

- Laminates – In the Laminates segment, the company has several brands namely Look Book, Lucida Kitchen Pro, Star line and Century Exteria.

- MDF – In the MDF (Medium Density Fibre) segment, the company has several brands namely DIR, Century Prowud, Century Prowud ARTZ and Premium Plus.

- Particle Board – It is a small segment which has only one brand named Century Particle Board: Proplank.

Subsidiaries: As on FY23, the company has 13 subsidiaries and 3 step down subsidiaries.

Key Rationale:

- Established Position – The Indian plywood industry is dominated by unorganised players, which account for around 70% of the total plywood market. Century Plyboards is India’s leading plywood manufacturer with a market share of ~25% in the country’s organised segment of the plywood sector, 15% in the organised Laminate sector, 15% in the organised MDF sector and 9% in the organised particle boards. In the overall market (Including unorganised players), the company’s market share in Plywood stands at 5%, Laminates at 8%, MDF at 14% and Particle Boards at 3%.

- Expansion – The capex in FY23 was at Rs.510 crs, largely towards MDF, particle board and laminate expansion. Going ahead, expected capex is Rs.1045 crs for FY24. It includes greenfield expansion for MDF product at Andhra Pradesh under its 100% subsidiary ‘Century Panels Ltd’ and is expected to come on-stream by H2FY24. In the plywood segment, incremental capacity expansion planned is 15,000-20,000 CBM every year in existing facilities and greenfield expansion of 60,000 CBM at Hoshiarpur (commissioning by FY24 end). Additionally, the company is also setting up of a greenfield laminate manufacturing facility in Andhra Pradesh in two phases with an overall installed capacity to manufacture 40 lakh sheets at a capex of Rs.200 crs. The management expects the first phase to get commissioned by Q3FY24. The expected capex is Rs.348 crs for FY25 (largely towards particle board plant in Chennai). The management expects the capacity to come on stream by FY25-end.

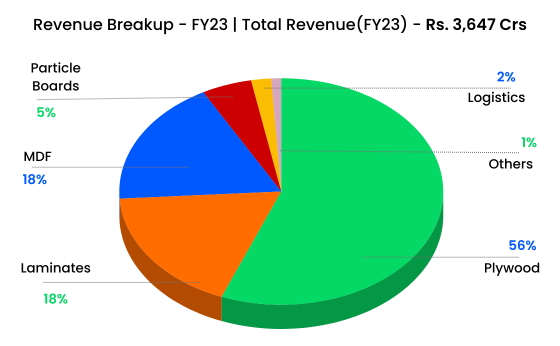

- Q4FY23 – The company reported a revenue growth of 7% YoY in Q4FY23 to Rs.965 crs. The Profit after tax reported a growth of 29% YoY to Rs.115 crs in Q4FY23 and recorded its highest ever quarterly profit by crossing Rs.100 crs. Segment wise, Revenues in the plywood segment have grown 19% YoY to Rs.567 crs, driven by 12.4% volume growth. MDF revenue declined 1% YoY to Rs.161 crs due to 3% decline in volume. Net sales in the laminates division during Q4FY23 declined 7.7% YoY to Rs.160 crs with ~9.2% decline in volumes. Revenues in the Particle board segment declined 20% YoY due to a 18% decline in the volumes.

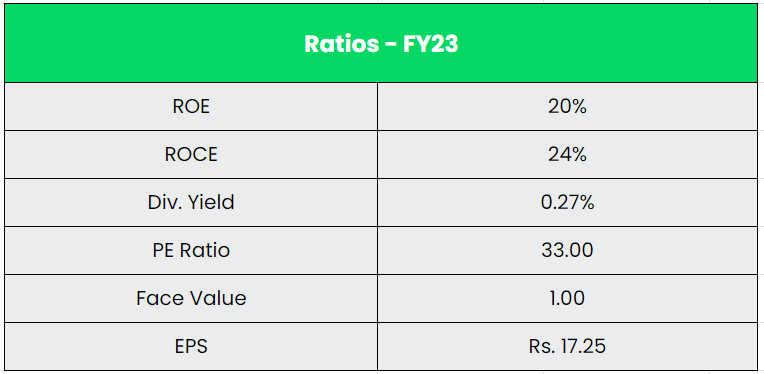

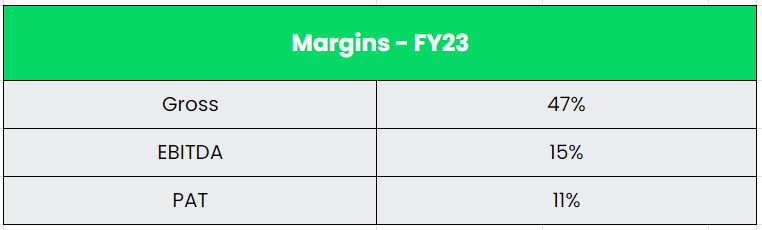

- Financial Performance – The total Plywood volumes of the company have grown at a CAGR of 7% between FY18-23 and the total MDF volumes have grown at a CAGR of 31% for the same period. The company’s revenue and PAT CAGR stands at 13% and 18% between FY18-23. The company has generated a cumulative Operating cashflow (OCF) of around Rs.1750 crs in the past 5 years (FY19-23). The working capital cycle remained healthy at 53 days in FY23 (vs. 63 days at FY22).

Industry:

India is the fifth largest producer and the fourth largest consumer of furniture. The Indian Furniture Market stood at US$ 23.33 billion in FY2021 and it is currently valued at US$ 32 billion, accounting for 5% share in the world market. It is growing at a CAGR of 6.0% to reach US$ 32.75 billion by FY2027 as per a report published by Research & Markets. The furniture exports from India have grown 3x between FY14-23. The Indian plywood market is estimated to be valued at Rs.24,390 crore in 2021 and expected to reach Rs.34,420 crore by 2027, exhibiting a CAGR of 6.0%. The Indian MDF industry was estimated to be Rs.3,000 crore in 2021 and is expected to grow at a CAGR of 15%-20% to Rs.6,000 crore by 2026. According to the industry experts, Indian work from home (WFH) furniture market was US$ 2.22 billion in FY2021 and is expected to be US$ 3.49 billion by FY2026 which would lead to higher demand for MDF.

Growth Drivers:

- The rising desire for modular and state-of-the-art furniture among the people living in urban areas, growing urbanization in Indian states, and rising need for durable and hybrid furniture are all driving the growth of the Indian furniture industry.

- The introduction of numerous initiatives by the Indian government, such as Pradhan Mantri Awas Yojana, DDA Housing Scheme, NTR Housing Scheme, etc., to promote the development of housing projects in the country is catalysing the product demand.

- India’s annual capacity for plywood is estimated at 10 million CBM compared to China’s annual capacity of 200 million CBM as per industry reports. Hence, there is huge penetration opportunity for the Indian plywood industry.

Competitors: Greenply Industries, Rushil Decor, etc.

Peer Analysis:

Century Plyboards is having a leading market share when compared to its closest competitor Greenply Industries. Century Plyboards is also having an upper hand in terms of fundamentals too. Greenply had demerged its business in the past and currently there are three companies namely Greenply Industries (Plywood), Greenpanel Industries (MDF) and Greenlam Industries (Laminates). Century Plyboards still having all the three business into a single company and any chance of demerger in the future will be value unlocking.

Outlook:

The management expects MDF demand to remain healthy (despite rise in imports in recent times) as the industry is expected to grow ~25% in the near term to medium term with higher consumption and better acceptance from consumers. It has guided for 30% volume, value growth in FY24 aided by offtake from new capacity. The guided sustainable margin is 20-25%. In the plywood segment, the management has guided for volume, value growth of 13%, 25% YoY, respectively, driven by healthy traction in the mass segment and its margin is expected to sustain at normalized levels of 12-14%. As a part of the strategy to relook the laminate segment, the company has planned two new large sized laminates, which will be commissioned from its upcoming plant in AP, catering to the export markets. Going forward, the company has guided for ~25% YoY volume, sales growth, respectively, during FY24. Additionally, the management expects margins to be at 12-14% in FY24. The management had earlier indicated that OEMs are major consumers of particle board in India, which is why imports have resulted in price cuts. Going forward, the company has guided for flat volume and sales during FY24 and the margin at the moderated level of ~20%, going ahead.

Valuation:

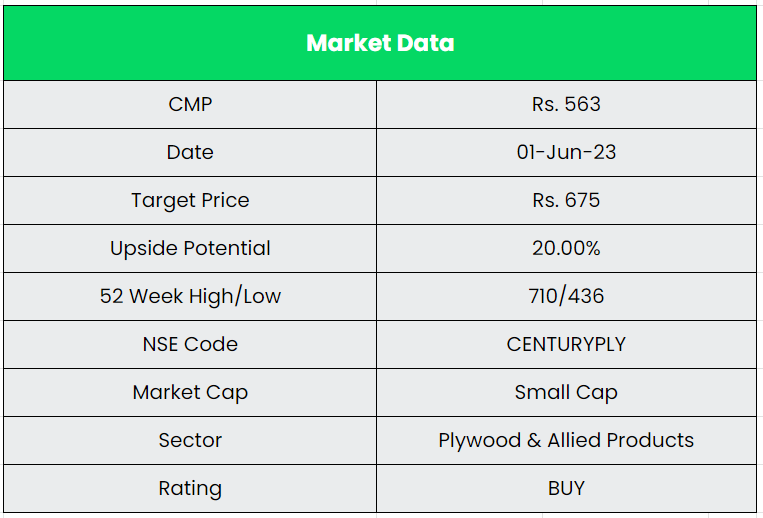

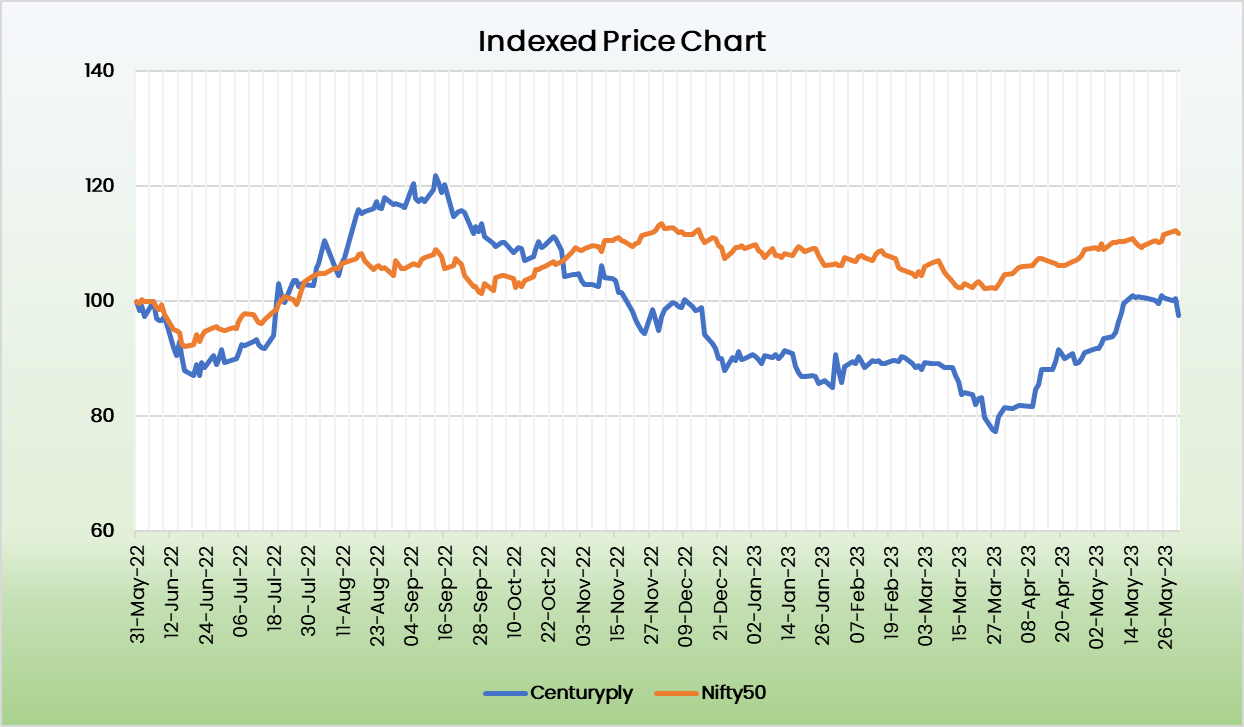

Century Plyboard has the most consistent and strong financial metrics in the industry and remains a leading manufacturer in the plywood segment. Also, the company’s expansion spree for the next two years will pave way for a strong growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.675, 28x FY25E EPS.

Risks:

- Expansion Risk – The company has large capex plans of around Rs.1000-1400 crs during FY23-FY25 and any delay in the expansion will affect the revenue growth of the company.

- Working Capital Risk – With the company manufacturing a wide range of products in plywood, laminates, MDF and particleboard segment, it needs to stock a large volume of raw material and finished goods to cater to the demand.

- Competitive Risk – The unorganized sector accounts for a substantial part (around 76% of the total market size) of the plywood industry. Though, the Century brand name commands premium prices, intense competition from a large number of unorganized and organized players restricts CPIL’s pricing flexibility.