With the CNX Midcap delivering 31% year-to-date thus far in 2014, against the CNX Nifty’s relatively modest 19%, all eyes are on the mid-cap universe. What makes the mid-cap stock universe a superior returning option (albeit with higher downside, no doubt) than their large-cap peers? And should your portfolio have a mid-cap fund to participate in the upside that this market cap segment offers?

What makes them tick?

Less tracked: Broadly, the stocks beyond the top 100 in terms of market capitalization fall under the mid/small-cap category. These stocks, unlike their large peers, are not tracked as vastly and therefore provide enough scope to benefit from information gap – that is market’s lack of knowledge of a particular company, thus leading to its prospects not factored into its price.

A couple of years ago, for instance, not many would have heard about Kaveri Seed Company or Jubilant Foodworks, until these stocks became multi baggers. Kaveri Seed For instance jumped 18 times in 5 years!

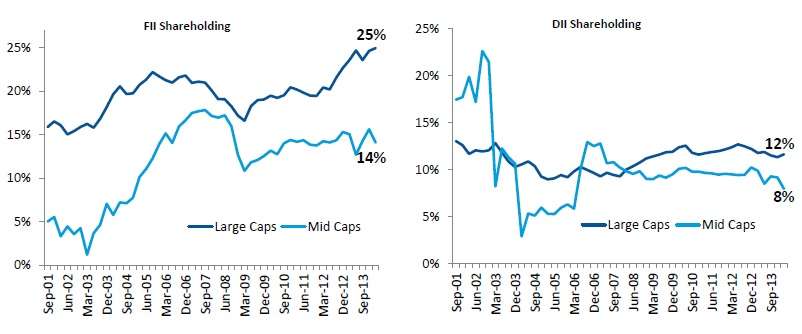

Under-owned nature of stocks: A number of mid-cap stocks are under-owned by broad markets either because they are highly illiquid (as a result o high promoter holding) or are not too known in the markets. As a result o low liquidity, even quality midcaps do not account for a large chunk of many institutional investors as the price impact of entering or exiting such stocks is high. Given below is the ownership pattern of the different market cap segment.

Such under ownership also means that there are enough opportunities to be tapped in this segment, with the right stocks that is.

Re-rating and wealth effect: The mid-sized nature of their business allows quality mid-cap companies to ramp up market share, grow their volumes and often times their profit margins, and achieve a critical mass that gets noticed in the market.

That is when the transition from being a midcap to a nascent large-cap or a large-cap begins to happen; thus leading to the stock suddenly receiving higher valuations, thus bringing the wealth effect.

Take the case of a stock like Lupin – from about Rs 3000 crore of market cap in mid-2005, the stock is now Rs 42,000 crore in market cap – 14 times or a compounded annual growth of over 35% in 9 years!

Unique opportunities

Besides the above, exposure to interesting and niche sectors can be had only through the mid-cap space. For instance, companies in the consumer retail space or internet-based businesses or other unique services would typically be mid-sized and growing. On the other hand, there could also be sectors whose market share is not large but have very dominant mid-cap players present in the segment.

Amara Raja Batteries in the auto ancillary sector or Jubilant Foodworks in the retail consumer segment are examples. Sectors such as logistics, select engineering segments, media and entertainment and retail consumption space would be industries that would have companies one would miss out in the large-cap space.

Having said that, mid-cap stocks are also highly vulnerable for some reasons: one, they often hold large debt in their books, as they typically grow through leverage. During slowdown or high interest rate regimes, therefore, they are the most hurt.

Two, many of them fail to regain market shares that they lost during a slowdown (as larger and more resilient players take over) and are unable to bounce back even when the economy recovers.

Three, exit of a large investor often leads to negative price impact and general pessimism affecting the stocks. Four, Regulatory issues, more often hit smaller companies more either because of the financial impact such regulation may have or other indirect cost of compliances.

How to participate

Hence, it is important to remember, a few rules to invest in the mid-cap space would help you participate adequately without burning your fingers.

One, for every mid-cap stock that is a multi-bagger there could be many that destroyed wealth. There are many stocks that destroyed as much as 90% of investors’ wealth in the years following the 2008 downturn.

Hence, unless you are a knowledgeable investor and research your stocks, direct equities can be risky for you. Use mutual funds to participate in the mid-cap story.

Two, mid-cap funds can be part of your portfolio but cannot be the only segment in your portfolio. Why? One, picking the wrong mid-cap funds can impact your portfolio very badly. For instance, the worst performing midcap fund fell as much as 75% in 2008.

And there are those that still sport single digit or low double digit returns over a 5-year period. That means, unless the fund is able to bounce back with a good portfolio of stocks, it can pull down portfolio performance.

Three, from the above point, it follows that mid-cap funds need a longer time horizon. Over a three-year period ending June 20, 2014, for instance, the CNX Nifty (large-cap index) delivered 12.6% annually, as against 11% annual return in the CNX Midcap. That means, after long periods of underperformance, midcaps can take time to recover. That may leave you with a mediocre portfolio if you had a shorter time frame.

Four, avoid the temptation of going all out on mid-cap funds for the following reasons:

– the mid-cap universe that funds can participate is limited. Hence owning too many mid-cap funds will only duplicate your portfolio.

- Taking very large exposure to a midcap fund is also not advisable for reasons mentioned earlier. Besides, remember that diversified equity funds will always do the job of upping mid-cap exposure when they find opportunities in that segment.

That means, you have to factor in the mid-cap exposure you get through the diversified funds that you may hold as well. Ideally, we would prefer not more than a 30% of equity exposure to pure midcap funds for even a reasonably aggressive investor.

Mid-cap funds have also shown to have cycles of out performance after which some get left behind. For those of you familiar with the mid-cap fund universe, you will know that the star performers of 2005, 2006 or 2007 are no longer the top-quartile names in this market-cap segment today. Hence, even when you are building a portfolio with a mid-cap fund it is imperative to review its performance at least every couple of years.

Lastly, given how mid-cap as a universe can swing, SIPs are the optimal way to invest in this segment to ensure you do not burn your fingers. IDFC Premier Equity, HDFC Mid-Cap Opportunities and Franklin India Prima are among the mid-cap funds that we currently recommend as part of a core long-term equity portfolio.

For those looking for more aggressive options funds such as Franklin India Smaller Companies Fund is an option. If you wish to have a value tilt to your mid-cap holding then ICICI Pru Value Discovery has demonstrated a sound record of performance.

When used judiciously, mid-cap funds can be ideal tools to build your wealth, without hurting yourself in the process.

Mam,

What is diversified funds. Are large & mid cap funds can be said diversified funds?

What are income funds? Is there any difference between short term debt fund and income funds?

Plz calrify..i am not able to find out the exact answer.

Hi Kamal, Diversified funds invest across market cap – large, mid and small. Income funds are debt funds. They invest in debt instruments with an intention to gain from the interest income (that accrues in the instruments) and also from capital appreciation when rates fall. Short-term debt funds invest in instruments with very short-term maturity. Pl. read my article (there is a debt fund to suit every time frame) http://www.fundsindia.com/capitalletter/Capital_letter_Dec12.pdf

to know the diff types of debt funds. Thanks, Vidya

Hi Vidya,

Nice article.

1. Can Mid cap funds be a part of CORE of portfolio?

2. I have SIP in 04 funds- FT Bluechip, PPFAS Long term , UTI Opportunity & ICICI Dynamic Fund.

I want to start SIP in following mid cap funds for 10+ years-

IDFC Pre. EQ, ICICI Pru Discovery & HDFC Mid cap Opportunities- Is my selection better?

Awaiting your valuable comments.

AMOL

Hello Amol,

1. yes you may. provided you do not go overboard. about 20-30% max is good enough.

2. For portfolio specific queries, you would need to use your FundsIndia account (if you have an activated account) and use the help tab – advisor appointment and we can help you with your query. This is a free value add service for all our investors to review/suggest funds.

thanks, Vidya

Hi Vidya,

It’s very nice to read your articles on investments. I have read your above article. After Mr. Modi took over the chair of Prime Minister, all most all Indians are hoping for a good growth in next 5 years. I have read an article that one has even predicted the Sensex level of 75000 in next 3-5 years.

In this scenario, I read many articles that Mid-caps are going to perform better in coming 5 years. So, I have fully concentrated on Midcaps now.

I have been investing in SBI Emerging business & SBI FMCG for the past one year through SIP. They were out performers before I started investing. After that FMCG fund was not performed as per market movements. My investment in Emerging Business Fund grown above 30% where as FMCG only 10%

I want to continue investing them through SIP for the next 5 yesrs and want to get an average returns of 25%

is it possible as per your vision. Or you are going to suggest another options to get 25% /per for next 5 years.

I can take full risk also for this. Please cc to my personal mail also. Please suggest the super funds for my target.

Thanks a lot.

Hello Purnaiah,

we have raised a ticket in your name and responded through that. In future, pl. use the help tab in your account as use the ‘advisory appointment’ feature to raise portfolio queries. The blog is a general discussion forum. thanks, Vidya

I think a good strategy and an excellent article , I recently interested in investing in the stock market, I think the key is to practice operations on a demo account , I found this page which tells you how to do it , I hope they serve http://trading60sec.com, for those who can not invest in large

Hello, I am a your loyal and regular website reader and finally thought of asking you a question.

I am giving my portfolio below. I am 33 now and have a kid of 4 year old.

My monthly income with spouse is 2 lakh. I have home loan of 50 lakh.

I am doing investment in all four mutual funds from last five years.

My goal is to have 1 Crore in next 15 years for kid’s education and 2 Crore in next 25 for retirement at the age of 60. I have taken inflation in mind.

Can you please review the information and help me if I can complete my goals. Appreciate if you give some suggestions. Thank you.

5,000 per month – Reliance Regular Savings Growth Equity NOW Reliance Value Fund

5,000 per month – DSP Blackrock Top 100

5,000 per month – Birla Sunlife Front Line Equity

5,000 per month – SBI bluechip fund growth direct

10,000 per month – RD

3 lakh FD

1 Crore Term Insurance Insurance cover

Total 10 Lakh LIC cover from Jeevan anand and Jeevan tarang

Hello Sir, Thank you for writing to us. We do portfolio advice and review through our advisors.We are constrained from doing any advisory through this forum. if you have an account with us, please write to us and we will help you build a plan and review your portfolio. Thanks, Vidya

Good afternoon,

I invest through SIP in three different fund. Each SIP is of 30,000. I have two large cap and one mid cap fund.

Now I have 3.6 lakh as a surplus. The questions is:

Can I do additional purchase of around 10,000 each month in each fund that is 30,000 per month for next 12 months rather than doing a lump sum purchase?

Please advice your opinion. Thank you.

Hello,

It is better to invest Rs 10,000 per month than a lump sum purchase at this point. If you have a large sum to invest today, you can set up an STP into your equity funds. Given the size of your investment, you can add a fourth fund to the three you have now, instead of your current idea of stepping up the investment by an additional Rs 10,000. You will have a very high concentration in each fund, otherwise.

Thanks,

Bhavana

Hi,

I invest in these three funds. 1. Aditya birla sunlife front line equity 2. Parag parikh long term equity 3. SBI bluechip

My amount for each fund is 10,000 per month. My goal is to generate 3 Cr. for retirement at 60. That is after 30 years. I am a moderate risk taker.

I know that I have two large cap and one multi cap. The question is can I add “kotak standard multicap” as another multi cap. Is this advisable?

I have regular investments in Post office schemes to cover my debt part of the investments, please help. Thank you very much.

Hello,

Apologies for the delay in reply. You can use calculators to assess how much you would need to save to reach Rs 3 crore in wealth, here. Adding a multicap fund to your existing funds is certainly doable and Kotak Standard Multicap is one that does not get too aggressive. However, it also depends on your allocation to each fund. Please talk to your advisor to get a through understanding.

Thanks,

Bhavana

Hi,

I invest in these three funds. 1. Aditya birla sunlife front line equity 2. Parag parikh long term equity 3. SBI bluechip

My amount for each fund is 10,000 per month. My goal is to generate 3 Cr. for retirement at 60. That is after 30 years. I am a moderate risk taker.

I know that I have two large cap and one multi cap. The question is can I add “kotak standard multicap” as another multi cap. Is this advisable?

I have regular investments in Post office schemes to cover my debt part of the investments, please help. Thank you very much.

Hello,

Apologies for the delay in reply. You can use calculators to assess how much you would need to save to reach Rs 3 crore in wealth, here. Adding a multicap fund to your existing funds is certainly doable and Kotak Standard Multicap is one that does not get too aggressive. However, it also depends on your allocation to each fund. Please talk to your advisor to get a through understanding.

Thanks,

Bhavana

I read your blog and it is always helpful. Your tips on investing are excellent.

I am investing in these 40,000 schemes from 2015. I am 27 yrs. old I want to accumulate wealth when I am 50 and goal is around 2 crore.

I have done a lot of research before investing it. All are direct plans. I just want to evaluate my portfolio and need you help to understand your views.

Kotak Emerging Equity Scheme – Mid Cap – 5,000

Reliance small cap – Small Cap – 5,000

Parag parikh long term equity – multi cap – 5,000

SBI bluechip – large cap – 15,000

Aditya birla sunlife front line equit – large cap – 10,000

Hello,

Thanks for your feedback!

We do not disseminate portfolio-specific advice on this forum. It is primarily for discussion and explanations of events and concepts. We use official channels through our platform for advisory, since we need to keep track of advice being asked for and provided, and for own accountability.

Please talk to your advisor for portfolio evaluations.

Thanks,

Bhavana

Mam,

What is diversified funds. Are large & mid cap funds can be said diversified funds?

What are income funds? Is there any difference between short term debt fund and income funds?

Plz calrify..i am not able to find out the exact answer.

Hi Kamal, Diversified funds invest across market cap – large, mid and small. Income funds are debt funds. They invest in debt instruments with an intention to gain from the interest income (that accrues in the instruments) and also from capital appreciation when rates fall. Short-term debt funds invest in instruments with very short-term maturity. Pl. read my article (there is a debt fund to suit every time frame) http://www.fundsindia.com/capitalletter/Capital_letter_Dec12.pdf

to know the diff types of debt funds. Thanks, Vidya

Hello, I am a your loyal and regular website reader and finally thought of asking you a question.

I am giving my portfolio below. I am 33 now and have a kid of 4 year old.

My monthly income with spouse is 2 lakh. I have home loan of 50 lakh.

I am doing investment in all four mutual funds from last five years.

My goal is to have 1 Crore in next 15 years for kid’s education and 2 Crore in next 25 for retirement at the age of 60. I have taken inflation in mind.

Can you please review the information and help me if I can complete my goals. Appreciate if you give some suggestions. Thank you.

5,000 per month – Reliance Regular Savings Growth Equity NOW Reliance Value Fund

5,000 per month – DSP Blackrock Top 100

5,000 per month – Birla Sunlife Front Line Equity

5,000 per month – SBI bluechip fund growth direct

10,000 per month – RD

3 lakh FD

1 Crore Term Insurance Insurance cover

Total 10 Lakh LIC cover from Jeevan anand and Jeevan tarang

Hello Sir, Thank you for writing to us. We do portfolio advice and review through our advisors.We are constrained from doing any advisory through this forum. if you have an account with us, please write to us and we will help you build a plan and review your portfolio. Thanks, Vidya

Hi Vidya,

Nice article.

1. Can Mid cap funds be a part of CORE of portfolio?

2. I have SIP in 04 funds- FT Bluechip, PPFAS Long term , UTI Opportunity & ICICI Dynamic Fund.

I want to start SIP in following mid cap funds for 10+ years-

IDFC Pre. EQ, ICICI Pru Discovery & HDFC Mid cap Opportunities- Is my selection better?

Awaiting your valuable comments.

AMOL

Hello Amol,

1. yes you may. provided you do not go overboard. about 20-30% max is good enough.

2. For portfolio specific queries, you would need to use your FundsIndia account (if you have an activated account) and use the help tab – advisor appointment and we can help you with your query. This is a free value add service for all our investors to review/suggest funds.

thanks, Vidya

Good afternoon,

I invest through SIP in three different fund. Each SIP is of 30,000. I have two large cap and one mid cap fund.

Now I have 3.6 lakh as a surplus. The questions is:

Can I do additional purchase of around 10,000 each month in each fund that is 30,000 per month for next 12 months rather than doing a lump sum purchase?

Please advice your opinion. Thank you.

Hello,

It is better to invest Rs 10,000 per month than a lump sum purchase at this point. If you have a large sum to invest today, you can set up an STP into your equity funds. Given the size of your investment, you can add a fourth fund to the three you have now, instead of your current idea of stepping up the investment by an additional Rs 10,000. You will have a very high concentration in each fund, otherwise.

Thanks,

Bhavana

I think a good strategy and an excellent article , I recently interested in investing in the stock market, I think the key is to practice operations on a demo account , I found this page which tells you how to do it , I hope they serve http://trading60sec.com, for those who can not invest in large

Hi Vidya,

It’s very nice to read your articles on investments. I have read your above article. After Mr. Modi took over the chair of Prime Minister, all most all Indians are hoping for a good growth in next 5 years. I have read an article that one has even predicted the Sensex level of 75000 in next 3-5 years.

In this scenario, I read many articles that Mid-caps are going to perform better in coming 5 years. So, I have fully concentrated on Midcaps now.

I have been investing in SBI Emerging business & SBI FMCG for the past one year through SIP. They were out performers before I started investing. After that FMCG fund was not performed as per market movements. My investment in Emerging Business Fund grown above 30% where as FMCG only 10%

I want to continue investing them through SIP for the next 5 yesrs and want to get an average returns of 25%

is it possible as per your vision. Or you are going to suggest another options to get 25% /per for next 5 years.

I can take full risk also for this. Please cc to my personal mail also. Please suggest the super funds for my target.

Thanks a lot.

Hello Purnaiah,

we have raised a ticket in your name and responded through that. In future, pl. use the help tab in your account as use the ‘advisory appointment’ feature to raise portfolio queries. The blog is a general discussion forum. thanks, Vidya

I read your blog and it is always helpful. Your tips on investing are excellent.

I am investing in these 40,000 schemes from 2015. I am 27 yrs. old I want to accumulate wealth when I am 50 and goal is around 2 crore.

I have done a lot of research before investing it. All are direct plans. I just want to evaluate my portfolio and need you help to understand your views.

Kotak Emerging Equity Scheme – Mid Cap – 5,000

Reliance small cap – Small Cap – 5,000

Parag parikh long term equity – multi cap – 5,000

SBI bluechip – large cap – 15,000

Aditya birla sunlife front line equit – large cap – 10,000

Hello,

Thanks for your feedback!

We do not disseminate portfolio-specific advice on this forum. It is primarily for discussion and explanations of events and concepts. We use official channels through our platform for advisory, since we need to keep track of advice being asked for and provided, and for own accountability.

Please talk to your advisor for portfolio evaluations.

Thanks,

Bhavana