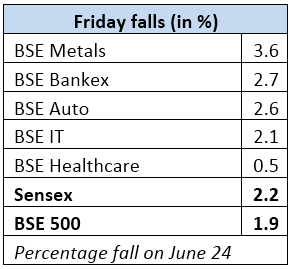

![]() The epic, if divisive, vote last Thursday that decided the United Kingdom’s exit from the European Union was a bombshell for the financial and political worlds. Stock markets across Europe, the US, and Asia crashed between 4 to 8 per cent, the pound plummeted, and commodity prices dipped.

The epic, if divisive, vote last Thursday that decided the United Kingdom’s exit from the European Union was a bombshell for the financial and political worlds. Stock markets across Europe, the US, and Asia crashed between 4 to 8 per cent, the pound plummeted, and commodity prices dipped.

What does this massive upheaval mean for your investments?

India, being a relatively smaller trade partner with the UK and EU and a net commodity importer, is shielded from much of the impact from Brexit. Hence, our growth story is still intact. Where it can hurt our markets is in foreign institutional inflows and currency fluctuations in the short to medium-term.

Financial markets, including our own, will be unstable for the next several weeks as the financial world digests the news. And that presents opportunities for you. This is the time for you to deploy your surplus and use this volatility to average down your investment costs. Over the long term, India, being the few spots of growth, in a tottering global economy should attract foreign flows once more.

Global impact

Brexit’s hardest impact will be, obviously, on UK’s economy as it breaks away from the union it has been a part of for decades. For starters, it loses access to the single market EU bloc, which forms about half its trade It will also mean no common trade agreements, as much of its other trade also came through the EU bloc agreements. This will pose the risk of more trade barriers and higher trade costs. It also requires the drawing of fresh trade agreements with countries.

Second, the EU is a major source of FDI for the UK and the city of London is the largest global financial centre. Changing regulations post the exit can affect both. Third, renegotiations involved in a number of other issues – such as access to open air space, status of immigrants and movement of Britons and EU nationals within the Eurozone – could all mean uncertainty in various industries, travel, tourism and also the job market.

Until the UK and the EU are able to find a new normal, there could be an intermediary slowdown in their trade, productivity and investments, thus causing an economic slowdown. This in turn could pull down global growth – especially as nations exporting to the zone see a dip in demand. While central banks across countries have pledged to support growth, what measures they will take remains to be seen.

Of course, the exit process has to be officially invoked first, and this in itself can get delayed. Further, once begun, the entire seceding process can take years to complete, and the method and impact is far from clear.

What is clear is that uncertainty will rule for the short to medium-term, shrinking the risk appetites of the financial markets until clarity emerges.

Impact on India

There are four key areas where India will be affected, to varying degrees:

Currency: Exchange rate fluctuation is the biggest fallout, for India, from Brexit. Uncertainty and a lower risk appetite can lead to an appreciation in the dollar and other safe havens such as gold and the yen, in turn depreciating the rupee and other emerging market currencies. Further, the FCNR redemptions due in September-November this year can pressure the rupee. Companies that have overseas borrowings can also get hit, depending on their loan tenure and extent of hedging. At the same time, the currency depreciation can keep India reasonably competitive, especially in a slowing demand scenario.

Trade: India is not a huge trade partner with the UK. Ministry of Commerce data shows that goods exports to UK have accounted for just around 3 per cent of the total from 2012-13 onwards, while imports are half that. Depreciation in the pound, a UK economic slowdown, and renegotiation of trade deals will thus have minimal overall impact. FDI inflows into our economy from the UK are also low at 2 per cent of the total in 2015-16, down from the 14 per cent in 2013-14, according to DIPP data.

Sector-specific: Though India is, more or less, insulated from the UK-EU turmoil, specific sectors will be hit on rupee appreciation against the pound or euro. The first is software, where reports peg UK’s share at 17 per cent of the total software exports. Some deals can become unviable while there can be delays in signing new deals. The IT sector has the second-heaviest weight in the BSE 500 and the Sensex.

The second is pharmaceuticals, which account for 5 per cent of exports to the UK. However, the US is by far the biggest market for this sector. The third large sector that will be impacted is auto ancillaries, which are huge exporters to the entire EU zone – for some listed players, the region forms close to half their revenues. Other smaller sectors that are exporters, but which don’t have much stock market representation are textiles, (accounts for 32 per cent of our exports to the UK) and gems and jewellery (6 per cent of UK exports). Metals and steel companies may also be affected as a growth slowdown caps commodity prices and realisations.

But given the diversified nature of companies in these sectors, the fall-out is likely to be very stock-specific. The market hasn’t reacted too sharply to the sectors as a whole, either.

Stock markets: The changing global economy, central bank actions, and currency fluctuations can prompt FPIs to rework their strategies. Besides, London is a leading financial centre, home to one of the largest stock and futures markets, several global pension funds, hedge funds, mutual funds, and insurance companies. Global equity flow can be further affected if regulations concerning capital flow and taxes change. Domestic markets can, therefore, see turbulence in the short to medium-term. FPIs hold 40 per cent of the BSE 500’s free-float capital and their moves sway the market.

India’s fundamentals hold

Over the longer term, however, FPI flows can return as India is among the few regions of growth in the slowing global economy. Besides, our own markets are strong – mutual funds have used FPI selling as opportunities over the past year thereby shoring up the market. So, a sustained equity inflow into MFs can be of some support.

- We are a net commodity importer. Muted prices of commodities such as steel, oil, and metals due to a potential slowdown will in fact be beneficial for us.

- We are a more domestic-driven economy. Consumer durable production captured in the IIP has been growing from last June. Retail bank credit is up 19.2 per cent in the past one year. They point to urban consumption recovery. The Seventh Pay Commission, due to be implemented, will increase domestic income. A consumption uptick can eventually drive production revival.

- Monsoon progress across the country has caught up, and the deficit in rainfall that had been in place so far is rapidly shrinking. Rural incomes, hit by two years of drought, can stage a comeback, broadening the consumption base.

- The index for the eight core industries has been improving from December, on the backs of increased production in electricity, cement, fertilisers, refineries, and coal. Sales of commercial vehicles, road toll rates, infrastructure project awards and progress, and so on are also on the uptick. All these are initial pointers to recovery in production and signs of capital investment.

- Corporate revenues finally arrested their decline in the March 2016 quarter, with even sectors such as infrastructure and engineering clocking revenue growth. Sustained low input costs can further boost profitability and earnings.

- RBI repo rate cuts and liquidity management measures are beginning to translate into lower interest rates. With more room to cut rates and a stable fiscal, the hitherto sedate industrial credit can pick up.

All this indicates that economic and corporate growth is bottoming out and long-term growth prospects are firmly in place. Even among other emerging market nations, India has stronger fundamentals.

What should you do?

The first and most important point is to continue with your SIPs. The bedlam gripping markets now should not push you into selling out or stopping your SIPs. With volatility on the cards, this is the best time to average investment costs lower. Since uncertainty can prevail for a good while, staggering your surplus over five to six tranches over the next few weeks will be a prudent move, especially for those of you who missed the opportunity in January and February this year. This investment can be in addition to your regular SIPs.

You can increase investments in your existing equity funds. If you’re looking for other funds to invest in, choose from the three below. We are suggesting these as they are a bit more volatile (allowing you better averaging in a short period), they have a mix of large-caps and mid-caps and represent different sector plays. Large-caps may also fall more than mid-caps in the immediate future if foreign investors pull out.

Birla Sun Life Frontline Equity: This is a large-cap fund with exposure to key export sectors such as IT and pharma, making it a slightly contrarian theme should exports from these sectors take a hit. Still, it has lower weights to these sectors compared with the index.

Kotak Select Focus: This is also a large-cap fund with some exposure to mid-caps. It has a low allocation to software, pharma, and auto ancillaries. This fund would be better if you wish to play on domestic themes such as banking and construction, and avoid any potential export fallouts.

Franklin India Prima Plus: This is a diversified fund with slightly higher standard deviation. The fund is currently betting on banking, engineering, and telecom. It has limited allocation to software, automobiles, and pharma.

For long-term investors, the takeaway is to deploy more, or, at the very least, stay invested. We know that market crashes happen, just as we know that bounce backs also follow.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Is it possible for me to invest 10000 RS more in next month SIP? If so how can I do that? how that is going to benefit me?

Hi Vipin,

Do you mean a one-time investment of Rs 10,000 next month? If so, you won’t be able to add it to your SIP, since SIPs are regular investments. The benefit in adding to your investments in phases over the next few weeks is to take advantage of any volatility that can come in. While the market is up for the past two days, there is still uncertainty in global markets. Investing more in such times will help average down investment costs if you hold for the long-term. As such, the extent to which you will be able to average costs depends on your existing investment and how much you can invest.

Thanks,

Bhavana

Detailed and Helpful article indeed.

Please clarify: when you say “short to medium term” , how long tenure are we looking at? (like, x months to x years)

Thanks, Ranga. It is hard to specifically say ‘x’ months because a lot depends on what the exit procedure is, what central banks do (in fact, expectations that central banks will be more accommodative to push growth has boosted sentiments this week), and the extent of the actual impact. Our own monsoon progress and earnings numbers for the next couple of quarters are other drivers for the market. All this together will help address uncertainties, in turn reducing volatility.

Regards,

Bhavana

I am following your articles regularly from few months. It provides very useful key informations to the beginners like me in mf feild. I am Investing 2000 rs per month in sbi small and midcap fund and pharma fund from one year.is my portpholio on right track? Could you please sujest other than this? If any.

I am following your articles regularly from few months. It provides very useful key informations to the beginners like me in mf feild. I am Investing 2000 rs per month in sbi small and midcap fund and pharma fund from one year.is my portpholio on right track? Could you please sujest other than this? If any.

Is it possible for me to invest 10000 RS more in next month SIP? If so how can I do that? how that is going to benefit me?

Hi Vipin,

Do you mean a one-time investment of Rs 10,000 next month? If so, you won’t be able to add it to your SIP, since SIPs are regular investments. The benefit in adding to your investments in phases over the next few weeks is to take advantage of any volatility that can come in. While the market is up for the past two days, there is still uncertainty in global markets. Investing more in such times will help average down investment costs if you hold for the long-term. As such, the extent to which you will be able to average costs depends on your existing investment and how much you can invest.

Thanks,

Bhavana

Detailed and Helpful article indeed.

Please clarify: when you say “short to medium term” , how long tenure are we looking at? (like, x months to x years)

Thanks, Ranga. It is hard to specifically say ‘x’ months because a lot depends on what the exit procedure is, what central banks do (in fact, expectations that central banks will be more accommodative to push growth has boosted sentiments this week), and the extent of the actual impact. Our own monsoon progress and earnings numbers for the next couple of quarters are other drivers for the market. All this together will help address uncertainties, in turn reducing volatility.

Regards,

Bhavana