Over the last 6 months, markets have been in the red often. While BSE Sensex and NSE Nifty 50 are back to their all time highs, small and midcap indices are far from their January 2018 peaks. The BSE small cap index has fallen by 19% and Mid cap index is down 12% from their Mid-January levels.

This is the time when investors start to panic. They wonder if they should get out of their funds or stop their SIPs. In the past, we have addressed why continuing to invest during the downturn is essential to make good gains from equity.

However, this article is not about that. This article tries to address the basic concern of why investors panic and whether there is a reason to panic. And finally, it tries to answer what measures an investor should take to prevent future shocks.

Understanding volatility

To explain this, it is important to first explain volatility. Volatility is a measure of variation in the price of an asset. This variation is measured by taking the average difference between the highest and lowest prices of the stock over a period of time. A stock which rises more, falls more.

Often times, volatility is used as a synonym for risk. This is ok for textbooks but is not really the case. Volatility is either a reaction to a risk event or an anticipation of a risk event that may or may not transpire. Volatility, therefore, tends to be higher in asset classes where prices are driven mostly by sentiments or where there isn’t enough information or direction or fundamentals about where the asset class or the company is headed. Bitcoins are a classic example of a high-volatile asset class not backed by sufficient fundamentals. Similarly, in the equity space, small-cap stocks are more prone to volatility simply because the likelihood of risky events transpiring is higher than in a large-cap stocks. The information arbitrage is also higher in small-cap stocks than in large-cap stocks. Thus, volatility causes sharp swings in the performance of an instrument/asset class.

Effects of volatility on the market

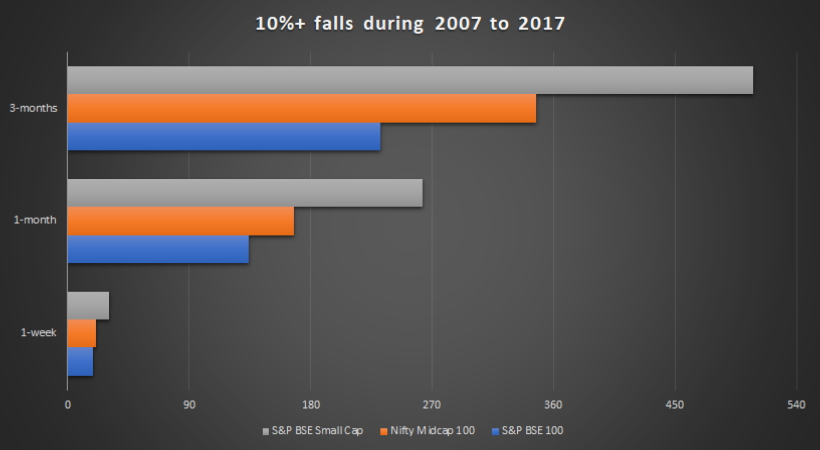

Consider this – during the years 2007 to 2017, there were 263 instances where BSE Small cap index fell by 10% within a month and 31 instances when it fell by 10% within a week. Imagine investing Rs. 5,00,000 in a fund and seeing its value fall to Rs 4,40,000 in a week. How would you react? In contrast, the number of such instances in the BSE 100 index were just 134 and 19 over a month and week respectively.

However, the year 2008 was an anomalous year. We generally don’t see such catastrophic falls. So we also counted the number of times these indices fell by more than 10% in a month after leaving out this year. The numbers were 148 for small cap index and 43 for BSE 100. So even if you had escaped the major correction, your small cap portfolio would have suffered many more times than your large cap portfolio.

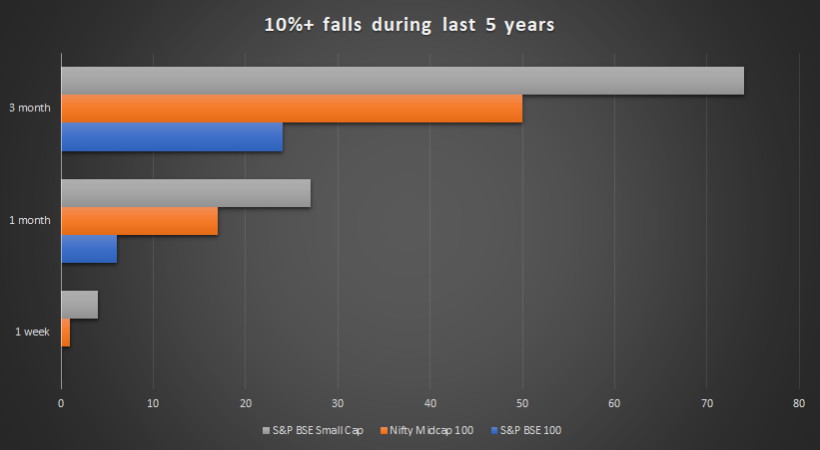

This does not however, mean that small caps give poorer returns. Over the last 5 years, BSE Small cap index has given annualised returns of close to 25%. This despite having experienced a 10% monthly fall on 27 occasions. In the same time, BSE 100 index has given returns of 15.4% per year, having experienced monthly falls of 10% or more on six occasions. And this demonstrates how volatility can be your friend if you are willing to take the pain.

So what does volatility do to you? It gives an impression that you have lost money by investing. The fact that it is a temporary fall and will bounce back does not seem logical in a state of panic. Hence, volatility triggers action on your side. And the action is often detrimental to your investments. How can you keep this action under check? Read on.

Learn how to manage volatility

Volatility is a given but there are some simple tools to manage volatility.

- The first is the humble SIP. Markets act randomly in the short term. SIPs help you walk in this randomness by ensuring you convert every volatile opportunity into a benefit.

- The second is having an asset allocated approach to investing. This means having some investments in low risk debt funds. This helps in two ways: one, debt provides some hedge against equity market volatility. Two, when you equity market falls and offers opportunities to invest more, money can be quickly moved from debt to equity.

- Third, an annual review and rebalancing will ensure your portfolio continues to match your risk appetite. This can be done by bringing down equity allocation if it has gone above your original allocation. This will automatically reduce risk. It also fulfills one of your needs to book profits in an asset class which has gained more. By booking profits this way, you can shift to a cheaper asset class (say, moving from equity to debt) without having to time the markets.

None of the above will stop the pain of volatility. It will only reduce the impact and ensure your investments bounce back faster. If you go through this cycle entirely once, you will know that markets will eventually revert to the mean, i.e., they will recover and your profits will be closer to the long term average. And when this happens, your annualised returns will still be higher than your bank FDs. All you need to do is give it time, wait for the volatility to play out and ignore the temporary fall in value of your investments if you are to reap the rewards.

Understand your risk appetite

This is also why it is important for you to be honest with yourself. When you invest in equity, close your eyes and imagine your dashboard showing a loss of 20%. How does it make you feel? If this is too much for you, then refrain from investing too much in high-risk assets. Diversify your equity portfolio.

A combination of 70% large cap and 30% small cap would have experienced a 10% monthly fall only 8 times over the past 5 years (much lower than small-cap’s 27), while still giving you an annualised return of 18.25%. At this rate, your money almost doubles in 4 years.

You don’t need to aim for the fund that gives the highest returns. You need to aim for an asset-allocated portfolio whose risk profile matches your risk appetite. This will ensure that you do not panic in times of volatility and reap the rewards of an asset class with superior returns.

Can we do SIP in multi cap + small cap for a period of 10 years for wealth creation. Is Franklin Smaller Cap fund a good idea to start fresh SIP now.

or ELSS + MultiCap is a better option

Hello,

You can run SIPs in multicap and smallcap funds if your horizon is 10 years. You will however need to ensure that the amount you have in smallcap is not high or a majority of your investment. You also need to include moderate risk funds in your portfolio. Aggressive multicap funds together with smallcap funds is too aggressive even if you’re a high risk investor. This moderate risk can come from large-cap funds or multicap funds which are not aggressive in taking mid-cap and small-cap exposure. Multicap + smallcap should not be the only combination you have in your portfolio. The call on what proportion to hold in smallcap or whether you need to hold small cap funds at all depends on your risk appetite. ELSS funds are multicap in nature.

Thanks,

Bhavana

Can we do SIP in multi cap + small cap for a period of 10 years for wealth creation. Is Franklin Smaller Cap fund a good idea to start fresh SIP now.

or ELSS + MultiCap is a better option

Hello,

You can run SIPs in multicap and smallcap funds if your horizon is 10 years. You will however need to ensure that the amount you have in smallcap is not high or a majority of your investment. You also need to include moderate risk funds in your portfolio. Aggressive multicap funds together with smallcap funds is too aggressive even if you’re a high risk investor. This moderate risk can come from large-cap funds or multicap funds which are not aggressive in taking mid-cap and small-cap exposure. Multicap + smallcap should not be the only combination you have in your portfolio. The call on what proportion to hold in smallcap or whether you need to hold small cap funds at all depends on your risk appetite. ELSS funds are multicap in nature.

Thanks,

Bhavana