Mutual Funds: Invest In Best Mutual Funds Online In India

Mutual funds help you invest wisely, grow wealth, and plan long-term goals. Explore Indian mutual fund websites to start your online investment journey today.

Start Your Investment Journey Today

What are Mutual Funds?

Mutual funds are pooled investments in which multiple investors contribute funds to invest in a professionally managed portfolio of stocks, debt instruments, or other securities, without needing to track markets full-time by yourself. These investments are handled or managed by professional managers known as mutual fund managers.

At FundsIndia, mutual fund investing goes beyond just “buying a fund.” We help you discover the right funds for your goals, risk profile, and investment horizon through research-backed recommendations, curated fund selections, and expert guidance.

From beginners to seasoned investors, FundsIndia makes your investing experience simpler and easier.

What are the Advantages of Investing in Mutual Funds?

Beyond the risks associated with market fluctuations, investing in mutual funds offers investors several advantages for building wealth with minimal hassle.

Diversification

Investors spread their investments across different funds, so underperformance in one, two, or a few funds does not affect the overall portfolio.

Professional Management

Skilled fund managers oversee the markets and make informed decisions, highly suitable for those lacking time and/or skills.

Liquidity

They offer easy redemption within 1 to 3 days, compared with fixed deposits and other stock investments.

Affordability

Mutual fund investments can be started with small amounts through SIPs, which facilitate disciplined investing.

Transparency

Daily NAV (Net Asset Value) announcements and disclosures are crucial in fostering trust.

Flexibility

Invest through SIP (Systematic Investment Plan), STP (Systematic Transfer Plan), and SWP (Systematic Withdrawal Plan); Easy switching between funds, Top-up SIPs, and more.

Tax Benefits

Equity-oriented mutual funds held for more than one year qualify for long-term capital gains (LTCG) taxation, where gains above ₹1.25 lakh in a financial year are taxed at 12.5%. Additionally, investments in ELSS funds may qualify for deductions under Section 80C (up to the applicable limit under the old tax regime).

These advantages make mutual funds outperform savings accounts and other bank deposits. Historically, equity fund returns have averaged 12–15%* annually, beating inflation.

*Past performance of the mutual funds and schemes is neither an indicator nor a guarantee of future performance and may not be considered the basis for future investment decisions.

How to Invest in Mutual Funds

Investing in mutual funds is simple and secure through the FundsIndia platform, your trusted SEBI-registered partner. You can manage all your investments digitally, backed by expert guidance and research.

How to Invest in Mutual Funds

Investing in mutual funds is simple and secure through the FundsIndia platform, your trusted SEBI-registered partner. You can manage all your investments digitally, backed by expert guidance and research.

Start investing in mutual funds

Start your investing journey with us.

Log in to FundsIndia

Create your investment account with FundsIndia. Log in to your FundsIndia App or Website to access your portfolio.

Choose the right fund

Explore a diverse range of mutual funds, including our fund recommendations. You can also connect with your dedicated mutual fund wealth manager for personalized investment guidance.

Start Investing

Once you have chosen the right fund for your goal, start investing using any method that suits you.

Pick Your Method

Choose how you want to invest your money.

Systematic Investment Plan

Invest fixed amounts on a monthly basis, for instance, ₹1000 and more, utilising rupee cost averaging to buy more units when the market valuations go down.

Lump Sum

This approach involves committing a one-time capital amount, which may offer superior growth opportunities during periods of upward market momentum.

Systematic Transfer Plan (STP)

Systematically move a fixed amount from one fund (e.g., debt) to another (e.g., equity) at set intervals. This strategy mitigates market timing risk and facilitates rupee-cost averaging on a lump sum.

Systematic Withdrawal Plan (SWP)

Receive a fixed amount or percentage from your total investment corpus periodically (monthly/quarterly). An ideal way to generate regular post-retirement income while allowing the rest of your corpus to continue growing.

Requirements for Investing in Mutual Funds

Finish these one-time steps and you are ready.

KYC Completion

Complete your KYC verification using PAN and Aadhaar to enable seamless mutual fund investing.

Active Bank Account

A valid bank account is required for SIP registrations, lump sum investments, and redemption payouts.

Activated FundsIndia Account

Open and activate your FundsIndia investment account to access mutual funds, SIPs, portfolio tracking, and expert guidance.

Steps to start investing in mutual funds

Log in to FundsIndia

Create your investment account with FundsIndia. Log in to your FundsIndia App or Website to access your portfolio.

Choose the right fund

Explore a diverse range of mutual funds, including our fund recommendations. You can also connect with your dedicated mutual fund wealth manager for personalized investment guidance.

Start Investing

Once you have chosen the right fund for your goal, start investing using any method that suits you.

Methods of Mutual Fund Investments

Systematic Investment Plan

Invest fixed amounts on a monthly basis, for instance, ₹1000 and more, utilising rupee cost averaging to buy more units when the market valuations go down.

Lump Sum

This approach involves committing a one-time capital amount, which may offer superior growth opportunities during periods of upward market momentum.

Systematic Transfer Plan (STP)

Systematically move a fixed amount from one fund (e.g., debt) to another (e.g., equity) at set intervals. This strategy mitigates market timing risk and facilitates rupee-cost averaging on a lump sum.

Systematic Withdrawal Plan (SWP)

Receive a fixed amount or percentage from your total investment corpus periodically (monthly/quarterly). An ideal way to generate regular post-retirement income while allowing the rest of your corpus to continue growing.

Requirements for Investing in Mutual Funds

KYC Completion

Complete your KYC verification using PAN and Aadhaar to enable seamless mutual fund investing.

Active Bank Account

A valid bank account is required for SIP registrations, lump sum investments, and redemption payouts.

Activated FundsIndia Account

Open and activate your FundsIndia investment account to access mutual funds, SIPs, portfolio tracking, and expert guidance.

At FundsIndia, we help simplify the entire process and guide you in building your portfolio curated for your goals.

FundsIndia’s approach to mutual fund investing

At FundsIndia, we help you invest with your life goals in mind through research-backed fund recommendations and expert wealth guidance tailored to your financial journey.

User-Friendly Platform

Access a super-intuitive dashboard, one-tap SIPs, seamless transaction management, and quick report generation.

Goal Focused

Whether short-term or long-term goals, guidance and portfolio tracking are right inside your app.

Expert Research & Tools

Access to our research reports, strategies and fund recommendations.

Unmatched Fund Choices

5,000+ schemes across 40+ AMCs available, ready to invest.

Secure & 100% Digital

Quick KYC, Paperless transactions and quick fund switches and redemptions.

Informed Decision Making

Access blogs, calculators, and webinars to invest with confidence.

Proactive Goal Monitoring

Ongoing portfolio reviews, rebalancing alerts via email/app, backed by your dedicated wealth managers.

Start your goal-based investment journey with us today.

Types of Mutual Funds

Mutual funds in India are categorised by asset class, risk, and structure. Here's a breakdown:

Equity Funds

15–20%- Description

Invest 65%+ in stocks. Sub-types: Large-Cap (stable giants like Reliance), Mid/Small-Cap (growth-oriented), Multi-Cap (diversified).

- Risk Level

- High

- Ideal For

Long-term growth-oriented investors (7+ years)

Debt Funds

6–8%- Description

Focus on bonds, G-Secs, and corporate debt. Sub-types: Liquid (short-term), Corporate Bond (medium), Gilt (govt. securities).

- Risk Level

- Low–Medium

- Ideal For

Short-term money-parking investors looking for stability.

Hybrid Funds

10–14%- Description

Mix equity (35–65%) and debt. Sub-types: Aggressive (equity-heavy), Conservative (debt-heavy), Balanced Advantage (dynamic allocation).

- Risk Level

- Medium

- Ideal For

Moderate risk-takers

Solution-Oriented Funds

12–16%- Description

Goal-specific, like Children's (locked 5 years) or Retirement (long lock-in).

- Risk Level

- Medium–High

- Ideal For

Milestone-planning investors.

Index / ETFs

13–18%- Description

Track indices like Nifty 50. Low-cost, passive.

- Risk Level

- Varies with index

- Ideal For

Cost-conscious investors

ELSS (Tax-Saving)

12–15%- Description

Equity funds with a 3-year lock-in are eligible for 80C deductions.

- Risk Level

- High

- Ideal For

Tax optimisation + growth-oriented investors.

Fund of Funds (FoFs)

8–12%- Description

Invest in other mutual funds, often international.

- Risk Level

- Medium

- Ideal For

Global diversification

Equity funds

Equity funds may suit long-term growth goals

Debt funds

Debt funds may suit stability and liquidity needs

Hybrid funds

Hybrid funds may suit investors looking for balanced exposure

ELSS funds

ELSS funds may help combine tax-saving with investing discipline

At FundsIndia, investors can explore expert-curated FI Select Funds, compare fund categories, invest via SIP or lump sum, and receive portfolio review and rebalancing support, all in one place, helping them build a more disciplined and goal-aligned investment journey.

*Past performance of the mutual funds and schemes is neither an indicator nor a guarantee of future performance and may not be considered the basis for future investment decisions.

What Our Customers Say

Real feedback from real people building real wealth

Frequently Asked Questions

What are the different types of mutual funds, and how are they different?

They are of various types: equity, hybrid, debt, index/ETFs, and ELSS. These funds differ in their asset allocation, the risk involved, and their investment objectives. In general, equity funds are growth-oriented and carry higher levels of risk, whereas debt funds aim for safety with minimal risk.

How do I choose the right mutual fund for my goals?

Choosing the right mutual fund depends on your financial goals, investment horizon, and risk appetite. At FundsIndia, you can also connect with your dedicated Wealth Manager / Advisor for personalised guidance on selecting suitable funds and building a goal-aligned investment portfolio.

What are the tax implications of investment in mutual funds?

Equity: LTCG > ₹1.25 lakh at 12.5% (1+ year); STCG at 20%. Debt: LTCG at 12.5% without indexation (>2 years); STCG as per slab. Dividends are taxable at slab rates. ELSS offers 80C benefits.

How much should I invest in a mutual fund?

Start SIP with ₹1000–₹5,000/month. Try to allocate 20–30% of your income towards MFs in a diversified manner. Step-up SIPs can be utilised to achieve goals such as building a ₹1 crore corpus with a 10–20% annual increase.

Is it possible to invest in several mutual funds at one go?

A focused mutual fund portfolio can be smarter than owning too many schemes. For many investors, 4–6 well-chosen funds may provide diversification while staying easy to manage. Too many funds can create overlap and reduce portfolio efficiency.

How do I calculate a mutual fund's returns?

Through Absolute Return = ((Final NAV − Initial NAV) / Initial NAV) × 100. XIRR is used to calculate the yield on SIPs, which is the annualised value. For example, the value invested is ₹10,000 invested every month. However, you need to ensure that futuristic return calculations are subject to market fluctuations.

What is the role of a fund manager in mutual funds?

Fund managers in mutual funds expertly select securities, manage portfolios, and adapt to market/economic changes. Their goal is to outperform benchmarks while providing investors with professional oversight and strong returns.

What are the risks involved in mutual funds?

Market risk (market volatility); credit risk (debt defaults); liquidity risk; and interest rate risk. While not completely inevitable, these risks can be mitigated through diversification, long investment horizons, and SIPs.

Can I redeem my mutual fund units at any time?

Yes, most open-ended mutual funds can be redeemed on business days, with T+1 / T+3 days, subject to scheme terms. Payout timelines vary by category. ELSS comes with a 3-year lock-in, while closed-ended funds follow maturity timelines. Exit load depends on the specific scheme and holding period.

What is the minimum investment to start a mutual fund?

Many SIPs start from ₹1000, while lump sum investments commonly begin from ₹1,000 to ₹5,000, depending on the fund selected and platform availability.

Does FundsIndia offer mutual fund recommendations?

Yes. FundsIndia offers research-backed mutual fund recommendations curated by our investment research team. You can explore ‘FI Select Funds’ section and filter further with the category type you are interested in.

What mutual fund research and insights does FundsIndia provide?

FundsIndia provides a range of research-backed investment insights and frameworks based on market conditions and investor goals. Some of the popular research offerings include:

1. FI Select Funds

2. SIP Conversation Frameworks

3. Wealth Conversation Frameworks

What are some popular mutual fund investment strategies?

Different investors follow different strategies based on goals and market conditions. Some popular strategies offered and discussed at FundsIndia include:

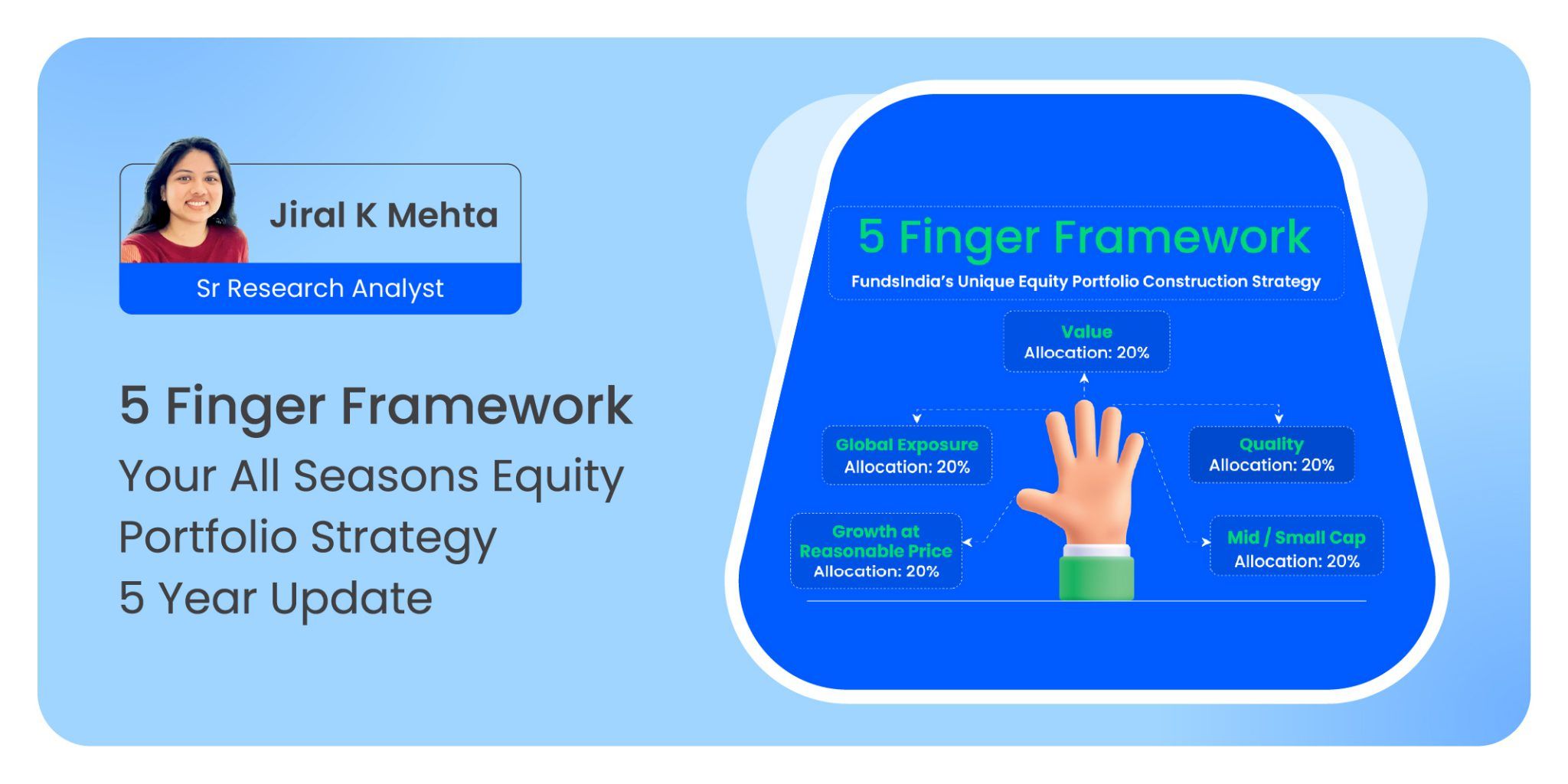

1. Five Finger Strategy

2. 7-5-3-1 Strategy

3. Power STP Strategy

4. SIP Step-Up Strategy

5. Goal-Based Asset Allocation

These strategies are designed to help investors build disciplined and structured portfolios.

Does FundsIndia offer SIP mandate registration?

Yes. FundsIndia supports SIP mandate registration for seamless and automated SIP investments directly from your bank account.

How do I contact my FundsIndia Wealth Manager or Advisor?

Login to your FundsIndia account and click on the “Let’s Talk” option available within the platform to instantly call or message your Wealth Manager.

How do I create multiple portfolios in the FundsIndia app?

Login to your FundsIndia App or website → View Portfolio → Create New Portfolio. You can create separate portfolios for different goals such as:

1. Retirement

2. Child Education

3. House Purchase

4. Emergency Corpus

This helps investors track goals more efficiently.

Insights & Research

We believe wealth is built on trust, clarity, and long-term thinkingWe believe wealth is built on trust, clarity, and long-term thinking. Our core values

ensure that every recommendation, every tool, and every decisions.