If the above headline does not convince you, this article has enough numbers to clear your doubt.

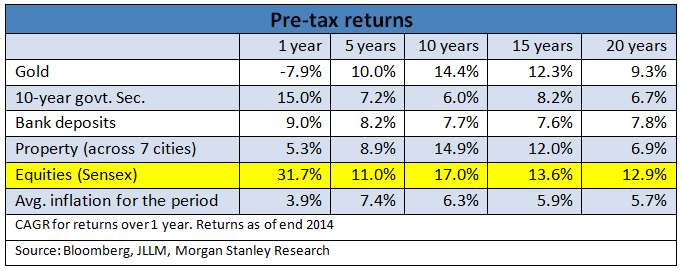

The table below is an extract of a recent report by Morgan Stanley named ‘Cross Asset Returns’. We are highlighting this not so much to showcase equity performance – it is likely that most of you will know how equities performed; but more to let you know how other asset classes do not perform.

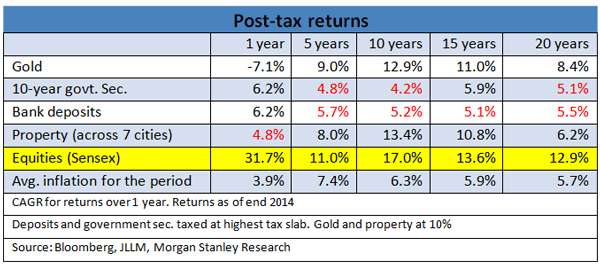

As the charts below show, the performance picture of post-tax returns becomes clear. Bank deposits, for instance, do not beat inflation over 5, 10,15 and 20-year time frames. Government securities somewhat break even over a 15-year time frame but fail otherwise.

Can you imagine building your long-term portfolio for your children’s education or for your own retirement with your favourite recurring deposit or some government bond? You would likely erode the value of your money. In other words, you will have ‘invisible’ capital erosion.

Property’s performance (above) may come as a surprise to you. The 7 cities talked of here are Mumbai, Delhi, Bangalore, Kolkata, Hyderabad, Pune and Chennai and the data is from a large property consultant. Are you surprised? Yes, property did yield a pre-tax 14.9 per cent annualised over the last 10 years. Sounds too less? That means your money grew 4 times. Sounds better?

But yes, equities did much better. Just that we are so not used to hearing equity returns in terms of doubling or trebling. Always the lame-sounding annualised return!

True, gold did come a close second to equities, just that its negative returns in the last 2 consecutive years made it lose sheen. Besides, how much can you forecast in an asset class than has no underlying fundamentals, save for the great Indian household demand? And yet, all the Indian ‘golden’ appetite put together could not pull its returns to overtake that of equity!

And, therefore folks, equity remains king. The reason is simple: the other asset classes either do not have any fundamentals (gold), or remain overcast with speculative activities (property) to be able to discover their true price.

And then, there are fixed-return asset classes that can deliver only fixed returns. The bank or the government which borrows from you benefits from volatility and passes the part that is least volatile to you. You may say you pay a price for certainty; or the surety of fixed returns. But your ‘real returns’ (post inflation) show you the real picture.

With equities, while the uncertainty of not having fixed returns causes it to swing in the short term, it is adequately compensated by returns (from tangible metrics such as cash flows of companies) over the long term.

Equities have strong underlying fundamentals; true they allow for some speculation in the short term; but such activity ultimately helps discover better long-term pricing/valuation. That, folks, is the beauty of equities especially in the long run.

Here’s how equity stacks up against other asset classes viewed qualitatively:

– No fixed returns but builds wealth (unlike fixed income instruments)

– Some speculative activity, but backed by an organised stock market system that corrects it and provides liquidity at all times (unlike property)

– Strong underlying fundamentals that reflect in long-term performance (unlike gold)

But how do you combat the volatility in equities? Simple: stop looking at your portfolio too often. By closing doors to your emotion, you will fully succeed in protecting your wealth.

It’s hard not to agree. But the last 20 years have been the best 20 years for Indian equity. Question is, if we take the last 100 years, is this true? What if the 20 years that are about to follow are not the best? I am sure some of us old enough to remember the 70s India are apprehensive of equity for that reason.

Hi, So what if the next 20 years do not yield returns like the last 20 years? You should view it relatively, the call is whether equity will still do better than gold and debt over the next 20 years and without doubt it will because the structure of the asset class is such. Debt returns are fixed and cannot be high, gold has no fundamentals and real estate in India has a long way to go before there is transparent information..and remember transparency reduces speculation and also curbs extraordinary returns.

If you missed the best years, it does not mean you will not invest. It is the question of which remains a relatively better choice for the next 10-20 years. regards, Vidya

Very nice flow. Same topic can be presented in 100 different ways, this is a nice read.

Very nice flow. Same topic can be presented in 100 different ways, this is a nice read.

It’s hard not to agree. But the last 20 years have been the best 20 years for Indian equity. Question is, if we take the last 100 years, is this true? What if the 20 years that are about to follow are not the best? I am sure some of us old enough to remember the 70s India are apprehensive of equity for that reason.

Hi, So what if the next 20 years do not yield returns like the last 20 years? You should view it relatively, the call is whether equity will still do better than gold and debt over the next 20 years and without doubt it will because the structure of the asset class is such. Debt returns are fixed and cannot be high, gold has no fundamentals and real estate in India has a long way to go before there is transparent information..and remember transparency reduces speculation and also curbs extraordinary returns.

If you missed the best years, it does not mean you will not invest. It is the question of which remains a relatively better choice for the next 10-20 years. regards, Vidya