If you expected Budget 2016 to put the Indian economy on a fast track growth path, you might be disappointed. The Union Budget has clearly prioritised fiscal prudence over aggressive growth targets. Moderate expenditure growth, with key investments in pressing areas such as agriculture, infrastructure, and employment generation, as well as providing for banking recapitalisation and the Seventh Pay Commission (partly) were finely balanced without compromising on the fiscal target of 3.5 per cent in FY-17.

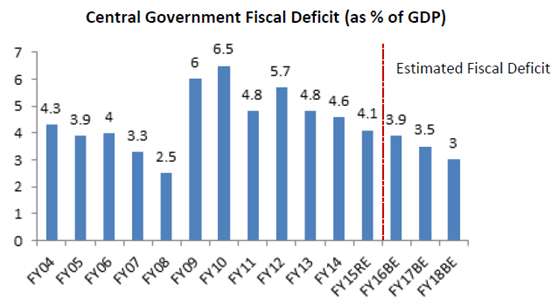

The table below indicates how far we have come in containing our deficit.

Why is fiscal prudence that important? We are already at a stage of low oil prices and a consequent fall in current account deficit, together with low inflation. That sets the path for lower interest rate, which is the need of the hour to boost corporate spending activity. Any extravagance, at this stage, could affect the sweet spot in inflation as well as deficit, thereby upsetting the case for lower rates. By sticking to fiscal targets, the government has provided the right signals for the Central Bank to act. It has achieved this by not entirely taking its foot off the pedal when it comes to key spending (infrastructure, rural development). It thus sets the tone for private spending by showing the way, but not indulging too much.

Also, it is noteworthy that the spending by the government, under these circumstances, is not piddly as it appears to be, if one merely looks at the 3.9 per cent increase in capital expenditure by the government. Experts from research firms such as CRISIL look at what is termed as Productive Expenditure – that is the sum of capital expenditure and a part of revenue expenditure that is used to create capital assets in the economy. Such productive spending as a share of the GDP is mildly up at 2.75 per cent of FY-17, as against 2.73 per cent in FY-16, according to reports. Also, it is noteworthy that the subsidy bill of the government is down, although it had to provide for pay commission and pension payouts. That means money is going into productive spending in the economy.

What’s in it for the markets?

Equity: Simply put, the stock markets pretty much get nothing. You can only lead a horse to the water, but the Government has shown the way. Companies have to pretty much take cues from government spending, take advantage of low oil and commodity prices, as well as make the best of heavy rural spending by the government and pick themselves up. While there are no major positives for Corporate India as a whole, there are pockets of benefits that companies can make the best of. We highlight some of them here:

– In the auto space, while taxes at the consumption end in the form of infrastructure cess, and tax collection at source for cars over Rs. 10 lakh can impact 4-wheeler sales, the large rural outlay, as well as key measures such as opening up the road transport sector in the passenger vehicle space (amendment to Motor Vehicles Act) can provide a fillip to 2-wheeler, tractor as well as commercial vehicle sales. Hence, we would view this as a positive for this sector.

– Even as rural consumption has been slackening over the past year, increased rural spending by way of Mahatma Gandhi National Rural Employment Guarantee Act (MNREGA) can provide some support to sales of consumer goods (FMCG).

– While the general thought has been that the banking recapitalisation amount of Rs. 25,000 crore is inadequate, we believe this space has to be seen from the point of structural changes being ushered in. A Bank Board Bureau to improve the governance of public sectors banks and providing a road map for their consolidation is a key development. Also empowering Asset Reconstruction Companies by way of amendment to respective laws and strengthening debt recovery tribunals are also positives, when viewed from a long-term perspective.

– The biggest positive, of course, comes from the massive outlay of Rs. 2.21 lakh crore for infrastructure, out of which Rs. 55,000 crore is budgeted for roads (with additional Rs. 15,000 crore to be raised through NHAI bonds). This clearly is a boost for companies in construction, as well as allied engineering and capital goods companies. Besides, a Resolution Disputes Bill for PPP (Public Private Partnership) projects and new guidelines to renegotiate agreements will be issued. This can provide a fresh lease of life to stalled/stressed projects.

Your equity portfolio: A good number of mutual funds have been taking measured exposure to cyclical sectors such as construction and automobile, and can benefit from the above positives. We still believe that funds that took contrarian views to go overweight on the banking sector could benefit the most as a combination of low valuations of many stocks in this space, together with a rate cut event, could trigger the prices of these stocks. Near term pain of fast tracking NPAs in their books has only ensured cleaning up of books sooner to make way for growth.

If you wish to average your equity portfolios, you have no more uncertainties. Start now.

Debt: Fiscal prudence by sticking to the deficit target received a big thumbs-up in the debt market as yields fell, causing bond prices to rally. This could signal that markets are readying themselves for a rate cut. A number of measures to deepen the corporate bond market, including allowing FPIs to invest in unlisted securities, and allowing large borrowers to tap market than go to banks could also mean that the debt market’s demand-supply scenario improves, thus reducing price volatility.

Your debt portfolio: Depending on how the RBI interprets the fiscal situation, as well as inflation, and a rate cut may trigger a rally. Hence, while a duration-driven rally may happen, we believe a steady unravelling corporate growth story and improving credit situation would be a more dependable story, and therefore, income accrual funds could be good bets for the long term.

A combination of duration and income accrual funds is, therefore, the way forward for a 2-3 year debt portfolio.

What’s with the way you invest?

This Budget discussion would not be complete without a mention on why your investments in products such as mutual funds gain more importance now than ever.

If you are already heavily into investing in market-linked instruments such as mutual funds, you may not be too worried by this. But for those largely depending on EPFs for their life savings, the proposal of partial taxation of your EPF may have sounded like a death knell. (Click here to read our blog post for our latest position on this) While we await clarity on the exact taxation (other than the fact that 40 per cent of the lump sum withdrawn would not be taxed) on EPF, we would urge you to take the spate of signals from the Government and the tax authorities on this. (Click here to read our blog post for our latest position on how the Budget impacts your taxes)

One, provident fund rates have declined from double digit rates in the 1990s, and are now, mostly in the range of 8-9 percent. Two, more recently, the rates on these small savings schemes (as well as many other such schemes) have been made more dynamic, with change in interest rates every quarter pegged closely to the gilt rates. That means they will hardly remain fixed in a given year, and can fall in line with rate falls. Three, in the latest budget, to provide parity between NPS and EPF, EPF is also proposed to be taxed partly.

All these hint at just one message: move to market-linked products. Of course, while the EPF-NPS transition may happen once companies provide the option, for you as an investor, it is important to also look beyond these options into more efficient market-linked options such as mutual funds to deliver tax efficient, superior returns.

For instance, in the same tax domain, an ELSS fund can be effectively used to save tax, with no capital gains tax, thereby helping you build a far superior retirement kitty that can be later moved to safer avenues, closer to retirement. The government is favouring savings in market-linked instruments. While you do that, make sure you pick efficient and superior wealth-building market-linked products.

Talk to your advisor if you wish to know how best you can save outside of the traditional provident fund options to ensure you are left with more money on the table.