“Should I go for growth option or take out the dividends in my fund?” – is a question frequently asked by many of you, when venturing into mutual fund investments. Before we move on to discussing what suits you best, let us get down to some brass tacks.

The difference

The growth option simply implies that the profits you make stay reinvested. In other words, the profits, along with your capital, are invested in stocks/debt to earn you more money.

Dividend payout implies that a part of such profits (an amount that the fund decides to give out) is stripped from your NAV and given to you. That means, a part of the fund’s profits are given in cash. Hence, your NAV falls to the extent of dividends. This is why the NAV of growth and dividend option are not the same.

In dividend reinvestment option too, profits are stripped. But instead of giving them as cash, they are allotted to you as units at the prevailing NAV. Hence, indirectly, by adding more units, you simply stay invested in the fund. Conceptually, the dividend reinvestment option is the same as growth option for all equity funds.

Two key factors will determine what is appropriate option is for you:

1. Cash requirement and time frame

2. Tax efficiency

Most people base their decisions on tax efficiency. While it is a key deciding criteria, let us also look at how other factors too, will play a role in choosing between dividend and growth.

Equity funds

Let’s take on the easy one first. Equity funds are meant for the long term. Your reason for choosing an equity fund must be to build wealth towards some goal which is perhaps at least few years away.

That simply means you should stay invested in the fund and not take the cash out (unless you will invest the dividends back diligently) to help compounding work for you. Since, long-term capital gains are free of tax, the solution here is simple: As a general principle, go for growth or dividend reinvestment in equity funds.

But there are exceptions: One, in case of theme funds or sector funds that you hold tactically, it makes sense to either opt for dividend payouts or book profits as the fortunes of themes can take a turn after one good cycle. Two, in case of ELSS, avoid dividend reinvestment as every reinvested unit will be subject to a three-year lock in. Prefer growth, Three, if you are generally risk averse and prefer to take your money out to invest in some debt option, then you should consider payouts or set triggers to book profits.

This category gets a bit tricky because the dividend suffers dividend distribution tax (DDT). DDT is nothing but the tax on the dividend paid out in debt and debt-oriented funds and gold funds. DDT is not applicable for equity funds.

Let us suppose a fund declares Rs 10 as dividend. A DDT of 28.33% ( 25% plus surcharge of 10% plus cess of 3% from June 1) is Rs 2.833. Now while you will get Rs 10 in your hands, Rs 2.833 will be further reduced from your NAV (your NAV after dividend will be – pre-dividend NAV minus dividend minus DDT).

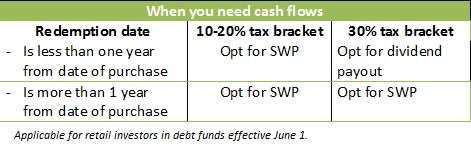

Now, to know the tax implication Let us split your universe into two based on your cash needs:

1. You need some cash flows from your debt fund: In this case, you can choose the dividend payout or the systematic withdrawal plan (SWP) under growth option. Look at the table below. The SWP is a clear winner for those in the 10% and 20% tax brackets. But please ensure that you do not end up paying exit load. Opt for SWP post the exit load period if you wish to avoid the load.

Those in the 30% tax bracket, can go for dividend payout, if you intend to hold the fund for less than a year.

But you do not gain much by doing so, as DDT will increase to 25% for all debt funds (earlier only for liquid funds) effective June 1.

But if you can park your money for more than a year and have no immediate cash flow requirements, opt for growth right when you invest and do a SWP from the beginning of the second year.

Remember, switching between options will also unnecessarily entail capital gains tax if you have profits. Hence, get your investment time frame right when you start your investment.

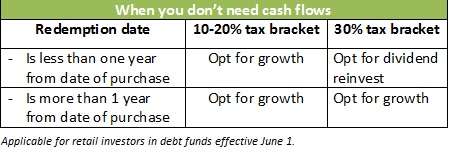

2. You don’t need cash flows from your debt fund: In this case, you have 2 options – to go for growth or dividend reinvestment. Look at the table below. Growth option scores in most cases, except when you are in the 30% tax bracket and redeem in less than a year.

When you are in the 30% tax bracket and hold for less than a year (will be the case with most of your liquid or ultra short-term funds) you will suffer DDT of 28.33% (including surcharge and cess effective June 1) on the dividend reinvested.

This will be slightly lower than the income tax slab of 30.9% (including cess).

Consider your fresh investments through the above routes. But if you make your switches now, do take into account the exit load(will vary for each fund) and the capital gains, if any, you may suffer on the fund now, especially if your holding period is less than a year and you do not have a long time frame for the investment from here on.

Hi Vidya,

[Quoting Vidya]

Two, in case of ELSS, avoid dividend reinvestment as every reinvested unit will be subject to a three-year lock in. Prefer growth,

[End of Quote]

Pls correct me if I am wrong.

1)In the case of ELSS, usually, a dividend is declared at least, every year.

2) The dividend reinvested, in turn will get a dividend, which in turn will get locked in for a period of 3 years & so on.

To conclude, rarely is it possible to encash the total dividend out in to our account in ELSS Dividend reinvestment option.

Hope, I have been able to put across my perception properly.

Thanks

Yes Shishir. True. To get out of this vicious cycle, most fund houses allow you to switch from a dividend reinvestment option to a dividend option by giving a request letter or change option slip. This can be done even during the lock-in period.

A switch to the growth option is also possible but only after lock-in period.

Thanks Vidya

Hi,

I am a live example of the same. Since I invested in the ICICI Pru Tax Plan Dividend Re-invest option I am not able to take out my complete funds even after wait of 7 years since it keeps on reinvesting and start a new Lock-in for the new units purchased under the re-investment.

Ankush, you simply have to switch to the dividend payout immediately. In fact, even during your initial lock-in period you are allowed to do this. tks, Vidya

If I do a switch from dividend re-investment to dividend payout, will the 3 year locking period start again from the date of the switch?

Sreedhar, good question. if you are talking about ELSS, then such switch is allowed without affecting the lock-in. thanks, Vidya

for regular monthly investment schemes, which option is to be choosen whether dividend reinvestment or growth, which option will be good, please reply, thanks

Is it possible to switch from Dividend reinvestment option to Growth .

Yes you can switch. But it will be considered a sale and purchase for tax purpose. Hence capital gains tax, if any (unlikely or very low in dividend), will be applicable. thanks, Vidya

I have started investing in ELSS Div-Reinvest schemes since 2015. But both my fund houses has converted them to div-payout. Seems reinv do not apply to ELSS schemes any more. This thread is quite old.

These are great points, and I think by default – people should opt for the growth option, and then they should have a really good reason to choose the dividend option. This way they will ensure that they take the right decision most of the time.

Hi Manshu, you’re right. Just that some people in the 30% bracket may still want to utilise the thin difference that exists in dividend option (over growth) for less than one year. In absolute terms, it will matter when the amount invested in large, although yield difference will seem marginal. Tks Vidya

Great post as usual Vidya.

So how does one decide between daily dividend Vs weekly dividend Vs monthly dividend. Or perhaps that doesn’t matter because dividends will be reinvested?

Scenario: Investing some lumpsum amount in a liquid fund for next 3-6 months. 30% tax bracket.

Hi Apoorv, Thank you. Very interesting question. Typically, its the liquid and ultra-short-term funds that have a maze of options – daily, weekly, monthly and so on. For the other debt categories it is mostly, monthly, quarterly and so on. We shall therefore restrict our discussion to liquid funds and ultra short term.

Before answering your question, let us step back a bit to understand why funds created these many options. Answer: they had only the institutional investors in mind; because even a few years ago, this was the class of investors that liquid funds were mostly catering to.

Large companies find liquid funds to be great parking grounds for their working capital money, for 2 reasons: one, bank fixed deposits had and still have a min. of 7 day tenure. Liquid funds can be parked even for a day. Two, since corporates deal with crores of money, even a day’s return matters for their treasury.Parking all the money in their cash credit account (called CC in corporate terms, these accounts are meant to overdraw) would earn zero return. But then, corporates did not want to pay high capital gains either.

It therefore helped them to take out as much as possible as dividends even if they stayed for 2-3 days (it is separate story that corporates used this to even book short-term capital losses using what was called dividend stripping strategy. that loophole was later plugged. But we will keep that for another day). Since, they are uncertain as to when they need the money, it helped them to have dividends as frequently as possible to keep their NAV value at bay. So opting for a monthly dividend may not suit them if they were to suddenly exit..and bear short-term capital gains tax. Note that their marginal rate of tax is higher than ours as they do not have slab rates like us.

And hence the options, that you see today cropped up to cater to them.

All liquid options give almost the entire gains back as dividends/units under the dividend option. Hence, the chances of a short-term capital gain is rather low in dividend option. For a retail investor, if the investment value is in crores and there is uncertainty over when he/she will need that amount, it makes sense to go for a daily or at best weekly reinvestment option for the sake of taxes. If you have a reasonable idea of when you will need your money and you can plan accordingly, then you can simply be neutral to this under a reinvestment option. The quantum reinvested is either small or high. In a weekly option, the money stays longer (and note that it earns returns every single day) before it is stripped and reinvested, whereas in a daily option, it is stripped quickly and reinvested.

That was a long story 🙂

Tks, Vidya

Thanks Vidya, that was a superb explanation.

Hello Vidya,

Thanks for the superb explanation.

I did a whole bunch of STP’s from liquid funds to equity funds over the last 3 weeks, and my initial investments have all been daily dividend reinvestments. I just thought that 1×7 == 7×1 and decided to take the daily route, almost arbitrarily.

Now I see the difference. Maybe I need to restructure my STPs now. Pain in the ass.

-T

Dear Vidya,

Very nice article. As Manshu says the growth option should serve most people by default. The article reminds of an issue reg. a STP. Most people ignore STCG while setting up the STP.

If I choose the dividend (or div reinvestment) option in the source debt fund and if I ensure transfer frequency is not less than the dividend frequency could I assume for all practical purposes zero STCG (or LTCG)?

Even then I find this a hassle. I see no need for a source debt fund. A simple transfer from a SB account should do for every case I can think of. Returns from the debt fund over a few months will not make much of a difference.

Hello Pattu,

Welcome! You are right that people often ignore the STCG implications.

If the source fund is a liquid fund, the entire accrual is typically paid out. Hence chances of STCG should be nil, if your STPs are accordingly planned.But I cannot say that with certainty for an ultra short-term fund. While most of them seek to pay out, given that they can have a higher proportion of MTM securities (as they can invest in slightly longer instruments), chances are that they may not always have accrual income to distribute.Some money may be left without distribution.

In all other debt funds, there is no way to ensure this.

STPs make sense when investors have a huge lump sum and are tempted to invest it right away as a bulk in the markets, instead of the money lying in the savings account. To prevent any ill-timing of markets and get a few extra bucks (and again only when you get a large sum say a jack pot or a say some robust inheritance money:-) ) over and above savings bank rates, STPs can be a good idea with liquid funds as the base. For a salary earner and somebody who is going to invest from his/her monthly savings, a regular SIP is good enough.

The less talked of part of an STP, is to use it to shift from equity to debt, especially when one needs to reduce equities holding in a phased manner closer to goals (like retirement). While not all funds may offer this as a feature directly, many platforms provide this for investors. This has more value. Tks, Vidya

Many thanks. That and your response to Apoorv is quite useful.

Vidya,

This is a very good set of information that you have thrown out there! Thanks for sharing and making investors aware of the options available and the situations that makes these options valuable !

– Thx again .

Ganesh

Hi Vidya,

This is related to Debt Funds which you have explained in this blog. Two key aspects to consider while choosing the funds are the period of redemption one year.

Some Debt Funds are coming with Five Year Lock In period say for example [DWS Hybrid Fixed Term Fund -Series 10 -Growth ], my questions are

1) In which scenarios these these funds/schemes with 3 year , 5 year lock in periods should be considered

2) Are the funds with the lock-in periods in any way better than the other schemes (say no lockin periods)

Thanks in advance.

Hi Karthick,

1. Typically longer tenures are preferred when interest rates have peaked and are set to fall. We are not necessarily in the peak. The descent has happened a while ago. Still, there is good scope for locking in to longer term FMPs for returns now. Caveat: FMPs are new offers. Nobody can vouch for their portfolio as they would not have built one at the time of NFO. It is therefore important to know the scope of portfolio and potential returns by looking into the offer document.

If the offer document, for example, says that the fund will invest quite a bit in say less than AAA rated instruments (say AA), then it is certainly going to give you that extra bit of returns for the addl. credit risk.

2. In case of FMPs the timing risk (interest rate risk) is much lower than an open ended fund. That s because the fund is simply going to invest in instruments that has the same tenure as the fund’s lock-in and wait for maturity. It will then provide the accrual income (interest income) from these instruments to you as gains.

Also, as they are close ended and face no redemption pressure from you, they are not forced to actively churn or manage their portfolio or constantly keep cash to pay investors. In other words, FMPs are less actively managed over the tenure, when comapred with an open-ended fund. On the flip side, that could also mean that they may not participate in some quick rally during such a period; on open-ended fund, on the other hand, will capitalise on the same.

FMPs are more comparable with bank deposits than open-ended debt mutual funds as the latter seeks to generate superior returns through active management.

Tks

Vidya

Hi Vidya,

That’s a very good explanation in simple terms.

Many Thanks

Karthick

Hi Vidya,

Great article, as always. I have one minor quibble though: your comparison of DDT vs. top marginal tax rate is somewhat misstated.

[quote]

..you will suffer DDT of 28.33% (including surcharge and cess effective June 1) on the dividend reinvested.

This will be slightly lower than the income tax slab of 30.9% (including cess).

[/quote]

A DDT 28.33% is equivalent to a tax rate of 22.08% which is significantly lower than the 30.9% figure. Think of it this way. I invest Rs. 100, fund manager grows it to Rs. 112.83 in, say, 6 months. If I am invested in dividend option, I get Rs. 10 which is tax free in my hands, GoI gets Rs. 2.83 as DDT and NAV goes back to Rs. 100. If i’m in growth option, and sell the unit, I realize Rs. 12.83 as STCG and have to pay Rs. 3.97 as tax as per my marginal tax rate and will be left with only Rs. 8.86.

None of this changes the thrust of your argument, but as I see it, dividend option in debt mutual funds is considerably more advantageous that woudl appear at first sight. The last budget has narrowed the gap by increasing DDT, but the difference persists. Unless my math is wrong, in which case I should be very much obliged if you would correct it 🙂

Hi Hari, There is no denying that for the short term the benefit of dividend still remains…we have only said it is now diminished than before. But I would disagree with this practice of calling 28.3% tax rate as 22% effectively.This is being used by quite a few planners. The yields do not work that way and here’s an example, I quoted in another blog for this purpose:

“This effective DDT used by planners is a theoretical calc. Look at it this way. Let us assume you have a liquid fund under dividend option. Currently DDT plus SC plus cess is 27.03%. Let us suppose you bought the fund at nav of rs 1000 and it has grown 8% to 1080. Now assume the fund declares rs 80 as dividend. That means Rs21.6 (27.03% of 80) will be deducted as DDT from the NAV. The NAV falls to 978.4 (1080-80-21.6). Now theoretically assume that you sell at this point or simply calculate your yield at this point. What is the money you totally get? it is 978.4+80=1058.4. Hence yield is 58.4/1000*100 =5.84%.

Now do your math by taking the gross return of 8% less effective DDT of 22% stated by you. what is the yield? it is 6.24%. Now this is incorrect because the actual returns post tax (as calculated above) is much lower.

Many a time, 22% is called the effective tax rate by planners. This is theoretical and does not tally, if you actually work the net returns in a simple, cash flow based manner. It is calculated by taking 2.83/12.83…why would you take the base as Rs 12.83 when 2.83 is in a way an expense incurred by you.

Let us face it….the increase in DDT has shrunk the net yield that we will get in hand. That is what matters at the end…number games not withstanding.”

Hi Vidya,

I love this blog. FundsIndia is doing a wonderful job in providing quality advice and that too for free. Many investors may not get it even from paid advisors.

However, with all due respect, I must say that you are wrong in effective DDT calculation above. I believe your calculations are more theoritical (or bad example, as I’ll show later). So, let me give you a very practical example:

Let’s say I invested Rs. 100,000 each in Reliance Liquidity Fund (G) [RLF-G] and Reliance Liquidity Fund (MD) [RLF-MD] for 1 month. Here are some values:

RLF-G NAV on 27-May-2013 – Rs. 1790.5819

RLF-MD NAV on 27-May-2013 – Rs. 1001.3742

Here’s what I get for my Rs. 100,000 each.

RLF-G – 55.8477 Units

RLF-MD – 99.8627 Units

Say I sell it on 25-Jun-2013

RLF-G NAV on 25-Jun-2013 – Rs. 1802.1037

RLF-MD NAV on 25-Jun-2013 – Rs. 1001.3717

RLF-MD Dividend of 5.02 Per Unit

Here’s what I get when I sell my units + Dividend in each case.

RLF-G – Rs. 100,643.34

RLF-MD – Rs. 99,999.68

RLF-MD Dividend – Rs. 501.31

My annualized return on RLF-G = 7.72%

My annualized return on RLF-MD = 6.01%

Effective DDT impact: (7.72 – 6.01) / 7.72 = 22.15%

Now, here’s why I called your example as A) Theoritical B) At best, a bad example

A) No fund house will go below it’s NAV just to declare dividend. If profit is Rs 80, it’ll give Rs. 62.4 as dividend and remaining will get reduced from NAV bringing it down to Rs. 1000.

B) Now this is possible in real world to have your example’s situation. Consider that I buy RLF-MD plan on 2-Jun-2013 and sell on 25-Jun-2013. Here, when I sell my units I incur a loss which is what you showed in your example. Now it is bad example since nobody should invest in MD plan anywhere in between the month and sell just after getting dividend. Because you incur a loss and with Dividend Stripping loophole caused, your effective yield is reduced.

Now, you can say I took an ideal example of buying right after one MD payout and selling right after 2nd payout, and this is not practical situation for liquid funds where you can’t plan for it. I am completely with you and hence another suggestion that you gave to an investor in another post that there is no difference in DD, WD, MD, QD plans as for dividend yield. The truth is DD is the best so that you don’t have to worry about buying and selling date. In other plans, if you don’t time the sale and purchase as per duration (like 7 days for WD, 28-31 days for MD, etc.) then you may incur either ST Capital loss (which is waste as you cannot offset it against any STCG) or have some portion of investment behaving as Growth and you make ST Capital gain and pay 30.9% tax on it.

I believe it was a very long post but it puts all such doubts at rest with a real world example.

Thanks!

Hello sir,

Thank you for visiting the blog and for your detailed post.Appreciate your effort.

I really don’t see what is the point of contention, as I agree DDT being paid from NAV etc. Only link I find missing in your calc is the capital gains of the growth scheme. When you are considering DDT on the dividend pay out option, you shouls consider post-tax returns on the growth option. And pl. view absolute returns as absolute. Do not annualise returns when investors did not have one. Yield calculations often lead to big nos. but do not solve the simply question of yeh kihna deti..in simple rupee terms. 🙂

As for taking theoretical examples, it is to make the learnign easier for readers. I hope you appreciate that one cannot sit in a transaction platform like ours without knowing the practicality of it 🙂 Tks.

Well I do not have any further comment. The point is, as I proved with practical example from market, that 22% effective tax in dividend option is the right way to calculate and compare. The example has all details, amount of return, % return, etc.

hello mahesh, I thought I also proved with an example (practical or not, egs. help calculate, as simple as that) that I am in disagreement with the ‘effective yield calculation used by many an advisor’ :-). Effective yield theory has to work when applied to actual cash flow and it did not in the 22% theory.

So we shall have to agree to disagree 🙂 Thanks, Vidya

Dividend reinvestment is much better than growth option. just compare the final values after 5 to years – reinvestment option stays high. by the way fixed deposits with bank give better return than MF. MFs are of no use . Fund managers do nothing . They do not trade regularly. They come to office shake hands with collegues , drink coffee, play video games and then go to club or home. if they would have been trading seriously , the mutual funds would have been giving more than 100% profit over the year. Why should the MFs move with the market ? the MFs should make profit by buying, holding and selling. All experts ( So called) suggest the small investers not to time the market than WHAT THESE SO CALLED FUND MANAGERS ARE FOR ? only to invest once and then let the market to take its toll ?

I am no expert ( Than these so called experts come a dozon per dime. at present no shortage of them ) but an inveater and looser too from lst 10 years. my advice go for bank FD for more than 5 years an feel assured and happy. THIS MUTUAL FUND BUSSINESS IS TOTALLY FAKE AND IS TO LOOT YOU ONLY THE FUND MANAGERS GET RICH BY IT.

hello mam,

i am a 20 year old guy. i can invest 5000 each month and want the fund in more liquidy. i don’t come in any tax category. what is the best option for me, sip or mf. if mutual fumd then what type of fund, equity or debt or growth??

Hi Gaurav, If your only requirement is liquidity, you could go for liquid funds. But investing 5000 rs every month without any goal may not be a prudent investment option as liquid funds are for temporarty parking of money and not for welath building. We suggest you talk/mail us with more details on your purpose, time frame,whether you can take some risks etc and we could get back to you. You can do this by using the ‘Ask Advisor’ feature, where you mail or schedule an appointment through that and our advisors will call back. Pl. see this to know where this feature is available in your account: http://content.fundsindia.com/images/GettingAdvice.png This facility does not cost you anything. tks, Vidya

actually i want to get back the invested money in approx each 3 years. i can invest on average 5000 each month but not in equal manner but in lump sum manner like 15000 in one time for next 3 month and like wise.

i want the liquidity not in all but in some of my fund to carry out my instance expenditures.

i don’t come in any tax category. my age is 21 now. So, now suggest some good investment options for me.

Hi Gaurav, If your investments keep varying, you can use the alert SIP or flexi SIP option available with FundsIndia for equity-oriented funds. Your investment can be a combination of balanced funds, MIPs and liquid funds. For fund-specific advice for individuals, you would have to take the ‘ask advisor’ route (pl. see the link I mentioned in my earlier reply to you). The advice given in a blog can be misconstrued as general advice. Fund requirements and needs vary across individuals. Tks, Vidya

Hi Vidya, nice post. Could you also suggest something for me. I would like to invest sumthing for my baby who is 1.5 years old. Thanks, Shilpi

Hi Vidya, very nice n interesting post.

Can you please suggest something for me too? I am a working lady and would like to invest something for my baby who is just 1.5 yrs old. Pls suggest.. Thanks, Shilpi

Hi Shilpi, Tks. It is a very prudent plan to start investing early for a kid. Would be happy to help. But we would need a lot of details such as your saving capacity, your risk profile, your time frame, what si the goal that you are saving towards – education, marriage etc. to choose the right funds that will work for you. All this is best addressed if you use our Ask Advisor facility (rather than a public forum like a blog), using your FundsIndia account (see this file to know where the feature is: http://content.fundsindia.com/images/GettingAdvice.png). It does not cost you. Schedule a call so that our advisor can call back and help you build a portfolio. Tks, Vidya

Hi Vidya, I want to setup a VTP from a liquid fund to an equity. However I am unsure as to whether I should choose dividend reinvestment option or growth for liquid fund. I am seeking advise specifically in terms of tax that I would incur in each option. Just for calculation purpose, say, I put a lump sump of 1.6lakhs in liquid fund and on a monthly basis do a STP / VTP for max 5000 into the equity fund. Also I would be continuining to invest in monthly basis in these funds for say next 3-5 years. Can you help me with all kinds of taxes that I would incurr which doing the VTP / STP and also when I would redeem that amounts in all of the following redemption scenarios:

1) Redeeming say 50000 from liquid fund within 1 year of initial investment

2) Redeeming say 50000 from liquid fund after1 year of initial investment

3) Quaterly SWP from equity fund after 1 year of first investment.

You have not mentioned what tax bracket you fall under. We will explain for all 3 rates.

1) Redeeming say 50000 from liquid fund within 1 year of initial investment

Response: You will incur short-term capital gains if growth is opted. Or you will suffer 28.3% (from june1) DDT plus capital gains tax (if you have any gain at the time of redemption) if dividend reinvestment is opted. If you are in the 10-20% tax bracket, prefer growth. If you are in the 30% bracket prefer dividend reinvestment.

2) Redeeming say 50000 from liquid fund after 1 year of initial investment – You will incur 28.3% DDT plus any capital gains tax of 10% without indexation or 20% with indexation (on gains if any) if dividend reinvestment is opted. If growth is opted then 10% without indexation or 20% with indexation. Prefer growth whichever tax bracket you are in.

3) Quarterly SWP from equity fund after 1 year of first investment.: withdrawal from equity fund after 1 year from date of instalment will not attract capital gains tax. No ddt n dividend. Hence youc an opt growth or dividend reinvestment. No tax impact.

Tks, Vidya

Hi Vidya, Thanks for clarification. I fall under 20% tax bracket right now, but would move into 30% possibly this year in another few months. Would that change any of your above suggestion.

Also when I do a VTP from Liquid Fund to Equity on a monthly basis, would that also incur me any tax since I have not left the investment for more than 1 year…maybe only 10 days into Liquid Fund investment since my first VTP to equity fund would start. So if I choose growth option in liquid fund, it would encur STCG tax, correct? But then I would not be transferring all funds from liquid to equity in one go. Maximum funds would stay (or keep on adding) in liquid fund for more than a year and only certain specific amount would be redeemed from liquid so as to invest in equity fund. SO in such situation which is the best option to incur minimum tax?

Also can I change the type from growth to dividend reinvestment from fundsindia itself. What’s the process for it?

Also for SWP from Equity, is there a way in which I can redeem the unit which was purchased a year back rather than most recently purchased unit so as to avoid any tax impact. Or would I have to leave the investment stagnant for 1 year after my last SIP before setting up SWP? Which would be best option.

Hi Gunjan,

1. There is no difference whether you do a VTP or STP. The fact is the money will suffer short-term capital gains tax if held for less than one year. For the purpose of deciding the time period of investment – the rule of FIRST IN FIRST OUT needs to be applied. Hence, the money/units that you invested first will be deemed to be redeemed and accordingly it will be treated as short term or long term.

Hence, based on time period, your requirement option will keep varying between dividend reinvestment and growth if you are in the 30% based on time period. There can therefore be no single formula.

Your call would be whether your money is mostly held for less than a year or not. If it is mostly parked for less than a year then you should use dividend reinvestment. If you do not want the hassle, you should simply stick to growth as the difference is marginal (30.9% vs 28.3%).

2. You can switch between growth and dividend reinvestment but fund houses treat it as a switch and hence capital gains will be applicable. It is therefore not a good idea to constantly keep changing between the two.

3. As we said earlier, FIRST IN FIRST OUT method is adopted for taxation. So if you are starting your SWPs says just one year after your SIPs, then there are chances that some units may be less than a year old (even if you follow FIFO). Hence, it is best to leave a few months’ gap before starting SWP. Moreover, I don’t think it is a good idea to do SWP in an equity just after one year of SIP/one year of holding. SIPs/VIPs need to be done for at least a 3-year time period in an equity fund before you decide to withdraw.

Tks, Vidya

I am investing Rs 5000/- per month RS 1500 in HDFC200 top gain [G], Rs2000 inHDFC Prudence [G]. Rs1500 inhdfc equity through SIP please advise me whether it is right investment for 10 years time.

The funds are good but why should you be investing all your SIPs in one fund house? Any reason? You may have some duplication in portfolio and benefit from only one style of investment. tks, Vidya

Hi I am 40 years currently and have two kids aged 8 and 7 yrs girls, I don’t have any info/idea on the Mutual funds, I would like to start investing 40K per month through SIP for 2-3 yrs and appreciate if you could advice what type of mutual funds and funds house to choose please.. Also I want to invest 1Lakh one time as i have the cash in hand currently.

Thanks

Hello Ram,

It is good that you have set yourself a time frame. Hope you will invest with a goal in mind. The 2-3 yr time frame is too short for you to go fully in to equity funds. Your amount and time frame would require us to discuss with you before we can suggest funds. You may pl. login to your FundsIndia account and use the Ask Advisor feature and schedule a call with our advisors. It is free of cost. Tks, Vidya

Hi I am 40 years currently and have two kids aged 8 and 7 yrs girls, I don’t have any info/idea on the Mutual funds, I would like to start investing 40K per month through SIP for 2-3 yrs and appreciate if you could advice what type of mutual funds and funds house to choose please.. Also I want to invest 1Lakh one time as i have the cash in hand currently.

Thanks

Hello Ram,

It is good that you have set yourself a time frame. Hope you will invest with a goal in mind. The 2-3 yr time frame is too short for you to go fully in to equity funds. Your amount and time frame would require us to discuss with you before we can suggest funds. You may pl. login to your FundsIndia account and use the Ask Advisor feature and schedule a call with our advisors. It is free of cost. Tks, Vidya

Thanks Vidya, the website ask to much of info for creating account and hence below details and appreciate your inputs:

Target amount around 2 cr by 55 yrs

Monthly investments willing to make: 40-50K per month or even more to get to the target amount

Risk – moderate

Type of investments looking at Mutual fund, FD, ETF

Thanks

Hello Ram,

I understand your predicament. At present, we answer only general queries through the blog. Our portfolio advisory services, which come free of charge, is a continuous service available to our account holders. The risk of answering portfolio queries in blog, is that other investors take it as ‘one size fits all’ and use it for their own goals as well.

Tks, Vidya

hi vidya

i am new to this type of invest ment. Let me know whats a mutual fund ? and whats an equity?

If i invest Rs one lakhs for a minimum of 5 years which will give much benifit?

Hi Neminath, Pl. visit our learn section to know about mutual funds and equities: http://pages.fundsindia.com/pages/learning/

Youc an also download our free ‘investment guide’ book for professionals.: https://blog.fundsindia.com/blog/general/investment-guide-for-todays-professionals/1794

Returns are not guranteed in mutual funds are stocks. But in the long term they have proven themselves to beat inflation as well as all other asset classes such as debt and gold. Tks, Vidya

hi vidya

i am new to this type of invest ment. Let me know whats a mutual fund ? and whats an equity?

If i invest Rs one lakhs for a minimum of 5 years which will give much benifit?

Hi Neminath, Pl. visit our learn section to know about mutual funds and equities: http://pages.fundsindia.com/pages/learning/

Youc an also download our free ‘investment guide’ book for professionals.: https://blog.fundsindia.com/blog/general/investment-guide-for-todays-professionals/1794

Returns are not guranteed in mutual funds are stocks. But in the long term they have proven themselves to beat inflation as well as all other asset classes such as debt and gold. Tks, Vidya

Hi Vidya,

I want to invest 5 laks into Liquid fund for 3-6 months time (which I need for downpayment of my house).

I want to invest another 10 laks for one year in liquid fund or FD (I am NRI so my interest on FD is tax free)?

Please could you advise in both cases which one is better for me.

Thanks

Ramesh

Hello Ramesh, You may choose any of the funds we have mentioned for the short-term in our select funds list. http://www.fundsindia.com/select-funds

But pl. ensure you are eligible to invest. NRIs from U.S and Canada cannot invest in certain funds. NRE deposits are tax free whereas liquid funds will suffer either capital gains tax od dividend distribution tax (based on which option you take). If the rates are over 7% you can go for it. Tks, Vidya

hey vidya..it was eye opening article on investments through mutual funds..

i need ur help in a query i m facing these days..

i have invested in a dividend plan (7 months) and now i m willing to shift to a growth plan within the same mutual fund.

i have to pay STCG on the increase in NAV of my current plan (dividend plan). i wish to opt an option of bonus stripping to nullify the tax effect…

my query is after shifting to the growth plan when i withdraw my investment (suppose after 6 months) would i be liable to STCG or LTCG..

STCG: FROM THE DATE OF SHIFTING??

LTCG: FROM THE DATE OF INVESTING IN THE MUTUAL FUND.

please give ur valuable advice and oblige me.. m waiting for the explanation…

thanks in advance

Hello Shrinuj,

Pl. go through the below tax law on restrictions when you use bonus stripping:

With effect from 1.4.2005, newly inserted S.94(8) of the Income Tax Act provides that if:

a. any person buys or acquires any units within a period of three months prior to the record date;

b. such person is allotted bonus units

c. such person sells or transfers all original units referred to in clause (a) within a period of nine months after such date,

he continues to hold all or any of the additional units referred to in clause (b),

then the loss, if any, arising to him on account of such purchase and sale of such units shall be ignored for the purposes of computing his income chargeable to tax. However, the amount of loss so ignored shall be deemed to be the cost of purchase of such additional units referred to in clause (b) as are held by him on the date of such sale or transfer.

In your case, your date of new purchase will be the date of shifting to the growth plan. Hence, if you exit 6 months after moving to growth, you will suffer STCG or if it is a loss (in case you have been issued bonus units)…such loss shall not be allowed to be set-off. For the bonus units, the date of allotment will be the date to be considered for purchase.

Put simply, to first of all enjoy any tax benefit from bonus stripping, you should have held the units (from the date of shifting) for a period of thee months before the bonsu units are issued. And the original units (other than bonus units) have to be held for at least 9 months from the bonus issue. Only then, the set-off of loss will kick-in.

Thanks,

Vidya

Hi, I read with interest the blog and your well researched replies. I for long time have a doubt about ELSS schemes. I expect these funds should perform better than equity funds in view of the mandatory lock-in period. The fund manager has an assured capital to play with during the lock-in period. In reality this is not happening and I find their performance is not much different than equity funds. Secondly since PPF savings limit has been increased to 1lakh per year ( maximum under 80cc) there is no charm in going in for ELSS.

Hi Gopalan,

Your observation about ELSS not performing any better than regular diversified funds is true. Perhaps the lack of pressure also makes these funds (or fund managers) a little laid back. Besides, there are only so many opportunities that are untapped. A ELSS scheme cannot discover a new opportunity (which is where alpha generation comes) that others haven’t. So in that sense, they are no different.

As for PPF, ELSS is linked to markets and the risk-return ratio is entirely different. Leave out the volatile markets of last few years, the returns that ELSS can generate (or has generated in the pre-2008 era) is far superior to a fixed-return product like PPF. Hence, I don;t think they are comparable. Also, PPF has many limitatiosn such as higher lock-in; ELSS has amonst the lowest lock-in for a tax-saving product.

Both these options can find place is a tax-saving portfolio if planned judiciously. Thanks, Vidya

Hi Vidya

It has been a great experience in reading your explanations to the vast number of queries, which also provoke me into contributing my two paisa worth thought.

IMHO there seems to be a bias in your reply that favours equity based products as compared to a simple debt product such as PPF.

There are at least 3 advantages in PPF as compared to an equity product such as mutual funds/stocks that are of far more significance to a large number of low and middle income savers.

Firstly, according to me return on PPF as a debt product with voluntary contributions has an implicit sovereign guarantee as the payouts are from the sovereign. Even if the returns may be lower as compared with voluntary contribution to EPF, savers other than those who are employees can beenfit from PPF. The current interest payout at 8.7% currently is more than the current YTM of the only other tax free debt products such as tax free infrastructure bonds issued by agencies such as NHAI,

Secondly, accumulated balances in PPF are not subject to the risks to capital value as compared to exchange traded debt or equity products. Even tax free infrastructure bonds are subject to market risks due to their being traded in exchanges.

Thirdly, PPF is easy to manage in terms of the savings bank account approach, which can be operated across both the bank and postal network. In spite of all of the advances in computerization, there are still a large number of persons who are not exactly comfortable with managing the complexity of maintaining fund or demat accounts.

I would admit that PPF’s disadvantage include the cap on annual contribution and lock in period of 6 years before withdrawals are permitted.

I think that these are worthwhile tradeoffs especially for lower or middle income households for whom, certainty of savings is perhaps more important than the uncertainty of capital appreciation and in worst case captial loss offset by the inflation beating returns that are at best marginal on annualized percentage basis.

It would still make sense for middle income households to accumulate Rs 1 lakh per year per family member in a safe product every year which could grow to a substantial sum over a a minimum of 15 years if not longer. This could be in addition to the contributions to the EPF and/or Superannuation schemes in case of salaried employees.

As many sensible financial advisers emphasize, difference in wealth creation is often attributed to the effect of regular savings of substantial amounts in a diversified manner across major asset classes over a long period. In such an approach it would be important to have both low risk fixed income instruments as well as high risk high return capital market instruments.

Perhaps it would be in the order of things to suggest that savers consider PPF upto the annual limit , as an essential element in their debt component of a diversified portfolio that includes other asset classes such as exchange traded equity/debt instruments as well as real estate, precious metals etc.

Regards

Rajasekaran

Hi, I read with interest the blog and your well researched replies. I for long time have a doubt about ELSS schemes. I expect these funds should perform better than equity funds in view of the mandatory lock-in period. The fund manager has an assured capital to play with during the lock-in period. In reality this is not happening and I find their performance is not much different than equity funds. Secondly since PPF savings limit has been increased to 1lakh per year ( maximum under 80cc) there is no charm in going in for ELSS.

Hi Gopalan,

Your observation about ELSS not performing any better than regular diversified funds is true. Perhaps the lack of pressure also makes these funds (or fund managers) a little laid back. Besides, there are only so many opportunities that are untapped. A ELSS scheme cannot discover a new opportunity (which is where alpha generation comes) that others haven’t. So in that sense, they are no different.

As for PPF, ELSS is linked to markets and the risk-return ratio is entirely different. Leave out the volatile markets of last few years, the returns that ELSS can generate (or has generated in the pre-2008 era) is far superior to a fixed-return product like PPF. Hence, I don;t think they are comparable. Also, PPF has many limitatiosn such as higher lock-in; ELSS has amonst the lowest lock-in for a tax-saving product.

Both these options can find place is a tax-saving portfolio if planned judiciously. Thanks, Vidya

Hi Vidya

It has been a great experience in reading your explanations to the vast number of queries, which also provoke me into contributing my two paisa worth thought.

IMHO there seems to be a bias in your reply that favours equity based products as compared to a simple debt product such as PPF.

There are at least 3 advantages in PPF as compared to an equity product such as mutual funds/stocks that are of far more significance to a large number of low and middle income savers.

Firstly, according to me return on PPF as a debt product with voluntary contributions has an implicit sovereign guarantee as the payouts are from the sovereign. Even if the returns may be lower as compared with voluntary contribution to EPF, savers other than those who are employees can beenfit from PPF. The current interest payout at 8.7% currently is more than the current YTM of the only other tax free debt products such as tax free infrastructure bonds issued by agencies such as NHAI,

Secondly, accumulated balances in PPF are not subject to the risks to capital value as compared to exchange traded debt or equity products. Even tax free infrastructure bonds are subject to market risks due to their being traded in exchanges.

Thirdly, PPF is easy to manage in terms of the savings bank account approach, which can be operated across both the bank and postal network. In spite of all of the advances in computerization, there are still a large number of persons who are not exactly comfortable with managing the complexity of maintaining fund or demat accounts.

I would admit that PPF’s disadvantage include the cap on annual contribution and lock in period of 6 years before withdrawals are permitted.

I think that these are worthwhile tradeoffs especially for lower or middle income households for whom, certainty of savings is perhaps more important than the uncertainty of capital appreciation and in worst case captial loss offset by the inflation beating returns that are at best marginal on annualized percentage basis.

It would still make sense for middle income households to accumulate Rs 1 lakh per year per family member in a safe product every year which could grow to a substantial sum over a a minimum of 15 years if not longer. This could be in addition to the contributions to the EPF and/or Superannuation schemes in case of salaried employees.

As many sensible financial advisers emphasize, difference in wealth creation is often attributed to the effect of regular savings of substantial amounts in a diversified manner across major asset classes over a long period. In such an approach it would be important to have both low risk fixed income instruments as well as high risk high return capital market instruments.

Perhaps it would be in the order of things to suggest that savers consider PPF upto the annual limit , as an essential element in their debt component of a diversified portfolio that includes other asset classes such as exchange traded equity/debt instruments as well as real estate, precious metals etc.

Regards

Rajasekaran

Hello Vidya,

Very informative post! Thanks!

Kindly add in your value added suggestions below!

I am a working professional under the 20%tax bracket. I wish to invest 50k in a money market fund and there on transfer it to a balanced (65% equity – 35% debt) combination fund i.e STP pf 5K per month. How advisable is it to go for it? Should I consider MIP aggressive/MIP conservative/ a pure liquid fund?

Also, Please explain the “taxation impact” if i may redeem all of them after 8-10 months.

Kindly suggest! Thanks in adv

Rgds

Snehal

Hello Snehal, If you simply transfer Rs 50,000 over 10 months, the STP will give you short-term capital gains tax under the growth option (the dividend option will suffer more DDT than your tax bracket). Hence for such short period (assuming you are starting the STP soon after investing in the money market fund), you might as well do an SIP from your savings account. Investing in balanced funds is a good idea provided you can hold them for 3-5 years and invest systematically for at least 2-3 years. Thanks, Vidya

Hi Vidya,

I fall under 30 % tax bracket and invest lot in Debt funds on fundsinida with dividend reinvestment, since fund house itself cut DDR , do we need to show proft in ITR as other source of income.

Pls advice..

Regards

Hello sir, You can avoid showing the dividend reinvested amount as dividends are anyway exempt in your hands and DDT is deducted. But in case you have sold the units and you do have capital gains (based on the reduced NAV after dividend payout) at the time of sale, it has to be shown as capital gains. Tks

Vidya

Hi Vidya,

I fall under 30 % tax bracket and invest lot in Debt funds on fundsinida with dividend reinvestment, since fund house itself cut DDR , do we need to show proft in ITR as other source of income.

Pls advice..

Regards

Hello sir, You can avoid showing the dividend reinvested amount as dividends are anyway exempt in your hands and DDT is deducted. But in case you have sold the units and you do have capital gains (based on the reduced NAV after dividend payout) at the time of sale, it has to be shown as capital gains. Tks

Vidya

Hello Vidya,

Thanks for the reply and very sorted explanation!

If someone has a certain amount being redeemed from loss making Mutual funds, doesn’t know where to invest it and needs it after a span 2-3 months; in such case will investing in a liquid fund be a safer option or an F.M.P?

Kindly suggest alternative options.

Thnx in advance

Rgds,

Snehal

Hello Snehal, Yes, liquid funds would be a better, safer and of course more liquid option for 2-3 months’ time frame. tks, Vidya

Thanks a lot Vidya!

Hello Vidya,

Thanks for the reply and very sorted explanation!

If someone has a certain amount being redeemed from loss making Mutual funds, doesn’t know where to invest it and needs it after a span 2-3 months; in such case will investing in a liquid fund be a safer option or an F.M.P?

Kindly suggest alternative options.

Thnx in advance

Rgds,

Snehal

Hello Snehal, Yes, liquid funds would be a better, safer and of course more liquid option for 2-3 months’ time frame. tks, Vidya

Thanks a lot Vidya!

Hello Mam

I have invested in brila and uti dividend yeild fund in dividend reinvestment option of Rs 60000

in each fund for one time i am 28 now and as i do business i will not be able to do SIP my query is that is both these funds enough to generate a target of 50 lakhs when i turn 60 years old.Thanks in advance

Hello Arun, if the funds earn 12% per annum then you would fall short. If they earn 15% per annum it should be possible. Take stock of it every few years and add more money if need be later. But wonder if you only need Rs 50 lakh for retirement? Hope you considered the impact of inflation on your cost of living. Do use the calculator in our retirement solutions service to know hhttp://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=4ow much you really need:

Vidya, a nice article explaining when to use the dividend or growth option – you seemed to have covered most of it (was linked here by you from your other article) https://blog.fundsindia.com/blog/mutual-funds/liquid-funds-invest/751

Hi Vidya,

Do all Ultra Short Term Debt funds have Dividend Reinvestment option? If not, where can I the list such funds offering this option?

Scenario: I want to invest lumpsum to start with and then SIP into the fund on a monthly basis. 30% tax bracket. Investment horizon: < 1 yr. This would be my emergency fund of my portfolio.

Regards,

Sandeep

Hi Sandeep, Yes, most of the ultra-short funds will have dividend reinvestment option. You can view the entire list in your FundsIndia account,within the said category. If your holding period is less than 1 year, dividend reinvestment is a good option for your tax bracket. But remember that ultra short-term funds will mostly have some exit load. Hence, if you are doing SIPs, ensure that you stop the SIP in such a way that you do not suffer exit load on the last/last few instalments (every instalment will be subject to the exit load period).thanks, Vidya

Hi Vidya,

Do all Ultra Short Term Debt funds have Dividend Reinvestment option? If not, where can I the list such funds offering this option?

Scenario: I want to invest lumpsum to start with and then SIP into the fund on a monthly basis. 30% tax bracket. Investment horizon: < 1 yr. This would be my emergency fund of my portfolio.

Regards,

Sandeep

Hi Sandeep, Yes, most of the ultra-short funds will have dividend reinvestment option. You can view the entire list in your FundsIndia account,within the said category. If your holding period is less than 1 year, dividend reinvestment is a good option for your tax bracket. But remember that ultra short-term funds will mostly have some exit load. Hence, if you are doing SIPs, ensure that you stop the SIP in such a way that you do not suffer exit load on the last/last few instalments (every instalment will be subject to the exit load period).thanks, Vidya

Dear Ms.Viday,

Please explain how Mutual Funds are Better than Bank FD’s/ NSCs ( > 6 years)?

Bank FDs/ NSCs will double in 6 years but

But majority of Mutual Funds returns will be in 2 digits, even after 6 years investment period?

i.e. I can get the double the amount in 6 years with NSCs but why Mutual Funds yield only certain percent ( ~ 15%) for same 6 years period?

tks.

Hello Mr Raja,

I think you may have misunderstood the concept of annualised return in mutual funds. When we say an annualised return of 15% it means the fund delivers 15% on an average every year in each of those 5 or 6 years. its not an absolute gain of 15%. That means, Rs 10,000 at 15% doubles itself in less than 5 years. Rs 10,000 invested in FD at say 10% takes about 7.3% to double without considering the damage of tax. with tax, the payback is even longer with FD. Yes, with NSC, depending on the rate which government offers it is possible. Thanks, Vidya

Thank you Ms. Vidya,

It’s confusing for me. Let’s say Return(%) for 6 moth =7.7%; 1 yr = 10.2 and 3 yr = 3.6%.

Here the Net return after 3 yrs = 3.6 x 3 = 10.8% .

From my previous post, f 3 yrs return= 15% means 3 x 15 = 45% is the total/ net return after 3 years. Is it so?

regards

rj

RETURNS (%)

6 mth 1 yr 3 yr

7.7 10.2 3.6

In the above example what is 3.6% means?

Does it mean it is the Average return for all 3 yrs or i

raja

hello raja, i am afraid you haven’t got the compounding interest theory right.It is not annual return multiplied by number of years. In financial parlance, any returns less than and up to 1 year is absolute and beyond that it is annualised (compounded), which is why universally, annualised return or CAGR is used for returns more than 1 year. This happens when interest or the gain stays along with the capital and also starts earning returns.

A 15% CAGR for 3 years means absolute returns of 52%.

Annualised return is calculated by (a/p)^ 1/n, where a is the final money you receive, P is the principal and n is the no. of years.

It is a derivative of the formula A= P(1+ r/100)^n for where, A is the final sum, P is the principal, r is the rate and n is the no. of years. While you may look up in the net on how compounding works, you can also use the rule of 72 for quick calc. Divide 72 by the rate of return to get the number of years. Example: If you expect 8% return, your money will double in 72/8=9 years. Rule of 114 applies for tripling and Rule of 144 for quadrupling.

Thanks.

It looks like the returns depicted for these funds with dividend reinvestment option is before applying DDT, correct?

(BTW, I am different Hari than the one commented some time back 🙂

Hi Hari,

I don’t know if you mean the example. We have not given any Did. reinvestment option as eg. here. But, dividend reinvestment very much suffers DDT. So any returns is always post DDt and in any case the NAV is after such DDT. Hence, any return calculation will be post DDT. Thanks

Sorry, I should have been more clear. E.g., take these two:

http://www.moneycontrol.com/mutual-funds/nav/icici-prudential-flexible-income-plan-wd-/MPI037

http://www.moneycontrol.com/mutual-funds/nav/iciciprudentialflexibleincomeplang/MPI036

They both report the same returns (I cross checked with FI as well). However, the absolute returns are different, which I am not sure includes the DDT, and how it can be -ve in case of dividend option.

Hi Vidhya,

I am a new comer in mutual fund but i want to take some good + safe return Gold ETF, Could you pls suggest me which is good for next 20-25yrs.(loooking for SIP with 1000/monthly).

Thanks in advance.

Reg,chaitanya

Hello Chaitanya, Pl. see the suggestions at the end of this article for gold funds. https://blog.fundsindia.com/blog/mutual-funds/how-have-your-gold-funds-fared/3660

Fund/portfolio advice is available free of cost to all FundsIndia investors who use the platform. If you have an activated account, pl. use the ‘Ask Advisor’ feature (Click help tab) to answer your query through mail or ask for an advisor call back. Our advisors can also help you build a long-term portfolio with sound asset allocation.Thanks.

Hi Vidya ,

Pls explain me whether large cap scrips and A group scrips are one and the same ?

Like wise Mid cap and B group scrips ?

Also generally people say that investing in Large cap scrips are more beneficial than investing Mid cap schemes ?

Pls clarify my doubts.

Hello Arun, Group A scrips are highly liquid scrips and typically are large or form part of top 200 companies by market-cap. Group A will be both large-caps and emerging large-caps (those that are not yet very large).

Group B will consistent of all residual stocks that are not under Group A or Group S (BSE Indonext or sme companies) or Group Z (companies that fail to comply with listing requirements).

BSE Midcap is not a group; it is an index based on the market-cap size of companies (mid-sized companies).

Investing in large-cap or mid-cap is a matter of risk and return reward you want. Mid-caps come with high risk and high returns. if you do not choose your mid-cap stock after proper research (in terms of company fundamentals as well as stock liquidity) then you may burn your fingers. Also, being a large-cap does not automatically mean good stable returns. many large-cap stocks delivered poor returns. If you are an invesgtor, you need to first understand, the sector performance and business performance of a company, whether large or mid-sized, before investing. That is the only key to good returns.

thanks, Vidya

Hi Vidya ,

I have savings of almost 50-60K in my savings account which i will require in coming 4-5 months for my higher studies.

I wanted to invest these in Liquid Funds , my tax bracket is 0% .

Which option should i go for (Growth , Dividend Re-investment) and also can you guide me for any specific Funds to invest.

Thanks,

Abhijeet

If you are in the 10% bracket, you might as well go for growth. Specific fund recommendations can be made through the free ‘Ask Advisor’ feature, if you have an activated FundsIndia account. thanks.

Dear Vidya,

I read with interest some of the posts.

1. I am a retired person in 20% tax bracket. I want to invest money for different time frames of 1 to 5 years. A return of over 10 percent or so will be fine.

2. Pl convey what are tax implications of FMP with a tenure starting in FY 2013-14 and maturing in 2015-16 ( example start date Feb 2013 , maturing April 2015) , and FMP starting Feb 2013 Maturing 2016.

3. What is the difference and comparison of Growth Vs Flexi options.

4 Which one is likely to be better for a period of 2-3 years FMP or Capital protection fund?

5. My questions are focused on funds which I understand are risk averse. In your opinion can there be a equity or debt equity mix fund which has a consistent good returns for say around last 7-8 years?

6. Most of the persons who work as financial advisers , whether in person or even in talk show on channel are not worth . some times the returns in MF on their advise is over all paltry 3-4% over a period of 4-5 years.

Thanks in anticipation

D. K. Arora

Hello Sir,

Thank you for reading the blog and writing here.

For your queries on funds/portfolio/allocation for you, we would be able to answer them only through our platform and not through the blog which is a general discussion centre. If you have an activated FundsIndia account, you could ask any number of questions/get review for your portfolio using our ‘Advisor appointment’ which is a free feature in the platform. This is an ongoing feature to ensure that you get on-demand advisory support, not just at the time of buying a fund but through the period of holding.

Pl. read our article https://blog.fundsindia.com/blog/mutual-funds/when-should-you-invest-in-fixed-maturity-plans/3278 to know tax implications for FMPs.

We do not recommend capital protection oriented funds as they are not efficient in delivering returns.

thanks, Vidya

Hi Vidya ,

I have savings of almost 50-60K in my savings account which i will require in coming 4-5 months for my higher studies.

I wanted to invest these in Liquid Funds , my tax bracket is 0% .

Which option should i go for (Growth , Dividend Re-investment) and also can you guide me for any specific Funds to invest.

Thanks,

Abhijeet

If you are in the 10% bracket, you might as well go for growth. Specific fund recommendations can be made through the free ‘Ask Advisor’ feature, if you have an activated FundsIndia account. thanks.

Dear Vidya,

I read with interest some of the posts.

1. I am a retired person in 20% tax bracket. I want to invest money for different time frames of 1 to 5 years. A return of over 10 percent or so will be fine.

2. Pl convey what are tax implications of FMP with a tenure starting in FY 2013-14 and maturing in 2015-16 ( example start date Feb 2013 , maturing April 2015) , and FMP starting Feb 2013 Maturing 2016.

3. What is the difference and comparison of Growth Vs Flexi options.

4 Which one is likely to be better for a period of 2-3 years FMP or Capital protection fund?

5. My questions are focused on funds which I understand are risk averse. In your opinion can there be a equity or debt equity mix fund which has a consistent good returns for say around last 7-8 years?

6. Most of the persons who work as financial advisers , whether in person or even in talk show on channel are not worth . some times the returns in MF on their advise is over all paltry 3-4% over a period of 4-5 years.

Thanks in anticipation

D. K. Arora

Hello Sir,

Thank you for reading the blog and writing here.

For your queries on funds/portfolio/allocation for you, we would be able to answer them only through our platform and not through the blog which is a general discussion centre. If you have an activated FundsIndia account, you could ask any number of questions/get review for your portfolio using our ‘Advisor appointment’ which is a free feature in the platform. This is an ongoing feature to ensure that you get on-demand advisory support, not just at the time of buying a fund but through the period of holding.

Pl. read our article https://blog.fundsindia.com/blog/mutual-funds/when-should-you-invest-in-fixed-maturity-plans/3278 to know tax implications for FMPs.

We do not recommend capital protection oriented funds as they are not efficient in delivering returns.

thanks, Vidya

i wish to invest approx 80,000/yr as SIP 7000/mth.

which u would advise from 04/14.

1canara robeco 2 axis long term equity

3 religare invesco 4 tata tax

5 hdfc tax saver 6 franklin india tax

sudhakar shenai,mumbai

senior citizen

Hello Sir,

I am forwarding your query to one of our advisors. They will get in touch with you for your query. In future, too, pl. use the advisor appointment (available when you click the help tab) to seek advisory or review services. This is a free service. The blog may pl. be used for general queries.Thanks, Vidya

Under dividend reinvestment optiop, dividend earned to be accounted for when units are redeemed or is it to be accounted for in the financial year in which it is earned?

Hello Joginder, on reinvested units, any gain calculatione etc. is always in the year of redemption. thanks, vidya

dear Sister,

i would like to invest Rs.1 Lakh (Emergency purpose) in Reliance Money manager fund. which option is good Growth or dividend? i’ waiting for your reply soon.

Best Regards.

RAJA

hello Sir, as the article states, if your holding period is less than 1 year and you are in the 10-120% tax bracket, opt for growth. else opt for dividend reinvestment. If your holding is greater than 1 year, then opt for growth. thanks, vidya

Hello Vidya,

I am investing Rs. 5000 per month in recurring deposits with different maturity timelines to serve the purpose of paying my insurance premiums across the year.

Is it good idea to switch to debt funds for the same purpose??

I am falling under 30% tax bracket. Please suggest.

Regards,

Deepak G.

hello Deepak, Sorry for the delayed reply. yes, it makes sense to go for liquid funds with dividend reinvestment option if you will take out the money in less than a year (if you are going to do an SIP, it would be less than a year of holding since you need the money to pay annual premium).

Hello Vidya,

I am planning to start investing a SIP in a HDFC Top 200 fund. I am looking at long term(say 10-15 years). Should i go for Growth option or Divident Re-investment option?

regards,

Nithin

Hello Roshan, sorry for the delayed response. They are the same in equities. Simply go for growth. thanks, Vidya

Hi Vidya,

First of all i want to congradulate you for patiently answering each and every ones query. Great work.

I’m maintaining NRI status and got some surplush cash in my savings account which will be required in 2 to 3 months time. Is it prudent to invest this cash in a liquid fund? if yes kindly advise the fund and type of option to choose?

Warm regards

shaji unni

Hello Shajji,

Yes, liquid funds are a good option to investing for short term in lieu of the entire money lying in a savings account. You can go with dividend reinvestment. I am afraid, I am constrained from offering you fund advice in this forum. If you have an account with us, pl. use the help tab (schedule an advisor appointment) and mail your query through that. the ticket will be answered by our advisors. thanks, Vidya

Hi Vidya,

Thanks for the reply. Can you just tell me the Tax implications for NRI’s investing in liquid fund dividend reinvestment options?. Do i need to pay any tax while withdrawing the funds?. Planning to open an A/C with Funds india during my next visit to india.

Regards

shaji unni

Hello Shaji, Sorry for the delayed response. Even in dividend reinvestment, if there is any capital gain (excluding the dividend reinvestment), you will have TDS (if holding is over one year it will be 20% on gains after indexation benefit. if held for less than 1 year then 30% on any gain) on any such gain. thanks, Vidya

Hello,

sorry one more doubt. while choosing the divident reinvestment option in a liquid fund which option to choose daily, weekly or mothly divident. I will require the money may be(may not be) after 4 to 6 months time . Also each divident re-investment amount will be considered for LTCG or STCG tax depending on the period of investment like in a equity fund.

Thanks

shaji

hello Shaji, unless the amount is very high in multiple lakhs or crore, weekly, daily options are not needed. on your second ques, yes, you are right..which is why growth is easier, now that there is not any tax diff because of DDT calculation change. see here for the change: https://blog.fundsindia.com/blog/mutual-funds/should-you-go-for-the-dividend-option-post-budget/5711

Hi

I have one question.

Is indexation apply on debt mutual fund with dividend option for long term investment ? (> 1 year). If yes, how to account for div. received while calculating gain/loss?

Hello Rajal,

Dividend will not be added while calculate capital gain as it is seprately taxed at the AMC end (DDT). Tiem period for investment for non-equity fudns have changed post budget. Pl. see our latest blog post. thanks, Vidya

I had invested Rs. 50,000 in UTI Fixed Term Fund (366 days), growth option & the same has been redeemed & the redemption amount is Rs. 55,352. What is the capital gain on this & is there any tax liability for me? If there is a tax liability, how is it arrived at?

Thanks

Hello Susan, Sorry for the delayed response. If you sold this after July 11 (when capital gains tax laws for debt funds changed), then it would be short-term capital gains taxed at your income tax slab rate (10, 20 or 30%). thanks, Vidya

Request clarification on the following

1) While computing absolute gain should we consider dividend reinvestment or only dividend payout?

2) what is the correct way of displaying returns ie absolute or annualized returns?

Hello Ramesh,

Sorry about the delayed response. I am assuming you are just asking about how to calculate gains. If you have a dividend option, ensure you add up the dividends to know your absolute gain. In dividend reinvestment, it will anyway be reflected. But pl note dividend paid out is not taxed in your hands.

Returns less than 1 year are absolute and over 1 year are usually shown as annualised.

Hello, Vidya

I am a 40 yr old Nre and new to Mutual funds. I would like to invest Rs 10k through SIP route for next 10 yrs. please suggest me some best mutual funds which are suitable for me with moderate risk

Hello Narayan, Sorry for the delayed response. The blog is mroe of a discussion forum.

We offer free fund advice and portfolio review for all our investors. Request you to open an account with us (no charges) to enable us to help you with any fund advice. You may be aware that we are an online platform offering which offers, convenient hassle free transacting experience for your entire family (with a single login) and provide quality investor advisory. If you wish to know more and need help opening an account, let me know and our support team can help you. the paper work is one time. This, provided you are an NRI from other than US/Canada. If you are from US/Canada, most AMCs do not offer funds for this category as SEC disclosure reqmts have made it tough for fund houses to cater to US/Canada NRIs. thanks, Vidya

Dear Vidya,

First of all the explanations in this blog really helps a below average investor like me a lot. Wish to know two things:

1) Kindly let me know 3 Liquid fund options to park money directly for short term horizon, like for 3-6 months, which can be also utilized as STP corpus.

2) Secondly need at least 5-10 funds in Large cap, midcap, balanced catagory for investing a total of 30K per month for 15 years as SIP.

Best regards,

Sanjoy

9619347113

Hello Sanjoy, thanks.

For us to be able to help you with portfolio advice and review, you would have to be an account holder with us. Once your account is activated you will hear from our advisors. Else, you can use the help tab and use the advisor appointment feature to ask your query. The blog is a discussion forum and I will be constrained from taking any portfolio/advisory queries in this. Request you to complete your one-time paper work formalities to avail continued advisory support. thanks, Vidya

Dear Vidya,

Do the funds maintain separate portfolios for Dividend option and Growth option or is it just Accounting jugglery. How far is this correct. I always thought the Dividend option requires a different approach for stock selection as against the Growth option.

Regards

Hello Sir,

There are separate NAV accounts maintained for growth and dividend as they have to delcare NAVs separately. But if youa re talking about portfolios, the issue does not arise as there is one portfolio for 1 scheme. The idea of dividend is simply to strip to gains made from managing a portfolio and give it back to you; whereas the same gain is retained and reinvested in the market in case of growth. For you, the gain made is on your NAV, dividend or growth as the case may be. The underlying stocks, are the same, as they ought to be.

thanks, Vidya

Hi Vidya,

Can you throw some light on the newly introduced Bonus option in Mutual Funds ? Can you explain in detail , their Tax efficiency , How the bonus is give etc…

Thanks

Jinny

hi,

I am investing in mutual funds of option Regular Growth, I am unable to understand what is meant by re-investing the amount. I have checked the statement for last 3 years but wasn’t able to see any additon of shares/re-investment.

Would be helpful if you can explain how is returns caculated for growth plan.

thanks in advance.

If you opt for dividend plan, then only dividends are declared. If you opt for growth plan, dividends will not be declared and the NAV grows much faster than the dividend plan.

It is similar to the cumulative and interest payout option in Bank FD. In cumulative option, you earn interest for the principal and get back the accrued interest and principal on maturity. In interest payout option, you withdraw the interest year on year and take back the capital on maturity.

Hi,

I want to invest in SIP for long term for my newly born baby. My motto is to accumulate money till the age if 18 years for his higher studies. I will not withdraw any amount from fund. Kindly suggest the type of Scheme & fund in which I should invest

Sandeep, for fund specific advice, you will need to write to us using your FundsIndia account. We will be glad to help you.The blog is only a general discussion forum. Broadly, for such long term, you should consider equity funds. thanks, Vidya

Hi Vidya,

I am planning to invest in a mutual fund (Growth). Correct me if I am wrong, now in the growth fund, basically the dividends if issued is reinvested in the fund automatically. I am not aware of any lock-in period. Also what is the difference between a regular expense ratio and direct ratio? I saw a 50% difference in a fund recently at one of Franklin India funds. Isn’t it best to invest in a growth fund and choose the direct ratio?

Thanks for your response!

Suresh

Hello Suresh,

There are no dividends declared in growth scheme (what youa re talking of is dividend reinvest). The gains simply accumulate in your NAV.

Direct mode implies investing directly through the AMC without a distributor. The difference in NAV is not as high as you mention but yes the NAV of the direct plan will be higher since there is no distribution fee involved int he expense ratio. The expense ratio is lower for direct since this component is not there. If you do not need any hand holding with funds, know where to invest and when to drop an underperformer and do not mind using multiple login to invest with multiple AMCs and invest through multiple portals, you can consider direct plan. Vidya

Thanks for your response Vidya. So is dividend-reinvest the same as growth scheme since it appears that they just leave the dividends and let it compound and grow?

Also in a dividend scheme, wouldn’t we be taxed if we get a dividend within a year, as this dividend paid out is extra income?

I was reading somewhere about dividend reinvest that the NAV value comes down when dividend is paid.

My understanding of a dividend reinvesting is described in the following example:

Let say I buy 100 shares for Rs 100 (Each Rs 1). Now I get a dividend of Rs. 10 after a year and so my value is now Rs 110 which is equal to 110 shares. Later the price for each share is Rs 2 and now my value has increased from Rs 110 to Rs 220.

But from what I read it says that my overall NAV value will be adjusted. My confusion is why should NAV value decrease if I get a dividend? The NAV value may increase or decrease regardless of dividends paid out right?

Thanks!