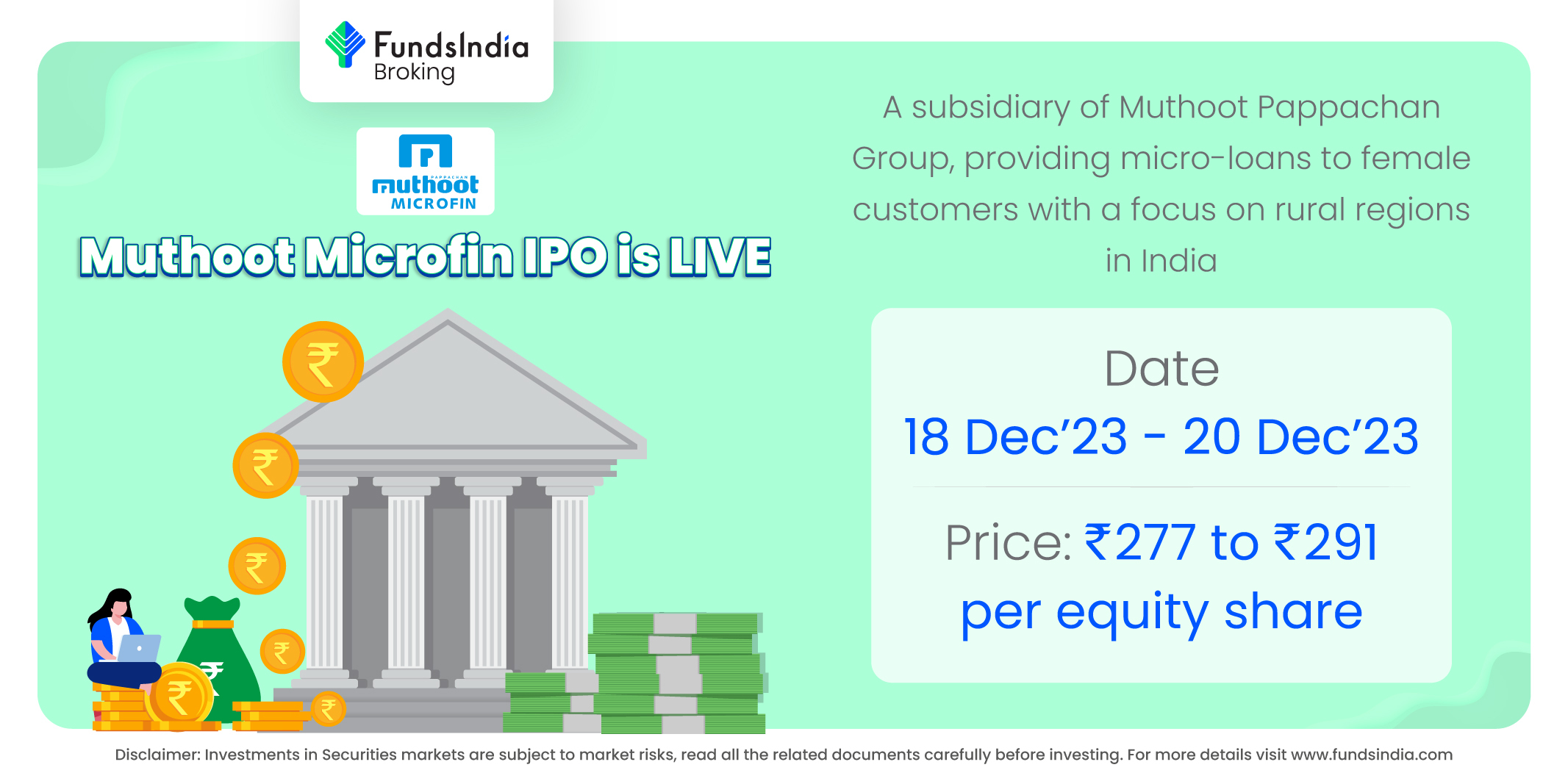

Company overview

Muthoot Microfin Ltd is Non-Banking Financial Company-Micro Finance Institution (NBFC-MFI) providing microloans to women customers (primarily for income generation purposes) with a focus on rural regions of India. The company is a part of Muthoot Pappachan Group, a business conglomerate with a history of over 50 years in financial services business. It is the second largest company under the Muthoot Pappachan Group, in terms of AUM for the Financial Year 2023. As of March 31, 2023, the company has 2.77 million active customers, who are serviced by 10,227 employees across 1,172 branches in 321 districts in 18 states and union territories in India.

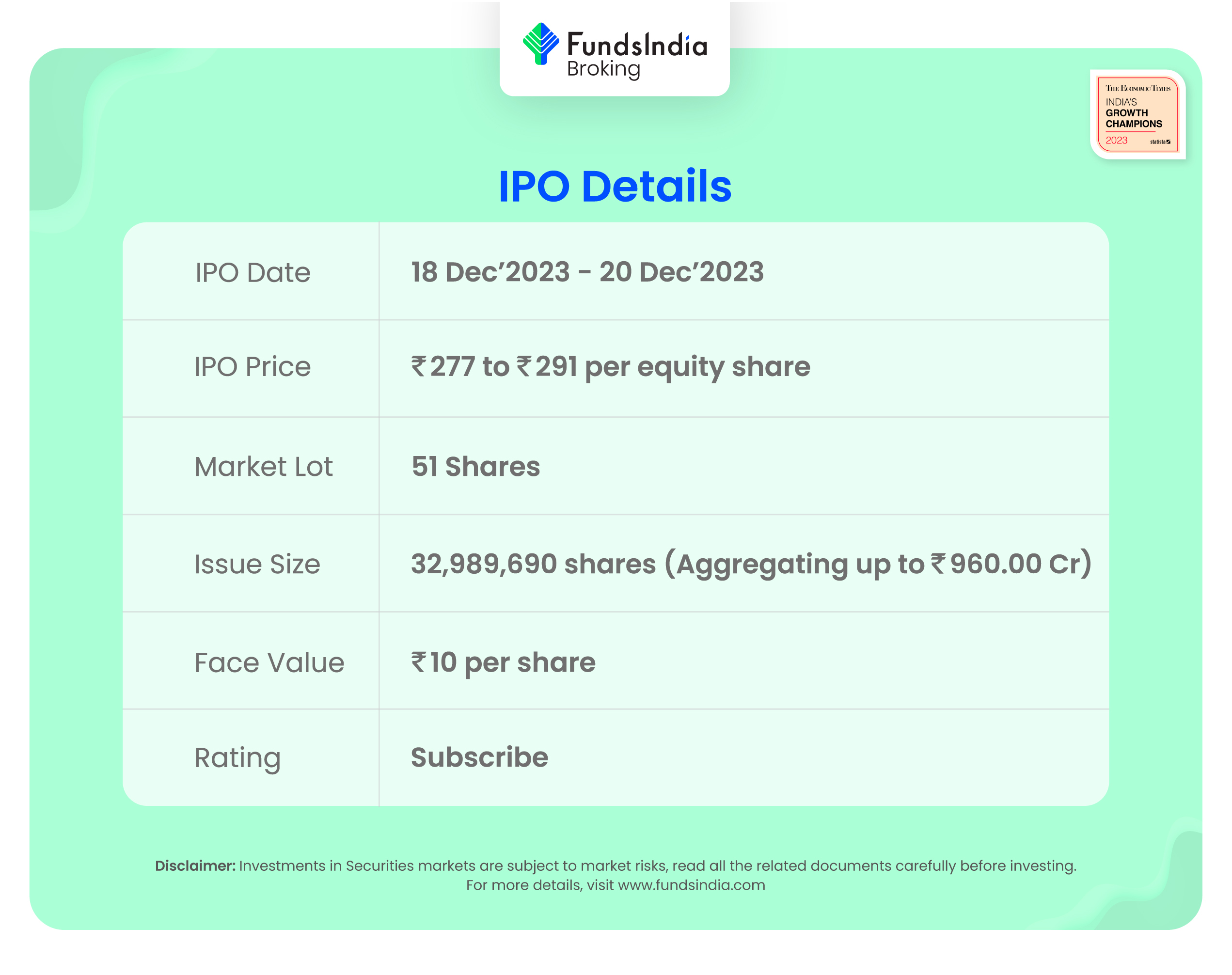

Objects of the offer

- Augmenting the company’s capital base to meet future capital requirements.

- To undertake existing business activities.

- To undertake the activities proposed to be funded from the Net Proceeds.

- Achieve the benefits of listing Equity Shares on the Stock Exchanges.

- Carry out offer for sale of up to 6,872,852 Equity Shares by the Selling Shareholders

Investment Rationale

- Diversified product portfolio – The company primarily provide loans for income generating purposes to women customers living in rural areas. The loan products comprise (i) group loans for livelihood solutions such as income generating loans, Pragathi loans (which are interim loans made to existing customers for working capital and income generating activities) and individual loans; (ii) life betterment solutions including mobile phones loans, solar lighting product loans and household appliances product loans; (iii) health and hygiene loans such as sanitation improvement loans; and (iv) secured loans in the form of gold loans and Muthoot Small & Growing Business (“MSGB”) loans. In 2021, the company launched its proprietary application “Mahila Mitra”, paving way for digital collection infrastructure which facilitates digital payment methods such as QR codes, websites, SMS-based links and voice-based payment methods. Collaborating with M-Swasth since December 2021, the company offers digital healthcare facilities to its customers through e-clinics. Additionally, it also provides natural calamity insurance products to its customers.

- Market leadership with pan India presence – As of March 31, 2023 the company’s gross loan portfolio amounted to Rs. 9208 crores. 95% of this was comprised of income generating loans totaling Rs. 8746 crores. It is the fourth largest NBFC-MFI in India in terms of gross loan portfolio as of December 31, 2022. It is also the third largest amongst NBFC-MFIs in South India in terms of gross loan portfolio, the largest in Kerala in terms of MFI market share, and a key player in Tamil Nadu with an almost 16% market share, as of December 31, 2022. The company’s robust risk management framework, customer selection methodologies and regular end use and payment monitoring have resulted in healthy portfolio quality indicators such as high collection efficiency, stable PAR and low rates of gross NPAs and net NPAs. Collection efficiency was 95.84% for the Financial Year 2023, and gross NPA ratio was 2.97% and net NPA ratio was 0.60%, as of March 31, 2023. As of December 31, 2022, the company had the second lowest gross NPA ratio and net NPA ratio among the selected NBFC-MFIs.

- Financial Track Record – The company reported a revenue of Rs.1429 crores in FY23 as against Rs.833 crores in FY22, an increase of 72% YoY. The revenue has grown at a CAGR of 45% between FY2021-23. The company posted interest income of Rs.1291 crores in FY23 as against Rs.729 crores in FY22, an increase of 77% YoY and a CAGR of 44% between FY21-23. The EBITDA of the company in FY23 was Rs.788 crores and EBITDA margin was at 55%. The PAT of the company in FY23 is at Rs. 164 crores and PAT margin is at 11%. The CAGR between FY2021-23 of EBITDA is 55% and PAT is 384%. The ROE of the company stands at 11% in FY23. GNPA improved from 6.26% in FY22 to 2.97% in FY23. NNPA improved from 1.55% for FY22 to 0.60% for FY23.

Key risks

- OFS risk – In addition to fresh issue, the IPO will see the offer for sale of shares worth upto Rs.70 crores each by promoters Thomas John Muthoot, Thomas Muthoot and Thomas George Muthoot, Rs. 30 crores each by promoters Preethi John Muthoot, Remmy Thomas and Nina George, and Rs.100 crores by investor Greater Pacific Capital WIV Ltd.

- Regulatory risk – As an MFI, the company is subject to inspections by RBI. Non-compliance with observations made by the RBI during these inspections could expose the company to penalties and restrictions which might have a material impact on the business and operating performance.

- Default risk – The risk of non-payment or default by customers may adversely affect the company’s business, results of operations and financial conditions. The company’s target customer segment is predominantly women from rural regions who generally has limited sources of income, savings and credit histories which might affect the credit worthiness and repayment capabilities.

Outlook

With the company’s operations concentrated historically in South India, the company has recently started to expand into North, West and East India and have a total of 596 branches across North, West and East India as of March 31, 2023, representing 50.85% of total branches as of March 31, 2023. The company’s strategy of expansion across various geographies in India and increasing customer base is expected to aid the company to continue its ongoing growth for future years as well. According to RHP, Equitas Small Finance Bank Limited, Ujjivan Small Finance Bank Limited, CreditAccess Grameen Limited and Suryoday Small Finance Bank Limited are few of the listed competitors for Muthoot Microfin. The peers are trading at an average P/E of 18.22x with the highest P/E of 26.67x and the lowest being 6.33x. At the higher price band, the listing market cap of Muthoot Microfin will be around ~Rs.4159.96 crores and the company is demanding a P/E multiple of 25.23x based on post issue diluted FY23 EPS of Rs.11.54. When compared with its peers, the issue seems to be fully priced in (fairly valued). Based on the above views, we provide a ‘Subscribe’ rating for this IPO for a medium to long-term Holding.

If you are new to FundsIndia, open your FREE investment account with us and enjoy lifelong research-backed investment guidance.