Glenmark Life Sciences Ltd. – Pure Play API Manufacturer

Glenmark Life Sciences (GLS), a subsidiary of Glenmark Pharmaceuticals Ltd, is one of the leading developers and manufacturers of selective high-value Active Pharmaceutical Ingredients. The company further operates in Contract Development and manufacturing operations to offer services to specialty Pharmaceutical companies. It has a diversified portfolio of 139 molecules and supplies its products to customers in India, Europe, North America, Latin America, Japan and the rest of the world (ROW). The company’s 4 manufacturing facilities are located in Ankleshwar, Dahej, Mohol and Kurkumbh with a total installed capacity of 1198 KL, which are regularly inspected by global regulators such as USFDA, PMDA (Japan) and EDQM (Europe).

Products & Services:

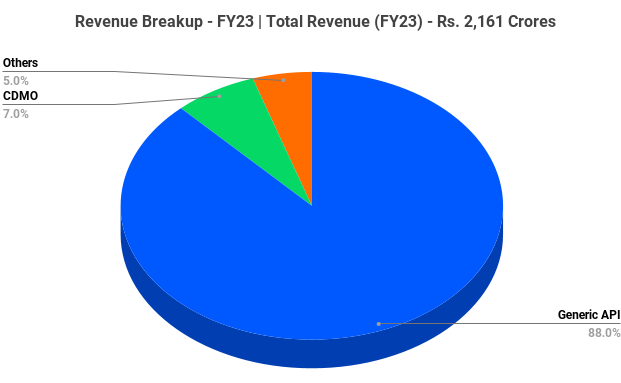

The company has three segments namely API, CDMO and others.

- Generic API – API (Active Pharmaceutical Ingredient) is the company’s major revenue generating segment which consists of 139 APIs across various therapeutic segments like Cardio Vascular Disease (CVS), Central Nervous Disorders (CNS), Diabetes, Oncology, Pain management, Anti-Infectives, Gastrointestinal health, etc.

- CDMO – The company leverage its process research, analytical research and chemistry capabilities to provide CDMO (Contract Development and Manufacturing Operations) services for a range of multinational corporations and specialty companies.

- Others – It’s a service segment which is nothing but providing end-to-end support to partners.

Subsidiaries: As on FY23, the company doesn’t have any subsidiaries.

Key Rationale:

- Established Position – GLS’ API segment consists of the development and manufacturing of APIs in chronic therapies, including CVS, CNS, pain management and diabetes. GLS also manufactures and sells APIs which is used to treat gastrointestinal disorders and those used for anti-infective applications and other therapeutic areas. GLS continues to have strong relationships with the top 20 global generic pharmaceutical companies based in the US, Europe and Japan, which provide revenue visibility. The company’s major API and intermediates have market leadership positions. The company’s ability to develop the niche and unique chemistry with a low-cost operational model is the key competitive advantage.

- Expansion – Glenmark Life Sciences has completed the addition of 240 KL of API capacity as well as the oncology facility at Dahej. A 208 KL backward integration plant is under construction at Ankleshwar, with a further 192 KL commissioned in Mar’23. The greenfield project at Solapur is also progressing well with consent to establishment (CTE) received for 1,000 KL, scheduled to be operationalised over FY24-FY26. Overall, the company’s reactor capacity stood at 1,198 KL as of FY23 which is targeted to double to 2,405 KL by FY26.

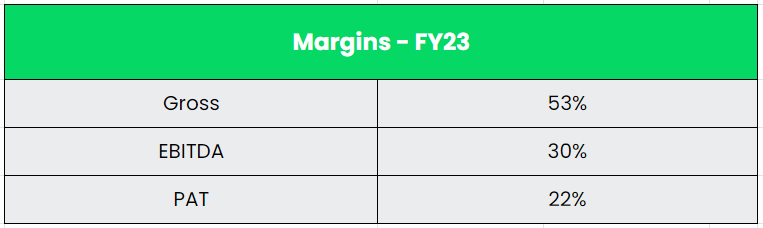

- Q4FY23 – Glenmark Life Sciences registered a revenue from operations of Rs.621 crs for Q4FY23, recording a strong growth of 14.8% QoQ and growth of 20.9% YoY. Gross Margins for the quarter were at 54.9%, up 390 bps QoQ and up 450 bps YoY driven by higher contribution from CDMO, better product mix, PLI scheme benefit and lower input cost. EBITDA for Q4 FY23 was at Rs.206 crs up 42% QoQ and 45% YoY. EBITDA margins were at 33%, up ~600 bps QoQ and up ~550 bps YoY. Profit After Tax (PAT) for the quarter was at Rs.146 crs in Q4FY23, registering a growth of 39% QoQ and 47.4% YoY. PAT Margin for the quarter was at 23.5%. Generic API revenues in Q4 FY23 increased 10.4% QoQ and increased 15.5% YoY. CDMO revenues at Rs.57 crs has doubled sequentially and grew by 30.5% YoY in Q4FY23. CVS, CNS and pain management portfolio continues to deliver a steady growth. Portfolio wise, CVS contributed 36% of the overall revenue, followed by CNS with 15%, Diabetes with 4%, Pain Management with 6% and others with 39% respectively for Q4FY23.

- Financial Performance – The company’s revenue and PAT CAGR stands at 25% and 24% between FY19-23. The Reserves in the balance sheet has grown at a whopping CAGR of 123% for the same period. The company has a positive operating cashflow historically and a total of ~Rs.1300 crs for the last three years. The company is literally a debt free company with a very zero borrowings in its balance sheet. The R&D spends for the company have grown at CAGR of 15% from Rs.37.6 crs in FY19 to Rs.65.2 crs in FY23. The R&D Spends as a % of sales stands at a record 3% in FY23.

Industry:

India is the largest provider of generic drugs globally and is known for its affordable vaccines and generic medications. The Indian Pharmaceutical industry is currently ranked third in pharmaceutical production by volume after evolving over time into a thriving industry growing at a CAGR of 9.43% since the past nine years. The pharmaceutical industry in India is currently valued at $50 Bn and it is expected to reach $65 Bn by 2024 and to $130 Bn by 2030. India is a major exporter of Pharmaceuticals, with over 200+ countries served by Indian pharma exports. India supplies over 50% of Africa’s requirement for generics, ~40% of generic demand in the US and ~25% of all medicine in the UK. Indian pharma companies have a substantial share in the prescription market in the US and EU. The largest number of FDA-approved plants outside the US is in India.

Growth Drivers:

- The cumulative FDI equity inflow in the Drugs and Pharmaceuticals industry is US$ 21.46 billion during the period April 2000 – March 2023.

- The Government introduces two PLI schemes named PLI 1.0 and PLI 2.0 for pharmaceuticals and bulk drugs with a total investment outlay of Rs.21,940 crs.

- The rising prevalence of chronic disorders, increasing demand for personalized medicine and emergence of novel drug delivery devices are some of the key factors expected to drive the API market over the next five years.

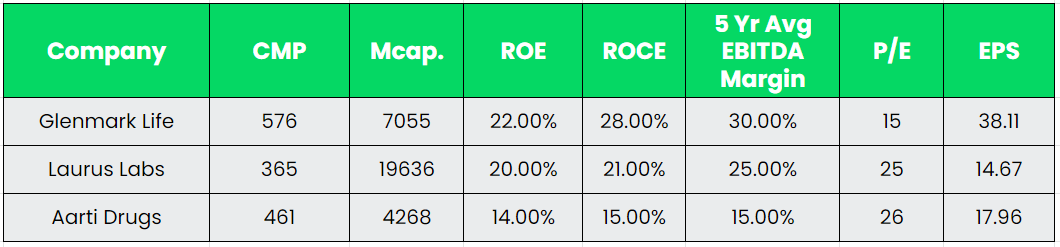

Competitors: Laurus Labs, Aarti Drugs, etc.

Peer Analysis:

Glenmark Life is generating the best ever EBITDA margins among its API peers with its low volume high value product strategy. Apart from EBITDA Margin, the other metrics such as return ratios, debt to equity and cashflow generation are also favouring the Glenmark Life sciences.

Outlook:

GLS’ positioning of being a pure-play API manufacturer is strengthened by its service offerings across markets, which enables it to act as a one-stop shop for formulation companies. The company’s DMF (Drug Master Files) filing continues across major markets in Q4FY23, taking the total cumulative filings to 468 as on 31 March, 2023. In the Generic API segment, Addition of 1 new high potent API to the development grid has taken the total number of high potent API in the GLS portfolio to 9, with a global market size of more than USD 19 billion (Source: IQVIA Dec’22). Out of the 9, 5 products are in an advanced stage of development. 3 iron compounds are in the various stages of development with cumulative global market size of more than USD 1.8 billion (Source: IQVIA MAT Dec’22). Out of the 3 iron compounds, 1 got the Regulatory filing completed. In the CDMO Segment, Multiple discussions are going with the companies across the globe for additional business opportunities.

Valuation:

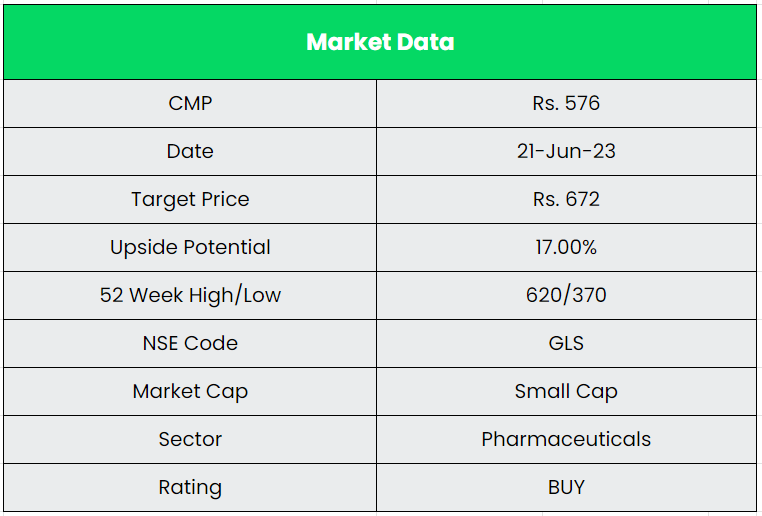

The company has a focus on specific high-value, non-commoditized APIs in chronic therapeutic areas of CVS, CNS, pain and anti-diabetic. It has a uniquely placed API portfolio, where it selectively chooses products based on market entry barriers and competitive intensity. We recommend a BUY rating in the stock with the target price (TP) of Rs.672, 13x FY25E EPS.

Risks:

- Client Concentration Risk – Over FY19-FY22, excluding Glenmark Pharma (Parent), GLS’ five largest customers accounted for 25-35% of sales. Some of these customers currently manufacture or may start manufacturing their own APIs and may discontinue purchasing APIs from GLS which is a key risk for the revenue.

- Forex Risk – A significant part of GLS’ revenues is denominated in currencies (mostly USD) other than INR. Though it has a partial natural hedge, any adverse forex movement can lead to forex losses for the company.

- Regulatory Risk – The US and EU are key geographies for GLS’s clientele, implying the risk of lapses in maintaining the strict cGMP standards required by regulators in these markets. However, there have been no regulatory lapses at the company’s manufacturing plants to date.