Are you enamoured by the attractive offers, especially the gold savings plans offered by jewelers this Akshaya Tritiya? ‘Pay 11 instalments and get the 12th instalment free’, ‘no wastage charges’, ‘enjoy loyalty club benefits’ and so on are some of the ‘offers’ that these schemes lure you with.

Are you enamoured by the attractive offers, especially the gold savings plans offered by jewelers this Akshaya Tritiya? ‘Pay 11 instalments and get the 12th instalment free’, ‘no wastage charges’, ‘enjoy loyalty club benefits’ and so on are some of the ‘offers’ that these schemes lure you with.

Let us take one such scheme offered by a popular jeweler in the country: you pay 11 instalments for the gold scheme and the jeweler contributes towards the 12th instalment. That means if you save Rs 3,000 a month in a gold scheme with a jeweler for 11 months – paying Rs 33,000 over the tenure, you get to buy gold worth Rs 36,000 at the end of the tenure. If you think that’s a big deal, then read on.

No Averaging

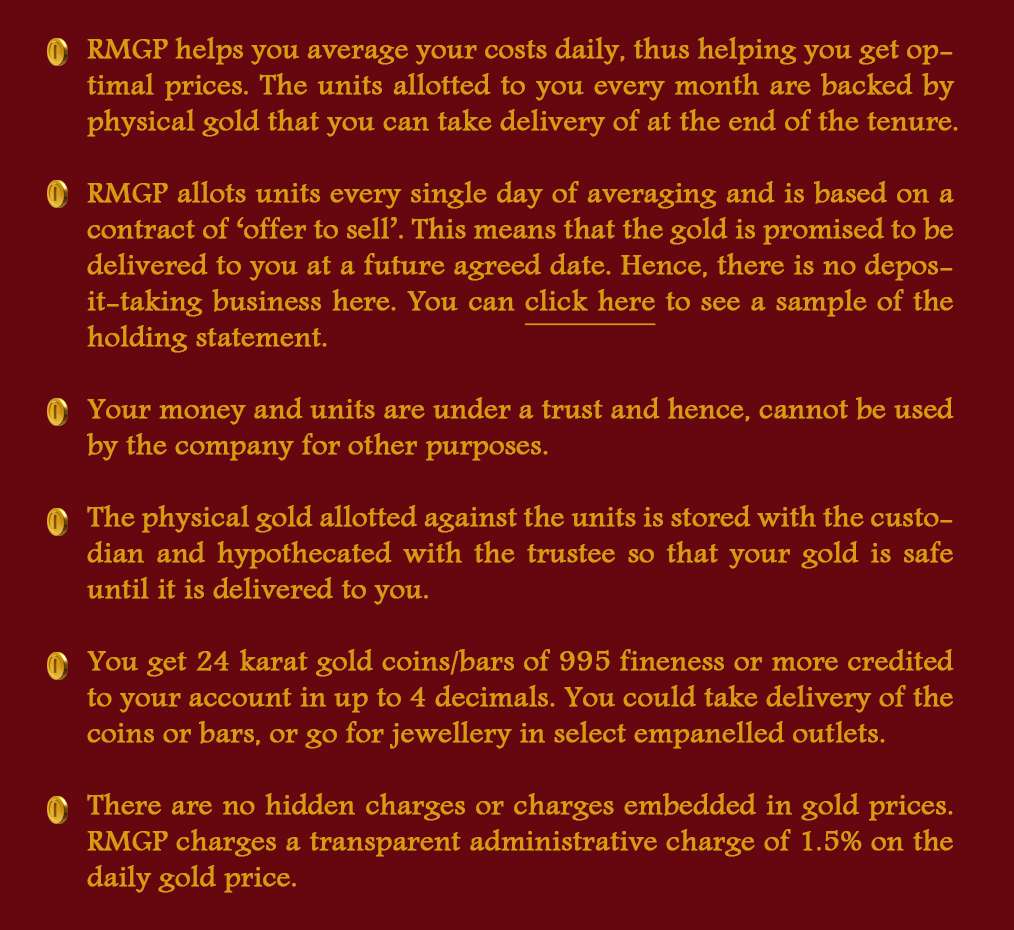

In schemes such as the one above, you are not allotted gold for every instalment that you make with the jeweler. That means the gold you are eligible to buy would be at the prevailing market price at the end of the term.

Let us suppose gold is Rs 2,895 a gram when you pay your first instalment. At the end of your 11th instalment, its price goes up to Rs 3000. That means you get to buy the jewellery at Rs 3,000 a gram and not at lower rates that may have prevailed earlier. In other words, you have no option to average your price of gold, although you pay an instalment every month.

It also follows that the Rs 3000 that the jeweler is contributing as the 12th instalment may actually fetch you a lesser gold equivalent. For instance, Rs 3000 paid by the jeweler would bring you just 1 gram, instead of 1.03 grams (at the beginning of the period in our illustration). Of course, you can argue that prices may come down. But then, would you be able to time your instalments knowing that prices are coming down?

You are Lending Money

On the face of it, you might seem to get a discount of 8.3% (Rs 3000 on Rs 36,000) in the above illustration. But is that really the case? By paying 11 instalments without any allotment of gold, you are effectively lending money to the jeweler. If a jeweler were to borrow outside, it would be anywhere between 10-18% for a loan, depending on the credit worthiness of the company. Hence, your money is a ‘low-cost’ credit line for him.

High Default Risk

Even assuming that the Rs 3000 you get is a form of interest for the money you lend for the tenure of the scheme, is your money in safe hands? Well, none of the jewelers’ schemes guarantee you gold and there is no separate body/trust safeguarding your money. And to add to it, since you do not have any units allotted (in the above illustration), there is always a possibility that you do not get gold if your jeweler decides to bid you goodbye.

In fact recently, a change in the deposit-taking rules under the Companies Law has large jewellery makers in a fix as the money that they take from you on the schemes may come under the Company Law radar, in which case, many of them may withdraw their schemes. You can click here to read more on this news.

Not a Pure Deal

As you may be aware, jewellery schemes allow you to buy only jewels which are of lower purity, often 22 karat or lower. This reduces the resale value of such gold as well.

Besides, you seldom get to buy jewellery for the value you have saved. In the above example, you may have Rs 36,000 at the end of the tenure but you may wish to buy jewels that are valued at Rs 50,000. Effectively, you not only offer a cheap loan to the jeweler but also enhance his business!

No Wastage…Really?

Do read the fine print or the ‘*’ that comes in the advertisements when it says no wastage. This is seldom the case. Often times, the wastage on designer jewellery is quite high that even if there is a small waiver on wastage, you seldom stand to gain much.

The Way Out – RMGP

If you are keen on buying physical gold, then Reliance My Gold Plan helps you overcome all the above limitations.

Besides this, you have a host of other features that make RMGP superior to jewellery schemes. Click here to read more for offers on the scheme.

60 thoughts on “Why Reliance My Gold Plan is Superior to Your Jewelers’ Schemes”

Comments are closed.

Could you please explain the business logic for Reliance here? How are they getting benefited by RMGP?

Hi Amit,

Reliance My Gold Plan is offered by Reliance Money Precious Metals Private Limited (RMPM), a Reliance Capital company. There is an independent trustee acting on behalf of all customers. For more details, please read here: http://ow.ly/whl9l

Had a clarification on the below points –

Customer can request for a partial fulfilment at least 1 month prior to maturity date subject to a

minimum fulfilment of 5 grams and in multiples of 0.5 grams thereafter. Customer can opt for

the partial fulfilment in form of Coin as well as Jewellery. No change to the fulfilment preferences

shall be allowed once the partial fulfilment request has been submitted

What does this mean? Do we need to have 5 grams of gold?

The Gold gram invoiced to the customer would be after adding the Administrative Charges on the Daily

Gold Price. The Administrative Charge would be 1.5% of the Daily Gold Price and shall be non-refundable.

For example, if the Daily Gold Price was Rs. 2800 per gram, then the price charged to the customer after

applying the Administrative Charge would be Rs. 2842 per gram.

As you mentioned that the amount would be distributed in 20 days cycle, so will the charges of 1.5% be on a daily basis.

Fulfilment Processing Charge of 2.5% will be charged on fulfilment requests made within 1 year

of Customer ID generation. The fulfilment Processing Charge will be levied on 12 times the

monthly subscription amount minus the cumulative subscription amount realized. For example, if

the monthly subscription amount of the customer is Rs. 3000/- and the customer has so far paid

Rs. 10,000 then Fulfillment Processing Charge @ 2.5% will be levied on Rs. 26,000 (i.e. Rs. 3000 x

12 – Rs. 10,000).

What would be the fulfilment charges if the gold is redeemed after 15 months?

Hi Lloyd,

1. Yes, you would need to have accumulated 5 grams of gold in your account to avail this partial fulfilment facility.

2. The charge deduction happens first, and the remaining amount is averaged over the purchases on a daily basis. The charge is not averaged over the purchases.

3. There is no fulfillment charges if the gold is redeemed after 15 months.

You didn’t talk about the 8% markup and additional charges?

http://capitalmind.in/2014/04/the-negatives-of-the-reliance-my-gold-plan/

Can we know how much commission you are earning from selling this product? (similar to how you have listed for other MFs on your site)

Hi Anshuk,

As per our agreement with our vendor we are not allowed to disclose the commission that we earn from selling this product.

However all products that are available on our site are in the best interests of an investor.

Seems like the gold prices in Reliance are very expensive. In their website today’s price its quoting Rs. 3,207.81 whereas the actual gold price is Rs. 2958 in mumbai. Do they have an explanation for this?

On one had they are offering 20% extra but on the other hand there is a difference of Rs.50

Hi Lloyd,

Reliance My Gold Plan is a savings plan which flashes a PAN India Price Landed Price (pre-tax) whereas others flashes a price which is not the landed Cost and has very specific delivery terms. This is also a necessity given that tax structures vary across different states of the country.

Can you explain, how this compares against Reliance Gold Mutual Fund in terms of expenses?

How are the units held? In the demat account? do the units have a secondary trading market?

I also see a banner advertisement below your article, which says limited period offer of 26% extra gold on first installment with funds India. Can you explain how Reliance is able to promise to credit additional 26% of first installment? Does this mean that there are hidden charges that are not clearly revealed upfront and 26% is a cashback of the larger hidden load/charge pie?

If you can kindly do a comparison of Reliance My Gold Plan vs Reliance Gold Fund vs Gold BEES and show the IRR difference between the 3 then things would be crystal clear for everyone.

Thanks,

Ashwin

Hi Ashwin,

The units are not held in a demat account. The gold is purchased on a daily basis and managed by a independent trustee. They don’t have a secondary trading market.

26% extra is only on the first instalment and only when you opt for a yearly SIP. There are no hidden charges and all the charges are clearly described on the website and FAQ documents.

Since Reliance My Gold Plan is a gold accumulation product, you cannot actually compare it with the other two since they are investment products. It would be tough to do an IRR calculation for Reliance My Gold Plan.

Thanks for the clarification. But I am still puzzled how they can afford to credit 26% into every yearly SIP account, even if it is just calculated on the first installment.

For ex: Take a SIP of 10,000/month. The charge applicable per sip is 1.5% = 150/month.

At the end of the year, net charges = 150 * 12 = 1,800 rs (assuming no other charges and no premature withdrawals).

Reliance promises to credit 26% of 1st installment, which is 2,600 rs.

The numbers don’t add up and there is a net deficit of 800 rs (1800 – 2600) that Reliance has to somehow provide for. If 1.5% is the only charge involved, the cost has to be loaded elsewhere. Can you explain this discrepancy, assuming that Reliance does not load the price of Gold itself to recover its costs?

Thanks,

Hi Ashwin,

Just like many jeweller’s schemes offer a free gold coin or other benefits to their customers, we’re offering 26% extra gold on the first instalment as a promotional offer to celebrate Akshaya Tritiya. This is a marketing expense for us and RMGP. We are proud to undertake this expense as we think this is the best plan currently available in the market to accumulate physical gold. As stated earlier, there are NO hidden charges and all the rates mentioned in the FAQ document of RMGP hold good.

I am puzzled at how you can conclude this (in your own words) to be “the best plan currently available in the market to accumulate physical gold” without computing the IRR as I requested in my previous post. Where are the data-points for this claim? Articles on this blog (specially by Vidya Bala) are backed by sound reasoning and data-points, but this one seems to be an outlier.

You are not competing with the corner-of-the-street jeweler, when you say “many jeweller’s schemes offer a free gold coin”, are you? We all know how these jewelers offer **free** gold. So the question was how Reliance plans to offer **free** gold. If its offered from FundsIndia’s kitty and is written off as “Marketing expense”, who bears the default risk on 26% promise? FundsIndia? or Reliance?

I am not nitpicking here, I respect FundsIndia, its transparency and standards of disclosure to its Mutual Fund customers. But unfortunately I don’t see the same high standards of transparency and conviction of disclosures when it comes to this particular product. I was not aware of such an offering until I saw the advt’s flashing all over funds India site and mail notifications. Had never experienced such an “in the face” ad campaign from funds India before.

Thanks,

Hello Ashwin,

I saw your comments on the blog on this article. While I do not analyse the product, I’d like to step in (and thanks for your complement) to share my understanding of this product with you. First, we do not ask the IRR of a gold product to a bank or a jeweller do we? It is the same here. This is simply a commodity/product you buy. Just that one may say it is a bit more efficient way to buy simply because you get to average the costs. What our team did, though, is compare buying gold coin (on a single day) with a bank and then see the average cost of buying through RMGP and the latter worked better.

Also, pl. note the IRR calculation would kick in only if there is also a cash inflow for you at the end of this product term. In this case it is gold that you get. Hence, the returns finally would depend on the price at which you sell the coin or bar, if you sell it, that is.

Next, it is not the corner street gold jewelers alone who offer gold schemes. Well-known country-wide players too offer it and this product RMGP is perhaps meant to compete with such schemes/products.

As for the ‘free’ offering, 20% is from RMGP. It is a promotional exercise as is the case with many products during festive seasons. the 6% from FundsIndia is indeed a promotional offer from us. The 20% onus is on RMGP and 6% on us. That answers your question on the default risk and who bears it.

Ashwin, if you are looking at gold from an investment angle, I am sure you know where to go – gold funds or gold ETFs is the place. And need I tell you that there are a number of people looking to invest in gold schemes because they WANT GOLD. RMGP caters to such requirement.

The advertisements on Gold flashing in FundsIndia is because it is Akshaya Tritiya season and there is an offer on. Hence the promotion. It will change once the offer is over. Ad campaigns can seem in the face depending on the nature of the product being offered some times 🙂 It is inevitable.

I would just like you to know that FundsIndia has done its bit of due diligence before offering this product and as has always been the case, we seek to offer unbiased services within the products we offer. You will appreciate that RMGP being a non-financial product has not been subject to the regular financial/analytical research that you see us giving with mutual funds on an ongoing basis.

Hope you see this point of view, even if you do not agree 🙂

Appreciate your participation/comments in our blog.

thanks, Vidya

Ashwin,

Just to add to my previous comment, you may, if interested read more details on RMGP here: http://s3-ap-southeast-1.amazonaws.com/fundsindia/LP/Topschemes/images/RMGP+AOF_TERMS+AND+CONDITIONS_Ver-1+5.pdf

thanks

Vidya

Thanks Vidya, your response clears quite a few concerns.

Your clarification on the product positioning that RMGP is for those who want physical gold and it is probably not the best choice for those who look at gold as a investment or inflation hedge, literally sets things crystal clear.

RMGP appeared like an interesting investment option when I came across it few weeks ago. However the documents go to a great extent to say that the price is not comparable. I understand few of their reasons but it makes me uncomfortable as a customer.

Some points in this article are valid but its like comparing apples and oranges – even if you put more data to prove a few scenarios, the future is not guaranteed. If I finally intend to buy jewellery with the gold, I’m sure no jeweller will give the market rate for Reliance’s gold simply because it was not purchased from them.

I’m also worried about the above-normal selling being done by FundsIndia for this scheme. Please refrain from it before you lose the trust of your customers!

Hi Pavan,

The gold offered under this plan is of 24 Karat purity at 995 fineness. If you wish to buy jewellery with the gold you accumulate through the plan, then you must know that the purity of gold offered by RMGP is quite high than the gold you purchase from conventional sources. Hence, you will get rates higher than what you would receive if you would just sell normal jewellery or gold coins. Also, if you consider this an issue, then you will face the same if you buy gold from banks or any other sources.

As an online investment platform, we’ve always strived to ensure that we offer an array of quality financial products to our customers. We’ve always refrained from offering all such products that aren’t feasible for our customers, or are of a sub-standard quality. We have and will always continue to stand by this belief.

Since gold plan is closed now, will Reliance return money or compel customers to purchase gold?

Hello Uttam, Sorry for the delayed response.

Many Gold plans of jewellers are closed as a result of deposit-taking norms of Companies Act. RMGP is not a deposit. It allots gold grams in your name as soon as you buy them. hence it is not closed.

Why not buy a gold ETF/MF in installments for 12 months and then convert to physical?

The only advantage of this installment system is that it averages the price. Well, that averaging can be achieved in the most cost-effective way by buying a gold ETF/mutual fund. Why would I want to use this plan instead?

And, anyway, averaging is better only half the time in an uptrend while it may be worse off in a downtrend. So, on average, over all customers and and over all trends, what difference does it make? Furthermore, the price risk within a year is not the predominant risk when the investment is for a long time horizon (of many years/decades).

And, what possible advantage is there in averaging daily within a month? That makes no sense whatsoever. The finance industry needs to stop spreading stupid ideas like daily averaging as if it is better.

Comparison with jewellers only doesn’t make sense. One can buy physical gold from banks and one can hedge future price risk with gold futures, ETFs, so any plan being offered by the financial industry needs to take these other avenues into account.

The main risk here is Reliance’s daily price which is not an industry-wide benchmark or an exchange price. Why is it not some exchange price + overhead? Reliance gets the benefit or knowing how much future purchase it needs to make (as people sign up for a plan in advance) so it can hedge future purchases or ensure that the supply is consistent so why does it not benchmark the price to the exchange/futures price with a fixed overhead?

Hello Vivek,

the discussion here is not to comapre ETF with RMGP. RMGP is to be purely viewed as a substitute for physical gold. it has allt he traits of physical gold purchase, except that it is more transparent and more efficient (online). As for averaging, compared witht he last price at which a jeweller gives, averaging has proved to work better. If averaging is better only half the time, then even SIPs in mutual funds should not be working right? But they work and work very well. We have also compared buying bulk purchase with bank versus averaging and the latter has worked better.

We are not talking of those using exchanges/ futures to buy gold. We are talking of lay people entering into jewellery schemes that are far riskier and opaque. Yes, pricing will not be the same gold landed price because we are talking of various other state taxes as well as transportation here. Yes, for investment purpose and for those who do not need physical gold, ETfs are good.

“the discussion here is not to comapre ETF with RMGP”

why not?

I think you don’t understand averaging. You did not address any of my points.

“We are not talking of those using exchanges/ futures to buy gold. ”

That is precisely my point. Why are you not talking about those avenues too? You should be.

“Yes, for investment purpose and for those who do not need physical gold, ETfs are good.”

I explained that you can convert your ETF holding with physical gold periodically if one so wishes. Again, you did not understand my point. Too bad.

Vivek, I am afraid, you have to first diferentiate between investing in gold and buying gold. RMGP is first a plan to simply buy gold in an efficient way. That is all. If you wish to talk about the other avenues (commodities etc), this is not the forum since we do not deal with them nor are they comparable. Nobody compares buying gold in a bank or jewellery shop with buying ETF or commodity futures. That is the same difference.

As for ETFs to gold…you need to be a HNI with KGS of gold to do that. we are talking of retail investors here.

“If averaging is better only half the time, then even SIPs in mutual funds should not be working right?”

Can you tell me which SIP plan talks about averaging WITHIN a month?

Hello Vivek, This is a gold plan that does averaging 20 days a month. So it is WITHIN a month. And not every averaging within the month will even out itself. Vidya

Dear Team,

I am interested in investing in this RMGP Gold ETF SIP. Could you please let me know the requirements (Required inputs for opening this ETF)

Regards,

Sreekanth

hello Sreekanth, RMGP is not an ETF. It is a monthly investment option to buy physical gold by avaraging it every month and getting gold units allotted every month. At the end of the tenure you get equivalent physical gold. With ETF,you don;t get physical gold. You can redeem the cash. If yu want ETFs, you need to have a demat brokerage account.

What about accumulated gold delivery. Is it any charges paid to reliance or fi. Deliver of physical gold is free or chargeable. If chargeable what are the charges against physical gold delivery

What about accumulated gold delivery. Is it any charges paid to reliance or fi. Deliver of physical gold is free or chargeable. If chargeable what are the charges against physical gold delivery

IS investing in RMGP still an option from FundsIndia? I am getting the below message while I try to invest,

“Sorry, we are not accepting fresh investments in the Reliance My Gold Plan (RMGP) at this point in time.”

IS investing in RMGP still an option from FundsIndia? I am getting the below message while I try to invest,

“Sorry, we are not accepting fresh investments in the Reliance My Gold Plan (RMGP) at this point in time.”

Hi Amit,

Reliance My Gold Plan is offered by Reliance Money Precious Metals Private Limited (RMPM), a Reliance Capital company. There is an independent trustee acting on behalf of all customers. For more details, please read here: http://ow.ly/whl9l

Seems like the gold prices in Reliance are very expensive. In their website today’s price its quoting Rs. 3,207.81 whereas the actual gold price is Rs. 2958 in mumbai. Do they have an explanation for this?

On one had they are offering 20% extra but on the other hand there is a difference of Rs.50

Hi Lloyd,

Reliance My Gold Plan is a savings plan which flashes a PAN India Price Landed Price (pre-tax) whereas others flashes a price which is not the landed Cost and has very specific delivery terms. This is also a necessity given that tax structures vary across different states of the country.

Could you please explain the business logic for Reliance here? How are they getting benefited by RMGP?

Had a clarification on the below points –

Customer can request for a partial fulfilment at least 1 month prior to maturity date subject to a

minimum fulfilment of 5 grams and in multiples of 0.5 grams thereafter. Customer can opt for

the partial fulfilment in form of Coin as well as Jewellery. No change to the fulfilment preferences

shall be allowed once the partial fulfilment request has been submitted

What does this mean? Do we need to have 5 grams of gold?

The Gold gram invoiced to the customer would be after adding the Administrative Charges on the Daily

Gold Price. The Administrative Charge would be 1.5% of the Daily Gold Price and shall be non-refundable.

For example, if the Daily Gold Price was Rs. 2800 per gram, then the price charged to the customer after

applying the Administrative Charge would be Rs. 2842 per gram.

As you mentioned that the amount would be distributed in 20 days cycle, so will the charges of 1.5% be on a daily basis.

Fulfilment Processing Charge of 2.5% will be charged on fulfilment requests made within 1 year

of Customer ID generation. The fulfilment Processing Charge will be levied on 12 times the

monthly subscription amount minus the cumulative subscription amount realized. For example, if

the monthly subscription amount of the customer is Rs. 3000/- and the customer has so far paid

Rs. 10,000 then Fulfillment Processing Charge @ 2.5% will be levied on Rs. 26,000 (i.e. Rs. 3000 x

12 – Rs. 10,000).

What would be the fulfilment charges if the gold is redeemed after 15 months?

Hi Lloyd,

1. Yes, you would need to have accumulated 5 grams of gold in your account to avail this partial fulfilment facility.

2. The charge deduction happens first, and the remaining amount is averaged over the purchases on a daily basis. The charge is not averaged over the purchases.

3. There is no fulfillment charges if the gold is redeemed after 15 months.

You didn’t talk about the 8% markup and additional charges?

http://capitalmind.in/2014/04/the-negatives-of-the-reliance-my-gold-plan/

Can we know how much commission you are earning from selling this product? (similar to how you have listed for other MFs on your site)

Hi Anshuk,

As per our agreement with our vendor we are not allowed to disclose the commission that we earn from selling this product.

However all products that are available on our site are in the best interests of an investor.

Can you explain, how this compares against Reliance Gold Mutual Fund in terms of expenses?

How are the units held? In the demat account? do the units have a secondary trading market?

I also see a banner advertisement below your article, which says limited period offer of 26% extra gold on first installment with funds India. Can you explain how Reliance is able to promise to credit additional 26% of first installment? Does this mean that there are hidden charges that are not clearly revealed upfront and 26% is a cashback of the larger hidden load/charge pie?

If you can kindly do a comparison of Reliance My Gold Plan vs Reliance Gold Fund vs Gold BEES and show the IRR difference between the 3 then things would be crystal clear for everyone.

Thanks,

Ashwin

Hi Ashwin,

The units are not held in a demat account. The gold is purchased on a daily basis and managed by a independent trustee. They don’t have a secondary trading market.

26% extra is only on the first instalment and only when you opt for a yearly SIP. There are no hidden charges and all the charges are clearly described on the website and FAQ documents.

Since Reliance My Gold Plan is a gold accumulation product, you cannot actually compare it with the other two since they are investment products. It would be tough to do an IRR calculation for Reliance My Gold Plan.

Thanks for the clarification. But I am still puzzled how they can afford to credit 26% into every yearly SIP account, even if it is just calculated on the first installment.

For ex: Take a SIP of 10,000/month. The charge applicable per sip is 1.5% = 150/month.

At the end of the year, net charges = 150 * 12 = 1,800 rs (assuming no other charges and no premature withdrawals).

Reliance promises to credit 26% of 1st installment, which is 2,600 rs.

The numbers don’t add up and there is a net deficit of 800 rs (1800 – 2600) that Reliance has to somehow provide for. If 1.5% is the only charge involved, the cost has to be loaded elsewhere. Can you explain this discrepancy, assuming that Reliance does not load the price of Gold itself to recover its costs?

Thanks,

Hi Ashwin,

Just like many jeweller’s schemes offer a free gold coin or other benefits to their customers, we’re offering 26% extra gold on the first instalment as a promotional offer to celebrate Akshaya Tritiya. This is a marketing expense for us and RMGP. We are proud to undertake this expense as we think this is the best plan currently available in the market to accumulate physical gold. As stated earlier, there are NO hidden charges and all the rates mentioned in the FAQ document of RMGP hold good.

Thanks Vidya, your response clears quite a few concerns.

Your clarification on the product positioning that RMGP is for those who want physical gold and it is probably not the best choice for those who look at gold as a investment or inflation hedge, literally sets things crystal clear.

I am puzzled at how you can conclude this (in your own words) to be “the best plan currently available in the market to accumulate physical gold” without computing the IRR as I requested in my previous post. Where are the data-points for this claim? Articles on this blog (specially by Vidya Bala) are backed by sound reasoning and data-points, but this one seems to be an outlier.

You are not competing with the corner-of-the-street jeweler, when you say “many jeweller’s schemes offer a free gold coin”, are you? We all know how these jewelers offer **free** gold. So the question was how Reliance plans to offer **free** gold. If its offered from FundsIndia’s kitty and is written off as “Marketing expense”, who bears the default risk on 26% promise? FundsIndia? or Reliance?

I am not nitpicking here, I respect FundsIndia, its transparency and standards of disclosure to its Mutual Fund customers. But unfortunately I don’t see the same high standards of transparency and conviction of disclosures when it comes to this particular product. I was not aware of such an offering until I saw the advt’s flashing all over funds India site and mail notifications. Had never experienced such an “in the face” ad campaign from funds India before.

Thanks,

Ashwin,

Just to add to my previous comment, you may, if interested read more details on RMGP here: http://s3-ap-southeast-1.amazonaws.com/fundsindia/LP/Topschemes/images/RMGP+AOF_TERMS+AND+CONDITIONS_Ver-1+5.pdf

thanks

Vidya

Hello Ashwin,

I saw your comments on the blog on this article. While I do not analyse the product, I’d like to step in (and thanks for your complement) to share my understanding of this product with you. First, we do not ask the IRR of a gold product to a bank or a jeweller do we? It is the same here. This is simply a commodity/product you buy. Just that one may say it is a bit more efficient way to buy simply because you get to average the costs. What our team did, though, is compare buying gold coin (on a single day) with a bank and then see the average cost of buying through RMGP and the latter worked better.

Also, pl. note the IRR calculation would kick in only if there is also a cash inflow for you at the end of this product term. In this case it is gold that you get. Hence, the returns finally would depend on the price at which you sell the coin or bar, if you sell it, that is.

Next, it is not the corner street gold jewelers alone who offer gold schemes. Well-known country-wide players too offer it and this product RMGP is perhaps meant to compete with such schemes/products.

As for the ‘free’ offering, 20% is from RMGP. It is a promotional exercise as is the case with many products during festive seasons. the 6% from FundsIndia is indeed a promotional offer from us. The 20% onus is on RMGP and 6% on us. That answers your question on the default risk and who bears it.

Ashwin, if you are looking at gold from an investment angle, I am sure you know where to go – gold funds or gold ETFs is the place. And need I tell you that there are a number of people looking to invest in gold schemes because they WANT GOLD. RMGP caters to such requirement.

The advertisements on Gold flashing in FundsIndia is because it is Akshaya Tritiya season and there is an offer on. Hence the promotion. It will change once the offer is over. Ad campaigns can seem in the face depending on the nature of the product being offered some times 🙂 It is inevitable.

I would just like you to know that FundsIndia has done its bit of due diligence before offering this product and as has always been the case, we seek to offer unbiased services within the products we offer. You will appreciate that RMGP being a non-financial product has not been subject to the regular financial/analytical research that you see us giving with mutual funds on an ongoing basis.

Hope you see this point of view, even if you do not agree 🙂

Appreciate your participation/comments in our blog.

thanks, Vidya

RMGP appeared like an interesting investment option when I came across it few weeks ago. However the documents go to a great extent to say that the price is not comparable. I understand few of their reasons but it makes me uncomfortable as a customer.

Some points in this article are valid but its like comparing apples and oranges – even if you put more data to prove a few scenarios, the future is not guaranteed. If I finally intend to buy jewellery with the gold, I’m sure no jeweller will give the market rate for Reliance’s gold simply because it was not purchased from them.

I’m also worried about the above-normal selling being done by FundsIndia for this scheme. Please refrain from it before you lose the trust of your customers!

Hi Pavan,

The gold offered under this plan is of 24 Karat purity at 995 fineness. If you wish to buy jewellery with the gold you accumulate through the plan, then you must know that the purity of gold offered by RMGP is quite high than the gold you purchase from conventional sources. Hence, you will get rates higher than what you would receive if you would just sell normal jewellery or gold coins. Also, if you consider this an issue, then you will face the same if you buy gold from banks or any other sources.

As an online investment platform, we’ve always strived to ensure that we offer an array of quality financial products to our customers. We’ve always refrained from offering all such products that aren’t feasible for our customers, or are of a sub-standard quality. We have and will always continue to stand by this belief.

Since gold plan is closed now, will Reliance return money or compel customers to purchase gold?

Hello Uttam, Sorry for the delayed response.

Many Gold plans of jewellers are closed as a result of deposit-taking norms of Companies Act. RMGP is not a deposit. It allots gold grams in your name as soon as you buy them. hence it is not closed.

Dear Team,

I am interested in investing in this RMGP Gold ETF SIP. Could you please let me know the requirements (Required inputs for opening this ETF)

Regards,

Sreekanth

hello Sreekanth, RMGP is not an ETF. It is a monthly investment option to buy physical gold by avaraging it every month and getting gold units allotted every month. At the end of the tenure you get equivalent physical gold. With ETF,you don;t get physical gold. You can redeem the cash. If yu want ETFs, you need to have a demat brokerage account.

Why not buy a gold ETF/MF in installments for 12 months and then convert to physical?

The only advantage of this installment system is that it averages the price. Well, that averaging can be achieved in the most cost-effective way by buying a gold ETF/mutual fund. Why would I want to use this plan instead?

And, anyway, averaging is better only half the time in an uptrend while it may be worse off in a downtrend. So, on average, over all customers and and over all trends, what difference does it make? Furthermore, the price risk within a year is not the predominant risk when the investment is for a long time horizon (of many years/decades).

And, what possible advantage is there in averaging daily within a month? That makes no sense whatsoever. The finance industry needs to stop spreading stupid ideas like daily averaging as if it is better.

Comparison with jewellers only doesn’t make sense. One can buy physical gold from banks and one can hedge future price risk with gold futures, ETFs, so any plan being offered by the financial industry needs to take these other avenues into account.

The main risk here is Reliance’s daily price which is not an industry-wide benchmark or an exchange price. Why is it not some exchange price + overhead? Reliance gets the benefit or knowing how much future purchase it needs to make (as people sign up for a plan in advance) so it can hedge future purchases or ensure that the supply is consistent so why does it not benchmark the price to the exchange/futures price with a fixed overhead?

Hello Vivek,

the discussion here is not to comapre ETF with RMGP. RMGP is to be purely viewed as a substitute for physical gold. it has allt he traits of physical gold purchase, except that it is more transparent and more efficient (online). As for averaging, compared witht he last price at which a jeweller gives, averaging has proved to work better. If averaging is better only half the time, then even SIPs in mutual funds should not be working right? But they work and work very well. We have also compared buying bulk purchase with bank versus averaging and the latter has worked better.

We are not talking of those using exchanges/ futures to buy gold. We are talking of lay people entering into jewellery schemes that are far riskier and opaque. Yes, pricing will not be the same gold landed price because we are talking of various other state taxes as well as transportation here. Yes, for investment purpose and for those who do not need physical gold, ETfs are good.

“the discussion here is not to comapre ETF with RMGP”

why not?

I think you don’t understand averaging. You did not address any of my points.

“We are not talking of those using exchanges/ futures to buy gold. ”

That is precisely my point. Why are you not talking about those avenues too? You should be.

“Yes, for investment purpose and for those who do not need physical gold, ETfs are good.”

I explained that you can convert your ETF holding with physical gold periodically if one so wishes. Again, you did not understand my point. Too bad.

Vivek, I am afraid, you have to first diferentiate between investing in gold and buying gold. RMGP is first a plan to simply buy gold in an efficient way. That is all. If you wish to talk about the other avenues (commodities etc), this is not the forum since we do not deal with them nor are they comparable. Nobody compares buying gold in a bank or jewellery shop with buying ETF or commodity futures. That is the same difference.

As for ETFs to gold…you need to be a HNI with KGS of gold to do that. we are talking of retail investors here.

“If averaging is better only half the time, then even SIPs in mutual funds should not be working right?”

Can you tell me which SIP plan talks about averaging WITHIN a month?

Hello Vivek, This is a gold plan that does averaging 20 days a month. So it is WITHIN a month. And not every averaging within the month will even out itself. Vidya