After a couple of European fund-of-fund launches in January 2014, and one fund house changing its existing fund strategy to invest in Europe, it is now the turn of Franklin Templeton India to launch a feeder fund that will invest in the European growth story.

The Franklin stable, which is not known to come up with NFOs too often, clearly sees a need to diversify its international fund offerings to investors through this European fund. The new fund called – Franklin India Feeder – Franklin European Growth Fund will invest in the parent fund called Franklin European Growth Fund. The NFO will close on May 9, 2014.

Why Europe?

If you wish to diversify your portfolio beyond Indian shores, then there may be a few reasons why Europe could be a part of your diversification strategy:

– As a region, the European Union is the largest economy. Europe accounts for 24% of the world’s GDP. Its sheer size means that it cannot be ignored.

– Europe also accounts for 23% of the world’s market cap. India, in contrast, accounts for just 2%.

European companies are known to be export-oriented. Europe’s exports as of September 2013 was $7032 billion as against North America’s $2001 billion. That means Europe’s growth story is not merely internal. It gains from other countries’ growth as well.

– Correlation between Indian markets and Europe (MSCI India and MSCI Europe) was between 0.4 to 0.45 in the last 1,3,5,7 and 10 year time frames, suggesting that Europe could be a good market to diversify when you hold an Indian portfolio.

– The above low correlation is evident in the performance of these markets. In 2011, when Indian markets fell 38%, Europe fell less than 14%. In 2013, when Indian markets lost 5.3%, Europe delivered a good 22%. Of course, in good years for India such as the one in 2012, Europe underperformed India.

Why Now?

– Europe was much slower than the US in terms of recovering from the financial crisis in 2008. While earnings of companies in Europe declined by 2-2.2% in 2010 and 2011, it rebounded to 7.2% in 2013.

– Similarly, the huge debt in the books of European companies also steadily declined in 2013.

– While the valuation in US markets quickly factored the improvement and rallied, European markets’ Price to Earnings Ratio still remains below their 15-year averages.

– As a result, the dividend yield of European stocks (MSCI Europe) at 3.4% is higher than the US’ S&P 500 yield of 2%.

– Sectors such as technology and financials which have rallied in the US are still available at lower valuations. For instance, the price to book value of technology stocks is still 23% lower than their 15-year averages, while it is 33% lower in the case of financial stocks.

The Fund

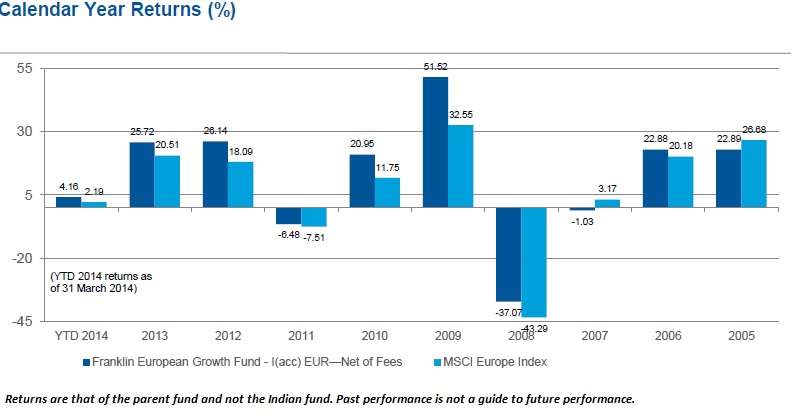

Franklin India Feeder – Franklin European Growth Fund will invest in the parent fund. The latter has been in existence since 2000 and has delivered over 20% annualized returns in the last 5 years, comfortably beating the MSCI Europe Index.

Consumer discretionary, industrials and financials were among the top sector exposures. UK, Netherlands, France and Switzerland are among the top countries the fund is exposed to. Given the persisting troubles with emerging Europe and the bounce back in the developed European markets, the exposure appears to be a balanced one.

Currently, JP Morgan, Religare Invesco and DWS are the fund houses offering exposure to European markets through the feeder route. You can read our call on these funds by clicking here.

Our comparison of the parent funds in the above schemes suggests that Franklin European Growth, with a longer track record, has also delivered superior returns over a 5-year time frame, when compared with other parent foreign funds.

Suitability

If you are looking to diversify into international markets, funds taking exposure to developed markets and markets less correlated with India – such as US and Europe – may present good options.

While these markets may not deliver as much in the long term as emerging markets such as India would, they may help curtail volatility; such as the present one in India since 2008. If you are trying to take a call between US and Europe; US might seem a bit expensive at this stage.

That said, we would still say that both US and Europe could complement each other well in your portfolio. While US could offer exposure to new-fangled sectors and themes that may enjoy the first wave of re-rating, Europe could provide exposure to well-established companies with sound balance sheets that may not be available at a similar scale in India.

If you decide to have say a 10% exposure to international funds, then you could consider an equal exposure to both regions. Do note that although investing in equities, international funds will be treated like debt funds for tax purposes alone.

Also, any appreciation in the Indian rupee against foreign currencies such as the euro or the dollar may pull down the returns of such funds. To this extent, there is a currency risk involved in these funds. However, for those building a portfolio for spending in foreign currency – such as children’s education in Europe, this could be a good currency hedge strategy.

Disclaimer: Past returns are not indicative of future performance.