If you are still scouting for safe tax-free options, then you will have time till March to choose one. But the current crop appear to offer attractive rates, thanks to the high gilt yields prevailing at present.

After public sector companies like NHAI and IRFC raised money through tax-free bonds, it is now the turn of the Indian Renewable Energy Development Agency (IREDA) to come up with its first public issue of tax-free bonds.

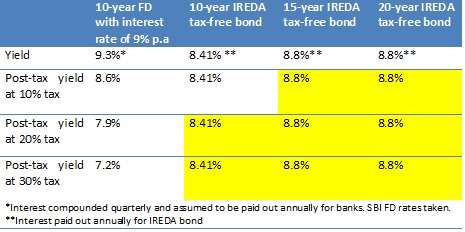

With rates of 8.41%, 8.8% and 8.8% for 10, 15 and 20-year tenures respectively for retail investors (those who invest upto Rs 10 lakh in the bond), IREDA’s yields will compete with FD rates. The issue also has a AAA (SO)-rating from rating agencies CARE and Brickwork Rating India.

The offer, open from February 17 to March 10, may be closed in advance or extended, based on the subscription response.

About IREDA

IREDA is a non-banking financial institution registered with RBI and is a Govt. of India undertaking. It is engaged in extending financing to projects and schemes for generating electricity and energy through renewable sources and conserving energy through energy efficiency.

For funding projects, the company has various sources of financial support – including banks, private placements of debentures and loans from international funding agencies.

Besides, the Govt. of India also infuses equity capital and provides budgetary support for IREDA.

Renewable energy projects typically funded are in hydro power, wind, biomass and solar segments, with wind power accounting for maximum lending.

While renewable energy projects are known to have either delays in execution of projects or uncertainties in repayment, IREDA has done well to reduce its non-performing assets through better monitoring and control.

It has also resorted to consortium/co-financing of large projects, thus reducing its risk.

While loans disbursed have been growing at a healthy pace, IREDA’s net NPAs have come down to 0.92% for FY-13 as against 2.5% for FY-12.

For the year ended FY-13 revenue from operations, primarily consisting of interest income from lending was Rs 719 crore as against Rs 520 crore in the previous years. Net profits after tax was Rs 202 crore in FY-13 compared with Rs 173 crore in the previous year.

What are tax-free bonds?

Tax-free bonds are non-convertible debentures on which the interest income does not suffer tax throughout the tenure of the bond. There is no tax benefit (such as 80C) on the principal. Most debt options, barring the PPF and EPF suffer tax on the interest component. Your FDs, post office schemes and corporate deposits are no exceptions.

The coupon rate of the tax-free bond is actually the post-tax return for you. This makes these classes of bonds attractive for most tax payers.

Added to this, government security yields have seen a rise after the recent hike in interest rate by RBI. As a result, long-term bond yields are high, providing scope for you to lock into them using these bonds.

The table below illustrates how IREDA bonds score over fixed deposits. For those in the 20% and 30% tax bracket, even a 10-year bond remains attractive. For those in the 10% tax bracket, the tax-free bond rates are attractive in the 15-year tenure.

It is noteworthy that these bonds are suitable for those looking for a regular flow of income from the bond. There is only an annual interest pay-out option and no cumulative option.

Hence, this instrument is not for building long-term wealth, unless you prudently reinvest the interest in other investment options as soon as you receive the money.

Firstly I would like to know your views of using Tax-free bonds to year income for my wife who is a housemaker. Interest (Ist generation) on amount gifted to my wife who invests in Tax-free bond will be taxed in my name. since these are tax-free there will be no addition tax for me. The interest received from Tax-free bonds, if invested in FDs, the interest on FDs will be taxed to my wife (being a 2nd generation income). This I feel is a legitimate way of taking advantage of the lower IT limit of spouse who has no other sources of income.

Secondly please advise as to what would be the optimum rate for purchase/ accumulate Tax-free bonds from secondary market to built my wife’s income.

I shall be grateful for your suggestions and comments

Regards

Venkat

Hello Venkat, as long as you have sought your auditor’s advice on this tax planning, it’s fine. We do not have secondary market recommendations for bonds. Besides liquidity issues, pricing risks as a result of yield changes makes it risky for retail investors in our opinion, unless they can track them and buy at the right time. thanks, Vidya

Thanks for the Great!~ advice. I have Demat account so I can invest in the Tax Free Bonds but how can my wife who doesnt have a Demat account invest in the same

hello Anurag, You can check with other offline distributors. But in genral. holding in electronic form is the future and is convenient as well as safe. thanks

Vidya

Can we do secondary market bond purchases through Funds India?

Hello Ram, If you have a demat account with FundsIndia. you can buy bonds in the secondary market. We do not have calls but you can use the plaform to execute transactions you want. thanks, Vidya

Do these tax free bonds pay devidends yearly or just one lump sum at the time of maturity? How to calculate the exact final maturity amount?

Hello hari, Interest (not dividends) are paid out annually. There is no other option. Maturity amount is only your principal amount as interest is paid out every year. thanks, Vidya

Thank you for the clarificatin and correcting my terminology 🙂

hi vidya

Pls tell me at the time of liquidation of said company or if the company faces losses or at time of gross or net npa’s going high how is our money secured with govt bonds as far as i know nhai and pfc amd nhb are good companies but how about ireda and enmore port bonds , crisil has given aaa rating to ireda . but how it is safe for the principal and interst thAT COMES TO US.

Pls tell me at the time of liquidation of said company or if the company faces losses or at time of gross or net npa’s going high how is our money secured with govt bonds as far as i know nhai and pfc amd nhb are good companies but how about ireda and enmore port bonds , crisil has given aaa rating to ireda . but how it is safe for the principal and interst thAT COMES TO US.

hello Ravi, being govt. cos. you have sovereign guarantee for repayment. thanks, Vidya

Vidya

Can we do secondary market bond purchases through Funds India?

Hello Ram, If you have a demat account with FundsIndia. you can buy bonds in the secondary market. We do not have calls but you can use the plaform to execute transactions you want. thanks, Vidya

hi vidya

Pls tell me at the time of liquidation of said company or if the company faces losses or at time of gross or net npa’s going high how is our money secured with govt bonds as far as i know nhai and pfc amd nhb are good companies but how about ireda and enmore port bonds , crisil has given aaa rating to ireda . but how it is safe for the principal and interst thAT COMES TO US.

Firstly I would like to know your views of using Tax-free bonds to year income for my wife who is a housemaker. Interest (Ist generation) on amount gifted to my wife who invests in Tax-free bond will be taxed in my name. since these are tax-free there will be no addition tax for me. The interest received from Tax-free bonds, if invested in FDs, the interest on FDs will be taxed to my wife (being a 2nd generation income). This I feel is a legitimate way of taking advantage of the lower IT limit of spouse who has no other sources of income.

Secondly please advise as to what would be the optimum rate for purchase/ accumulate Tax-free bonds from secondary market to built my wife’s income.

I shall be grateful for your suggestions and comments

Regards

Venkat

Hello Venkat, as long as you have sought your auditor’s advice on this tax planning, it’s fine. We do not have secondary market recommendations for bonds. Besides liquidity issues, pricing risks as a result of yield changes makes it risky for retail investors in our opinion, unless they can track them and buy at the right time. thanks, Vidya

Thanks for the Great!~ advice. I have Demat account so I can invest in the Tax Free Bonds but how can my wife who doesnt have a Demat account invest in the same

hello Anurag, You can check with other offline distributors. But in genral. holding in electronic form is the future and is convenient as well as safe. thanks

Do these tax free bonds pay devidends yearly or just one lump sum at the time of maturity? How to calculate the exact final maturity amount?

Hello hari, Interest (not dividends) are paid out annually. There is no other option. Maturity amount is only your principal amount as interest is paid out every year. thanks, Vidya

Thank you for the clarificatin and correcting my terminology 🙂

Pls tell me at the time of liquidation of said company or if the company faces losses or at time of gross or net npa’s going high how is our money secured with govt bonds as far as i know nhai and pfc amd nhb are good companies but how about ireda and enmore port bonds , crisil has given aaa rating to ireda . but how it is safe for the principal and interst thAT COMES TO US.

hello Ravi, being govt. cos. you have sovereign guarantee for repayment. thanks, Vidya