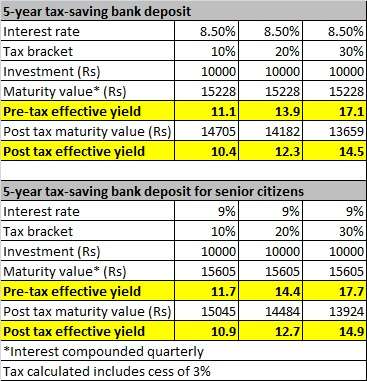

It’s the tax-saving season and one of the popular tax-saving instruments – the five-year tax-saving bank deposit – is being promoted by banks. A major public sector bank has been prominently advertising its five-year tax-saving deposit, stating yields of 16.64 per cent pre-tax, for regular investors and 17.39 per cent for senior citizens. The rates of interest on these are 8.5 per cent and 9 per cent respectively.

The pre-tax magic

How can an 8.5-percent-a-year interest-generating deposit deliver almost twice the return? Are their claims valid?

Well, they are; only it does not give the full picture. The said advertisement bumps up your returns by considering the tax you save but totally ignores the tax that your interest income will suffer. In other words, it considers the benefit and stops there at a pre-tax stage to make the returns attractive.

Let us take an example to see how this is done: If you invest Rs 10,000 in a five-year deposit that returns 8.5 per cent a year (compounded quarterly) then you will have Rs 15,228 at the end of five years. But remember, in the first year you save taxes to the extent of Rs 3,090 (30% of Rs 10,000 plus 3% cess), if you are in the 30% tax bracket. Therefore your net cash outflow in the year of investment is taken to be Rs 6,910 (10,000-3090).

Lower returns post tax

The effective pre-tax yield is therefore about 17.1 per cent {(15,228/6910)^1/5}. But did you know that the interest of Rs 5228 suffers income tax? Interest income from deposits are treated as ‘income from other sources’ and taxed. So if you are in the 30% tax bracket, you will have a tax burden of Rs 1615, including 3% cess. Net of this, your maturity value is only Rs 13,613 (Rs 15,228-1,615). So the yield comes down to 14.5 per cent.

The return comes down if you are in the lower tax bracket of 10 per cent. Why? Because you enjoy only Rs 1,030 (10% of Rs 10,000 plus cess) as tax saved, instead of Rs 3,090. See table below to know, the actual post tax yields for those in the 10%, 20% and 30% tax bracket.

And remember, if you are a senior citizen, you may well be in the lower tax bracket, which means that your benefits post tax are definitely much lower than what the advertisement claims; although you may receive a slightly higher rate of interest.

Hence, you would do well to take the claims of ‘high yield’ advertisements with a pinch of salt.

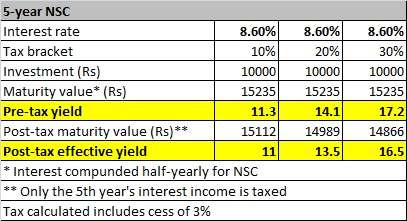

The humble NSC

That said, are there any other debt options with similar maturity at this juncture that would provide tax-saving under Section 80C and also deliver good yields post tax?

As seen in the table, both regular investors and senior citizens can earn superior post tax yield if they invest in NSC. This is because, the interest on NSC, although taxable, is treated as reinvested every year under Section 80C and is therefore allowed as deduction. As a result, only the last year’s interest is actually taxed.

In contrast, interest on a bank tax-saving deposit is taxed entirely.

Hence, if you are a tax payer and can take a five-year lock-in, NSC’s current rate (applicable only up to March 2013) is attractive from a post tax perspective.

Madam,

Are interest on Recurring Deposits Taxed?

Hello sir, Interest on recurring deposits is indeed taxable under the head ‘income from other sources’. While banks do not deduct TDS, the responsibility to pay self-assessment tax before filing returns rests on the investor. Many investors think it is tax free because TDS is not deducted by the bank. In fact, even the interest on your saving bank account balance is taxable, although there is no TDS deducted. In all these cases, PAN no. acts as the link for any tracking purpose by IT authorities. – Tks, Vidya

Vidya,

Thanks for the nice article. Have 2 questions :-

1) Any reason why there in no TDS in case of Recurring Deposit as compared tp normal FD. Any logical reasoning behind that.

2) You mentioned”in NSC , the interest in reinvested every year “. I guess it also happens in case of FD right (Compound Interest ) or is it that in case of NFC, we can claim deductions on the interest component.

Hi Rohit, Thanks for raising pertinent questions.

1. There are no specific reasons. For savings channels like RD and your savings bank account, banks are not required to deduct TDS. So that is how it stands. These are also often used by people who do not fall under tax bracket but may not be savvy enough to submit form 15H/15G etc. Hence, to save them the pain of deduction and later claiming exemption (which is not possible if they do not have a PAN or are not tax assesses), such a practice may be in vogue.

2. You are right that interest of 5-yr FD is compounded and hence stays there. But currently, such a clause for claiming deduction on reinvestment is available only for NSC. There is no explicit clause to claim them as exemption for 5-year FD. In fact, banks deduct TDS annually on the interest accrued if it exceeds Rs 10,000 per annum (unless one provides form 15H or 15G if they are not taxable). This, in one way, appears to suggest that the interest income is taxable. – Tks Vidya

Hi Vidhya,

This article gave me a good clarify of how Tax Saver in Banks & NSC in Post Offices.

Thanks,

Lakshmanan.

Hi Vidhya,

Thanks for your information.

I have one doubt — what is the more beneficial to invest in NSC or in 5year Bank FD , both in I-Tax point of view as well as investment point of view.Please note I am in 10% tax bracket.

Your early reply will be great.

Regards

Jayanta

Hello Jayanta,

Srikanth from FundsIndia here. Vidya is on leave presently.

Both NSC and Bank FD provides an interest of 8.5%. The return is taxable from both NSC and the Bank FD’s. The only advantage with FD is that the interest can be taken as a pay out, where in NSC, the interest gets accumulated and paid out after the maturity. If you are looking from I-Tax angle, it is advisable to invest in a PPF, even though the investment period is 15 years, the returns are tax-free. The returns varies from 8-9% per annum. This is advisable if you are risk averse investor. If you would like to take some risk, we strongly recommend you to invest in ELSS schemes available in mutual funds comes with the lock-in period of 3 years. There are few funds like franklin india tax shield, icici pru tax saver etc., that have delivered a decent return and the returns are completely tax free.

Hope this helps.

Thanks,

Srikanth

Hi Vidhya,

Thanks for your information.

I have one doubt — what is the more beneficial to invest in NSC or in 5year Bank FD , both in I-Tax point of view as well as investment point of view.Please note I am in 10% tax bracket.

Your early reply will be great.

Regards

Jayanta

Hello Jayanta,

Srikanth from FundsIndia here. Vidya is on leave presently.

Both NSC and Bank FD provides an interest of 8.5%. The return is taxable from both NSC and the Bank FD’s. The only advantage with FD is that the interest can be taken as a pay out, where in NSC, the interest gets accumulated and paid out after the maturity. If you are looking from I-Tax angle, it is advisable to invest in a PPF, even though the investment period is 15 years, the returns are tax-free. The returns varies from 8-9% per annum. This is advisable if you are risk averse investor. If you would like to take some risk, we strongly recommend you to invest in ELSS schemes available in mutual funds comes with the lock-in period of 3 years. There are few funds like franklin india tax shield, icici pru tax saver etc., that have delivered a decent return and the returns are completely tax free.

Hope this helps.

Thanks,

Srikanth

Vidya,

Thanks for the nice article. Have 2 questions :-

1) Any reason why there in no TDS in case of Recurring Deposit as compared tp normal FD. Any logical reasoning behind that.

2) You mentioned”in NSC , the interest in reinvested every year “. I guess it also happens in case of FD right (Compound Interest ) or is it that in case of NFC, we can claim deductions on the interest component.

Hi Rohit, Thanks for raising pertinent questions.

1. There are no specific reasons. For savings channels like RD and your savings bank account, banks are not required to deduct TDS. So that is how it stands. These are also often used by people who do not fall under tax bracket but may not be savvy enough to submit form 15H/15G etc. Hence, to save them the pain of deduction and later claiming exemption (which is not possible if they do not have a PAN or are not tax assesses), such a practice may be in vogue.

2. You are right that interest of 5-yr FD is compounded and hence stays there. But currently, such a clause for claiming deduction on reinvestment is available only for NSC. There is no explicit clause to claim them as exemption for 5-year FD. In fact, banks deduct TDS annually on the interest accrued if it exceeds Rs 10,000 per annum (unless one provides form 15H or 15G if they are not taxable). This, in one way, appears to suggest that the interest income is taxable. – Tks Vidya

Madam,

Are interest on Recurring Deposits Taxed?

Hello sir, Interest on recurring deposits is indeed taxable under the head ‘income from other sources’. While banks do not deduct TDS, the responsibility to pay self-assessment tax before filing returns rests on the investor. Many investors think it is tax free because TDS is not deducted by the bank. In fact, even the interest on your saving bank account balance is taxable, although there is no TDS deducted. In all these cases, PAN no. acts as the link for any tracking purpose by IT authorities. – Tks, Vidya

Hi Vidhya,

This article gave me a good clarify of how Tax Saver in Banks & NSC in Post Offices.

Thanks,

Lakshmanan.