Whenever you are looking for funds to invest and look at the performance screen of a fund, the 1-year returns is the number that registers and also influences decision. There are two problems with this: One, the returns are taken at a specific point in time. Two, one year is too short a time period to evaluate most funds (barring short term debt funds). We’ve written about the perils of point-to-point returns. Here, we’ll show you how short-term returns can distort the bigger picture.

The past year has been full of lessons. If you got carried away by how equity and debt markets have been behaving in prior periods, 2018 served as a reality check. This year gave a number of examples to demonstrate why short-term returns are not sufficient to evaluate or understand fund characteristics. So let us look at how picking funds based on 1-year return could have impacted your portfolio.

Picking chart toppers

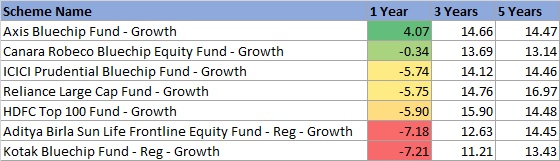

As the good old largecap category which invests in stable blue-chip companies dived into the negative zone, investors became picky. At this time, there were a few funds which managed to come out shining, not just by managing to contain losses, but also by generating decent returns. One such example is Axis Bluechip fund. When such funds outshine the category, they immediately get all the limelight. This is one of the problems with 1-year returns. Below is a table which has Axis Bluechip against a few other consistent and popular funds.

Returns as of 23rd Jan 2018

Returns as of 23rd Jan 2018

You can see that the one year outperformance of Axis Bluechip doesn’t reflect in its long term performance. Over 3 & 5 year periods, it is pretty close to the average. While Axis Bluechip indeed stood out for its performance in 2018, we cannot conclude that it is the best fund to invest in.

Funds have to be evaluated based on multiple criteria including long term returns, volatility, ability to contain downsides and so on. This does not necessarily mean that funds with high 1-year return may not perform well. But that is not the only measure to see if a fund is good enough to stay invested in the future. We’ve talked about picking specific funds here. Can this behaviour be extended to a category of funds?

Picking and dropping mid-caps

Yes, 2017 was a year where everyone wanted midcaps in their portfolio. And as the next year saw the scenario reverse, midcaps were no longer preferred. Investors go back and forth with their choices as they see returns swing. This can significantly impact the eventual returns you get from your portfolio. For example, if you had entered in 2017 looking solely at past returns and exited in panic in 2018 when you saw the returns falling, you would have booked losses.

| Average returns on Midcap funds (%) | ||||

|---|---|---|---|---|

| 2018 | 2017 | 2016 | 2015 | 2014 |

| -11.38 | 42.40 | 3.20 | 7.16 | 69.40 |

The table shows the calendar year returns of midcap category over the last 5 years. We can see how divergent the returns are. This is the reason why we regard mid-caps as risky and ask investors to have at least a 5-year period in mind while investing in them. Given how volatile they are, it is very difficult to stay with them only during strong rallies and exit when they start falling. Like in the example, investors try to get in and get out based on short term returns.

While the 1-year return at the end of 2018 was -11.39%, 5-year return for the same period was 13.29% annualised. For someone who invested 5 years back, this fall didn’t do much damage. In fact, someone running SIPs during the fall will benefit immensely when the midcaps take an upward turn again.

Being influenced by 1-year return can cost you a lot if that is all you look at. Similar examples can be taken for investors who got into the momentum rally of dynamic bond funds which gave double digit returns in early 2017 and dipped into negative in 2018. If you simply hold for 3 years or more, the funds will likely stabilise into giving you returns expected of that category. Wherever a longer holding period is warranted, you should not let short period returns decide your investment choices.

Am Currently having 5 SIPs each of 1000 for 60 installments (5 years)…

1) ICICI Pru Bluechip Fund(G)

2) SBI Small Cap Fund-Reg(G)

3) L&T Midcap Fund-Reg(G)

4) Motilal Oswal Multicap 35 Fund-Reg(D)

5) Mirae Asset India Equity Fund-Reg(G)…

What are the taxes I need to pay after 5 years when withdrawing??

Awaiting the early reply.

Thanks in Advance.

Sai

Hi,

It is not possible to calculate in advance the tax to be paid. Equity fund returns are not predictable. Tax to be paid depends on your capital gain, which is decided by your fund’s returns.

Thanks,

Bhavana

Am Currently having 5 SIPs each of 1000 for 60 installments (5 years)…

1) ICICI Pru Bluechip Fund(G)

2) SBI Small Cap Fund-Reg(G)

3) L&T Midcap Fund-Reg(G)

4) Motilal Oswal Multicap 35 Fund-Reg(D)

5) Mirae Asset India Equity Fund-Reg(G)…

What are the taxes I need to pay after 5 years when withdrawing??

Awaiting the early reply.

Thanks in Advance.

Sai

Hi,

It is not possible to calculate in advance the tax to be paid. Equity fund returns are not predictable. Tax to be paid depends on your capital gain, which is decided by your fund’s returns.

Thanks,

Bhavana