Synopsis

- Point-to-point returns do not show whether the fund is able to consistently do well

- Point-to-point returns do not show volatility in returns or performance in different market cycles

- It is not possible to understand fund strategy and thus suitability from point-to-point returns

- Return expectations based on 1-3-5 year returns would be erroneous

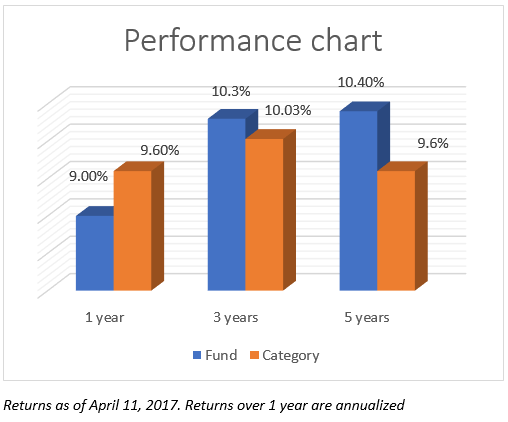

Today, the 1-year return of BNP Paribas Midcap looks to be among the best at 40%. L&T India Value sports a 1-year return of 31.7%. On a 3-year basis too, BNP Paribas Midcap has higher returns than L&T India Value. So is BNP Paribas Midcap a better fund than L&T India Value? The instinctive answer would be yes, for most investors.

Consider the 1-year returns for the two funds on 12th December 2016. BNP Paribas Midcap’s return was 6.4% while L&T India Value sported a 17% 1-year return. On a 3-year return basis, BNP Paribas Midcap undershot L&T India Value’s return by 5 percentage points. Or take the 5-year returns today. BNP Paribas Midcap is marginally lower than L&T India Value. Would you revisit the answer to the question above?

The answer is that you do not use the 1, 3, and 5-year returns alone to base decisions. These returns neither offer sufficient information for you to choose funds nor are they the right benchmark to set your future return expectations. These returns, when displayed anywhere, are point-to-point – that is, they are returns from a single day to a single day. Looking at just the 1, 3, and 5-year return gives a limited idea of a fund’s performance. There are four aspects to these point-to-point returns.

One, returns change on a daily basis. If markets – whether debt or equity – change every day, so too would the NAV. Therefore, fund returns would also keep changing. 1-year return for HDFC Midcap Opportunities, for example, leaped from 32.4% on 20th November 2017 to 37.2% the next day. ICICI Prudential Balanced went from a 1-year return of 25.4% on 24th November 2017 to 20.8% just five sessions later.

In a rising market phase, the trend of returns would be upward and vice versa. Most mid-cap/ small-cap funds for example were clocking losses or low single-digit returns on a 3-year basis throughout 2013. In the rally the following year, average 3-year returns were upwards of 15% by mid-2014 and rose beyond 25% towards the end. Similarly, average 5-year returns for large-cap and diversified funds crashed from 50% plus at the start of 2008 to less than 15% by the end of 2008 after stock markets sank that year.

Besides, it is not just market movements that affect fund NAVs. Fund portfolios also play a role. In the short term, stocks move higher or lower depending on news flows. The impact these movements have on NAVs depends on the extent to which they hold that stock. Funds holding a heavier weight in Infosys such as HDFC Top 200, for example, felt the 13% plunge in the share’s price on the day its CEO resigned in August more than those that held a smaller weight. In dynamic bond funds, those that are more aggressive on duration, such as Aditya Birla Sun Life Dynamic Bond are sporting much lower returns today than those that are either less aggressive, such as UTI Dynamic Bond, or have aligned their portfolios towards an accrual strategy, such as Kotak Flexi Debt.

Two, returns can be influenced by what takes place either on the start date or the end date. If markets were down on the start date, the returns may look higher and vice versa. Dynamic bond funds are an example. With gilt yields falling, especially towards the last few months of 2016, the bond price rally sent the 1-year returns of these funds as high as 15-16%. Gilt funds had even higher returns. But concerns over inflation, exchange rates, and sell-offs, bond yields have been creeping up. Therefore, the 1-year return today for these funds is just about 3%. A sharp fall in bond prices today when taken against a high bond price last year was partly responsible for the stark differential in returns.

This base effect holds true for funds that have begun to slide in performance (which pulls returns lower) or begun to improve performance (which pushes returns much higher). For example, among the best-performing mid-cap funds this year with a 51% 1-year return is IDFC Sterling Equity. The fund had been languishing in the lower quartiles for years before a fund manager and strategy change in April 2016 turned things around.

Three, point-to-point returns ignore events that transpired between the two dates. In other words, the returns don’t show what happened over a period of time. They only show what happened on a particular day. For longer timeframes such as 5 years or even 3 years, when especially equity markets go through phases, the return does not show the returns volatility in the years between the two dates considered. The current 5-year return for equity funds does not show that markets spent 2013 first correcting and then moving sideways, does not show that large-cap indices and funds corrected in 2015, does not show that there were some months in 2016 and 2017 where almost all funds clocked losses on a 1-year basis.

Four, the returns of different periods are not comparable. It is not possible to compare the returns of different periods with each other and draw any sort of conclusion. It would be wrong to look at equity fund returns today and conclude that a 1 year holding period would yield more than a 3 year or 5 year period. Because returns change each day and they are influenced by what was happening both on the two point-to-point dates, the 1 year return may sometimes be higher than the 3 year or the 5 year return may be higher than the 1 year and so on.

For large-cap equity funds, at this time in 2016, the 1-year return was lower by around 6 percentage points lower than the 3-year return which was in turn equal to the 5-year return. The picture is the opposite today. For dynamic bond funds, the 1-year return is around 1-3% today while the 3 and 5 year returns are around 8-9%. Last year, the 1-year return was the highest at about 13-14% which was much better than the 10-12% of the 3 year and 5 year periods.

What we are trying to say? That merely looking at the 1 year, 3 year, and 5 year returns will give you the wrong picture of a fund.

- It does not show whether the fund is able to consistently do well. For a fund to be good, the trend of indentifying securities that deliver a higher return than the benchmark (and peers) should be sustained. This understanding will not come through by looking at 1, 3, and 5 year returns in isolation – it does not show whether the fund has done well on any day in any year instead of just that single day. What are the chances that you invested in the fund on that one day it did well? What would have happened if you had invested on other days? As investing in a fund can be done on any day, you would need that fund to deliver market and category beating returns no matter when you invested. That comes about only if a fund is consistent which cannot be judged by just the 1-3-5 year returns.IDFC Sterling Equity, for example, looks strong today but it has begun to do well only this year. In earlier years, the fund lagged both the Nifty Midcap 100 index and the peer average; even as recent as January 2017, the fund trailed the index on a 1-year return. Similarly, the 1-3-5 year returns may look like a fund is not doing well now, but the fund could in fact be a good and consistent performer in earlier years. Though this could mean something is wrong with the fund, oftentimes it is the strategy that can cause shorter term slips. In such a case, it would be premature to exit the fund based on relatively lower 1 or 3 year returns. ICICI Prudential Value Discovery is a good example here. The fund’s move into contrarian sectors and stocks which are out of favour now pulled down returns. But the fund’s strategy is to discover under-valued stocks in order to gain from a rerating later and thus it is actually doing its job. Looking at its returns in earlier years will tell you that it has, in fact, usually been able to deliver returns above category and benchmark.

The 1-3-5 year returns also do not tell whether the fund is volatile – that is, are its returns prone to swinging widely higher or lower or are they steadier? A more volatile fund requires a higher risk appetite. Funds with lower volatility are also those that eventually deliver better returns over the longer term.

- It does not show fund strategy. And this strategy may require a different risk level from you as an investor. As seen with ICICI Prudential Value Discovery, the 1-3-5 year returns do not show what kind of strategy the fund follows. A fund following a growth-oriented strategy would today show better returns than one with a value-driven one. A value fund requires a longer holding period and a higher risk level. A fund with a higher mid-cap allocation may be doing better today than one with a lower mid-cap allocation, but such a fund may not be a good fit for all.It holds true for debt funds too. Franklin India Ultra Short-term Bond shows returns of 8-9% across the three timeframes, but this does not show that the higher returns are because its portfolio is made up far riskier instruments than a fund like Aditya Birla SL FRF or ICICI Prudential Flexible Income Plan. An income fund such as HDFC Medium Term Opportunities may seem sedate in terms of returns but the fund’s steady strategy of investing only in top-rated instruments may be the best option for those simply looking for FD-plus returns.

- It is not a return indicator. What often happens is that recent returns are taken to as return expectations. As explained above, given that returns change every day, basing expectations on past returns is hardly right. Low returns may give way to higher returns or vice versa. Using past returns are especially dangerous for sector funds as high 1-year returns usually means that a good part of the sector uptrend is already captured.

So how do you get around the bias of 1-3-5 year point to point returns? It can only be done by looking at these returns over a period of time – across market phases, in different quarters, in different calendar years. Only then would there be a more balanced view of a fund’s performance.

How we use returns

At research, we don’t look at the point-to-point returns. What we use are rolling returns – i.e., we take returns of different periods ( 1 year, 3 years) and roll them every day for a number of years. Pitching these returns against the benchmark indices or peers will give the answer to a fund’s consistency in delivering higher returns. Because fund strategies play a key role in returns, we may be willing to let near term underperformance slide if the strategy is such that it can play out well and if the fund has earlier been consistent. In the same vein, a fund that has just started outperforming may require some more time to judge sustenance of its performance.

We average out these rolling returns so that we’re able to arrive at a more realistic return figure that considers both market phases and the effects of a fund’s strategy. So a fund with a higher average return would place better. We also use returns to look at volatility, incidences of losses, and the ability of the fund to keep them in check because recovering from steeper losses takes more effort. We see returns in different market cycles (whether in debt or in equity) to judge its ability to perform no matter what is happening in the markets.

Given the ongoing uncertainty and valuation worries in equity markets and on the interest rate front for debt markets, the 1-3-5 year returns in each category can be quite divergent. It’s important not to get unduly influenced by the simple returns and pick a fund that may not suit your appetite or purposes. This is why some of the funds we pick at research may not be the 1-3-5 year return chart busters.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.

{kind=link}