For most investors, mutual funds mean investing in equities and therefore come tagged with risks.

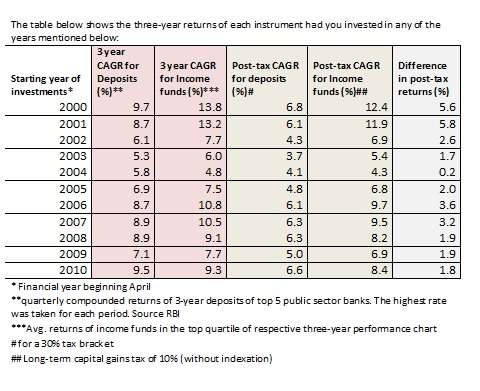

Given this, for a risk-averse investor, there may be little choice left than to invest in plain vanilla bank fixed deposits. But did you know that a three-year deposit that you invested in 2010, for example, would not beat inflation (post tax), when you receive the maturity amount out in 2013? (Please see table below for returns).

What if you had a similar debt product that can deliver returns superior to fixed deposit returns and beat inflation? Would you not consider that?

If you are investing for not less than two years, then ‘income funds’ a class of debt mutual funds can deliver superior returns compared with bank deposits. That means you can earn a bit more than traditional debt avenues, by still staying invested in debt.

What are income funds and what makes them attractive?

Income funds

Income funds are a class of debt mutual funds that invest in a combination of government securities, certificates of deposits, corporate bonds and money market instruments. They are managed by expert fund managers who actively try to manage the portfolio based on interest rate movements, while at the same time keeping the portfolio credit worthy.

In other words, they seek to generate returns both in declining and rising interest rate scenarios by managing their portfolio actively. They either generate interest income by holding the instruments till maturity or manage gains by selling them in the debt market if the price of the instrument rallies well.

That means that these instruments will not guarantee you fixed returns like deposits. Yet, over the last 10 years, they have beaten three-year deposit rates, irrespective of the year in which you invested. Let us look at income funds’ features and how they score over fixed deposits.

Income fund advantages

• Highly liquid. Can with draw money anytime unlike fixed deposits that come with a fixed lock-in period

• Actively managed. Seek to generate returns from varying interest rate cycles. Fixed deposits, on the other hand, carry re-investment risk. When a deposit matures and is reinvested, you may fall into a low interest rate regime and get lower returns than before.

• Have historically generated superior returns than fixed deposits. Please see data given.

• Very tax efficient, especially for those in the 20% and 30% tax brackets. Long-term capital gains (for holding over one year) are taxed at 10% without indexation or 20% with indexation. Interest on fixed deposits, though, is taxed at your income slab. Please see table for post-tax returns

• Offers high flexibility. Besides investing systematically you can even withdraw money systematically thus generating regular cash flow for yourself.

How to use income funds

• Invest your money in a combination of traditional fixed income options such as deposits and income funds to pep overall returns. You need not put your money in one basket.

• When you build a mutual fund portfolio, consider investing over one half of your capital in income funds when you have a time frame of say 2-3 years

• Use income funds, along with equity funds, as part of a long-term asset allocation strategy to build wealth. Choose the growth option.

• You can use income funds to also provide for some monthly cash flows by opting for a systematic withdrawal plan after first holding it for at least two years.

Note: If you have a time frame of less than 18 months, there are other short-term debt schemes that mutual funds offer. Income funds will not fit a short time frame. Also, remember that income funds do not guarantee fixed returns nor are they covered by insurance as is the case with bank fixed deposits (up to Rs 1 lakh). To this extent, they do not top the safety chart.

However, for longer periods, the interest rate risks are taken care of, thus generating superior returns for the limited risks assumed.

Birla Sun Life Dynamic Bond fund, IDFC SSI Medium Term Plan A, Templeton India Income Opportunities and HDFC Medium Term Opportunities are some of the consistent performers in this category.

Hi Vidya,

How do you compare Liquid Funds and Income funds. I couldnt get much difference b/w the 2.

Hi Rohit, thanks for your query. Liquid funds, as the name suggests, provide you liquidity. They can be withdrawn any time. That means they also need to invest only in very very short-term instruments. In one way, they are almost as liquid as your savings bank (except that they do not offer atm facilities barring one fund house). Income funds are like your fixed deposits. They are for a higher tenure. That means they actively invest in a combination of short and long term instruments. But unlike fixed deposits that are locked in for a fixed period, you enjoy better liquidity in income funds. This is because they are open ended. But you need to hold them for a period of say at least 18 months or so, to benefit from the fund’s strategy of timing its holding according to interest rates.

In all liquid funds are not investment avenues….they are simply saving avenues. They are not meant to deliver some great returns. Income funds seek to deliver good returns, generally superior to most traditional debt products. Of course, that also means that income funds are riskier than liquid funds. To sum up, liquid funds and income funds are 2 different products and should not be compared.

Hope this helps. – Tks Vidya

Hi Vidya..You said liquid funds do not offer ATM facility but i would like to tell you that i am already using ATM with “Reliance Money Manager-Daily Dividend” Fund.

Please advise if i should keep my investment in this fund or there are better funds. It’s fine if i don’t get ATM facility compared to high returns as online redemption request gets completed in 1 day..

FYI – Already given my documents to Fundsindia.com. My account will be activated in 2-3 days, he said.

Hello Vibhor, Yes, that is the only fund house that has ATM facility. With liquid funds performance keep varying as their portfolio maturities are short term. Hence, avoid chasing returns in liquid funds, as long as they deliver above savings bank rate. Currently Peerless Liquid Super and Templeton India TMA Super are top performers. But this may well change. As for the fund you hold – it s an ultra short-term fund and not a liquid fund..hence its returns tend to be higher than average returns of liquid funds.

Once, your account is activated, kindly use the ‘Ask Advisor’ feature (available when you click the help tab) for any specific portfolio queries on your funds with FundsIndia. Thanks.

Hi Vidya

Thanks for your reply. What is the difference between Ultra Short term fund and Liquid Fund? Which one is better considering high tax bracket?

The tax treatment is the same. Ultra short-term funds invest in slightly higher risk instruments than liquid funds. Also, many ultra short-term funds (not the one you hold) have exit loads for withdrawal within short periods. Liquid funds have no exit loads. thanks.

Hi,

Yet another insightful article. I would like to know when is the ideal time to invest in

1 income fund

2 dynamic fund

3 long term fund

Suggest funds if I want to lock in the money for 3 years and the bank interest rate is 6-7

Hello Karthik,

Instead of giving an ideal time, let us say the minimum time required to not suffer exit load and for the fund to perform would be 18-24 months for income funds and dynamic funds. Dynamic funds fall under the broader classification of income funds. It can be held upto your goal period,whether 3, 5,10 years.

By long-term fund, we do not know if you mean a gilt fund. Long term Gilt fund would require a 3-5 year approach.

An ideal time would depend on one’s own goals and time frame too.

For your 3-year requirement, kindly use the Ask advisor facility (in the help section on the top right of your fundsindia account, once you log in. This will help us answer you specifically, instead of generalising in a forum. In that query, kindly mention what is your risk appetite or whether you are looking for only debt funds or would like some equity as well and also the amount you can spare – whether lump sum or SIP. – Tks Vidya

Hi Vidhya, What option to choose in MIP between growth and dividend. Iam in a 30% tax bracket. How choosing between growth or dividend will impact the returns

Hello Ramkumar, MIPs are typically recommended for longer term of 2-3 years at least. That means, ideally, you would not suffer short-term capital gains tax. Since, the long-term Capital gains tax is 10% without indexation (or 20% with indexation) it is better to go for growth option; the dividend distribution tax for a dividend payout/reinvestment scheme would be 12.5% – which is marginally higher than the LTCG tax. In general, if you are in the higher tax bracket, and holding for over one year, growth is a superior option. – Tks Vidya

Hi Vidya and the FundsIndia team,

It is nice to read your informative articles. It is also nice to see prompt answers to questions from readers. Keep up the good work.

Regards

Satheesh

Thanks Satheesh. Do feel free to provide ideas/suggestions on topics that would interest investors. Vidya

Please confirm whether all dynamic bond funds by various MFs fall in this category?

Hello Hemant, yes, dynamic bond funds fall under the broad ‘income fund’ category. tks Vidya

Great article as always. Here are two suggestions, the first one for a future blog post hopefully:

1. A table similar to the following:

Fund Type Returns Risk Horizon

======= ==== === =====

FMPs avg avg 30 days +

ST income avg low 1-3 yrs

liquid funds low low < 3 mnths

etc

etc

I think this will be a very handy resource.

2. And then a way to actually select funds based on these categories (FMPs, ultra ST debt, liquid, income, whatever etc) on fundsindia.com

Hello Apoorv, great suggestions. Thanks! Will explore these for future newsletters. – Tks Vidya

Hi Vidya Bala, i want to invest 4-5 lacs. Can u suggest me some monthly return plans.

Hi Paramjit, Request you to kindly seek our detailed suggestions through your fundsindia account. Login and use the help tab (to your top right) to get in to ask advisor and mail us your query with your risk appetite, goal period if any or time horizon of invest and mode of investment – SIP or Lump sum. Youu can alternatively fix a schedule for our advisors to call you. Pl. note that mutual funds do not promise monthly fixed returns. You may choose to get some monthly cash flow through dividends, as and when declared or get a fixed sum regularly by using the systematic withdrawal plan option that you can choose. – Tks Vidya

Dear Vidya

i wnat to know about the RGESS Scheme , As i already have a demat Account and already invested thru demat account so whether m i eligible under this scheme or not

Pls Help

Regards

Hello Alok,

If you have a demat and are already invested through it, you are not eligible for RGESS. The first criteria for RGESS is that you should be a new investor in equities and should not have invested earlier. You do not qualify under this criteria. Tks, Vidya

Thanks Mam for ur clarification , bt i have to invest around 36000 to complete 100000 investment Target to avail 80 C benefit at full , so can u please suggest me the few ELSS Fund to invest thru SIP

Regards

Alok

Hi Alok, ICICI Pru Tax Plan and Franklin India Taxshield are good options. For the amount you have mentioned, one fund should suffice. You should prefer the Franklin fund if you have a low risk appetite and prefer large-caps. tks Vidya

Hi Ms.Vidya,

Kudos for a really apt article which talks about asset allocation using income funds. But there is a slight problem for beginners in the sense that Income funds can be categorized as Medium Term, Long Term, Credit Opportunities, Dynamic Bond Funds etc. So it would be nice to talk about these since some of them may not be suitable for the average investor seeking safety. For example, Templeton India Income Opportunities is actually a credit opportunities (CROP) type fund which invests in AA paper and usually needs people to stick with it though one complete interest rate cycle 🙂

Of course, at the other end ot the spectrum one has income funds which park a majority of their money in really long term papers and look stellar when GSEC yields drop.But there is a really a large interest rate risk and can actually give negative returns if the GSEC yields go against them. I am sure you do know about these issues in detail. Just wanted to mention these for the benefit of folks reading comments. Apologize for the long post.

Cheers

Arun

Hi Arun, You have all the pertinent points. Thanks for sharing! Income funds come in all shades and time frames. For the sake of brevity (lest the article becomes an essay 🙂 ), this article simply explored the returns angle. We did not also take in to account gilt funds or short-term income funds (most people follow the value research categories and we kept our category of income funds in line with that). We can certainly explore the kinds of income funds are their varying risk profile in a later article. – Tks, Vidya

Hi Vidya,

I want to start a SIP of Rs.2000/- in some income or Liquid fund for an year.Suggest me some good options that I can opt.

Hello Manoj, if your time frame is just about a year, we would not suggest income funds. You can consider a short-term fund like PineBridge Short Term Plan (growth) if you will hold for not less than a year. Otherwise, if you are merely investing for temporary liquidity purpose, you can go for growth option of HDFC Cash Management Savings Liquid OR Pramerica Liquid. tks

Hi Vidya,

I’m 43 yrs and looking for an investment of 1 Cr where in I should get monthly returns. Can you suggest me any guaranteed fund. I was thinking of going with FD as my risk appetite is Zero

Thanks,

Sudhir

Hello sir, There are no mutual funds that can guarantee returns as they are market driven. Given your sum and your requirement, we need to know your risk appetite and your time frame before suggesting funds. Request you to write in detail your requirement by logging in to your FundsIndia account and using the Ask Advisor feature. Our advisor will respond through mail or call back, whichever option you choose. Pl. see link to know where this feature is in you account: http://content.fundsindia.com/images/GettingAdvice.png . As you may be aware, this is a value add feature available to our users free of charge. Tks, Vidya

dear Vidya,

I saw one of your comment says if an investor is already having a DEMAT a/c, he is not eligible for RGESS. I do agree. Is it also true that if I had a past DEMAT a/c and traded for one time and closed the a/c, I am not holding current any demat a/c, still not eligible for RGESS. I hope I will not be termed as first time investor anymore. Please explain…:-(

i want to invest 50 lakhs , who will be better fd or income fund… i am a senior citizen. i m 72 years old

Hello sir,

If you require regular assured income then you should consider FDs first. You can probably invest 10% in income funds and use a systematic withdrawal plan to ensure regular cash flow for yourself.

If you do not require any income from this Rs 50 lakh, you should still consider investing a majority in FDs and good top-rated corporate deposits and probably 10-20% in income funds, if you have at least a 3-year view. Tks, Vidya

AS PER VRO RATING IDFC MODERATE ASSET ALLOCATION FUND IS GIVEN 5 STAR RATING WHERE AS YOUR WEBSITE SHOWS THERE IS NO RATING FOR THE SCHEME. WHY?

Sir, Thanks for highlighting this. I shall ask my back-end team to look at it. tks, vidya

Hello Vidya –

Interesting Article. Is it better to split the money into two debt income funds if the amount is more (e.g 10 lakhs in each fund)? I was actually planning to to invest into FD, when somebody mentioned to me about the Income funds. My period of investment is for 1 to 1.5 years, and as per my research they say its better to invest in Flexi or Dynamic income funds. Which one would you recommend?

Regards,

AK

Hello Ashok,

It is always better to diversify into 2-3 funds to reduce risks, if the investment amount is large and is invested in bulk. Hope you are aware that income funds do not guarantee returns like FDs. We recommend income/dynamic bond funds only with a 2-3 year perspective. We prefer short-term funds for 1-1.5 year time frame. You may refer to our preferred funds here: http://www.fundsindia.com/select-funds. Any specific query on portfolio may pl. be sent through the ‘ask advisor’ feature available to all FundsIndia account holders. Tks, Vidya

Hi Vidya,

Hope you are doing good. I was just surfing internet to find which option is better between FD’s and Debt Mutual Fund and I found this blog. So I thought to ask my query on this blog. Please advice whether Long term debt mutual fund(like SBI Dynamic bond fund or SBI Magnum Income fund) is better or 390days fixed deposit is better, which is fetching 9% p.a. interest. I am in 20% tax bracket. Also please advice me which debt funds are best to give higher return. I hope you reply soon.

Thanks

Hi Rahul, income funds (like the ones you have mentioned) have known to deliver superior returns in the long-term of 2-3 years. But as you know, they do not carry fixed returns like FDs. No marked-linked instrument (equity market or debt market) can assure fixed returns. Also, high returns comes because of the additional risks that one takes.

For the periods mentioned by you, which is about a year, only ultra short-term or short-term debt funds are safer bets in the mutual fund universe. So far these have delivered more than 9%. You may refer our list of ‘Select funds’ in http://www.fundsindia.com/select-funds.

To answer your question – income funds are suitable from a 2-3 year perspective to deliver superior returns. They cannot be compared with a 390-day deposit. For a 3-5 year deposit, I would say, income funds can score better.Thanks, Vidya

I have no idea about Fund market. My Property and FD Targets are already achieved. I want to Invest nearly 70 lacs in a period of time from my Salary. I want monthly income from the fund and the amount of risk involved (Extreme Condition) with the Capital. kindly inform the average monthly amount from this Capital.

Hello sir, your question is not clear. If you wish to know the average returns you will get from your capital, it would entirely depend on the fund choice and the asset class choice (equity or debt). Besides, unlike fixed deposits, mutual funds do not give any promised fixed returns as they are products linked to the market. Once the funds/asset class is determined a rough estimate of what can be the possible returns can be arrived at partly based on past performance of the fund. Returns could be in 8-10% range for debt and 10-18% range for equity. Hence, to arrive at portfolio returns would not be possible based on your input.

As funds do not guarantee returns, if you wish to build a portfolio with funds and derive monthly income from it in future, then Systematic withdrawal plan will be a good option. For building a portfolio, you may use the Ask Advisor feature available for all FundsIndia advisors. You can also use our retirement calculator,which is part of our Smart Solutions if your purpose is for retirement: http://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=4

Thanks, Vidya

Hi Vidya,

Bit confused about Gilt and MIP fund. Which is better between the two, want to go for low risk returns. I have already invested in Debt Long Term, Equity and Liquid funds. Which fund house will be better for MIP investment as well as Gilt?.

Thanks in advance.

Hello Ranjan,

You may decide the funds you need to go for based on your time frame and risk appetite. Gilt funds carry higher risks and are meant for strategic holding. MIPs carry some amount of risk as they have 20-25% in equities. If your time frame is less than 1 year, then only liquid, ultra short-term will suit you. For 1.2 years short-term funds will be good and for 2 years plus income funds or MIP (if you can take the equity) will suit well. For fund recommendations catering to your needs, you will have to use the ‘Ask Advisor’ feature in your activated FundsIndia account, so that we can track your portfolio query and respond. You may state your requirement and ask for a email response or call back from our advisor. It is a free service to our customers. Tks, Vidya

Thanks a lot, you cleared my all doubts. 🙂

Dear Madam,

Your blog is really good & informative. Please explain more on income fund,dynamic bond funds,corporate bond fund when we should take exposure to this funds, how this funds are tax efficient. Will be glad if you us with example

Hi Sonali,

Thanks. Your question would call for very long sessions 🙂 We have already discussed many of these at various points in this forum. Pl. read the archives in this blog and do keep following us for the information you asked. tks, Vidya

1. Do we have SIP plan in Income funds?

2. Some of my bank FDs are maturing towards the end of this year and I’ll end up with fifteen lacs+ (after paying 33%tax). Would you recommend the following:

a. 30% in Income funds (long term).

b. 30% in Tax free bonds

c. 30% in Liquid funds

d. 10% to have a ball.

Thanks.

Hello sir,

1. Yes, there are SIPs in income funds

2. I would recommend the foll:

– 30% in post office senior citizens scheme (if you are over 60) or 20% in bank deposits and 10% in quality corporate deposits or NCDs/bonds from PSU companies

– 30% in tax free bonds if they are issued. There are none now.

– 20% in ultra short-term funds and 10% in liquid funds

– rest as you wish.

thanks

Thank you very much.

Dear Vidya,

I’m in 30% tax bracket. Would you therefore not recommend tax-free bonds which are traded in the share market?

hello Ravi, Bonds traded in the market suffer from poor liquidity and hence not considered a good ground for retail investors (unless you are a bond trader). these are best bought at the time of offer. We will have companies lining up this year for tax-free bonds. You may get an opportunity then. Thanks.

The way the market is tumbling, the best option is gold. Considering the present scenario, whatever you do, you won’t be able to beat the inflation factor. So have a ball while the going is good…and go in for a new car.

Cheers, and thanks a lot.

@Ravi Bedi

If you want good yield and considerably safe returns, you may consider investign in 1 year fmp…currently yields are around 9.80-9.85 or 1 year fmp…and you may take growth option so post tax yield would work out to roughly 8.90%!!

Very good option!

Hi Vidya

I am planning to create a Pension fund . I am planning to invest Rs 10000 every month for next 20 years through SIP.

I am ready to take Medium risk by inversting 50% of my amount in good mutual funds .

Is it safe to do SIP in good returning Mutual funds for 15-20 years horizon.

For the remaning 50% , I am planning to select Debt/Income funds which gives much safer returns .

Is this a good plan ? Can you suggest me an alternative plan if you feel that this is not a good plan .

thanks/regards

Arun K

Note : I have already submitted documents for activating account with Fundsindia. Hoping it will get activated in next 2-3 days

Hi Arun and Rajnikanth. Thanks Rajnikanth for sharing your views. NPS is no doubt a low cost option to invest in equities. But if somebody does not specifically need to receive the money as pension and can simply invest in fixed income instruments post retirement, then a good portfolio of mutual funds will certainly score over NPS until retirement.

Arun, when you say 50% of your money in mutual funds, I suppose you mean equity mutual funds. If you are conservative that is fine. if you have moderate risk and a time horizon of not less than 10-15 years then you should consider at least about 70% in equities. You should not worry about its volatility in the short term. By volatility I mean there will be periods when the portfolio will go below capital. But with a 10-15 year view, the chances of losing money in equities is nil. If youa re not game for such risk, then restrict to 50%. Your plan is otherwise good.

Once, you activate your account, pl. use the ‘Ask Advisor’ feature (click help tab for this) and you will be able to ask us for a emailed response or call back by our advisors. A portfolio of funds can be suggested through this. This feature will also help us keep track of your questions and responses.

Thanks

Vidya

Sir

I want to invest for 2 to 3 years. Kindly suggest me 2-3 good Income Funds.

With Regards

V.A.BHAT.

hello sir,

Fund advice is available through our free feature’ Ask advisor’ if you have an activated FundsIndia account. Kindly request yout o register with us and finsih the one-time formalities. if you are already KYC compliant, then you can actually start using FundsIndia platform without any paper work. We will be constrained from offered advice over the blog. thanks.

Hi,

With the interest rate cycle phase(either increasing or decreasing) depends or related to type of fund to be invested to make good returns ?

Hello Sundar, the rate cycle and your own time frame are equally important in deciding what type of funds to go for. If you have a 3-year time frame, then income funds will provide gains, esp when rates start falling. But that may not happen in the near term. If you have a 1-2 year view then ultra short-term and short-term funds will provide gains as short-term rates provide scope for both ‘accrual’ (interest coming from the high rates in the short-term) and some appreciation when short-term rates ease. thanks, Vidya

Hi vidya,

my age is 25 now i want to invest 2 to 3k per month for a long term through SIP in debt funds so plz suggest me where to invest and avg returns.

Hello Vijay

For fund advice, kindly use the free’Ask Advisor’ feature in your FundsIndia account to get portfolios and reviews. I(f you do not have one, pl. contact our team to acticate your free account. thanks

Hello,

I want to invest 3 lakhs for 2 to 3 yrs either in Bank/Corp FD or Debt MF. Required rate of return is 8.45% (HDFC deposits offering 8.45% for 22 months to senior citizens). I have no no other income and fall in 0% tax bracket, so tax is not a consideration in comparing returns. Please advice if income fund will be suitable in current scenario. Whether to go for dynamic fund or credit opportunity fund or plain income fund. How much additional return can I expect over FD and whether it is adequate in relation to the additional risk they carry. thanks.

Sumit, If you are in the zero tax bracket, please use post office senior citizens’ first and then park some money in short-term debt funds and use a systematic withdrawal plan to create a fixed cash flow for you every month. Returns will likely beat bank fds. If you are going for income or dynamic bond funds, you should leave it as is for at least 2-3 years before you take it out. Also, you should be prepared for some volatility. We will not be able to give any future returns as regulations do not permit it. thanks, Vidya

Can you please explain difference between following three funds:

1)HDFC Income Fund – Direct Plan (Normal Dividend)

2)HDFC Income Fund – Direct Plan (QD)

3)HDFC Income Fund – Direct Plan (G)

All 3 are direct plan options – that is you buy them from the fund house. One is a dividend option (mormal) hwere dividend can be declred any time as desired by the fund. The second is a quarterly dividend option and third is a growth option where no dividend will be declared and the gain simply accumlates in your NAV. Thanks

can i suggest some long term debt fund option for invest?

Hello sir, individual investor advice can be done if you write to us through your FundsIndia account. thanks, Vidya

can i suggest some long term debt fund for invest?

Hello Sir,

Sorry for the delayed response. We will be constrained from providing individual recommendations. Please get in touch with us through your FundsIndia account.

Vidya

Hi Vidya,

I want to start a SIP of Rs.2000/- in some income or Liquid fund for an year.Suggest me some good options that I can opt.

Hello Manoj, if your time frame is just about a year, we would not suggest income funds. You can consider a short-term fund like PineBridge Short Term Plan (growth) if you will hold for not less than a year. Otherwise, if you are merely investing for temporary liquidity purpose, you can go for growth option of HDFC Cash Management Savings Liquid OR Pramerica Liquid. tks

Hi Vidya,

I’m 43 yrs and looking for an investment of 1 Cr where in I should get monthly returns. Can you suggest me any guaranteed fund. I was thinking of going with FD as my risk appetite is Zero

Thanks,

Sudhir

Hello sir, There are no mutual funds that can guarantee returns as they are market driven. Given your sum and your requirement, we need to know your risk appetite and your time frame before suggesting funds. Request you to write in detail your requirement by logging in to your FundsIndia account and using the Ask Advisor feature. Our advisor will respond through mail or call back, whichever option you choose. Pl. see link to know where this feature is in you account: http://content.fundsindia.com/images/GettingAdvice.png . As you may be aware, this is a value add feature available to our users free of charge. Tks, Vidya

dear Vidya,

I saw one of your comment says if an investor is already having a DEMAT a/c, he is not eligible for RGESS. I do agree. Is it also true that if I had a past DEMAT a/c and traded for one time and closed the a/c, I am not holding current any demat a/c, still not eligible for RGESS. I hope I will not be termed as first time investor anymore. Please explain…:-(

Dear Madam,

Your blog is really good & informative. Please explain more on income fund,dynamic bond funds,corporate bond fund when we should take exposure to this funds, how this funds are tax efficient. Will be glad if you us with example

Hi Sonali,

Thanks. Your question would call for very long sessions 🙂 We have already discussed many of these at various points in this forum. Pl. read the archives in this blog and do keep following us for the information you asked. tks, Vidya

Hi Vidya,

Hope you are doing good. I was just surfing internet to find which option is better between FD’s and Debt Mutual Fund and I found this blog. So I thought to ask my query on this blog. Please advice whether Long term debt mutual fund(like SBI Dynamic bond fund or SBI Magnum Income fund) is better or 390days fixed deposit is better, which is fetching 9% p.a. interest. I am in 20% tax bracket. Also please advice me which debt funds are best to give higher return. I hope you reply soon.

Thanks

Hi Rahul, income funds (like the ones you have mentioned) have known to deliver superior returns in the long-term of 2-3 years. But as you know, they do not carry fixed returns like FDs. No marked-linked instrument (equity market or debt market) can assure fixed returns. Also, high returns comes because of the additional risks that one takes.

For the periods mentioned by you, which is about a year, only ultra short-term or short-term debt funds are safer bets in the mutual fund universe. So far these have delivered more than 9%. You may refer our list of ‘Select funds’ in http://www.fundsindia.com/select-funds.

To answer your question – income funds are suitable from a 2-3 year perspective to deliver superior returns. They cannot be compared with a 390-day deposit. For a 3-5 year deposit, I would say, income funds can score better.Thanks, Vidya

AS PER VRO RATING IDFC MODERATE ASSET ALLOCATION FUND IS GIVEN 5 STAR RATING WHERE AS YOUR WEBSITE SHOWS THERE IS NO RATING FOR THE SCHEME. WHY?

Sir, Thanks for highlighting this. I shall ask my back-end team to look at it. tks, vidya

Hello Vidya –

Interesting Article. Is it better to split the money into two debt income funds if the amount is more (e.g 10 lakhs in each fund)? I was actually planning to to invest into FD, when somebody mentioned to me about the Income funds. My period of investment is for 1 to 1.5 years, and as per my research they say its better to invest in Flexi or Dynamic income funds. Which one would you recommend?

Regards,

AK

Hello Ashok,

It is always better to diversify into 2-3 funds to reduce risks, if the investment amount is large and is invested in bulk. Hope you are aware that income funds do not guarantee returns like FDs. We recommend income/dynamic bond funds only with a 2-3 year perspective. We prefer short-term funds for 1-1.5 year time frame. You may refer to our preferred funds here: http://www.fundsindia.com/select-funds. Any specific query on portfolio may pl. be sent through the ‘ask advisor’ feature available to all FundsIndia account holders. Tks, Vidya

i want to invest 50 lakhs , who will be better fd or income fund… i am a senior citizen. i m 72 years old

Hello sir,

If you require regular assured income then you should consider FDs first. You can probably invest 10% in income funds and use a systematic withdrawal plan to ensure regular cash flow for yourself.

If you do not require any income from this Rs 50 lakh, you should still consider investing a majority in FDs and good top-rated corporate deposits and probably 10-20% in income funds, if you have at least a 3-year view. Tks, Vidya

I have no idea about Fund market. My Property and FD Targets are already achieved. I want to Invest nearly 70 lacs in a period of time from my Salary. I want monthly income from the fund and the amount of risk involved (Extreme Condition) with the Capital. kindly inform the average monthly amount from this Capital.

Hello sir, your question is not clear. If you wish to know the average returns you will get from your capital, it would entirely depend on the fund choice and the asset class choice (equity or debt). Besides, unlike fixed deposits, mutual funds do not give any promised fixed returns as they are products linked to the market. Once the funds/asset class is determined a rough estimate of what can be the possible returns can be arrived at partly based on past performance of the fund. Returns could be in 8-10% range for debt and 10-18% range for equity. Hence, to arrive at portfolio returns would not be possible based on your input.

As funds do not guarantee returns, if you wish to build a portfolio with funds and derive monthly income from it in future, then Systematic withdrawal plan will be a good option. For building a portfolio, you may use the Ask Advisor feature available for all FundsIndia advisors. You can also use our retirement calculator,which is part of our Smart Solutions if your purpose is for retirement: http://www.fundsindia.com/content/jsp/investor/SmartSolutions.do?method=showScreen&ssid=4

Thanks, Vidya

1. Do we have SIP plan in Income funds?

2. Some of my bank FDs are maturing towards the end of this year and I’ll end up with fifteen lacs+ (after paying 33%tax). Would you recommend the following:

a. 30% in Income funds (long term).

b. 30% in Tax free bonds

c. 30% in Liquid funds

d. 10% to have a ball.

Thanks.

Hello sir,

1. Yes, there are SIPs in income funds

2. I would recommend the foll:

– 30% in post office senior citizens scheme (if you are over 60) or 20% in bank deposits and 10% in quality corporate deposits or NCDs/bonds from PSU companies

– 30% in tax free bonds if they are issued. There are none now.

– 20% in ultra short-term funds and 10% in liquid funds

– rest as you wish.

thanks

Thank you very much.

@Ravi Bedi

If you want good yield and considerably safe returns, you may consider investign in 1 year fmp…currently yields are around 9.80-9.85 or 1 year fmp…and you may take growth option so post tax yield would work out to roughly 8.90%!!

Very good option!

Hi Vidya,

Bit confused about Gilt and MIP fund. Which is better between the two, want to go for low risk returns. I have already invested in Debt Long Term, Equity and Liquid funds. Which fund house will be better for MIP investment as well as Gilt?.

Thanks in advance.

Hello Ranjan,

You may decide the funds you need to go for based on your time frame and risk appetite. Gilt funds carry higher risks and are meant for strategic holding. MIPs carry some amount of risk as they have 20-25% in equities. If your time frame is less than 1 year, then only liquid, ultra short-term will suit you. For 1.2 years short-term funds will be good and for 2 years plus income funds or MIP (if you can take the equity) will suit well. For fund recommendations catering to your needs, you will have to use the ‘Ask Advisor’ feature in your activated FundsIndia account, so that we can track your portfolio query and respond. You may state your requirement and ask for a email response or call back from our advisor. It is a free service to our customers. Tks, Vidya

Thanks a lot, you cleared my all doubts. 🙂

Sir

I want to invest for 2 to 3 years. Kindly suggest me 2-3 good Income Funds.

With Regards

V.A.BHAT.

hello sir,

Fund advice is available through our free feature’ Ask advisor’ if you have an activated FundsIndia account. Kindly request yout o register with us and finsih the one-time formalities. if you are already KYC compliant, then you can actually start using FundsIndia platform without any paper work. We will be constrained from offered advice over the blog. thanks.

Hi Vidya

I am planning to create a Pension fund . I am planning to invest Rs 10000 every month for next 20 years through SIP.

I am ready to take Medium risk by inversting 50% of my amount in good mutual funds .

Is it safe to do SIP in good returning Mutual funds for 15-20 years horizon.

For the remaning 50% , I am planning to select Debt/Income funds which gives much safer returns .

Is this a good plan ? Can you suggest me an alternative plan if you feel that this is not a good plan .

thanks/regards

Arun K

Note : I have already submitted documents for activating account with Fundsindia. Hoping it will get activated in next 2-3 days

Hi Arun and Rajnikanth. Thanks Rajnikanth for sharing your views. NPS is no doubt a low cost option to invest in equities. But if somebody does not specifically need to receive the money as pension and can simply invest in fixed income instruments post retirement, then a good portfolio of mutual funds will certainly score over NPS until retirement.

Arun, when you say 50% of your money in mutual funds, I suppose you mean equity mutual funds. If you are conservative that is fine. if you have moderate risk and a time horizon of not less than 10-15 years then you should consider at least about 70% in equities. You should not worry about its volatility in the short term. By volatility I mean there will be periods when the portfolio will go below capital. But with a 10-15 year view, the chances of losing money in equities is nil. If youa re not game for such risk, then restrict to 50%. Your plan is otherwise good.

Once, you activate your account, pl. use the ‘Ask Advisor’ feature (click help tab for this) and you will be able to ask us for a emailed response or call back by our advisors. A portfolio of funds can be suggested through this. This feature will also help us keep track of your questions and responses.

Thanks

Vidya

Hi vidya,

my age is 25 now i want to invest 2 to 3k per month for a long term through SIP in debt funds so plz suggest me where to invest and avg returns.

Hello Vijay

For fund advice, kindly use the free’Ask Advisor’ feature in your FundsIndia account to get portfolios and reviews. I(f you do not have one, pl. contact our team to acticate your free account. thanks

Hello,

I want to invest 3 lakhs for 2 to 3 yrs either in Bank/Corp FD or Debt MF. Required rate of return is 8.45% (HDFC deposits offering 8.45% for 22 months to senior citizens). I have no no other income and fall in 0% tax bracket, so tax is not a consideration in comparing returns. Please advice if income fund will be suitable in current scenario. Whether to go for dynamic fund or credit opportunity fund or plain income fund. How much additional return can I expect over FD and whether it is adequate in relation to the additional risk they carry. thanks.

Sumit, If you are in the zero tax bracket, please use post office senior citizens’ first and then park some money in short-term debt funds and use a systematic withdrawal plan to create a fixed cash flow for you every month. Returns will likely beat bank fds. If you are going for income or dynamic bond funds, you should leave it as is for at least 2-3 years before you take it out. Also, you should be prepared for some volatility. We will not be able to give any future returns as regulations do not permit it. thanks, Vidya

Dear Vidya,

I’m in 30% tax bracket. Would you therefore not recommend tax-free bonds which are traded in the share market?

hello Ravi, Bonds traded in the market suffer from poor liquidity and hence not considered a good ground for retail investors (unless you are a bond trader). these are best bought at the time of offer. We will have companies lining up this year for tax-free bonds. You may get an opportunity then. Thanks.

The way the market is tumbling, the best option is gold. Considering the present scenario, whatever you do, you won’t be able to beat the inflation factor. So have a ball while the going is good…and go in for a new car.

Cheers, and thanks a lot.

Can you please explain difference between following three funds:

1)HDFC Income Fund – Direct Plan (Normal Dividend)

2)HDFC Income Fund – Direct Plan (QD)

3)HDFC Income Fund – Direct Plan (G)

All 3 are direct plan options – that is you buy them from the fund house. One is a dividend option (mormal) hwere dividend can be declred any time as desired by the fund. The second is a quarterly dividend option and third is a growth option where no dividend will be declared and the gain simply accumlates in your NAV. Thanks

Hi Vidya Bala, i want to invest 4-5 lacs. Can u suggest me some monthly return plans.

Hi Paramjit, Request you to kindly seek our detailed suggestions through your fundsindia account. Login and use the help tab (to your top right) to get in to ask advisor and mail us your query with your risk appetite, goal period if any or time horizon of invest and mode of investment – SIP or Lump sum. Youu can alternatively fix a schedule for our advisors to call you. Pl. note that mutual funds do not promise monthly fixed returns. You may choose to get some monthly cash flow through dividends, as and when declared or get a fixed sum regularly by using the systematic withdrawal plan option that you can choose. – Tks Vidya

Hi Ms.Vidya,

Kudos for a really apt article which talks about asset allocation using income funds. But there is a slight problem for beginners in the sense that Income funds can be categorized as Medium Term, Long Term, Credit Opportunities, Dynamic Bond Funds etc. So it would be nice to talk about these since some of them may not be suitable for the average investor seeking safety. For example, Templeton India Income Opportunities is actually a credit opportunities (CROP) type fund which invests in AA paper and usually needs people to stick with it though one complete interest rate cycle 🙂

Of course, at the other end ot the spectrum one has income funds which park a majority of their money in really long term papers and look stellar when GSEC yields drop.But there is a really a large interest rate risk and can actually give negative returns if the GSEC yields go against them. I am sure you do know about these issues in detail. Just wanted to mention these for the benefit of folks reading comments. Apologize for the long post.

Cheers

Arun

Hi Arun, You have all the pertinent points. Thanks for sharing! Income funds come in all shades and time frames. For the sake of brevity (lest the article becomes an essay 🙂 ), this article simply explored the returns angle. We did not also take in to account gilt funds or short-term income funds (most people follow the value research categories and we kept our category of income funds in line with that). We can certainly explore the kinds of income funds are their varying risk profile in a later article. – Tks, Vidya

can i suggest some long term debt fund option for invest?

Hello sir, individual investor advice can be done if you write to us through your FundsIndia account. thanks, Vidya

Dear Vidya

i wnat to know about the RGESS Scheme , As i already have a demat Account and already invested thru demat account so whether m i eligible under this scheme or not

Pls Help

Regards

Hello Alok,

If you have a demat and are already invested through it, you are not eligible for RGESS. The first criteria for RGESS is that you should be a new investor in equities and should not have invested earlier. You do not qualify under this criteria. Tks, Vidya

Thanks Mam for ur clarification , bt i have to invest around 36000 to complete 100000 investment Target to avail 80 C benefit at full , so can u please suggest me the few ELSS Fund to invest thru SIP

Regards

Alok

Hi Alok, ICICI Pru Tax Plan and Franklin India Taxshield are good options. For the amount you have mentioned, one fund should suffice. You should prefer the Franklin fund if you have a low risk appetite and prefer large-caps. tks Vidya

Great article as always. Here are two suggestions, the first one for a future blog post hopefully:

1. A table similar to the following:

Fund Type Returns Risk Horizon

======= ==== === =====

FMPs avg avg 30 days +

ST income avg low 1-3 yrs

liquid funds low low < 3 mnths

etc

etc

I think this will be a very handy resource.

2. And then a way to actually select funds based on these categories (FMPs, ultra ST debt, liquid, income, whatever etc) on fundsindia.com

Hello Apoorv, great suggestions. Thanks! Will explore these for future newsletters. – Tks Vidya

Hi,

With the interest rate cycle phase(either increasing or decreasing) depends or related to type of fund to be invested to make good returns ?

Hello Sundar, the rate cycle and your own time frame are equally important in deciding what type of funds to go for. If you have a 3-year time frame, then income funds will provide gains, esp when rates start falling. But that may not happen in the near term. If you have a 1-2 year view then ultra short-term and short-term funds will provide gains as short-term rates provide scope for both ‘accrual’ (interest coming from the high rates in the short-term) and some appreciation when short-term rates ease. thanks, Vidya

can i suggest some long term debt fund for invest?

Hello Sir,

Sorry for the delayed response. We will be constrained from providing individual recommendations. Please get in touch with us through your FundsIndia account.

Vidya

Hi Vidya,

How do you compare Liquid Funds and Income funds. I couldnt get much difference b/w the 2.

Hi Rohit, thanks for your query. Liquid funds, as the name suggests, provide you liquidity. They can be withdrawn any time. That means they also need to invest only in very very short-term instruments. In one way, they are almost as liquid as your savings bank (except that they do not offer atm facilities barring one fund house). Income funds are like your fixed deposits. They are for a higher tenure. That means they actively invest in a combination of short and long term instruments. But unlike fixed deposits that are locked in for a fixed period, you enjoy better liquidity in income funds. This is because they are open ended. But you need to hold them for a period of say at least 18 months or so, to benefit from the fund’s strategy of timing its holding according to interest rates.

In all liquid funds are not investment avenues….they are simply saving avenues. They are not meant to deliver some great returns. Income funds seek to deliver good returns, generally superior to most traditional debt products. Of course, that also means that income funds are riskier than liquid funds. To sum up, liquid funds and income funds are 2 different products and should not be compared.

Hope this helps. – Tks Vidya

Hi Vidya..You said liquid funds do not offer ATM facility but i would like to tell you that i am already using ATM with “Reliance Money Manager-Daily Dividend” Fund.

Please advise if i should keep my investment in this fund or there are better funds. It’s fine if i don’t get ATM facility compared to high returns as online redemption request gets completed in 1 day..

FYI – Already given my documents to Fundsindia.com. My account will be activated in 2-3 days, he said.

Hello Vibhor, Yes, that is the only fund house that has ATM facility. With liquid funds performance keep varying as their portfolio maturities are short term. Hence, avoid chasing returns in liquid funds, as long as they deliver above savings bank rate. Currently Peerless Liquid Super and Templeton India TMA Super are top performers. But this may well change. As for the fund you hold – it s an ultra short-term fund and not a liquid fund..hence its returns tend to be higher than average returns of liquid funds.

Once, your account is activated, kindly use the ‘Ask Advisor’ feature (available when you click the help tab) for any specific portfolio queries on your funds with FundsIndia. Thanks.

Hi Vidya

Thanks for your reply. What is the difference between Ultra Short term fund and Liquid Fund? Which one is better considering high tax bracket?

The tax treatment is the same. Ultra short-term funds invest in slightly higher risk instruments than liquid funds. Also, many ultra short-term funds (not the one you hold) have exit loads for withdrawal within short periods. Liquid funds have no exit loads. thanks.

Hi,

Yet another insightful article. I would like to know when is the ideal time to invest in

1 income fund

2 dynamic fund

3 long term fund

Suggest funds if I want to lock in the money for 3 years and the bank interest rate is 6-7

Hello Karthik,

Instead of giving an ideal time, let us say the minimum time required to not suffer exit load and for the fund to perform would be 18-24 months for income funds and dynamic funds. Dynamic funds fall under the broader classification of income funds. It can be held upto your goal period,whether 3, 5,10 years.

By long-term fund, we do not know if you mean a gilt fund. Long term Gilt fund would require a 3-5 year approach.

An ideal time would depend on one’s own goals and time frame too.

For your 3-year requirement, kindly use the Ask advisor facility (in the help section on the top right of your fundsindia account, once you log in. This will help us answer you specifically, instead of generalising in a forum. In that query, kindly mention what is your risk appetite or whether you are looking for only debt funds or would like some equity as well and also the amount you can spare – whether lump sum or SIP. – Tks Vidya

Hi Vidhya, What option to choose in MIP between growth and dividend. Iam in a 30% tax bracket. How choosing between growth or dividend will impact the returns

Hello Ramkumar, MIPs are typically recommended for longer term of 2-3 years at least. That means, ideally, you would not suffer short-term capital gains tax. Since, the long-term Capital gains tax is 10% without indexation (or 20% with indexation) it is better to go for growth option; the dividend distribution tax for a dividend payout/reinvestment scheme would be 12.5% – which is marginally higher than the LTCG tax. In general, if you are in the higher tax bracket, and holding for over one year, growth is a superior option. – Tks Vidya

Please confirm whether all dynamic bond funds by various MFs fall in this category?

Hello Hemant, yes, dynamic bond funds fall under the broad ‘income fund’ category. tks Vidya

Hi Vidya and the FundsIndia team,

It is nice to read your informative articles. It is also nice to see prompt answers to questions from readers. Keep up the good work.

Regards

Satheesh

Thanks Satheesh. Do feel free to provide ideas/suggestions on topics that would interest investors. Vidya