If you are looking to play the opportunities in the debt market with at least a 1-2 year investment perspective, you can consider investments in Templeton India Short Term Income Plan.

This fund, which seeks to tap the opportunities in the corporate debt segment has, over years, proved its mettle in navigating tough markets and generating returns superior to traditional options such as fixed deposits, on a post-tax basis. The fund delivered returns of 9% compounded annually over the last 5 years, comfortably beating benchmark Crisil Short Term Bond Fund Index’ return of 7.4%.

Suitability and Strategy

Templeton India Short Term Income Plan is a good fund to tide over an uncertain interest rate environment, given its relatively low average maturity profile. But that does not make it a low risk fund as it has exposure to slightly lower rated corporate bonds, albeit investment grade. That means, while the fund is low on interest rate risk, it does carry credit risk.

The fund is therefore suitable only if you have some risk appetite. Investment at this point, if you wish to exit from the fund in the next 1-1.5 years, will provide you with double indexation benefit. That is likely to ensure that your tax is either very low or nil.

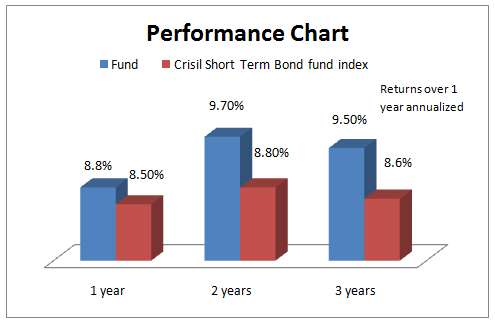

Templeton India Short Term Income Plan has beat its benchmark 100% of the times on a rolling one-year return basis for the past 3 years. While it did not generate negative returns (1-year return) on any of these occasions, the least 1-year return generated by it was between March 2010 and March 2011 – at 5.5%.

The maximum 1-year return during this period was a good 11.9%. Interestingly enough, its 1-year rolling return, taken on any date through 2013, has mostly been in the 8-11% range, the poor debt market conditions notwithstanding (in the second half of 2013).

That said, we analyzed how the fund performed on a monthly rolling-return basis to know whether the fund managed to tide over short-term volatilities such as the one in mid-2013. We observed that the fund’s rolling return did go negative, in the month of July 2013, when the debt market witnessed turmoil.

However, the worst fall though was -1.65% (for 1-month ending July 24, 2013). It is noteworthy that this is still superior to the 2-4% fall that many income/gilt funds with longer duration witnessed.

To summarize, while the fund is not totally immune to rate risks, with a low average maturity, it has managed volatility well.

Portfolio

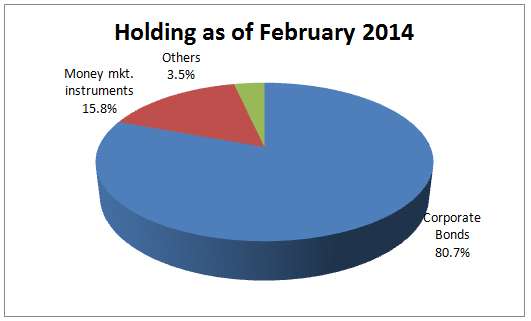

Templeton India Short Term Income Plan has over 80% of its assets in corporate bonds, a small exposure to public sector bonds and the rest in money market instruments. Its corporate bond holdings mostly come with an AA credit rating. The average maturity of the portfolio was 1.78 years as of February and has seen a steady decline from about 2.6 years in March 2013, to keep the portfolio risk low in line with rising interest rates.

The fund has one of the most diversified debt portfolios with 70-80 instruments. Bonds from NBFCs in the Cholamandalam or Sundaram BNP Paribas Group, besides bonds of many of the unlisted arms of the Tata group and quite a few instruments from the Mahindra group find a place in the portfolio.

We think given the slightly lower rating of the instruments, the diversification, albeit appearing to be one too many, may be required to soften any impact in the event of trouble with any instrument.

Outlook

We believe investors can gain adequately with short-to medium-term instruments for the simple reason that short-term rates are, at present, higher than long-dated ones.

Any decline in yields will be more beneficial at the short end. Even if a rate cut does not happen, funds such as Templeton India Short Term Income Plan are best placed to gain from the high interest accruals coming from corporate bonds. As of February, the yield to maturity of this fund was 11.13%.

The fund is managed by Umesh Sharma and Sachin Padwal-Desai. The fund will have an exit load if redeemed within 1 year.

Hi Vidya,

I am not sure if birla-sun-life-floating-rate-long-term-plan falls under the same category as this fund. Could you please draw some parallel between these two? I was comparing these 2 for same investment duration(1-2 yrs).

Thanks

Hello Rahaman, There are not comparable in terms of credit risk. They both have mandate to invest in short to medium tenure instruments. Birla Sun Life Floating Rate LTP does not take credit risks. So the comparison was more for the duration. thanks,

Hi Vidya,

I have seen many articles recommending various mutual funds from you.

One consistent feature I see is the comparison with Benchmark.

In case of good or average performer the fund will be beating benchmark.

I would like to rather see the comparison with the other best funds in this category.

I would say that would be the real test while deciding which fund in that category customer should choose.

While comparing same criteria can be applied for eg, volatility, consistent performance or rolling returns etc.

And also mentioning its rating w.r.t crisil, where it stands w.r.t to yearly returns, rolling returns etc would help your readers.

I don’t consider comparison with benchmark as good enough.

Just my thoughts.

Regards,

-Praveen

Hello Praveen,

Thanks for your feedback. We will certainly incorporate them when needed.

when we select funds, we certainly take into account the performance in terms of various metrics over peers as well. But benchmark is a very key criteria when it comes to consistency. I cannot compare one fund to another for consistency. What we do is rather compare each of it with its benchmark and see which is superior. End of the day, a fund’s mandate is to beat its benchmark. We of course, do peer comparison but often times, given the varied strategy peer comparison is sometimes unfair.

Similarly, on various other metrics such as risk-adjusted returns, standard deviation too, we do the comparison. However, it may be too much information and hence keep the details limited. But in a good number of our reviews, we do mention some form of peer comparison. We do not go by Crisil ratings as we have our in-house criteria for filtering funds.

Hi Vidya,

1. Crisil rating was a suggestion. If you have your own rating you can mention the same as well.

2. There might be many funds performing better than a benchmark. So investor would like to know one of the best funds in terms of return but would like to credit risk, exit load etc while taking an informed decision.

For eg information that can be included would be: Exit load, Average rating of the investment instead of just saying high credit risk. That can give some indication to rating of these bonds.

Exit load is an important factor in my opinion. if a fund charges 1% exit load if redeemed within 1 year than it could be an important factor to investor.

Regards,

-Praveen

Hello Praveen,

Thanks for your suggestions.

1. At present we do not have ratings as we do not wish to compartmentalize funds merely based on past performance. however, once you create a portfolio, you can go to the instant review in each portfolio and see what is our call on each of the equity funds you hold.

Fund selection, to us, comes based on a mix of quantitative and qualitative factors, unlike just quantitative factors considered by most rating agencies. However, we do carry value research’s rating for each fund on our website for investor reference. Once you see a scheme in our explorer or in the transaction page, you will also get its rating.

2. Details of exit load is all available in the scheme information displayed in our website. http://www.fundsindia.com/products/mutual-fund/all

Also, any abnornal loads are factored when we choose funds. But the call as such focuses on fund performance and not on investment/operational details. Unless it is something that needs to be brought to an investor’s notice (such as 2 or 3-year exit load and so on, in which case we do mention), the same can be viewed by you on the website before investing. Having an online portal, it is easier for us to provide details there. Exit load of 1% for redemption within 1 year for instance is quite normal now in most equity funds to discourage churning.

Dear Ms.Vidya,

How this fund compares with Birla Sun Life,both short term and Medium Fund for my consideration.

Hello Mr Anand,

This fund is slightly lower on risk compared with Birla Sun Life Medium Term and Short Term in terms of the risk profile of portfolio and the 2 funds require a 2-3 year holding period at least. Hope this helps.

In future, request you to route any investment specific queries through your account (advisor support) to enable us to respond faster. The blog may pl. be used as a discussion forum.

thanks

Vidya

Since we are talking about debt funds quoting exit load of equity fUnd is not appropriate.

exit loads of debt funds varies lot even within same category of funds.

So i felt explicitly mentioning it will help with readers.

But if you feel readers have to visit other pages to make decision on your recommendation the that is left to your readers.

Regards,

Praveen

Hi Vidhya ,

I want to Invest in Monthly Income Plan.

Please Recommned

Hello Manu. Sorry for the delayed response. In future, kindly route all your queries through the ‘advisor appointment’ feature available in your account if you click the help tab. This will help our advisory team to track and reply to queries in a process-driven manner. You can pick any of the funds in our select funds under the category of – Hybrid funds – low risk in the link: http://www.fundsindia.com/select-funds

If you need further help, pl use the help tab mentioned above to post in your query and our advisors will get back to you. The blog is more a discussion forum. We will be happy to help you with investments, through our formal channel – through your account. thanks, Vidya

Hi Vidya,

I am not sure if birla-sun-life-floating-rate-long-term-plan falls under the same category as this fund. Could you please draw some parallel between these two? I was comparing these 2 for same investment duration(1-2 yrs).

Thanks

Hello Rahaman, There are not comparable in terms of credit risk. They both have mandate to invest in short to medium tenure instruments. Birla Sun Life Floating Rate LTP does not take credit risks. So the comparison was more for the duration. thanks,

Hi Vidhya ,

I want to Invest in Monthly Income Plan.

Please Recommned

Hello Manu. Sorry for the delayed response. In future, kindly route all your queries through the ‘advisor appointment’ feature available in your account if you click the help tab. This will help our advisory team to track and reply to queries in a process-driven manner. You can pick any of the funds in our select funds under the category of – Hybrid funds – low risk in the link: http://www.fundsindia.com/select-funds

If you need further help, pl use the help tab mentioned above to post in your query and our advisors will get back to you. The blog is more a discussion forum. We will be happy to help you with investments, through our formal channel – through your account. thanks, Vidya

Hi Vidya,

I have seen many articles recommending various mutual funds from you.

One consistent feature I see is the comparison with Benchmark.

In case of good or average performer the fund will be beating benchmark.

I would like to rather see the comparison with the other best funds in this category.

I would say that would be the real test while deciding which fund in that category customer should choose.

While comparing same criteria can be applied for eg, volatility, consistent performance or rolling returns etc.

And also mentioning its rating w.r.t crisil, where it stands w.r.t to yearly returns, rolling returns etc would help your readers.

I don’t consider comparison with benchmark as good enough.

Just my thoughts.

Regards,

-Praveen

Hello Praveen,

Thanks for your feedback. We will certainly incorporate them when needed.

when we select funds, we certainly take into account the performance in terms of various metrics over peers as well. But benchmark is a very key criteria when it comes to consistency. I cannot compare one fund to another for consistency. What we do is rather compare each of it with its benchmark and see which is superior. End of the day, a fund’s mandate is to beat its benchmark. We of course, do peer comparison but often times, given the varied strategy peer comparison is sometimes unfair.

Similarly, on various other metrics such as risk-adjusted returns, standard deviation too, we do the comparison. However, it may be too much information and hence keep the details limited. But in a good number of our reviews, we do mention some form of peer comparison. We do not go by Crisil ratings as we have our in-house criteria for filtering funds.

Hi Vidya,

1. Crisil rating was a suggestion. If you have your own rating you can mention the same as well.

2. There might be many funds performing better than a benchmark. So investor would like to know one of the best funds in terms of return but would like to credit risk, exit load etc while taking an informed decision.

For eg information that can be included would be: Exit load, Average rating of the investment instead of just saying high credit risk. That can give some indication to rating of these bonds.

Exit load is an important factor in my opinion. if a fund charges 1% exit load if redeemed within 1 year than it could be an important factor to investor.

Regards,

-Praveen

Hello Praveen,

Thanks for your suggestions.

1. At present we do not have ratings as we do not wish to compartmentalize funds merely based on past performance. however, once you create a portfolio, you can go to the instant review in each portfolio and see what is our call on each of the equity funds you hold.

Fund selection, to us, comes based on a mix of quantitative and qualitative factors, unlike just quantitative factors considered by most rating agencies. However, we do carry value research’s rating for each fund on our website for investor reference. Once you see a scheme in our explorer or in the transaction page, you will also get its rating.

2. Details of exit load is all available in the scheme information displayed in our website. http://www.fundsindia.com/products/mutual-fund/all

Also, any abnornal loads are factored when we choose funds. But the call as such focuses on fund performance and not on investment/operational details. Unless it is something that needs to be brought to an investor’s notice (such as 2 or 3-year exit load and so on, in which case we do mention), the same can be viewed by you on the website before investing. Having an online portal, it is easier for us to provide details there. Exit load of 1% for redemption within 1 year for instance is quite normal now in most equity funds to discourage churning.

Dear Ms.Vidya,

How this fund compares with Birla Sun Life,both short term and Medium Fund for my consideration.

Hello Mr Anand,

This fund is slightly lower on risk compared with Birla Sun Life Medium Term and Short Term in terms of the risk profile of portfolio and the 2 funds require a 2-3 year holding period at least. Hope this helps.

In future, request you to route any investment specific queries through your account (advisor support) to enable us to respond faster. The blog may pl. be used as a discussion forum.

thanks

Vidya

Since we are talking about debt funds quoting exit load of equity fUnd is not appropriate.

exit loads of debt funds varies lot even within same category of funds.

So i felt explicitly mentioning it will help with readers.

But if you feel readers have to visit other pages to make decision on your recommendation the that is left to your readers.

Regards,

Praveen