An article a couple of weeks ago, in a leading business newspaper, may have come as a rude shock to some of you. Over the past ten years, it claimed, large-cap equity funds delivered returns on par with bank fixed deposits.

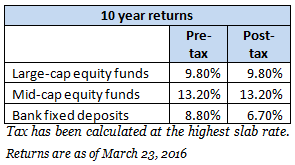

Equity large-cap funds delivered an annual average return of 9.8 per cent from March 2006 to now. A bank deposit taken at the same time would have delivered 8.8 per cent. So is there no use in equity investment? No. A look past the simple return numbers will help restore your faith in equities.

High risk, high returns

One, the return on the bank deposit works out to the figure of 8.8% only when considering the highest rate, as per RBI data. On a similar note, the highest return a large-cap fund delivered in the past ten years is actually an annual 14.5 per cent. That is perfectly satisfactory. In fact, over 60 per cent of the large-cap funds beat the category’s 9.8 per cent average return, ranging between 10 and 12 per cent. Choosing a fund that has consistently beaten the market and its category, therefore, is of immense importance when deciding to invest in a mutual fund.

Two, interest on fixed deposit is taxed at slab rates and this cuts into the return. At the 10,  20 and 30 per cent tax brackets, the return on the fixed deposit drops to 8.1%, 7.4%, and 6.7% respectively. Gains on equity funds, when held for more than one year, are not taxed. The one percentage point differential between fixed deposits and large-cap funds, therefore, widens to two to three percentage points.

20 and 30 per cent tax brackets, the return on the fixed deposit drops to 8.1%, 7.4%, and 6.7% respectively. Gains on equity funds, when held for more than one year, are not taxed. The one percentage point differential between fixed deposits and large-cap funds, therefore, widens to two to three percentage points.

Three, using the SIP method to invest over the past ten years would have higher yields at an average of 10.5 per cent for large-cap funds. Recurring deposits pay lower interest than fixed deposits, widening the gap between equity and debt. The average SIP return for large-cap equity funds is also higher than the Nifty 50 or the Sensex which delivered yields of 8.2 and 7.9 per cent in the past ten years.

Four, for long-term horizons such as 10 years, large-cap equity must be mixed with mid-cap funds as well. Mid-cap funds in the last ten years delivered an annual average return of 13.2 per cent. The best fund returned a good 18.8 per cent. A monthly SIP would have yielded 16.7 per cent on an average. So, including mid-caps to the extent of 20 per cent of a portfolio will yield, on an average, a return of 12 per cent.

Keeping it realistic

Equity does deliver returns superior to debt, as we have seen. But it’s also important to have realistic expectations while investing in equities. For one thing, while in one year, the market can soar (as it happened in 2007 and 2009, when the Nifty 50 moved up by over 50 per cent), over the long term, the returns even out. Market lows inevitably follow such booms.

For another, an equity mutual fund invests in a basket of fundamentally sound stocks, to keep risk diffused and bring in a balance of risk and return. Most individuals invest in mutual funds because they do not have the time or expertise to identify stocks that will multiply several times. Nor do they have the risk appetite that is required for direct stock investments. Therefore, even if a stock happens to be a multi-bagger in a ten or fifteen year period, a fund is not going to have its entire portfolio in that stock. The fund’s returns will thus be lower than those star stocks.

In any case, stocks that are fundamentally sound with good corporate governance that jump multi-fold are not common. In the past 20 years, the Sensex has returned an average of 13.8 per cent in any ten-year period. It would be unrealistic, then, to expect annual returns of 30 or 40 per cent from equity over the long term. While building portfolios and estimating returns equity will bring in over the long term, an average of 12 to 15 per cent is appropriate and an acceptable figure.

Therefore, take heart that equities have not, and will not, let you down as long as you hold for the long-term and keep your expectations realistic.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

It is good and nice to see that some one has given a rebuttal answer to the ‘famous’ / ‘infamous’ / ‘misleading’ newspaper item. The news item was completely wrong. You cannot compare a debt denominated instruments’ return v/s a category average return.

In fact, a debt instrument can never beat a riskier equity investment return over a long period of time. The wide is more glaring when comparing the returns ‘after-tax’.

I perfectly agree with the tax argument. Bank term deposits are taxable and returns from equity are tax free after one year and dividends are also tax free in the hands of investor. But good things END there. Equity investment will give you better returns if held for LONG term is the most common method to fool yourself. I invest in equity mutual fund for diversification and have very little hopes from my equity investments. For my core portfolio like retirement planning I prefer ppf and nps (debt option). For my child’s education also fixed deposits are more advisable. Worst thing about equity/ equity funds is the SELECTION step because selecting right funds/ stocks is the REAL game and secondly you can NEVER predict which way markets will move. So frequently it is seen that when you need funds the most then only markets are passing through a rough patch. Giving a secured guaranteed tax free return is difficult for banks/ Government. Hence Government as well as lots of EXPERTS keep you pushing towards equities. Remember the so called experts and everyone will benefit if more people are investing in equity. My suggestion will beas pointed in article also BE REALISTIC. Do NOT day dream that by investing as low as 1500-2000 in equities per month you can become crorepati and use predictable instruments for meeting major expenses like retirement and children education.

Hello sir,

Really appreciate your feedback! We agree with you on points you have made. Simply investing in equity will not guarantee high sums! All funds will not give you good returns; as we said in the article, selecting a fund that beats both benchmark and category consistently is important. You are also very correct in saying that investing small sums will not make one a crorepati.

We’d also like to make a few points. One, the problem with relying on fixed deposits apart from the taxation, is that the amount you have to save to meet your goal increases as the returns are lower. Given that people have multiple goals running at the same time – retirement, education, etc – it is best to use the leeway in terms of time horizon for long term goals to earn higher returns and save relatively lower sums than in FD. Two, you also need an asset-allocated approach and not put all your investments in equity either, so debt investments are absolutely necessary. PPF here is better than FD because among all debt products, it delivers the highest return because of its tax efficiency. You can also consider debt mutual funds. Three, as you approach your goal, the prudent thing to do would be to gradually shift out of equity and put it into debt. This will address to a good extent the concern that markets will tank just when you need the money. When you have invested for years together, this gradual shifting will not hurt your returns very greatly.

Thanks again for your inputs,

Bhavana

I perfectly agree with the tax argument. Bank term deposits are taxable and returns from equity are tax free after one year and dividends are also tax free in the hands of investor. But good things END there. Equity investment will give you better returns if held for LONG term is the most common method to fool yourself. I invest in equity mutual fund for diversification and have very little hopes from my equity investments. For my core portfolio like retirement planning I prefer ppf and nps (debt option). For my child’s education also fixed deposits are more advisable. Worst thing about equity/ equity funds is the SELECTION step because selecting right funds/ stocks is the REAL game and secondly you can NEVER predict which way markets will move. So frequently it is seen that when you need funds the most then only markets are passing through a rough patch. Giving a secured guaranteed tax free return is difficult for banks/ Government. Hence Government as well as lots of EXPERTS keep you pushing towards equities. Remember the so called experts and everyone will benefit if more people are investing in equity. My suggestion will beas pointed in article also BE REALISTIC. Do NOT day dream that by investing as low as 1500-2000 in equities per month you can become crorepati and use predictable instruments for meeting major expenses like retirement and children education.

Hello sir,

Really appreciate your feedback! We agree with you on points you have made. Simply investing in equity will not guarantee high sums! All funds will not give you good returns; as we said in the article, selecting a fund that beats both benchmark and category consistently is important. You are also very correct in saying that investing small sums will not make one a crorepati.

We’d also like to make a few points. One, the problem with relying on fixed deposits apart from the taxation, is that the amount you have to save to meet your goal increases as the returns are lower. Given that people have multiple goals running at the same time – retirement, education, etc – it is best to use the leeway in terms of time horizon for long term goals to earn higher returns and save relatively lower sums than in FD. Two, you also need an asset-allocated approach and not put all your investments in equity either, so debt investments are absolutely necessary. PPF here is better than FD because among all debt products, it delivers the highest return because of its tax efficiency. You can also consider debt mutual funds. Three, as you approach your goal, the prudent thing to do would be to gradually shift out of equity and put it into debt. This will address to a good extent the concern that markets will tank just when you need the money. When you have invested for years together, this gradual shifting will not hurt your returns very greatly.

Thanks again for your inputs,

Bhavana

Very realistic picture given… Especially the SIP figures are very informative. Also the fact that post tax return on Debt can never compete with equity due to capital gains light tax structure that we have, is nicely brought out.

Thank u for this.

Very realistic picture given… Especially the SIP figures are very informative. Also the fact that post tax return on Debt can never compete with equity due to capital gains light tax structure that we have, is nicely brought out.

Thank u for this.

Very realistic picture given… Especially the SIP figures are very informative. Also the fact that post tax return on Debt can never compete with equity due to capital gains light tax structure that we have, is nicely brought out.

Thank u for this.

There is no option to share these useful articles via WhatsApp/Hike.

Hello Bhavana

I invested in Hdfc top 200 and hdfc equity with a horizon of 25 years as well SBI emerging businesses- all SIP mode. should i continue with them. your select list does not mention them why.

are they below par funds. i am a long term saver and value HDFC house

Hello Mandeep,

HDFC Top 200, while being an underperformer, has a good track record and has done badly partly because they follow a long-term value-based strategy which hasn’t worked. Because there are better performers, we removed it from our Select list some time ago. SBI Emerging Businesses is a high-risk fund – its benchmark agnostic and highly concentrated, and does not fit most investor portfolios. It also does not do well on consistency in beating its category. So for portfolio-specific advice, please log into your FundsIndia account and schedule an appointment with your advisor. Calls on whether or not to stop SIPs in a fund also depends on the other funds you hold. Also, if you stop SIP in one fund, you must start it in another to maintain your savings.

Thanks,

Bhavana

Hi Bhavna

Would you like to say something on ( what is your advice ) in HDFC equity fund. I started SIP in this fund because of it’s long track record, diversified nature and the fund manager Prashant Jain. At that time my thinking was that one should check past performance of fund as well as fund manager. Now Prashant Jain is still managing HDFC equity fund and it is still a diversified fund BUT NOT performing. Should I wait more or stop SIP. I am running out of patience with this fund. What’s the problem here I simply cannot understand.

Hello,

HDFC Equity typically does very well when markets are rising and does poorly during corrections. This aside, HDFC Equity has suffered from the same stock or sector choices that other HDFC funds have in the past year, because of a valuation stance and the long-term calls that the fund house takes. If expectations regarding growth pan out, returns may pick up. Deciding whether to stop a fund depends on when you started investing in it as well. For portfolio and fund-specific advice, please use your FundsIndia account to schedule an appointment with your advisor.

Thanks,

Bhavana

thanks

so are you telling to move from HDFC house to another fund even though for a horizon of 25 years.

how do you value HDFC Equity

Hi Mandeep,

Let me explain one point first. Just because one has a long-term horizon, it doesn’t mean you continue investing in an underperforming fund for the entirety of that horizon. You can stop putting fresh money in that fund, but continue to hold it. That is a call that has to be taken on a case-to-case basis. Now coming to your question. When you started investing in the fund matters, as well as the other funds you hold, before giving any call. For such portfolio-specific advice, request you to please schedule an appointment with your advisor through your FundsIndia account.

Thanks,

Bhavana

thanks

so are you telling to move from HDFC house to another fund even though for a horizon of 25 years.

how do you value HDFC Equity

Hi Mandeep,

Let me explain one point first. Just because one has a long-term horizon, it doesn’t mean you continue investing in an underperforming fund for the entirety of that horizon. You can stop putting fresh money in that fund, but continue to hold it. That is a call that has to be taken on a case-to-case basis. Now coming to your question. When you started investing in the fund matters, as well as the other funds you hold, before giving any call. For such portfolio-specific advice, request you to please schedule an appointment with your advisor through your FundsIndia account.

Thanks,

Bhavana

Hi,

if we invest directly in to secondary markets, without going through SIP route, how should one build their own portfolio. Which are the most important parameters, to be taken care.

Hi Mitesh,

If you’re directly investing in equities, you need to have the time to do the research on stocks and the time to maintain it. It requires far more effort to directly invest in equities than the MF route. When you’re stock-picking, go for fundamentally healthy stocks, those that have seen MF buying (they have a better record than FPIs at picking winners). Try to avoid stocks with governance issues, but you will have to do a good bit of reading to find this out. Those with high debt are also best avoided. Also, invest with a horizon in mind – longer term investments require fundamentally sound companies.

SIPs in stocks is not a good idea – it builds concentration in a single stock (in a mutual fund, you’re buying a basket of stocks, which will also be actively managed), it hinges entirely on your ability to pick a stock that will deliver very high returns, and if your stock has changed fundamentally, you would be throwing good money after bad.

Thanks,

Bhavana

Hi,

if we invest directly in to secondary markets, without going through SIP route, how should one build their own portfolio. Which are the most important parameters, to be taken care.

Hi Mitesh,

If you’re directly investing in equities, you need to have the time to do the research on stocks and the time to maintain it. It requires far more effort to directly invest in equities than the MF route. When you’re stock-picking, go for fundamentally healthy stocks, those that have seen MF buying (they have a better record than FPIs at picking winners). Try to avoid stocks with governance issues, but you will have to do a good bit of reading to find this out. Those with high debt are also best avoided. Also, invest with a horizon in mind – longer term investments require fundamentally sound companies.

SIPs in stocks is not a good idea – it builds concentration in a single stock (in a mutual fund, you’re buying a basket of stocks, which will also be actively managed), it hinges entirely on your ability to pick a stock that will deliver very high returns, and if your stock has changed fundamentally, you would be throwing good money after bad.

Thanks,

Bhavana

I am trying to build an ideal mutual fund all weather high return portfolio for so many long years and not able to do so yet. More I read more I discover my ignorance. I will never advice directly investing in secondary market. Even as initially I used to always invest directly, then I was young and used to think if I invest directly I could beat returns generated from mutual funds and direct investing after thorough homework is the key to real big money.

Thanks Bhavna for elaborating your views on HDFC equity.

I am trying to build an ideal mutual fund all weather high return portfolio for so many long years and not able to do so yet. More I read more I discover my ignorance. I will never advice directly investing in secondary market. Even as initially I used to always invest directly, then I was young and used to think if I invest directly I could beat returns generated from mutual funds and direct investing after thorough homework is the key to real big money.

Thanks Bhavna for elaborating your views on HDFC equity.

There is no option to share these useful articles via WhatsApp/Hike.

Very realistic picture given… Especially the SIP figures are very informative. Also the fact that post tax return on Debt can never compete with equity due to capital gains light tax structure that we have, is nicely brought out.

Thank u for this.

It is good and nice to see that some one has given a rebuttal answer to the ‘famous’ / ‘infamous’ / ‘misleading’ newspaper item. The news item was completely wrong. You cannot compare a debt denominated instruments’ return v/s a category average return.

In fact, a debt instrument can never beat a riskier equity investment return over a long period of time. The wide is more glaring when comparing the returns ‘after-tax’.

Hello Bhavana

I invested in Hdfc top 200 and hdfc equity with a horizon of 25 years as well SBI emerging businesses- all SIP mode. should i continue with them. your select list does not mention them why.

are they below par funds. i am a long term saver and value HDFC house

Hello Mandeep,

HDFC Top 200, while being an underperformer, has a good track record and has done badly partly because they follow a long-term value-based strategy which hasn’t worked. Because there are better performers, we removed it from our Select list some time ago. SBI Emerging Businesses is a high-risk fund – its benchmark agnostic and highly concentrated, and does not fit most investor portfolios. It also does not do well on consistency in beating its category. So for portfolio-specific advice, please log into your FundsIndia account and schedule an appointment with your advisor. Calls on whether or not to stop SIPs in a fund also depends on the other funds you hold. Also, if you stop SIP in one fund, you must start it in another to maintain your savings.

Thanks,

Bhavana

Hi Bhavna

Would you like to say something on ( what is your advice ) in HDFC equity fund. I started SIP in this fund because of it’s long track record, diversified nature and the fund manager Prashant Jain. At that time my thinking was that one should check past performance of fund as well as fund manager. Now Prashant Jain is still managing HDFC equity fund and it is still a diversified fund BUT NOT performing. Should I wait more or stop SIP. I am running out of patience with this fund. What’s the problem here I simply cannot understand.

Hello,

HDFC Equity typically does very well when markets are rising and does poorly during corrections. This aside, HDFC Equity has suffered from the same stock or sector choices that other HDFC funds have in the past year, because of a valuation stance and the long-term calls that the fund house takes. If expectations regarding growth pan out, returns may pick up. Deciding whether to stop a fund depends on when you started investing in it as well. For portfolio and fund-specific advice, please use your FundsIndia account to schedule an appointment with your advisor.

Thanks,

Bhavana