If you are sitting down to calculate your gains on debt funds that you had held for more than a year and sold in the just ended financial year, do consider the capital gains index or cost inflation index .

Long-term capital gains

Long-term capital gains (held over a year) on debt funds suffer a 10% tax without indexation or 20% with indexation benefit. In the case of the latter, by indexing, you bring your cost of investment to the current value, after factoring general price rise for consumers.

Given that the capital gains index has been expanding at a good pace (see table below), courtesy inflation, using the index will likely ensure that you pay very little tax or nil tax on your gains.

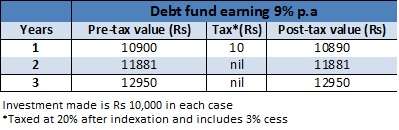

Let us take an example of a debt fund, say an income fund, that you bought for Rs 10,000 in 2011-12. If the fund returned 9% and you sell it for Rs 10,900, your long-term capital gain would normally be Rs 900. A 10% tax on this plus cess would be Rs 93.

But if you index the cost of the same with the CII for 2010-11 and 2011-12 and 2012-13, then the cost would be Rs 10,853.5 (10,000*852/785). So your gain, for tax purposes, would be Rs 46.5 (10,900-10,853.5). A 20% tax on Rs 46.5 will be just Rs 9.3.

With the same return, you may not even have to pay tax if you held the fund for say 2 years or 3 years, as the post-indexation cost will be higher than your sale value. For instance, assuming your returns were the same 9% annually, if you index your cost for 2 years, it would be Rs 11,983, as against sale value of Rs 11,881, resulting in a capital loss for tax purposes.

Hence, make a quick calculation of your gains post indexation before you pay your tax in the next few months.

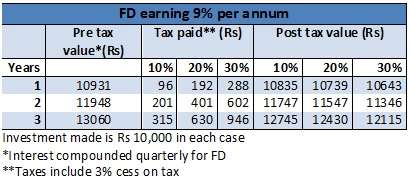

Comparison with FD

See the tables below to know how indexation makes a debt fund a superior post-tax product compared with FD, assuming that they earn the same returns.

It is noteworthy that even if you are in the 10% tax bracket, your post-tax returns would be lower in a fixed deposit. The difference widens if you are in the 30% tax bracket. If you are not a tax payer, only then, you may benefit from holding FDs (depending on whether FD returns are superior or not to debt funds).

HI Vidya,

Please tell me how the units in the Liquid fund considered ? Is it last in first out (LIFO) or FIFO ?

Hi Jinny, It is first in first out. Tks, Vidya

Vidya,

The same applies for equities? I mean in terms of calculating the long/short term gains?

Can we also recover the capital losses in the ITR?

Thank you

Hi Sumit, Hope you know there is no indexation for equity funds as long term gains on equity funds are exempt from tax.

You can set off your short-term capital loss from equity against short-term capital gain of both your equity and debt investments as well as long-term capital gains of debt (pl. note that long term capital gain on equity is exempt from tax. hence you cannot use it for set off purposes). Tks, Vidya

Hi Vidya,

Did you mean that we can set off a short term loss from equity with a long term gain on DEbt fund?

Lets say I bought shares of XYZ in april 2014 and sell it off in may 2014 booking a loss of rs 1000. Now during the same financial year (2014-2015) if I have a LTCG from a Debt fund of 2000, can I set off the STCL of 1000 incurred in Equity? with that my total tax liability would be 1000 (I took the indexation part away for easy calculation)

Please let me know if my understanding is right

Hi Manjunath, yes, your understanding is right. Vidya

Madam

Would the increase in DDT for Debt funds effect the returns on Growth category Debt funds, if held over one year, either in the hands of the fund or the buyer.

Thank you

Venkat

Hello Venkat, DDT is charged for dividend option of a debt fund. There is no DDT for growth option as there is no dividend paid here. Only the capital gains, at the time of sale will be taxed as usual. Hence, budget does not change anything for growth option. tks, Vidya

Hi Vidya, in the Reports section available in FI can columns for both 10% and 20% with indexation also be added so that we are saved some time looking up the CII and calculating manually? Thanks.

Hi Sheetal,

I suppose you mean the capital gains statement. If so it is meant to merely showcase your gains or loss and not to calculate tax. This is because many people may be availing offs or other tax adjustments and cannot directly calculate tax on the gain. But I shall certainly forward your suggestion to our tech team. Tks, Vidya

How to calculate tax in case of MIPS (say Reliance MIPS) when interest is credited every month

HOw does indexing work in such cases

Thanks

Krishnan

Hello Krishnan, MIPs receive the same tax treatment as any other debt fund.

I am not sure if you meant dividend payout or dividend reinvestment. In both cases, as long as it is long-term capital gain indexation will apply. But it is unlikely that you will have any gain. You will have a capital loss that can be set off against capital gain. But as far as the cost in dividend reinvestment option is concerned, for the additional units allotted, the NAV at which it was allotted (as dividend reinvested units) should be considered for indexing purposes and not the original cost of your investment.

But do remember that your dividends also indirectly suffer tax by way of DDT.

Tks, Vidya

Dear Vidya,

Indexation is something which can benefit lot of debt fund users to a great extent more so if they fall in highest income tax bracket.

However, to my great dismay, there is huge lack of unedrstanding and awareness of this benefit amongst the AMC executives themselves as well as CAMS which services a large chunk of AMCs. The CAMS has been generating a grossly incorrect capital gains statement for my folios for quite sometime (few months). This is because they have been calculating incorrect indexed cost in some cases whereas in some cases (withdrawal from liquid fund after one year) they are not applying indexation at all. I am specifically mentioning this as there was a query from reader askingif it applies to liquid fund as well. If an institution like CAMS does not know this fact, then it is natural for ordinary investors like us to have this doubt.

After a serious follow-up, CAMS has given me telephonic asuanrance to rectify it for one of the AMCs. At the same for another AMC, CAMS executive has intimated me by e-0mail that indexation is not applicable to things other than FMPs.

So those who get enlighetened by Vidya’s article and look forward to availing the indexation benefit, please ensure to prepare an excel sheet for all such investments using the CII table and calculate it on your own. Most of the AMC websites as well as CAMS is generating incorrect and incoherent capital gains statement in case of debt funds. I am yet to analyse similar statements for AMCs services by Karvy.

Regards

Hemant

Hello Hemant, Thanks for sharing your experience. I hope other readers too become sensitised to this issue that you have raised.

The capital gains statement generated by CAMs or Karvy, should best be used for the limited purpose knowing one’s gains. In other words it is a ‘capital gains’ statement and not ‘capital gains tax’ statement. It is best that the investor or his/her auditor does the indexing and tax part and not depend on external parties. Any error, especially understating can prove to be costly.

Tks, Vidya

I think there’a a mistake in the example:

You wrote: “cost of the same with the CII for 2010-11 and 2011-12..”. It should be “cost of the same with the CII for 2011-12 and 2012-13”. The calculation itself is correct, only this text is not…

Thanks for pointing it out Apoorv. it is 2011-12 and 2012-13. I have corrected it. Tks, Vidya

How to calculate tax in case of MIPS (say Reliance MIPS) when interest is credited every month

HOw does indexing work in such cases

Thanks

Krishnan

Hello Krishnan, MIPs receive the same tax treatment as any other debt fund.

I am not sure if you meant dividend payout or dividend reinvestment. In both cases, as long as it is long-term capital gain indexation will apply. But it is unlikely that you will have any gain. You will have a capital loss that can be set off against capital gain. But as far as the cost in dividend reinvestment option is concerned, for the additional units allotted, the NAV at which it was allotted (as dividend reinvested units) should be considered for indexing purposes and not the original cost of your investment.

But do remember that your dividends also indirectly suffer tax by way of DDT.

Tks, Vidya

Dear Vidya,

Indexation is something which can benefit lot of debt fund users to a great extent more so if they fall in highest income tax bracket.

However, to my great dismay, there is huge lack of unedrstanding and awareness of this benefit amongst the AMC executives themselves as well as CAMS which services a large chunk of AMCs. The CAMS has been generating a grossly incorrect capital gains statement for my folios for quite sometime (few months). This is because they have been calculating incorrect indexed cost in some cases whereas in some cases (withdrawal from liquid fund after one year) they are not applying indexation at all. I am specifically mentioning this as there was a query from reader askingif it applies to liquid fund as well. If an institution like CAMS does not know this fact, then it is natural for ordinary investors like us to have this doubt.

After a serious follow-up, CAMS has given me telephonic asuanrance to rectify it for one of the AMCs. At the same for another AMC, CAMS executive has intimated me by e-0mail that indexation is not applicable to things other than FMPs.

So those who get enlighetened by Vidya’s article and look forward to availing the indexation benefit, please ensure to prepare an excel sheet for all such investments using the CII table and calculate it on your own. Most of the AMC websites as well as CAMS is generating incorrect and incoherent capital gains statement in case of debt funds. I am yet to analyse similar statements for AMCs services by Karvy.

Regards

Hemant

Hello Hemant, Thanks for sharing your experience. I hope other readers too become sensitised to this issue that you have raised.

The capital gains statement generated by CAMs or Karvy, should best be used for the limited purpose knowing one’s gains. In other words it is a ‘capital gains’ statement and not ‘capital gains tax’ statement. It is best that the investor or his/her auditor does the indexing and tax part and not depend on external parties. Any error, especially understating can prove to be costly.

Tks, Vidya

I think there’a a mistake in the example:

You wrote: “cost of the same with the CII for 2010-11 and 2011-12..”. It should be “cost of the same with the CII for 2011-12 and 2012-13”. The calculation itself is correct, only this text is not…

Thanks for pointing it out Apoorv. it is 2011-12 and 2012-13. I have corrected it. Tks, Vidya

Dear Vidya,

I am account holder in FundsIndia and a regular reader of ur articles.

I have 8 IFCI 7.85% Infra bonds @ Face value of Rs 5000 i.e.Rs 40000 which was invested in FY 2010-11 for availing tax benefits u/s 80ccf. It had a lock in period of 5 yrs with an option to buyback after 5yrs or sell off. I have taken maximum benefit of 4 bonds in my return.

Recently i checked its value in demat holding. It showed Rs around Rs 32000 per bond. i.e. 6 times its cost in just 2 years.

I had some queries-

How and where can one sell these bonds after 5 years if the price is similar i.e. around 32000.

If it is not sold after 5 yrs, then IFCI will give normal FV and interest thereon to the investor?

Can i sell the bonds which i have excess purchased above Rs 20000 limit now? If yes, then how?

Looking for a positive response.

Thanks,

Amit

Hi Amit, Do you hold the series I (FY-11) 10 year bond with cumulative option? We assume it is , going by the coupon rate you have mentioned.

I checked their current market price in BSE. It was Rs 6000 a bond. That roughly tallies with 2 years of accumulated interest on it. Pl. check as to how their price is captured in demat. Many of the debt instrument prices cannot be captured properly as they are hardly traded in the retail debt market segment.

As these instruments are very thinly traded in the stock market and is hence not easy to get out by trading in the market. You can try checking with your broker about its tradability after 5 years. But remember you will have capital gains tax if sold in the market.

Details of the buyback and the amount you will get are given by IFCI in this link: http://www.ifciltd.com/InvestorsSection/Bondholders/InfrastructureBonds/SeriesI.aspx I hope this is the series you applied for. There are multiple series that the company issued.

tks

Vidya

Dear Vidya,

Thanks for the reply.

Yes i have the same bonds cumulative option but with buyback option after 5 yrs.

However the value of one bond as per CDSL today is shown as Rs 30958/- Please click the link below:

http://www.cdslindia.com/investors/popup-isin.jsp?isin_code=2336-2496-2208-1536-1632-1824-2080-1536-1792-1568-1600-1600&isin_name=IFCI%20LTD-7.85%UNSEC%20RED%20IFCI%20LONG%20TERM%20INFRA%20(BUYBACK/CUM)%20NCB%20SR-I%20OPT-II%20PN%20PP%20LOA-RD%20DT15.09.2020

Its really strange that the value of bond has shot from Rs 5000 to Rs 30958 in just 2 years even if it is thinly traded?

How can BSE show different price than CDSL? Further, my application to convert my demat account into BSDA account was rejected as they told my portfolio value is above Rs 2 Lakhs solely because CDSL captured value of IFCI bonds Rs 2.4 lakhs as compared to Rs 40000/- (cost).

Further, do brokers like indiabulls really help in selling these tax saving bonds even if we have not bought it through them?

Thanks,

Amit

Hello Mr Amit, Thanks for the further details given. I was looking at the wrong series. The data your provided helped me check the right one: http://www.bseindia.com/stock-share-price/ifci-ltd/ifci150910b/972609/

As you said, it is indeed at Rs 30958 and odd. But the last traded price was aug 2012 after which trading has been suspended. i believe there has been some freak trade that has resulted in the price jumping and therefore also causing suspension. You will not be able to sell it for now. You may watch out for revival in trade ..check the BSE website (debt section) with scrip code 972609. In any case your lock-in is 5 yrs as it is an infra bond.

Now, your question on selling – if you have a demat account, there must be a brokerage house/bank through which you would have opened the demat. If you are going to sell in the open market, you can do so only with a brokerage account. Hence, check with them to see if they evince interest (when you decide to sell after 5 yrs) in helping you put through this trade. Otherwise, simply hold and get the payment directly by opting for buyback. But be assured that the amt captured here is artificial and will not be the amount you will get. As to why this happened, you will have to contact CDSL or IFCI to know details. tks, Vidya

Thanks Vidya for the elaborate reply..

Another query-

If an individual want to invest in some instrument apart from equity, may be mutual fund, bond, debenture etc.. which one you will recommend in the current market scenario with a investment horizon of 2 years. If an individual is in 20% tax bracket, then max one can expect 7%(post tax) returns from FD. However if he desires to better the post tax returns to atleast around 10% considering liquidity is not a concern, which instrument you will recommend? Less exposure to equity is desired.

Thanks,

Amit

Hello Amit, Post tax of 20%, FDs will yield 6.8-7% now. Bonds and debentures with good credit rating may deliver only very marginally higher than this in a falling interest rate scenario.

But you can expect marginally higher returns from income funds. However, your returns of 10% may be tough to achieve in a pure debt fund. Even if we consider debt-oriented funds like MIPs, this returns is possible only when equities perform well. Given the current scenario, 2-years is too short a time frame to say whether this is possible with certainty with 25% equities. Fortunes of equities will solely determine returns and that is a tough forecast to make at this stage. In general, in the short term return expectations are best kept muted. – tks, Vidya

Thanks Vidya…

What are income funds exactly?

Further can FMP be a better option?? Indexation benefit is available so that the CG minimizes a lot…Ofcourse we have missed double indexation benefit available in last week of march..

Thanks,

Amit

Hi Amit,

1. Income funds are a class of debt funds that try to manage their credit and itnerest rate profile based on debt market scenarios. The article I quoted has everything about income funds. I am quoting from that, but do pl. take a look at it:

“Income funds are a class of debt mutual funds that invest in a combination of government securities, certificates of deposits, corporate bonds and money market instruments. They are managed by expert fund managers who actively try to manage the portfolio based on interest rate movements, while at the same time keeping the portfolio credit worthy.

In other words, they seek to generate returns both in declining and rising interest rate scenarios by managing their portfolio actively. They either generate interest income by holding the instruments till maturity or manage gains by selling them in the debt market if the price of the instrument rallies well.

That means that these instruments will not guarantee you fixed returns like deposits. Yet, over the last 10 years, they have beaten three-year deposit rates, irrespective of the year in which you invested. Let us look at income funds’ features and how they score over fixed deposits.”

2. Income funds can be better options to FMPs if your risk appetite is slightly more. FMPs decide the instruments to invest in and hold them till maturity while income funds dynamically manage the portfolio based on interest rate movements. FMPs are close ended while income funds do not have such lock-in. They are open ended and may at best have exit load if exited before specified time period. Income funds too (for that matter all debt funds) have indexation benefits if held for more than 1 year. Double indexation benefit will be available for any debt fund you invest towards close of financial year and not just FMPs. Just that FMPs with a 370 or 400 day tenure are timed just before FY-ending to highlight double indexation benefit. Youc an d the same by investing in a regular open-ended debt fund. Tks, Vidya

Hi Vidya,

When redeeming the debt funds after 1 year or more does investor have the option to choose – with/without indexation being applied on his investment ?

Thanks,

Nimesh

Hello Nimesh, yes, you have the option to choose whether to go for indexation or not. tks, Vidya

Hi Vidya,

I had a question, How can we go for the indexation option, how can I communicate to the AMC. For eg I have invested in sbi mf so what I need to do to work out the indexation.

Hi Debojyoti, You need not communicate it to the AMC. If you hold for more than 1 year, you need to decide whether to go for 10% capital gains tax (on the gain), without indexation or index it and tax at 20% (pl search on the internet, you will get enough dope on how to index the cost using the capital gains index). The AMC is not going to deduct capital gains tax and hence it is for you to do it. As for knowing what is you gain, if you have a FundsIndia account, you wills ee the gain classified neatly as short term or long term. Thanks.

Hello Vidya – My question is not related to this post may be. But would you be able to tell me how long-term RDs are taxed? i assume there is no TDS on RDs and only interest is taxable, if this is true, then how exactly the tax will be calculated? Will the interest earned be included in my yearly income and will be taxed as per the tax slab applicable? please let me know, many thanks in advance

Hi Saurabh, Interest on RD does not have TDS but is taxable. The interest, in the year of maturity, is added with your total income under the head ‘income from other sources’ and taxed according to your slab rate. There is no separate tax treatment. You will either have to disclose it to our employer as part of other income or pay your own self assessment tax before or when you file your annual tax returns. tks, Vidya

Hi Vidya,

Extremely good and Timely post. I have 2 questions: –

I have setup STP from FundsIndia on various debt funds (Daliy Dividend) to respective Equity Fund in the same fundhouse. If I convert the Dividend funds to Growth Funds, Will the STP have to be recreated and what will be the taxation situation considering:

1. STP begins for the next week onwards

2. STP begins after 1 year

Regards,

Anjani Singh

Sir,

Converting from dividend to growth option is like exiting and entering afresh. Hence, check for capital gains etc, if any (unlikely since you have a daily dividend running). Yes, you will have to stop the STPs and start a fresh STP on the growth option of the debt funds.

1. as far as the debt fund is concerned the day of moving them to the growth option will be the date of purchase. Any exit/STP from the fund within one year of such purchase (as growth fund) will be taxed at your income tax slab rate.

2. If the transfer is made after one year, the tax will be 10% without indexation or 20% with indexation. But pl. remember in case you put more money in the debt fund later, the order of exit/transfer is first in first out. Money which came in first will be treated as having exited first.

tks,

Vidya

Hi,

As and NRI status i do hold couple of Debt/Liquid funds.How do i take the advantage of indexation.This can be done while filing return or is there any way out.But the problem is as soon as we sell any units it proceeds is net of TDS.Please advise.

Hello Vishal,

TDS is deducted flat by the AMC. There is no way they are going to consider indexation benefit. Hence, it is for you to compute your actual gains and tax after indexation at the time of filing returns. This is indeed a limitation as often times your actual tax (after indexation) would be lower than the TDS and entail a refund, if you do not have too many other sources of income here. Tks, Vidya

Hi,

Thanks for the nice article. I have two queries.

1. Can we calculate the capital loss if the indexed value is more than the returns in debt funds on long term investment in ITR.

2. If i purchase a debt fund in March 2011 and sold it in April 2013, I have to calculate indexation for two years or three years.

Thanks,

Aswanth

1. yes, you can have a situation of capital loss if the sale value (total proceeds you get from selling units) is less than the indexed cost. But such loss can be set off only against other capital gain and not against your regular income.

2. You will get benefit for 3 years.

Tks

Vidya

Hi,

Was planning to invest fd amount in Birla Medium term plan for time frame of 2 years. shall i proceed.

what can be other options.

I am looking for return of 9- 9.5 post tax.

Thanks

Hi Barkha,

I hope you are aware the Birla Sun Life Medium Term Plan is a high risk fund given that it takes credit risk. Hence, it is not a substitute for FDs.

Pl. read our review on this fund, in case you wish to know more: https://blog.fundsindia.com/blog/mutual-funds/fundsindia-reviews-birla-sun-life-medium-term-plan/1778

Based on this fund’s current returns, a post-tax return of about 9.0-10% (if you hold for more than 1 year) may be feasible. In FD you post-tax return at 30% tax would currently be about 6.4% for 2 years (interest compounded quarterly and under cumulative option) For fund suggestions, kindly use our Ask Advisor feature (in your FundsIndia account) and give your detailed requirement so that our advisor can write back or talk to you.

Tks,

Vidya

Hi,

Time frame can be 1 year minimum -2 years or even longer.I was withdrawing the bank interest quarterly hence i expect same in mutual funds. I would be satisfied with 9+ returns.

Please suggest me the funds.

Hi Barkha,

Pl. be aware that there can be no surity in returns like the way banks give. We only go by the portfolio and present performance of the funds. Also, remember, you cannot rely on mutual funds to declare assured returns every month or quarter. they may declare based on surplus, but there is not mandate to declare. Hence, while mutual funds are ideal for wealth building (that is buy and hold for long term, without wanting any regular income in between), if you wish regular income payout then you should allow the fund to grow for a couple of years and then use a systematic withdrawal plan, where you get to take a fixed amount out, every month or quarter. Fund suggestion requires, knowing risk appetite, current investments, time frame and investment amount. Hence, we normally take fund questions through our Ask Advisor Feature (mail or schedule a call), which is available free in your FundsIndia account. Tks, Vidya

Hi,

How do we pay any such tax on debt funds? Do we have to file IT return using some special form? Can you give an example of such return with details to be mentioned in there?

Thanks

Hello Kumar,

At the time of filing your returns (before due date), you will have to pay self assessment tax on any gain you have in debt funds (it is like any other tax you will pay on other income such as interest income etc). Your ITR V form, online or offline will have a provision to submit details of capital gains. You can also use the tax calculator available in the iNcome tax dept. website: http://law.incometaxindia.gov.in/DIT/Xtras/taxcalc.aspx

Im looking for example of sample filled ITR2 with calculations.

Can you provide an example of sample filled ITR2 with calculations please?

Hello Kumar, We do not have any sample. You may kindly refer this article to know to fill ITR2. http://taxguru.in/income-tax/how-to-fill-and-file-income-tax-return-itr-2.html

Tks, Vidya

Hi Vidya, how do we decide whether to use index or without index for calculating long term capital gains for any asset? From where can we get index values for the applicable years?

Hi Kumar,

All you need to do is index your cost first (cost*index value in yr. of sale/index value in yr. of purchase). Refer our article for index values: https://blog.fundsindia.com/blog/mutual-funds/make-use-of-indexation-benefit-for-debt-funds/1971. If your sale value less indexed cost is a loss, you simply need to take indexation benefit. If this is a profit, then calculate 20% tax on this. Then, without indexing, calculate 10% of capital gain (sales value less cost).

If the 20% tax on capital gains after indexation is lower than the 10% tax (without indexation), then you need to go for indexation.

tks

Vidya

We get to choose whether to use indexation or calculate without indexation? Are returns always better with indexation?

Hi Kumar, yes you have the option of choosing. Indexation need not be always better. It depends on whether the inflation index is growing high every year. If inflation index is flat (in periods of very low inflation), you may not benefit much.

Vidya

Would it be wise to sell blue chip shares and reinvest in debt funds in the current scenario – as a long term investment are the shares better or are debt funds better ?

Hi, as a long-term investor, bluechip shares will make immense sense over debt. We would not recommend that you sell blue chips for debt. But ensure you always have a good mix of equity and debt to provide good hedge and reap benefits from both. Tks, Vidya

Vidya, can you recommend some debt fund please with horizon of 1 to 1.5 yrs?

Hello Kumar, You may pl. refer http://www.fundsindia.com/select-funds to choose a debt fund for the time frame you have mentioned.Tks, Vidya

Vidya, can you recommend some debt fund please with horizon of 1 to 1.5 yrs?

Hello Kumar, You may pl. refer http://www.fundsindia.com/select-funds to choose a debt fund for the time frame you have mentioned.Tks, Vidya

Hello Vidya, considering that we are in falling interest rate environment, would it be wise to invest in a income fund for 1 to 2 yrs and expecting a post tax return of 10 %.? DO income funds invest in corporate bonds and debentures as well?

Considering that the investor has a lower to medium risk appetite and falls in 10 % tax bracket, which fund (having no allocation to equity) would you recommend ?

Thanks, Sumit

Hello Sumit,

Thanks for writing in.

In general, irrespective of interest rate cycle, income funds require a 2-3 year time frame to deliver well with limited risk. In the time frame you mentioned short-term funds are a better choice. A 10% return may be possible in exceptional interest rate fall cycle (where rates fall sharply triggering price rally). But as we are likely to have a gentle slide hereon, this returns is possible only when funds take credit risk too. Very few funds do that. So to answer your question, is its not too easy.

Yes, income fund very much invest in corporate bonds and debentures. In fact that is typically their largest holding.

You may refer to our select funds http://www.fundsindia.com/select-funds to choose your funds from our select list or alternatively use our Ask Advisor feature on the net (available for all our investors) so that our advisors can help determine the right funds for you.

Thanks, Vidya

Hello Vidya, considering that we are in falling interest rate environment, would it be wise to invest in a income fund for 1 to 2 yrs and expecting a post tax return of 10 %.? DO income funds invest in corporate bonds and debentures as well?

Considering that the investor has a lower to medium risk appetite and falls in 10 % tax bracket, which fund (having no allocation to equity) would you recommend ?

Thanks, Sumit

Hello Sumit,

Thanks for writing in.

In general, irrespective of interest rate cycle, income funds require a 2-3 year time frame to deliver well with limited risk. In the time frame you mentioned short-term funds are a better choice. A 10% return may be possible in exceptional interest rate fall cycle (where rates fall sharply triggering price rally). But as we are likely to have a gentle slide hereon, this returns is possible only when funds take credit risk too. Very few funds do that. So to answer your question, is its not too easy.

Yes, income fund very much invest in corporate bonds and debentures. In fact that is typically their largest holding.

You may refer to our select funds http://www.fundsindia.com/select-funds to choose your funds from our select list or alternatively use our Ask Advisor feature on the net (available for all our investors) so that our advisors can help determine the right funds for you.

Thanks, Vidya

Thanks for this article. I am little new to investing in funds so please pardon my ignorance. Who would do this indexation for tax returns? Is it me? Also, do you suggest there are 2 options – 10% long term gains tax or 20% with indexation? It left me little confused.

Hi Sunil, Yes, you will be the one choosing which option to go for – that is 10% without indexing or 20% with indexing. The best way to find out is to calculate. The time period of holding and how inflation index has grown will determine which one of these options is better. On years when the inflation index is very growing slowly, then the 10% option may turn out to be better. Take a look at the example in the article to know how tax under the 2 options are calculated.

tks, Vidya

Hi Vidya,

Very well written and super informative. Fundsindia is really lucky to have you.

You said: “The article I quoted has everything about income funds. I am quoting from that, but do pl. take a look at it”

I am not sure about the article. So, posting my very naive query about growth option of income funds:

1) Do they pay dividends?

2) Do they pay periodic interest (maybe annual or more frequent)

If both the above are true, then is it correct to say that the only tax liability will be at the time of selling the fund (capital gains)?

Thanks.

Hello Vikas,

Thanks!

To answer your question:

1. Growth option itself means that no dividends are paid out. The profits are allowed to accumulate

2. There is no concept of interest in mutual funds

The tax liability is certainly the capital gains, which is nothing the profit that accumulates in the NAV.

Thanks, Vidya

Thanks for confirming.

Hi Vidya, I know this might be complicated but can you give us some sense of how the debt fund’s NAV is calculated. Who decides that the NAV should go up if the interest rates go down?

Hi Vikas,

NAVs move based on the value of underlying investments, which could be equity stocks or debt instruments. Hence, if stocks move up, the sum total of the movement in that portfolio is reflected in the NAV. Similalrly, when yields of respective debt instruments falls, their prices rally, thus reflecting in rally in the NAV and vice versa. From this, expenses incurred in managing the fund are deducted and the NAV that you see is captured. Hence, it is only the market – either equity or debt – that decides the NAV ultimately because all the money is invested in equity or debt market.

Thanks

Vidya

Hi,

Trust indexation benefit is also available for redemption of Fund of Funds (FT India Dynamic PE Ratio FoF – Dividend payout option). While the dividends are considered exempt, no STT was deducted at the time of redemption. Therefore, is it ok if I consider indexed costs of acquisition and claim long term capital loss, adjustable against other long term gains.

Regards,

Venkat

Hello Venkat,

FT India Dynamic PE ratio fund is a debt-oriented fund for tax purposes (not all FoF are debt-oriented). Hence indexation benefits are available. There is no STT on debt funds and that does not stop your from claiming indexation benefit. Thanks, Vidya

hello Vidya!

Can the indexation be applied for general term deposits/fixed deposits in a nationalized or private banks?

please send your reply to my mail if possible

Hello Lalith,

Interest from deposits (banks or companies) are not in the nature of capital gains. Hence no indexation benefit is available for them. This is what makes mutual funds a tax-efficient product compared with traditional products

You said indexation benefit is not available for FDs as there is no capital gain. At the same time you said that indexation benefit is available for all debt funds. Does it mean that all debt funds have capital gains including UST, liquid funds and FMPs.

Thanks

Hi Mahesh, Yes, all debt funds very much have indexation benefit if held for more than 1 year. This is what makes them superior to other debt products like FDs from a tax angle. Thanks, Vidya

I have noticed in a bank that they depreciate their interest rate for the deposits tenured 3-5 years. Why is it done? Is it because a deposit locked in for more than 3 years make it long term capital gain and can be indexed?

Hello lalith,

Any interest income under the Income Tax Act is taxed in the respective slab rate. That means they do not come under capital gains purview. You may have to check with the respective bank as to the nature of the product you are mentioning and what is the treatment the bank gives to such product. There is a deposit called capital gains account scheme used for investing any ‘property capital gains’ to save tax. Interest from even this account is taxable like other interest. Hence pl. verify with the said bank. Thanks.

Information provided is simple to understand and adds great value to our knowledge.

Thanks

I sold my old (more than one year old) MIP mutual funds. I got the capital gains statement from cams/karvy website.

Long Term Gain with Indexation is negative while Long Term Gain without Indexation is positive.

1. As Long Term Gain with Indexation is negative, I believe I do not have to pay any tax.

2. Where do I mention value of Long Term Gain with Indexation in ITR-2 form.

Yes, negative means capital loss. Hence no tax. But this can be adjusted against any long-term capital gain. See Schedule CG for capital gains and CYLA for set off, if any. Tks, Vidya

Thanks Vidya for clarification.

One more thing, I have no other long-term capital gain to adjust against for the long-term capital loss. In this case, do I have to put details of long-term capital loss in the Schedule CG, or can I ignore and leave Schedule SG blank?

I checked the ITR – 2 form, I believe I have to fill in details at B2 section of Schedule SG.

a) Full value of consideration

b) Cost of acquisition after indexation

c) Cost of Improvement will be zero in case of Mutual funds?

Thanks

Hardik, If you intend to carry forward the loss pl show it in Sch CFL (details of losses to be carried forward to future years).

Tks, Vidya

Thanks Vidya for clarification.

One more thing, I have no other long-term capital gain to adjust against for the long-term capital loss. In this case, do I have to put details of long-term capital loss in the Schedule CG, or can I ignore and leave Schedule SG blank?

I checked the ITR – 2 form, I believe I have to fill in details at B2 section of Schedule SG.

a) Full value of consideration

b) Cost of acquisition after indexation

c) Cost of Improvement will be zero in case of Mutual funds?

Thanks

Hardik, If you intend to carry forward the loss pl show it in Sch CFL (details of losses to be carried forward to future years).

Tks, Vidya

Hi Vidya,

Thanks for a very clear write up and such prompt responses to queries as well! I have a follow up question to an earlier query posted by someone on Long Term Capital Gains on Debt Funds with Daily Dividend Reinvestment option. Say I purchased 100 units in 2009-10 @ NAV of Rs 10, hence purchase cost Rs 1000. Since it is daily dividend reinvestment, the NAV stayed at Rs 10 and over the last 3 years the no. of units reinvested amount to 30. In 2012-13 I sell all 130 units at the present NAV of Rs 10, hence sale consideration Rs 1300. Questions:

a) Can I apply inflation indexation to the original investment of Rs 1000?

b) Can I also apply indexation to the 30 units reinvested in the 3 years of holding (taking each year’s CII separately)?

c) Will the answer be any different if the result is a loss and not gain?

Hello Nikhil,

1. If your holding is more than 1 year you can apply CII

2. Yes, you can apply on addl. units but get their cost indexed separately. Also do not index addl. units that are less than 1 year. For this short-term capital gain will apply. Hence find out their cost and their Market value (no. of short-term units *NAV on sale) seprately.

3. Loss or gain for tax purposes arises only after indexing (for holdings over 1 year). Hence, the answer will not be different.

thanks

Thank you so much Vidya!

Hi Vidya,

Could you help in how to fill short term gain in form ITR2?

I have 3 different debt funds and I have gains from funds 1 & 2 and losses from fund 3.

All these are short term. Now where do I report these details ?

Thank you

hello Satyanarayana, all gains need to be added with total income and taxes calculated at your usual slab rates, along with salary income etc. thanks.

Hi,

Why comparatively Bank Fds are less return then Mutual funds Debt Funds/FMPs ?

Hi Sumaya, Mutual funds have the flexibility to move their investments according to rate and debt market conditions and may fetch higher returns when such calls favour them. FDs offer only fixed returns and hence there is no such flexibility. Thanks

can u pls elaborate it with examples……

Hi Vidya,

A clarification required. Incase I invest in the FMP’s in the month of March for a 13 or 14 month tenure, Will I get a double indexation benefit??? Have the rules now changed wherein a person can take benefit of double indexation but has to stay invested in the scheme for the entire year rather than exiting in April or May???

Thanks in advance

Hi Rinku, the rule is yet to change. You can get the benefit for now. thanks.

Hi,

please explain how long term capital gains are applied for debt funds if I hold more than an year. Do I have to pay long term capital gain tax for every year for the interest I earned that year? or Do I have to pay only when I sold it? Does the AMC deduct TDS every year if I hold for more than an year?

Hi, LTCG for debt funds held for more than 1 year is taxed at 10% on gains without indexation or 20% on capital gains arrived at after indexing the cost (you may refer the internet for capital gains index and how to calculate). It is taxed only in the year of sale. There is no interest that is taxed. it is only the capital gain. No TDS will be deducted for any mutual fund if you are resident Indian. Thanks.

How should we calculate taxation if I only withdraw some of my money from debt funds after I hold it for more than a year. what is the tax rate if I hold it for less than a year.

Hello sir, Tax will be on a first-in-first out basis. The no. of units * their cost price will be your cost. This will be indexed using CG indexation. Then this value reduced from sale value will be taxed at 20%. You can also choose not to index the cost and opt for a 10% tax on gains. If you hold debt fund for less than a year, it will be taxed in your tax slab rate, whether 10,20,30%. Thanks.

I am looking for one single debt class(just like FD) that will work in all economic conditions(say, high inflation and high growth to low inflation and low growth environment that is, current india and us situations).I don’t have knowledge to shift things when rates / economic situations change. I don’t want to invest in hybrid funds. Can I invest in liquid funds , ultrashort term funds and short term funds? Can I invest in ultra short and short term floating rate funds? how much I lose in the above funds(floating and non-floating) if interest rates are decreased from 8%(india) to 0.5%(USA) in a year? I think you forgot to mention three things in the above article:

1. Only 1 lakh rupees of my money in a bank is safe(combined savings account balance and FDs) unless we have a sheila bair(ex-FDIC chairwoman) who ensures that nobody loses their FDs when banks go bankrupt once the flood gates to banking licenses are given. A bank a day may go bankrupt.

2. FD breaking charges. They will shave 1% of my pre-tax FD money.

3. There is no asset class that truly saves our money (from US treasury(they may not pay interest if they don’t agree on rasing debt ceiling) to real estate). we are back to square one just like old days when there is no capitalistic democracy.

Hello sir, thank you for your comments. Both Ultra short-term and short-term funds will generate reasonable returns with limited (when I say limited there could be some short-term volatility which tends to normalise itself if held for the duration for which the fund should ideally be held) risks. The chance of rates decreasing from 8% to 0.5% in India is nil. Any dip whether 1 or 2 percentage point at best, will result in a price (NAV) rally in these funds and not a loss.

Thanks

Vidya

Please advise if the losses incurred on sale of tax free bonds are tax deductible.

hi Venkat, If you sell them in the stock market, then any capital losses can be set off against any other capital gain that is taxable. But long-term loss has to be set off against long-term taxable capital gain. Short-term capital loss can be set off against other long or short-term capital gain.

Please advise if the losses incurred on sale of tax free bonds are tax deductible.

hi Venkat, If you sell them in the stock market, then any capital losses can be set off against any other capital gain that is taxable. But long-term loss has to be set off against long-term taxable capital gain. Short-term capital loss can be set off against other long or short-term capital gain.

Hi Vidya. Good article about the benefits of indexation. Is Birla Sun Life Short Term Fund (G) eligible for double indexation? In fact, when and on which document do you have to specify 10% non-indexed OR 20% indexed taxation option? Also, is it too late to benefit from double indexation this year?

Hi Vaibhav, Double indexation is not a separate benefit. It is the capital gains index benefit, you enjoy when you invest for a little over a year but enjoy 2 years’ benefit. So investments made closer to financial year ending (march) and exited soon after the close of the next financial year will enjoy double indexation, although not held for 2 years. yes, all debt funds will get it, based on the timing of your investment.Thanks

Good article..The data is presented well and properly articulated..

http://www.moneymazics.com

Nice post Vidya.

few questions –

a) where do we get the chart from every year.

b) do we have to mentioned somewhere that the tax calculated is after indexation. Eg. in Tax return.

c) what is the generic formula to calculate the present value for funds held for more the 1 or 2 year.

1. You can google to get the index. 2. Yes 3. Cost of fund*index at the time of selling/index at the time of buying the fund.

Dear madam

I have an option of 5 yr fmp from UTI AMC (1825) days pls let me know how many indexation benefit I will getting in this plan and also how effecient it is as compared to FD

pls let me know

thanks

Kutub

hello Sir,

Depending on which date you invested in you will have 5or 6 yrs of indexation benefit when the fund matures. Returns cannot be compared now as it will depend on the underlying instruments’ yield. They are likely to be better than FD on post-tax basis, if inflation remains high and you get high indexation benefits. We do not usually recommend long-term FMPs, given that we will not know the credit risk of instruments for longer tenure. To help us advice you, pl use the free ‘Ask Advisor’ feature if you have your activated FundsIndia account. thanks, Vidya

Hi Vidya.

I invested in a debt fund with monthly dividend option about 23 months back (on 13/4/2012). As of now it has a small gain (in NAV) and I have been receiving dividends monthly.

If I redeem now and apply indexation, instead of gain it is becoming loss,

My questions are.

1. Can i carry forward this long term capital loss?

2. Do I need to account for the dividends I have received in the previous months while showing the loss?

I am asking this because I do not know if dividend stripping is applicable in this case? If I add the dividends I received from this debt fund to the sale proceeds then the result will be back to capital gains (instead of loss).

3. If I do not need to account the prior dividends in sales proceeds and if I can carry forward the losses because of indexation benefits, then I will sell in the next financial year so that there will be higher long term capital loss. Or else I will sell this week itself as I need that money now. Please comment.

Thank you.

Satyanarayana

Hi Satyanarayana,

Yes, you can carry forward the loss and adjust against future gains. But disclose such loss at the time of filing this year to be able to carry it forward.

2. No, you need not account for dividend income. dividends are taxed with the AMC (DDT). You need not account.

3. Dividend stripping prevention provisions kick-in only if a person buys any units within a period of three months before the record date, sells such units within nine months after such date. This is not so in your case. So you can carry forward the loss.

thanks,

Thank you Vidya for such a quick reply, that too on Sunday.

Just to reconfirm from you – so I do not need to add even the last 9 months dividend in the sales proceeds. Right?

Is this because DDT is already paid or is it because I am holding for longer than 12 months?

Thank you.

Satyanarayana

Hi,

1. Because DDT is paid dividend is not taxable at your end, whatever be the tenure. It is exempt income for you.

2. And because there is not dividend stripping, there is no need for adjustment of dividends against capital loss.

Thought I will answer as you may have to take a decision before Fin. yr ends 🙂 thanks, Vidya

How long term capital gain tax calculated in SIP of 2000/month of 5 years in DEBT Fund. Take all amount after 5 years of regular SIP in DEBT Fund ?

I want to count taxation with Indexation. So please help me.

Thanks

Hello Dharmesh,

This link will have the index to be usedhttp://cadiary.org/cost-inflation-index-capital-gain/

If you have help the fund for more than one year, multiply the cost of your fund by index in the year of sale/index in the year of purchase…this will be your indexed cost. Now subtract this from your sale value..that will give you the gains or loss. If gains, cal. tax t 20% plus s.c+cess.

Hello Dharmesh, Every instalment should have completed 1 year to have long-term capital gains indexation benefit. If less than one year, then that part of your units will be taxed at your slab rate. thanks, Vidya

Hi Vidya,

I want to show the LTCG with indexation for my debt funds in the return to be filed for FY 2013-14

that is AY 2014-15.

In the new ITR-2 forms released for AY 2014-2015, the Capital gains section has been changed a lot from last year.

I am not able to see a suitable option for reporting LTCG with indexation for debt funds

Following are the sections in schedule CG for LTCG..

B1 – for land or building (without indexation )

B2 – for bonds or debentures (with indexation)

B3 – for listed securities or units or zero coupon bonds (with out indexation)

B4 – NRI

B5 – NRI

B6 – NRI

B7 – not in B1 to B6 but (without indexation )

So where does one show debt fund LTCG with indexation ? Should I show in B2 only ? as that is the only option with indexation. But its meant for bond & debenture only …

Hi,

This is the form I see and there is a schedule clearly there called CG http://law.incometaxindia.gov.in/DITTaxmann/IncomeTaxRules/PDF/Ay-2012-2013/FormITR2ENG.pdf

Vidya

Hi,

In case of FMP with Dividend payment option, can we also claim indexation benefit on the principal amount and show capital loss?

During the FY year 2014-15, the FMPs divested upto July 10, 2014 have only one option at 10% tax without indexation?

Regards,

Venkat

Hello Venkat, indexation can be claimed for holding of more than 3 years on the investment value less cost..whatever be the dividend paid out. Yes, even if it is a capital loss.

You second question is not clear. If you mean sales made before July 10 2014, then the earlier taxation of no indexation (taxed at slab rate) for less than 1 year and 20% with indexation or 10% without indexation for holding more than 1 year would apply. thanks

Thanks Vidya for your clarifications. The FMP (dividend payout) option was exercised and redeemed after 1 year (but less than 3 years) during the period April 2014 to July 10, 2014.

My query on second part is from the Income tax return (Form 2) under Capital Gains B(3) it is mentioned that

(i) From sale of listed securities(other than a unit) or zero coupon bonds where proviso under section 112(1) is applicable or unit of a Mutual Fund transferred on or before 10-07-2014 (taxable @ 10% without indexation benefit)

Not clear where we need to classify if the individual wants to claim indexation benefit.

Regards,

Venkat

Hello venkat – if you claim indexation (and therefore pay tax at 20%) then such gain after indexation will come in b(ii) under capital gains.

Is there an indexation benefit given in case of a long term switch out transaction?

Hi Monisha, Yes, every every switch if the units are held for over one year (first in first out considered for sale of units) will enjoy indexation. tks, Vidya

Hi vidya,

I really loved your way of response to investors. Its very easy to understand and knowledge on investments. In reference to Union Budget 2014, can you please explain the impact of taxation part of 10% to 20% in debt investments and the tenure has been extended from 12 months to 36 months. Request to explain with example.

Thanks in Advance

Amarnath R

Hi Amarnath,

Thanks.We will soon be sending out a note to all FundsIndia investors on the impact and the strategy to use to over come it. thanks, Vidya

Dear Vidya,

There is confusion about AIR reporting for investment in MF. It is understood that if investment in MF is Rs 2 L or more it will be reported in AIR. I may invest in a particular scheme by way of fresh contribution plus switch in the same scheme from another one and get dividend reinvested in the same scheme. All these put together may be 2 L or more.

The question is whether switching and reivestment is also considered fresh investment within the limit of Rs 2L while reporting, when in reality it is not so.

Seondly, does this limit apply to all schemes/folios in the same AMC put together or to each scheme/folio in the same AMC separately.

Kindly clarify as this invites undue queries and hassle for investor.

Thanks.

Hello Mahesh, You will need the advice of a practicing tax expert for the issue on ‘switch’. The views remain varied. In my personal opinion since the law says ‘payments’ made aggregating to Rs 2 lakh or more, it is on money ‘receipts’ and not units created. But if you face an issue otherwise, you need to talk to the AMC concerned or a tax expert. Two, Rs 2 lakh is for diff schemes/folios of that AMC. So if you have 2 or more schemes in an AMC, the limit will be Rs 2 lakh for all put together. thanks, Vidya

Thanks for your prompt reply.

I presume that your views on Div Reinvestment is same as that on Switch.i.e., limit should not apply to units created and should be on payment recd and therefore should not be applicable to Div Reinv. where units are created.

Kindly confirm.

Thanks.

Mahesh – sorry about the delayed response. Yes, but as I said, the view is entirely personal. thanks

DEAR SIR/MADAM ,

I am NALLANDULARAMYA Sir i am doing in project title(debt funds to ultra short term debt funds ) please data given to me in ultra short term bond . The project data are given below.

1. Introduction of debt funds

2. Review of literature

3.Data collection and analysis -5 years before (companies are:1. edelweiss,SBI ultra short term debt fund,franklin india ultra short term debt fund, L & T ultra short term debt fund ,IDBI ultra short term debt fund )

4. Debt funds formulas and ultra short term debt funds formulas and tools

please its requesting you data provide to me sir,So kindly requesting you sir

Thanking you sir

your sincerely,

NALLANDULA RAMYA

Hello Sir, You will get all the data you need in the respective fund house websites and also in valueresearchonline.com and morningstar.in. thanks, Vidya

Dear Vidya Bala,

I read your all comments. Its are very helpful to upgrade my knowledge.

But I have one doubt…

Suppose I invested rs.100000 in Monthly income plan (debt scheme) on 1-10-2013. And sold half of the investment’s for an amount of rs.62000 on 1-10-2014. What type of gain has I made? And what is the rate of tax applicable?

I want answer for the above question. Please help me..

Thanks in advance.

Hello Premkumar, Sorry for the delay in responding. It would be short-term capital gain and taxed at your income tax slab rate. thanks

Hi Vidya,

Looks like this article needs updates with respect to FY2015-16 Taxation (short term gain) for period less than 3 years. Long term gain wrt beyond 3 years.

Can you please explain it via 1 examples each?

Regards,

Anjani Singh

Anjani, thanks. Done. Have provided link there to an article written post changes on taxation.

Dear Ms Vidya,

I have an active account with your FundsIndia. I need your help in the following matter.

I made a premature exit from NPS (a debt-oriented hybrid scheme. Am I right?) Tier I account on 11-12-2014 and Tier II account on 27-02-2015. Upon exit I was faced with a problem as to how to calculate capital gain (Long Term as well as Short Term) on the 20% of my accumulated wealth of Tier I account (Rs. 5583.83, credited to my bank account on 16-12-2014) and on the entire wealth (a mere Rs. 1410.90 of Tier II account, credited to my bank account on 27-02-2015). (The NPS team has yet not provided me with a capital gain statement. My pension fund manager is ICICI Prudential Life Insurance Company.)

I have now been able to calculate my total gain on Tier I and Tier II accounts with the help of the Transaction Statement I have been provided with).

As for as my gain on Tier II account is concerned, it is clear enough- a mere Rs 410.90-, as my total contribution to this account was a mere Rs 1000, which I had made on 06-09-12. My capital gain on Tier I account comes to Rs 1670.98. (The last time I contributed to this account was on 16-09-13.)

I suppose my gains on both the accounts are short-term.

Now I want to know how I can calculate tax on the total gain (Rs2081.88) and where I should show this figure in ITR 2 (excel) from.

Please help me. (Please tell me also how I can get a capital gain statement from the NPS team or ICICI Prudential Life Insurance Company, or any other source.)

I look forward to hearing from you at your earliest convenience.

Thanking you, in anticipation.

Sincerely, yours

Sanjay Kumar Srivastava

Cell No.: 9794708019

hello Sir,

sorry for the delayed response. As things stand today, nowhere in the IT Act does it state that NPS will enjoy capital gain indexation benefit. Experts view as of now is that it is EET and the ‘T’ implies it i fully taxable on receipt, at your income tax slab rate and therefore added to other income. If you have your NPS account with us, please write to our customer support.They may be able to guide you better on receiving statement from the AMC.

thanks

Vidya

Dear Ms. Bala,

On July 22, 2015, you had replied thus to a query by Mr. Venkat :

“My query on second part is from the Income tax return (Form 2) under Capital Gains B(3) it is mentioned that

(i) From sale of listed securities(other than a unit) or zero coupon bonds where proviso under section 112(1) is applicable or unit of a Mutual Fund transferred on or before 10-07-2014 (taxable @ 10% without indexation benefit)

Not clear where we need to classify if the individual wants to claim indexation benefit.

Regards,

Venkat

Vidya Bala July 22, 2015 at 5:14 pm #

Hello venkat – if you claim indexation (and therefore pay tax at 20%) then such gain after indexation will come in b(ii) under capital gains.”

However, in ITR-2 for AY 2015-16, B2 reads “From sale of bonds or debentures (….)”. Did you, perhaps, mean B7? Although B7 is itself negatively indicated for LTCG “From sale of assets where B1 to B6 above are not applicable” ! Please confirm that LTCG for debt-oriented MFs are covered by B3 (no indexation) and B7 (with indexation).

Thank you.

Prakash

Hello Sir, I meant page 1 here: http://www.incometaxindia.gov.in/forms/income-tax%20rules/2015/itr2_2015.pdf

The details are as you stated in page S3.

i have an investment in debt mutual fund that is” UTI CHILDREN CAREER GROWTH PLAN” which current value is around 70,000/- what will be the tax treatment, please advice me the investment was done in the year 2000

Hello Sir,

If you mean UTI Children’s career Balanced plan, if your holding period is more than 3 years (which is the case), then you will be able to do indexation (using capital gain inflation index) for the cost, and on the gain post such indexation, you will pay 20% tax. In other words, you will get indexation benefit at the time of sale. You can check mroe on indexation here: http://www.bemoneyaware.com/blog/cost-inflation-index/

Vidya

madam,

What would be more beneficial between FD and debt funds in case of non-tax payers.please suggest some good funds.

Regard,

Nishikant

Hello, Sorry for the delayed response. Yes, it is possible for debt funds to beat FDs with marginally higher returns, even if you are a non tax payer. If you are a FundsIndia investor, please write to us through your account and we will understand your requirement and suggest suitable funds. thanks, Vidya

Hello Vidya

There can be transactions as follows in the same scheme of a fund house:

1. div payout to direct div payout

2. div reinv to direct div reinv

3. growth to direct growth

In all above cases will it be considered as switch from one scheme to another where units are first redeemed and redeemed amount is considered as fresh investment. Or it will be considered as change of option in the same scheme without redemption and consequent fresh investment.

Kindly clarify.

Thanks.

Hello Sir, as things stand they will be considered as redemption and fresh investment for tax purposes. thanks, Vidya

Hello Vidya,

Is there any criterion applying which one can figure out when a switch will be considered redemption and fresh investment and when a simple change in option.

Thanks.

Hello Mahesh, Sorry for the delayed response. A switch is always considered redemption for tax purposes. thanks, Vidya

Hi Vidya,

What about auto switch that happens by the fund house itself when they want to merge some schemes ?

I read somewhere that it will not be considered as redemption – to encourage fund houses to merge schemes.

Viral, mergers of schemes are not switches. Switch is when you voluntarily move from one plan to another. That is considered redemption. Howeever, when a fund house merges 2 plans within a scheme, then such transaction is not considered redemption and no capitalgains tax at that point. This was announced in budget 2016.

thanks,

Vidya

Hi Vidya,

Is there a difference in “merger of 2 plans within a scheme” vs “merger of schemes” ?

for e.g.

A. If a fund merges say DHFL short term retail plan & DHFL short term institutional plan – both are of same scheme.

B. If a fund merges 2 schemes, e.g. DHFL short term fund is merged to DHFL money fund.

IN both cases there will be no capital gain tax or only for case A ?

Viral, In both cases capital gains is exempt.

thanks,

Vidya

Hello Vidya,

Is there any criterion where investor can figure out as to when it will be a redemption and fresh reinvestment and when a simple switch.

Thanks

Madam,

I have purchased HDFC debt fund in past. I am first time investor in debt fund, purchased by a agent. I am a senior citizen and not so technology friendly. I had not submitted e-mail id in the fund papers. I recently came to knew after redemption of fund units there is anything like “capital gain statement” to be filed in income tax return. 3 Years of fund about to complete & i want indexation benifit. So how will I have to proceed for getting “capital gain statement”? Should I just ask it from my agent? Or I need to do anything else?

Sir, please ask your agent to help you know what is your long term capital gain. But for indexation, if you cannot do it yourself, seek an auditor’s help. thanks, Vidya

Hi Vidya,

My query is on FMP with Dividend Payout option. Dividends received are tax free on our hands as Mutual Funds have paid DDT at 25+%. My query is whether an investor can claim LTCG loss on the redemption of the principal amount by taking the indexed cost of acquisition?

For instance, I bought Birla Sun Life FMP (Dividend Payout) for 1093 days in August 2012 for Rs.50000/- and received Dividend of Rs.10208/- and got back the principal of Rs.50000/- in Sep 2015. If we taken the indexed cost of acquisition, then the investment works out to Rs.63439/- and so can I claim LT Capital Loss of Rs.13439/-.

Thanks.

Hello venkat, The only issue is that it should not attract the dividend stripping provisions. Please check with you auditor on this. thanks, Vidya

Hello Vidya,

Thank you for this blog and for your prompt responses. I have few queries regarding the debt funds. Requesting your expert advice here.

1. How is the tax calculated on a debt fund with holding period of 30-90 days?

2. How is the tax calculated on a debt fund with holding period of upto 365 days?

3. I understand that post 1 year period, I have an option to either get taxed at flat 10% without indexation or at 20% post indexation. In this case, if I have a SIP going on for a Debt fund, will each SIP be counted as a separate entity and has to complete 1 year period to get indexation benefit?

4. Suppose I start a SIP in a debt fund in August 2016 and withdraw the entire amount in April 2018 thus making total 21 SIPs. Out of these, only 8 would have completed a period of 1 year. How will tax be calculated then?

5. Is there an exit load for the SIPs withdrawn before 1 year period?

Looking forward to your kind guidance.

Regards,

Aman

Hi Aman,

Sorry for the delayed response:

1&2. Debt fund tax calculation is at slab rate for all holdings up to 3 years

3. The law has changed now You are looking at a dated article. It is now slab rate for less than 3 years and 20% with indexation benefit for holding more than 3 years.

4. Apply the same with a 3 year period. Only those instalments that have crossed over 3 years will get indexation benefit

5. Exit load period is different for different fund and applies from the date of your investment. If it is SIP, date of that particular SIP.

thanks, Vidya

Hi Vidya,

If I am an NRI investing in open-ended Debt Mutual Funds, can I avail indexation benefits after 3 years. On most of the Mutual Fund websites, they have mentioned that for unlisted non-equity funds, the tax applicable is 10% without indexation. Are open-ended Mutual Funds listed funds or unlisted funds and will I be able to avail of indexation benefits?

Thanks!

You will have indexation benefits with 20% tax post such indexation for debt funds held for over 3 years. it is the same for NRI and RI. You will however have TDS while RIs will not have.

Hi vidya

I invested in a Gilt fund in march 2012 which I want to redeem now. As I am in 30% tax bracket what tax I have to pay ( assuming STCG) and can I avail indexation benefit?

Thanks

Jiten,

Sorry for the delayed response. If you bough the entire amount in March 2012 then you have crossed 3 years and will have TCG when you sell. You can therefore avail indexation benefit and tax of 20% post that. Thanks, Vidya

I hold unlisted shares of a company at 10 rs per share. Today after 7 years can I sell it at 5 Rs and claim indexation so that my loss in books may be more 5 Rs ?

If your indexed cost is higher than the sale price, such loss can be set off or carried forward against any LTCG that is not exempt.

Resp. Maam,

I have a question regarding redeeming tax saving bonds after lock-in period of 3 years is over. Two government institutions like NHAI or REC are allowd to raise the money through LGCG tax bonds under section 54EC. Since these bonds cannot be traded on any stock exchanges nor can be pledged, how can we redeem the amount invested once the lock-in period of 3 years is over? — Chawla

Hello sir, The maturity proceeds will be given to you automatically at the end of the term. Thanks, Vidya

Resp. Maam,

I have a question regarding redeeming tax saving bonds after lock-in period of 3 years is over. Two government institutions like NHAI or REC are allowd to raise the money through LGCG tax bonds under section 54EC. Since these bonds cannot be traded on any stock exchanges nor can be pledged, how can we redeem the amount invested once the lock-in period of 3 years is over? — Chawla

Hello sir, The maturity proceeds will be given to you automatically at the end of the term. Thanks, Vidya

HI Vidya,

Please tell me how the units in the Liquid fund considered ? Is it last in first out (LIFO) or FIFO ?

Hi Jinny, It is first in first out. Tks, Vidya

Vidya,

The same applies for equities? I mean in terms of calculating the long/short term gains?

Can we also recover the capital losses in the ITR?

Thank you

Hi Sumit, Hope you know there is no indexation for equity funds as long term gains on equity funds are exempt from tax.

You can set off your short-term capital loss from equity against short-term capital gain of both your equity and debt investments as well as long-term capital gains of debt (pl. note that long term capital gain on equity is exempt from tax. hence you cannot use it for set off purposes). Tks, Vidya

Hi Vidya,

Did you mean that we can set off a short term loss from equity with a long term gain on DEbt fund?

Lets say I bought shares of XYZ in april 2014 and sell it off in may 2014 booking a loss of rs 1000. Now during the same financial year (2014-2015) if I have a LTCG from a Debt fund of 2000, can I set off the STCL of 1000 incurred in Equity? with that my total tax liability would be 1000 (I took the indexation part away for easy calculation)

Please let me know if my understanding is right

Hi Manjunath, yes, your understanding is right. Vidya

Madam

Would the increase in DDT for Debt funds effect the returns on Growth category Debt funds, if held over one year, either in the hands of the fund or the buyer.

Thank you

Venkat

Hello Venkat, DDT is charged for dividend option of a debt fund. There is no DDT for growth option as there is no dividend paid here. Only the capital gains, at the time of sale will be taxed as usual. Hence, budget does not change anything for growth option. tks, Vidya

Hi Vidya, in the Reports section available in FI can columns for both 10% and 20% with indexation also be added so that we are saved some time looking up the CII and calculating manually? Thanks.

Hi Sheetal,

I suppose you mean the capital gains statement. If so it is meant to merely showcase your gains or loss and not to calculate tax. This is because many people may be availing offs or other tax adjustments and cannot directly calculate tax on the gain. But I shall certainly forward your suggestion to our tech team. Tks, Vidya

Dear Vidya,

I am account holder in FundsIndia and a regular reader of ur articles.

I have 8 IFCI 7.85% Infra bonds @ Face value of Rs 5000 i.e.Rs 40000 which was invested in FY 2010-11 for availing tax benefits u/s 80ccf. It had a lock in period of 5 yrs with an option to buyback after 5yrs or sell off. I have taken maximum benefit of 4 bonds in my return.

Recently i checked its value in demat holding. It showed Rs around Rs 32000 per bond. i.e. 6 times its cost in just 2 years.

I had some queries-

How and where can one sell these bonds after 5 years if the price is similar i.e. around 32000.

If it is not sold after 5 yrs, then IFCI will give normal FV and interest thereon to the investor?

Can i sell the bonds which i have excess purchased above Rs 20000 limit now? If yes, then how?

Looking for a positive response.

Thanks,

Amit

Hi Amit, Do you hold the series I (FY-11) 10 year bond with cumulative option? We assume it is , going by the coupon rate you have mentioned.

I checked their current market price in BSE. It was Rs 6000 a bond. That roughly tallies with 2 years of accumulated interest on it. Pl. check as to how their price is captured in demat. Many of the debt instrument prices cannot be captured properly as they are hardly traded in the retail debt market segment.

As these instruments are very thinly traded in the stock market and is hence not easy to get out by trading in the market. You can try checking with your broker about its tradability after 5 years. But remember you will have capital gains tax if sold in the market.

Details of the buyback and the amount you will get are given by IFCI in this link: http://www.ifciltd.com/InvestorsSection/Bondholders/InfrastructureBonds/SeriesI.aspx I hope this is the series you applied for. There are multiple series that the company issued.

tks

Vidya

Dear Vidya,

Thanks for the reply.

Yes i have the same bonds cumulative option but with buyback option after 5 yrs.

However the value of one bond as per CDSL today is shown as Rs 30958/- Please click the link below:

http://www.cdslindia.com/investors/popup-isin.jsp?isin_code=2336-2496-2208-1536-1632-1824-2080-1536-1792-1568-1600-1600&isin_name=IFCI%20LTD-7.85%UNSEC%20RED%20IFCI%20LONG%20TERM%20INFRA%20(BUYBACK/CUM)%20NCB%20SR-I%20OPT-II%20PN%20PP%20LOA-RD%20DT15.09.2020

Its really strange that the value of bond has shot from Rs 5000 to Rs 30958 in just 2 years even if it is thinly traded?

How can BSE show different price than CDSL? Further, my application to convert my demat account into BSDA account was rejected as they told my portfolio value is above Rs 2 Lakhs solely because CDSL captured value of IFCI bonds Rs 2.4 lakhs as compared to Rs 40000/- (cost).

Further, do brokers like indiabulls really help in selling these tax saving bonds even if we have not bought it through them?

Thanks,

Amit

Hello Mr Amit, Thanks for the further details given. I was looking at the wrong series. The data your provided helped me check the right one: http://www.bseindia.com/stock-share-price/ifci-ltd/ifci150910b/972609/

As you said, it is indeed at Rs 30958 and odd. But the last traded price was aug 2012 after which trading has been suspended. i believe there has been some freak trade that has resulted in the price jumping and therefore also causing suspension. You will not be able to sell it for now. You may watch out for revival in trade ..check the BSE website (debt section) with scrip code 972609. In any case your lock-in is 5 yrs as it is an infra bond.

Now, your question on selling – if you have a demat account, there must be a brokerage house/bank through which you would have opened the demat. If you are going to sell in the open market, you can do so only with a brokerage account. Hence, check with them to see if they evince interest (when you decide to sell after 5 yrs) in helping you put through this trade. Otherwise, simply hold and get the payment directly by opting for buyback. But be assured that the amt captured here is artificial and will not be the amount you will get. As to why this happened, you will have to contact CDSL or IFCI to know details. tks, Vidya

Thanks Vidya for the elaborate reply..

Another query-

If an individual want to invest in some instrument apart from equity, may be mutual fund, bond, debenture etc.. which one you will recommend in the current market scenario with a investment horizon of 2 years. If an individual is in 20% tax bracket, then max one can expect 7%(post tax) returns from FD. However if he desires to better the post tax returns to atleast around 10% considering liquidity is not a concern, which instrument you will recommend? Less exposure to equity is desired.

Thanks,

Amit

Hello Amit, Post tax of 20%, FDs will yield 6.8-7% now. Bonds and debentures with good credit rating may deliver only very marginally higher than this in a falling interest rate scenario.

But you can expect marginally higher returns from income funds. However, your returns of 10% may be tough to achieve in a pure debt fund. Even if we consider debt-oriented funds like MIPs, this returns is possible only when equities perform well. Given the current scenario, 2-years is too short a time frame to say whether this is possible with certainty with 25% equities. Fortunes of equities will solely determine returns and that is a tough forecast to make at this stage. In general, in the short term return expectations are best kept muted. – tks, Vidya

Thanks Vidya…

What are income funds exactly?

Further can FMP be a better option?? Indexation benefit is available so that the CG minimizes a lot…Ofcourse we have missed double indexation benefit available in last week of march..

Thanks,

Amit

Hi Amit,

1. Income funds are a class of debt funds that try to manage their credit and itnerest rate profile based on debt market scenarios. The article I quoted has everything about income funds. I am quoting from that, but do pl. take a look at it:

“Income funds are a class of debt mutual funds that invest in a combination of government securities, certificates of deposits, corporate bonds and money market instruments. They are managed by expert fund managers who actively try to manage the portfolio based on interest rate movements, while at the same time keeping the portfolio credit worthy.

In other words, they seek to generate returns both in declining and rising interest rate scenarios by managing their portfolio actively. They either generate interest income by holding the instruments till maturity or manage gains by selling them in the debt market if the price of the instrument rallies well.

That means that these instruments will not guarantee you fixed returns like deposits. Yet, over the last 10 years, they have beaten three-year deposit rates, irrespective of the year in which you invested. Let us look at income funds’ features and how they score over fixed deposits.”