If there was one characteristic for the debt market last year, it was the suspense over interest rate direction and the consequent decisions of debt fund managers. More specifically, dynamic bond funds had a tough year, since they aim to make gains by predicting interest rate direction. With better clarity now on rate direction and the beating they took over the past year, dynamic bond funds are shifting strategies into accrual now.

Moving away from rate cut bets

2016 was a good year for dynamic bond funds, especially in the second half as prices rallied on falling yields and high liquidity. The category’s 1-year returns soared into the double digits then. This reversed as the Reserve Bank changed its stance from being accommodative on further rate cuts to being neutral on rates. Over the course of the year, based on data points and RBI commentary, expectations ran the gamut from hikes to cuts.

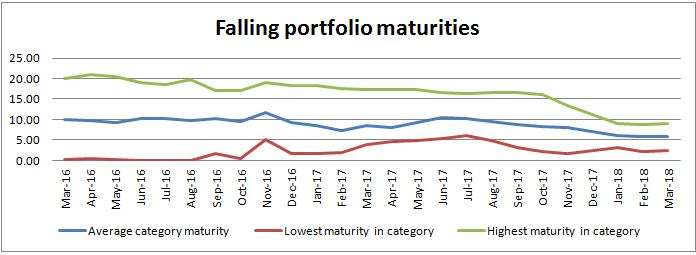

Consequently, some dynamic bond funds rapidly jumped between duration and accrual, some played the middle ground by having a bit of both, and some firmly bet on duration. However, with the sharp rise in yields and the virtual drying up of rate cut expectations at the end of 2017, dynamic bond funds are shifting away from duration. This can be seen from the steady decline in funds’ average portfolio maturities in the past three months especially. We have considered FundsIndia’s dynamic bond category for this article.

Average portfolio maturity is a metric by which to gauge duration play. Since duration can be played mainly through longer term government bonds, a high portfolio maturity indicates that funds are adding gilts on the expectation that rates will fall that in turn trigger bond price rallies. The average share of gilts in dynamic bond funds’ portfolios has also dipped to 39% in March 2018 portfolios (latest available data) from the 60%-plus share in late 2016.

A second indicator that dynamic bond funds are shifting gears is their average portfolio yield-to-maturity. Portfolio YTM indicates the approximate yield on the papers the fund holds. A high gilt share usually results in lower YTMs – funds make money off gilt price rallies and not coupon. A rising YTM and share of corporate bonds, therefore, indicates that the fund intends to earn returns through coupon accrual. Average YTM for the dynamic bond category is at 7.8% for March 2018, a level last seen in mid-2016. For many dynamic bond funds, their latest portfolio YTMs are the highest in two years.

Narrowing differentials

Given the uncertainty over rate direction last year, funds were also very different from each other in terms of strategy. This differential is also reducing now, with even aggressive dynamic bond funds shifting strategy into accrual by adding a higher share of corporate bonds. This narrowing deviation within the category can also be seen in the graph. The changing allocations also look to be having a positive effect on the category’s returns. Going by the 3-month rolling returns since January last year, the category’s average returns have come off the 2017 lows.

Note: This article first appeared in the online edition of Economic Times.