For those of you looking at buying a house for letting out or simply investing in a second house, the tax laws may no longer be that kind to you.

Budget 2017 proposes that any set-off of loss under the head ‘income from house property’ (under Section 71 of the Income Tax Act) against any other income shall be restricted to Rs 2 lakh per annum. The unabsorbed loss can however be carried forward to subsequent years and be set off against any income from house property within 8 years.

Why is this change done and how does it impact you?

First, Rs 2 lakh was the amount allowed as home loan interest deduction if you had a self-occupied property. However, if you rented out a property, your interest claim can be the full interest paid. Thus, those with rented property enjoyed an undue advantage over those who occupied their own property. The law now says, whether a property is self-occupied or let out, you can claim a maximum loss of Rs 2 lakh per year (and the remaining if any can be carried forward) to be set off against any other income for that year.

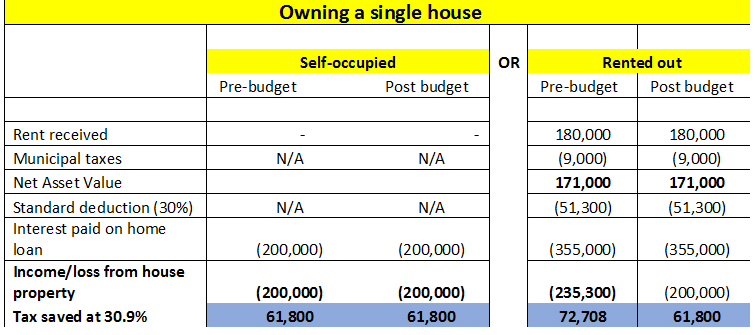

Now look at the table below on what happens to the tax deduction of those who have let out their property. The illustrations below assumes a Rs 15,000 per month of rental income and Rs 40 lakh loan at 9% over 15 years.

The above table is a scenario wherein you own only one house and that is either self-occupied or let out. If it is self-occupied there is no impact. On a property that you let out, you will now have close to Rs 11,000 of tax impact, assuming you are in the 30% tax slab.

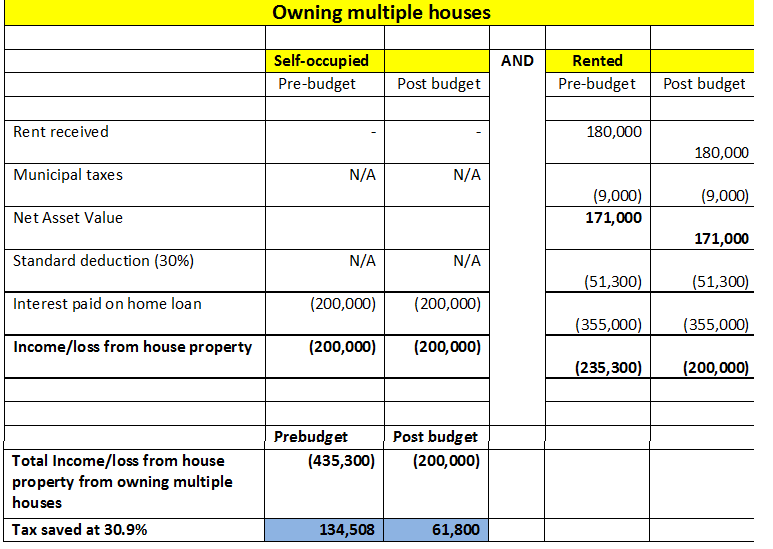

The next table (below) is a scenario where you own more than one house. In this case, one property is deemed to be occupied by you and the rest let out. As the total carry forward loss from house property is restricted to Rs 2 lakh a year, you will see that there is a significant jump in your tax out go.

While it can be argued that carry forward of losses is allowed, it will be possible only if your rental income steeply increases to set off this loss (as you must generate sufficient surplus under this head of income in subsequent years, to set off this loss). To this extent, the change appears to be a deterrent for those who were enjoying high tax benefits from letting our property that was bought with a home loan. In other words, if you were using this provision to set off the losses from your property and significantly reduce your overall taxable income, that may no longer be possible.

There is also an indirect impact on the artificial property prices today, mostly propped by ‘investment’ demand. This change could make property less attractive as an investment option. If that happens, then there could also be a price correction, at least in pockets where the prices have steeply gone up in the past few years; as demand will likely dip. To this extent, to, the kind of capital appreciation that you saw in property in the past, may not be possible in future.

In all, it may be about time we reduced our penchant for holding properties (especially with the intention of tax sops) and instead focus on liquid, regulated investments, backed by sound prospects of companies and the economy.

1 thought on “Why borrowing and ‘investing’ in property is no longer attractive”