If you are one of those risk-averse investors, chances are that your savings would be locked into various fixed and recurring deposits.

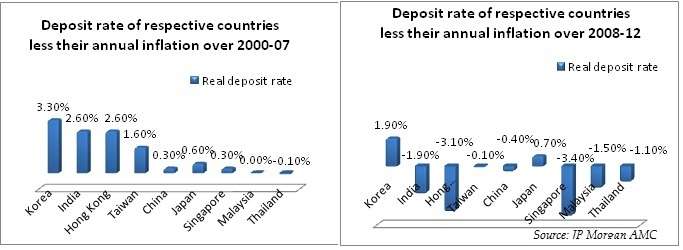

And yet, have the typical safe modes such as deposits offered you the protection you seek? Not in the ‘real’ sense suggests this data from JP Morgan Asset Management. Across the Asian countries mentioned below, deposit rates managed to beat inflation and leave you with some surplus (returns mentioned below are deposit rates post yearly inflation) until 2007.

However, since the start of the economic slowdown in 2008, most Asian countries have seen either lower interest rates and low growth or high inflation. As a result, investors in deposits have ‘negative real returns’. For India, rising prices were higher than deposit rates by 1.9 percentage points. Simply put, the interest income from deposits has not helped you keep pace with rising cost of goods. Net result, you would have had to dig in to your capital/savings to meet it.

Now, in a way, that too amounts to erosion of capital does it not? That means, while you may not lose your capital through risky investments, you lose it to a lethal force called inflation.

And yet, the deposit-investing culture has hardly seen a shift. According to the same report by JP Morgan Asset Management, in 2001, 67 per cent of investors in emerging Asia preferred deposits over other risky assets. This proportion did not change as late as 2011.

Way out?

But what choice do you have to combat this? Not much but here are a few suggestions:

If you are at the fag end of your income earning career or are retired, ensure that you diversify your investments across a few products. Of course, you do not have to compromise on the quantum of risk you can take (or cannot take). If you want only debt products, look beyond bank deposits. There would be times when top-rated bonds and debentures come up with good rates. Be on the look-out and lock into them. Keep a demat account ready for this purpose as most bonds require you to have a demat account. Explore corporate deposits in credit worthy companies that are rated. Avoid going for unrated companies unless you have knowledge on the financials of such companies.

Ensure that instruments have high credit rating such as AAA before you invest either in bonds or deposits. Look for debt mutual funds that have delivered not less than 7 per cent annually in the past and have at least a three-year record. Use systematic transfer plan in these options if you wish to get a steady payout.

Grin and bear

Even with all this, there is no guarantee that you will successfully combat inflation. The fact is that if you had a sufficiently large corpus, you can simply park your money in instruments that earn 6-7 per cent and still not worry too much about losing a bit of your capital.

But such a corpus can be built only if you invest across asset classes spanning equities, debt gold and real estate early on in life. While some of them may earn mediocre returns, they will protect capital. The rest, will, hopefully, take risks and still deliver in the long term. Hence, if you are still in your early earning years, you have very little choice in the current inflation scenario, but to take on some risks.

Starting early, investing regularly, reviewing and rebalancing periodically and investing for the long term could be the only way out to take on the devil called inflation. You can always move a good chunk of your money to deposits, when your need for fixed income generation turns high post retirement.

Thanks Vidya,

Could you please also write an article on good debt investment opportunities to benefit from upcoming interest rate reduction cycle. I know there is an element of speculation, but coming months this choice might pay richly for an investment horizon of 18-36 months.

Hi Ashwin, yes it appears we may be at the fag end of the high interest rate cycle. The last few debt/debt-oriented funds that we have been recommending including Reliance MIP, IDFC SSI Medium Term Plan A and Birla Sun life Dynamic Bond are all geared to take advantage of fall in yields. Among other debt products, bank deposits have already seen a dip.You can look at some of the corporate deposits with high rating and returns of 9-pus percent. But then these are fixed returns and hence will not capture a price rally. – Vidya

Nice article Vidya.

Have a related query.Would it be wise to go with liquid funds in this time when interest rates are expected to fall or better to go with better FD wherin you would get a lockin interest rate.

Hi Rohit, you have the answer in what you just stated 🙂 Liquid funds are not a substitute for fixed deposits, especially if you are looking at deposits on 1-plus year. As fixed deposits will lock the rates, if you do get good rates, you should lock-into them. Use liquid funds like a transit option; either to park money for contingencies or for impending expenses or to move in to better investment avenues like equities. – Vidya

Dear Vidya,

Thanks for such a wonderful read. It surely gives us an idea on debt products besides the good old bank deposits. These days CDs have become more prevalent and also provide attractive net returns post-inflation. Investors should also look into the MIPs as you have justly pointed out.

However, I was thinking if investing in well-bred blue chips could also do the trick to stay profitable. Any ideas around that?

Hi Asar, By ‘well-bred bluechip’, if you mean investing in bluechip large-cap stocks, yes it is certainly one of the superior options to build long-term wealth. But since stocks do not guarantee returns and come at much higher risk, we did not compare it with the fixed income options. If you have the time to analyse and pick the right stocks, it can be rewarding. otherwise, mutual funds have experts in fund managers to do the same, with better diversification and managing to enter and exit stocks as and when required without your incurring short-term capital gains (if you sell individual stocks withing a year you would incur capital gains). – Vidya

Hi I am a member of FUNDS INDIA.Kindly suggest me should I invest in Tax Free Bonds issued by Govt.

Hi Indranil, as you may be aware, tax-free bonds provide interest-free income. There is no tax benefit on the capital invested. To know whether a tax-free bond offer is lucrative for you – take in to account your tax bracket and the interest rate offered and compare such rate with a bank FD. for instance if a 5-10 year bank FD provides 9% now, then your returns post tax, if you are in the 30% tax bracket in 6.3% {9% – (9%*30%)}. Hence, if a tax-free bond offers a rate higher than this, then it will still be beneficial. If you are in the 20% tax bracket then your returns from the bond should be not less than 7.2% for it to be better than a bank FD rate.Currently IRFC bonds offer rates higher than what us mentioned above, especially for retail investors. You can see the details in http://www.fundsindia.com/content/jsp/corporate/IRFCTaxFreebonds.do – Vidya

I think the calculation isn’t as simple as that. Bank FD interest is usually compounded 4 times a year whereas interest from tax free bonds is an annual payout.

Hi Vikas, we took a payout comparison for both deposit and bond so that it is like to like. If you wish to calculate the compounded quarterly and then annual payout or simply a cumulative option for the FD, even then the current IRFC rates are superior at the higher tax bracket. – Vidya

Nice article Vidya.

Have a related query.Would it be wise to go with liquid funds in this time when interest rates are expected to fall or better to go with better FD wherin you would get a lockin interest rate.

Hi Rohit, you have the answer in what you just stated 🙂 Liquid funds are not a substitute for fixed deposits, especially if you are looking at deposits on 1-plus year. As fixed deposits will lock the rates, if you do get good rates, you should lock-into them. Use liquid funds like a transit option; either to park money for contingencies or for impending expenses or to move in to better investment avenues like equities. – Vidya

Hi vidya

If invest in tax saving bond how long will i be locked in the TAX saving bonds which are availble in the market as of now

Hi Shane, currently there are only tax-free bonds (Tax-saving bonds or infrastructure bonds are different. They offer deduction on the principal invested. No issues are available in current financial year). Tax-free bonds offer interest income that is free of tax. There is no other tax deduction available. the lock-in varies in each offer and each bond. Currently, IRFC offers 10-yr and 15-yr maturity periods. You may check this link for details: http://www.fundsindia.com/content/jsp/corporate/IRFCTaxFreebonds.do. These bonds are traded in the market and can be sold even before maturity. But you have to be careful as to exiting at the right price, without loss. Hence, it is safer to hold till maturity.

can u suggest best performing debt mutual instrument for 1-2 year span.thanks

Hi Meena, for fund-specific recommendations, request you to kindly send your query with your investment purpose if any, risk appetite as well as the mode of investment – SIP or lump sum to support@fundsindia.com

i liked ur suggestions and recommendations. I am a retail investor and keep investing in Equity, MF’s Bonds etc. pl. suggest some Liquid funds to keep my money instead in savings account. I shall appreciate if Tax implications are also told . Currently I am in 30% tax bracket. regards.

Hi Tejinder, You may like to read this link on liquid funds where I have discussed in detail about these funds and their tax implications. There is also a list of liquid funds that deliver well. You can choose from them. https://blog.fundsindia.com/blog/index.php/mutual-funds/liquid-funds-invest/751/ . But pl. remember that liquid funds are good to park some surplus that you may require for contingency. Hence any excess in savings account can be shidted to liquid funds. But do ensure that you keep enough balance in your savings account for your day to day operational cash flow needs. – Vidya

Hi Vidya,

I want to invest Rs. 1,00,000 in the Tax free Bonds.

Which is better 1. Hudco Tax Free Bond or 2. IRFC Tax Fee Bond.

Or shall I divide in both of them.

Regards

Indranil

Hi Indranil, kindly check if Hudco is open. At the time of issue, its closing date was stated as Jan 22. IRFC has a notch higher credit rating than HUDCO. – Vidya

Great Article.

But I have my doubts.

What with all this talk of inflation and Asset Allocation, Equity-Debt-Hybrid-MIP-SIP appears to be mumbo-jumbo when compared to the real estate. In my last 40 years , I have not seen rates of real estate coming down though they might have stagnated at times. Today, one could not purchase a 2BHK in any t locality in Delhi/Mumbai/Chennai etc. had he invested in any Agreesive fund(s) in a SIP mode the same amount as he would have paid EMI. So, I personally think is it not better to invest in real estate through EMI mode rather than in any MF schemes/ Bonds in SIP mode? (BTW i am aware of American Housing collapse but India seems to me to be a different Ball game what with so much of population and with Builders lobby drawing the last blood from the poor so called middle class and upper middle class and govt also having its pie , a collapse in the Real Estate may happen some time beyond 2050 if i am right).

Thanks for your thoughts Mr Mohan. I am sure the kind of run up in real estate can easily entice investors to go for this asset class. But remember wealth building is also about balancing your risk.

Just step back and try recollecting instances of reading in the newspaper about builders going bust or land purchased having no clean title. can you recall the land/farm schemes that we read going bust? Or projects of even very large builders stuck in the middle (even now)? What happens to the money then?

We only hear the success stories in real estate not the ones (which are plenty if you ask any practicing lawyer) that soured.

Sir, real estate should certainly form a part of your portfolio. But if it is your entire portfolio, it is simply high risk. Also, you can never liquidate money at short notice when you need it. Until we have clean titles, until we have more efficient instruments like real estate investment trusts (REITs) and more importantly until we have unbiased and scientific valuation methods and mapping for land, real estate will remain not only risky and ill-liquid but also suck too much lump sum at one go.

And you do not have to wait for a real estate bust to happen. Look at the NHB Residex index in cities such as Bangalore and Hyderabad. Five years from 2007 and the index of these cities still have negative returns, showing that investors in these markets would only have burnt their fingers.

While asset allocation may sound sophisticated, in reality it is nothing but buying into 3-4 asset classes and staying put with that ratio. Asset allocation is not about chasing returns; it is about building wealth.

Yes, mutual funds can certainly not build you enough money in the medium term (if your savings are limited) to buy you a house in a city; they can at best help you make the 20% margin upfront. – Vidya

OK vidya ji

So how do i invest in the real estate asset class in India?

Thanks for your reply.

Sir, in today’s real estate market, you cannot invest without taking risks. The risks with property is less if you choose a builder who is of repute and the building is already constructed. Land becomes a lot more risky unless you have experience in conducting the due diligence. Then there is a third route called real estate funds (which is a private placement by venture capital and private equity plays). These are of course not mutul funds.

You may have heard big names like HDFC, Kotak, Birla launch these close-end funds. They cannot be advertised as they are privately placed. These are again for those who can take risks as the money is directly deployed as equity in real estate projects of builders. But yes the IRR can be quite high if successful. the downside is these funds have a lock-in of anywhere between 5-10 years and require you to have huge sums (typically 25 lakh plus) to invest. Banks do not lend for this purpose.

End of day, real estate is a pure risk-reward play. Those with deep pockets and reasonable knowledge can venture. For the rest, a property beyond a self-occupied one may not be easy.

Hi Vidya

I have applied for NPS. It my decision right. Maximum how much can I invest. Is there any ceiling.

Regards

Indranil

Hello sir, today NPS is amongst the lost cost and efficient means to build a pension kitty for yourself. If you are not going to be a pension earner from your employer, this is certainly a good move. If you applied for NPS voluntarily (and not an NPS programme offered by your employer) then you can invest any amount. There is no ceiling but the min. amt. is rs 500 per month or Rs 6000 a year. Tax deduction under Section 80C is however, within the overall limit of Rs 1 lakh. – Vidya

Hi, MAM,

I WANT TO INVEST 12000 P.M. FOR MY CHILD’S EDUCATION. TILL NOW I DON’T HAVE ANY INVESTMENT. I WANT SAFE INVESTMENT. SHOULD I INVEST IN PPF, RD OR MF FOR GOOD RETURNS AFTER 15 YEARS.REGARDS.

Shaikh, you can always invest in a combination of what you just mentioned. But if your horizon is 15 years then mutul funds are likely to deliver superior returns than govt instruments and bank deposits. Pl. seek an MF aadvisory appointment through the web so that we can help you build an mf portfolio based on yout time frame/goal amount and risk appetite.- Vidya

I HAVE A PLAN TO INVEST RS 1500000 IN MIP OF DIFFERENT MF’S AND WOULD LIKE TO DO SWP OF RS 20000 FROM 2015 ONWARDS. MY QUESTION IS DOES MY SWP ATTRACTS ANY TAX ? OR IS IT WISE TO CHOOSE DIVIDEND OPTION? INSTEAD OF SWP. (I HAVE NO OTHER INCOME).

Sir, if you are looking for assured income flows and are dependent on this source of income, it may be better to go for SWPs. Funds do not guarantee regular/fixed sums as dividends even if the plan is an MIP.

That said, to answer your query on tax, MIPs are debt funds and would therefore attract short/longterm capital gains tax. If you hold for more than a year then you can pay 10% without indexation or 20% with indexation benefits. Dividend distribution tax (on the fund’s end), on the other hand would be 13.52% including cess and surcharge. – Vidya

Company is P/E 0 ,And EPS 0 , Book Value – our what mind..? what is comany cclose step at or company beining…?

Mr Pramod, your question is not clear.

Hi Vidya,

I want to invest Rs. 1,00,000 in the Tax free Bonds.

Which is better 1. Hudco Tax Free Bond or 2. IRFC Tax Fee Bond.

Or shall I divide in both of them.

Regards

Indranil

Hi Indranil, kindly check if Hudco is open. At the time of issue, its closing date was stated as Jan 22. IRFC has a notch higher credit rating than HUDCO. – Vidya

i liked ur suggestions and recommendations. I am a retail investor and keep investing in Equity, MF’s Bonds etc. pl. suggest some Liquid funds to keep my money instead in savings account. I shall appreciate if Tax implications are also told . Currently I am in 30% tax bracket. regards.

Hi Tejinder, You may like to read this link on liquid funds where I have discussed in detail about these funds and their tax implications. There is also a list of liquid funds that deliver well. You can choose from them. https://blog.fundsindia.com/blog/index.php/mutual-funds/liquid-funds-invest/751/ . But pl. remember that liquid funds are good to park some surplus that you may require for contingency. Hence any excess in savings account can be shidted to liquid funds. But do ensure that you keep enough balance in your savings account for your day to day operational cash flow needs. – Vidya

Great Article.

But I have my doubts.

What with all this talk of inflation and Asset Allocation, Equity-Debt-Hybrid-MIP-SIP appears to be mumbo-jumbo when compared to the real estate. In my last 40 years , I have not seen rates of real estate coming down though they might have stagnated at times. Today, one could not purchase a 2BHK in any t locality in Delhi/Mumbai/Chennai etc. had he invested in any Agreesive fund(s) in a SIP mode the same amount as he would have paid EMI. So, I personally think is it not better to invest in real estate through EMI mode rather than in any MF schemes/ Bonds in SIP mode? (BTW i am aware of American Housing collapse but India seems to me to be a different Ball game what with so much of population and with Builders lobby drawing the last blood from the poor so called middle class and upper middle class and govt also having its pie , a collapse in the Real Estate may happen some time beyond 2050 if i am right).

Thanks for your thoughts Mr Mohan. I am sure the kind of run up in real estate can easily entice investors to go for this asset class. But remember wealth building is also about balancing your risk.

Just step back and try recollecting instances of reading in the newspaper about builders going bust or land purchased having no clean title. can you recall the land/farm schemes that we read going bust? Or projects of even very large builders stuck in the middle (even now)? What happens to the money then?

We only hear the success stories in real estate not the ones (which are plenty if you ask any practicing lawyer) that soured.

Sir, real estate should certainly form a part of your portfolio. But if it is your entire portfolio, it is simply high risk. Also, you can never liquidate money at short notice when you need it. Until we have clean titles, until we have more efficient instruments like real estate investment trusts (REITs) and more importantly until we have unbiased and scientific valuation methods and mapping for land, real estate will remain not only risky and ill-liquid but also suck too much lump sum at one go.

And you do not have to wait for a real estate bust to happen. Look at the NHB Residex index in cities such as Bangalore and Hyderabad. Five years from 2007 and the index of these cities still have negative returns, showing that investors in these markets would only have burnt their fingers.

While asset allocation may sound sophisticated, in reality it is nothing but buying into 3-4 asset classes and staying put with that ratio. Asset allocation is not about chasing returns; it is about building wealth.

Yes, mutual funds can certainly not build you enough money in the medium term (if your savings are limited) to buy you a house in a city; they can at best help you make the 20% margin upfront. – Vidya

OK vidya ji

So how do i invest in the real estate asset class in India?

Thanks for your reply.

Sir, in today’s real estate market, you cannot invest without taking risks. The risks with property is less if you choose a builder who is of repute and the building is already constructed. Land becomes a lot more risky unless you have experience in conducting the due diligence. Then there is a third route called real estate funds (which is a private placement by venture capital and private equity plays). These are of course not mutul funds.

You may have heard big names like HDFC, Kotak, Birla launch these close-end funds. They cannot be advertised as they are privately placed. These are again for those who can take risks as the money is directly deployed as equity in real estate projects of builders. But yes the IRR can be quite high if successful. the downside is these funds have a lock-in of anywhere between 5-10 years and require you to have huge sums (typically 25 lakh plus) to invest. Banks do not lend for this purpose.

End of day, real estate is a pure risk-reward play. Those with deep pockets and reasonable knowledge can venture. For the rest, a property beyond a self-occupied one may not be easy.

Hi Vidya

I have applied for NPS. It my decision right. Maximum how much can I invest. Is there any ceiling.

Regards

Indranil

Hello sir, today NPS is amongst the lost cost and efficient means to build a pension kitty for yourself. If you are not going to be a pension earner from your employer, this is certainly a good move. If you applied for NPS voluntarily (and not an NPS programme offered by your employer) then you can invest any amount. There is no ceiling but the min. amt. is rs 500 per month or Rs 6000 a year. Tax deduction under Section 80C is however, within the overall limit of Rs 1 lakh. – Vidya

Company is P/E 0 ,And EPS 0 , Book Value – our what mind..? what is comany cclose step at or company beining…?

Mr Pramod, your question is not clear.

Hi vidya

If invest in tax saving bond how long will i be locked in the TAX saving bonds which are availble in the market as of now

Hi Shane, currently there are only tax-free bonds (Tax-saving bonds or infrastructure bonds are different. They offer deduction on the principal invested. No issues are available in current financial year). Tax-free bonds offer interest income that is free of tax. There is no other tax deduction available. the lock-in varies in each offer and each bond. Currently, IRFC offers 10-yr and 15-yr maturity periods. You may check this link for details: http://www.fundsindia.com/content/jsp/corporate/IRFCTaxFreebonds.do. These bonds are traded in the market and can be sold even before maturity. But you have to be careful as to exiting at the right price, without loss. Hence, it is safer to hold till maturity.

I HAVE A PLAN TO INVEST RS 1500000 IN MIP OF DIFFERENT MF’S AND WOULD LIKE TO DO SWP OF RS 20000 FROM 2015 ONWARDS. MY QUESTION IS DOES MY SWP ATTRACTS ANY TAX ? OR IS IT WISE TO CHOOSE DIVIDEND OPTION? INSTEAD OF SWP. (I HAVE NO OTHER INCOME).

Sir, if you are looking for assured income flows and are dependent on this source of income, it may be better to go for SWPs. Funds do not guarantee regular/fixed sums as dividends even if the plan is an MIP.

That said, to answer your query on tax, MIPs are debt funds and would therefore attract short/longterm capital gains tax. If you hold for more than a year then you can pay 10% without indexation or 20% with indexation benefits. Dividend distribution tax (on the fund’s end), on the other hand would be 13.52% including cess and surcharge. – Vidya

Hi, MAM,

I WANT TO INVEST 12000 P.M. FOR MY CHILD’S EDUCATION. TILL NOW I DON’T HAVE ANY INVESTMENT. I WANT SAFE INVESTMENT. SHOULD I INVEST IN PPF, RD OR MF FOR GOOD RETURNS AFTER 15 YEARS.REGARDS.

Shaikh, you can always invest in a combination of what you just mentioned. But if your horizon is 15 years then mutul funds are likely to deliver superior returns than govt instruments and bank deposits. Pl. seek an MF aadvisory appointment through the web so that we can help you build an mf portfolio based on yout time frame/goal amount and risk appetite.- Vidya

Dear Vidya,

Thanks for such a wonderful read. It surely gives us an idea on debt products besides the good old bank deposits. These days CDs have become more prevalent and also provide attractive net returns post-inflation. Investors should also look into the MIPs as you have justly pointed out.

However, I was thinking if investing in well-bred blue chips could also do the trick to stay profitable. Any ideas around that?

Hi Asar, By ‘well-bred bluechip’, if you mean investing in bluechip large-cap stocks, yes it is certainly one of the superior options to build long-term wealth. But since stocks do not guarantee returns and come at much higher risk, we did not compare it with the fixed income options. If you have the time to analyse and pick the right stocks, it can be rewarding. otherwise, mutual funds have experts in fund managers to do the same, with better diversification and managing to enter and exit stocks as and when required without your incurring short-term capital gains (if you sell individual stocks withing a year you would incur capital gains). – Vidya

Hi I am a member of FUNDS INDIA.Kindly suggest me should I invest in Tax Free Bonds issued by Govt.

Hi Indranil, as you may be aware, tax-free bonds provide interest-free income. There is no tax benefit on the capital invested. To know whether a tax-free bond offer is lucrative for you – take in to account your tax bracket and the interest rate offered and compare such rate with a bank FD. for instance if a 5-10 year bank FD provides 9% now, then your returns post tax, if you are in the 30% tax bracket in 6.3% {9% – (9%*30%)}. Hence, if a tax-free bond offers a rate higher than this, then it will still be beneficial. If you are in the 20% tax bracket then your returns from the bond should be not less than 7.2% for it to be better than a bank FD rate.Currently IRFC bonds offer rates higher than what us mentioned above, especially for retail investors. You can see the details in http://www.fundsindia.com/content/jsp/corporate/IRFCTaxFreebonds.do – Vidya

I think the calculation isn’t as simple as that. Bank FD interest is usually compounded 4 times a year whereas interest from tax free bonds is an annual payout.

Hi Vikas, we took a payout comparison for both deposit and bond so that it is like to like. If you wish to calculate the compounded quarterly and then annual payout or simply a cumulative option for the FD, even then the current IRFC rates are superior at the higher tax bracket. – Vidya

Thanks Vidya,

Could you please also write an article on good debt investment opportunities to benefit from upcoming interest rate reduction cycle. I know there is an element of speculation, but coming months this choice might pay richly for an investment horizon of 18-36 months.

Hi Ashwin, yes it appears we may be at the fag end of the high interest rate cycle. The last few debt/debt-oriented funds that we have been recommending including Reliance MIP, IDFC SSI Medium Term Plan A and Birla Sun life Dynamic Bond are all geared to take advantage of fall in yields. Among other debt products, bank deposits have already seen a dip.You can look at some of the corporate deposits with high rating and returns of 9-pus percent. But then these are fixed returns and hence will not capture a price rally. – Vidya

can u suggest best performing debt mutual instrument for 1-2 year span.thanks

Hi Meena, for fund-specific recommendations, request you to kindly send your query with your investment purpose if any, risk appetite as well as the mode of investment – SIP or lump sum to support@fundsindia.com