Your good friend earns more than you and not surprisingly, he also spends more than you. This makes you feel like he is richer than you, and you think that when you both retire, he is going to lead a much more comfortable and ‘affordable’ retired life. This may not be necessarily true. To put it on record, a good current salary is no guarantee for a comfortable and well-funded retirement. Let’s use data to prove our hypothesis.

Your good friend earns more than you and not surprisingly, he also spends more than you. This makes you feel like he is richer than you, and you think that when you both retire, he is going to lead a much more comfortable and ‘affordable’ retired life. This may not be necessarily true. To put it on record, a good current salary is no guarantee for a comfortable and well-funded retirement. Let’s use data to prove our hypothesis.

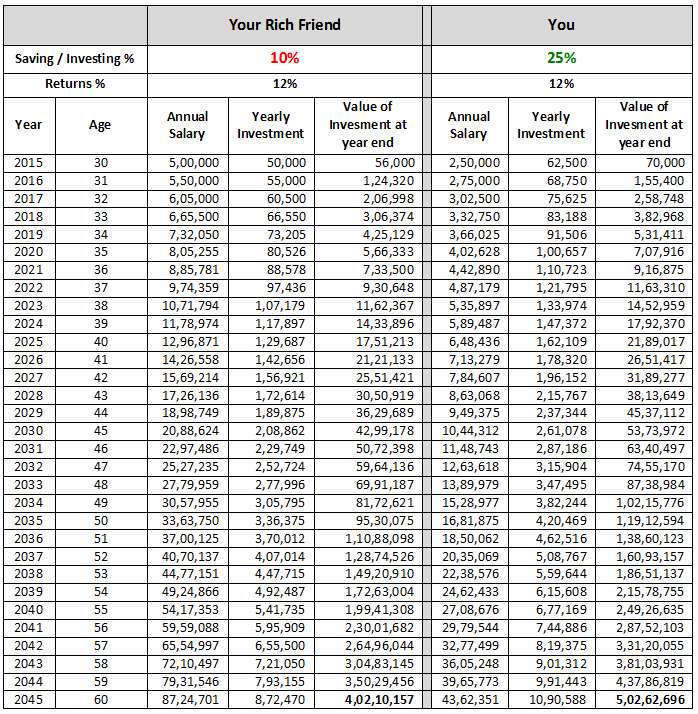

Let’s assume that you and your friend are 30 years old with no savings. Your friend starts his earning career at 30, and earns a handsome salary of Rs. 5 lakh a year. In comparison, you only earn Rs. 2.5 lakh a year, i.e., just half of what your friend earns! Seems like a sad start, no? Read on.

In this example, it is assumed that both you and your friend are able to get a 10 per cent salary hike every year up to retirement (60 years). But there is another difference between the two of you, besides your salary. Your friend is a spendthrift, and is only able to save (and invest) 10 per cent of his annual salary. However, you have a tighter control over your finances and are able to save 25 per cent of your salary. Mind you, you’re still drawing just half of what your friend earns every year.

Now, what do you think will happen on the day you both retire? Who will have a bigger retirement corpus? The answer might surprise you, but you know what? It’s going to be YOU!

You, even after earning half of what your friend made all through your life, are able to create a bigger corpus. You end up with a corpus of Rs. 5.02 crore,and your friend ends up with a crore short at Rs 4.02 crore. How is this even possible?

The answer is that you saved and invested more than your friend. Add to it the fact that you (and your friend too) were sincere enough to allow your money to compound. If you are interested in detailed calculation, take a look at the data below:

This example clearly shows that even though earning a high income is desirable, it is not the only requirement that needs to be fulfilled for a successful, well-funded retirement. You also need to rationalise your expenses and invest as much as possible. Another important thing to note here is that your friend has a more lavish lifestyle than yours, and this is deduced by his lower savings rate. Now considering that his corpus is lower than yours, it is quite obvious that he will have a tougher time maintaining his lifestyle using the smaller corpus. This, especially given that he has had a high lifestyle almost all his life. You, on other hand, will be able to comfortably use the bigger retirement corpus for maintaining the relatively modest lifestyle you have always had.

So, the next time you feel low about earning lesser than your friends, make sure that you put every effort to save and invest much more than what they are doing currently. More importantly, ensure that when you do move to a job or pay scale that matches your friends, you up your savings rate as well proportionately. That way, you will be on your way to a successful retirement.

The views mentioned in the article are personal.

Discipline saving in long term would definitely pay off, Nice article, it’s definitely going to encourage many to be regular in their personal finance.

Easy story telling style ! gr8

Thanks Raghvendra. Glad you and many others found it useful.

Very nice article and I like the aspect it is trying to highlight. These days people are started earning at a very early age, but making a wealth doesn’t depend on how much one is earning. The habit of investment is the myth here.

The more one can save, the more wealth can be created in long term. This will also help to reduce daily expenses and put a control on un-necessary expenses.

What you say is absolutely correct Santanu. If we can lower our unnecessary expenditures and increase our savings (investment) rates, then there is nothing like it. A very decent corpus can be accumulated in due course of time.

The value of 5 crore in 30 years would be 6-7 lakhs of today..which is current 3 years income and would be really insufficient to survive for retired life…

Inflation adjusted value of Rs 5 Crs will be around Rs 56 Lakhs after 30 years (considering 7% inflation) and not 7 Lakhs. But even if this amount seems to be small, then it all the more points to importance of saving (and investing) more for retirement corpus.

Another point to note here is that for MF returns, I have considered 12% – which is a quite conservative estimate. There are many funds which have been able to deliver more than 15% for 10-15 years. So there is still a possibility of ending up with more than Rs 5 Crs.

Even after saving 25% of his salary for his entire life, he was able to save about 12 months salary….he cant survive more than 12 months with that salary….what a retirement planning….lol…first one lived his life….we should spend as much as we can and commit suicide at the age of 61.

Hi Vicky

I think you are referring to an end-corpus of Rs 5.05 Crs and the annual salary at that time – Rs 43.63 Lakhs. This is equivalent to about 12 years and not 12 months.

5 crore with a inflation of 7pc will be 65.70 lac. One should not underestimate the power of compounding.

I agree with the above formula and this is how the best investment should be thought off. I would like to add that diversifying the funds will also help in managing the risk that may arise to get such rates and we should not forget to invest money in all forms that are available in the market.

I agree with the above formula and this is how the best investment should be thought off. I would like to add that diversifying the funds will also help in managing the risk that may arise to get such rates and we should not forget to invest money in all forms that are available in the market.

Very nice article and I like the aspect it is trying to highlight. These days people are started earning at a very early age, but making a wealth doesn’t depend on how much one is earning. The habit of investment is the myth here.

The more one can save, the more wealth can be created in long term. This will also help to reduce daily expenses and put a control on un-necessary expenses.

What you say is absolutely correct Santanu. If we can lower our unnecessary expenditures and increase our savings (investment) rates, then there is nothing like it. A very decent corpus can be accumulated in due course of time.

5 crore with a inflation of 7pc will be 65.70 lac. One should not underestimate the power of compounding.

Even after saving 25% of his salary for his entire life, he was able to save about 12 months salary….he cant survive more than 12 months with that salary….what a retirement planning….lol…first one lived his life….we should spend as much as we can and commit suicide at the age of 61.

Hi Vicky

I think you are referring to an end-corpus of Rs 5.05 Crs and the annual salary at that time – Rs 43.63 Lakhs. This is equivalent to about 12 years and not 12 months.

The value of 5 crore in 30 years would be 6-7 lakhs of today..which is current 3 years income and would be really insufficient to survive for retired life…

Inflation adjusted value of Rs 5 Crs will be around Rs 56 Lakhs after 30 years (considering 7% inflation) and not 7 Lakhs. But even if this amount seems to be small, then it all the more points to importance of saving (and investing) more for retirement corpus.

Another point to note here is that for MF returns, I have considered 12% – which is a quite conservative estimate. There are many funds which have been able to deliver more than 15% for 10-15 years. So there is still a possibility of ending up with more than Rs 5 Crs.

Discipline saving in long term would definitely pay off, Nice article, it’s definitely going to encourage many to be regular in their personal finance.

Easy story telling style ! gr8

Thanks Raghvendra. Glad you and many others found it useful.

I agree with the above formula and this is how the best investment should be thought off.