If you are worrying about falling interest rates leaving you with no fixed income options, you are right – if your only fixed income option is bank Fixed Deposits (FDs). But did you know that falling interest rates can actually be a great opportunity in the debt market? Read on.

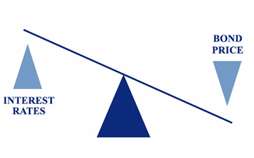

You may have often heard analysts say that there is an inverse correlation between bond prices and interest rates movement. Yes, that is where the opportunity lies. But first let us see what this relationship is all about.

Let us assume that you had invested Rs. 100 in a 5-year bank Fixed Deposit at the interest rate of 10 per cent (annual interest payout) a year ago. You have received Rs. 10 as the first year’s interest payment. If the interest rate in the country fell by 1 per cent now, you will earn 1 per cent more than the market for the next four years. Now, your friend too wishes to get a 10 per cent interest, or Rs. 10 interest income on an FD; however, she cannot do that as the current rates are 9 per cent. But if she is willing to pay a price to generate a regular 10 per cent income for herself, she might want to buy it from you to secure her annual income.

Bank FDs cannot be transferred by you. But just for the sake of this example, let us assume that it is transferable. If your friend is keen to generate Rs. 10 as income today, she will have to invest at least Rs. 103 to generate Rs. 10 every year. Now that is the value of your Rs. 100 deposit today.

But if the deposit market is not very liquid, and not easily available in the market for sale, then Rs. 103 could be trading at an even slightly higher price as a result of demand. That means, if you sell it today, you get a capital gain (Rs. 3), over and above the Rs. 10 interest.

Bank FDs are not tradable in real life situations; hence, you can’t gain from it by selling it before the maturity. However, government bonds, Public Sector Unit (PSU) bonds, corporate bonds, and bank certificates of deposits are tradable instruments. As a retail investor, you can’t buy them in small quantities. You need to open an account with a primary dealer to buy and sell these bonds in large quantities. Besides, would you know when is the right time to buy or sell them? Also for every such sale after buying, you would have a tax impact, especially if you actively churn your portfolio.

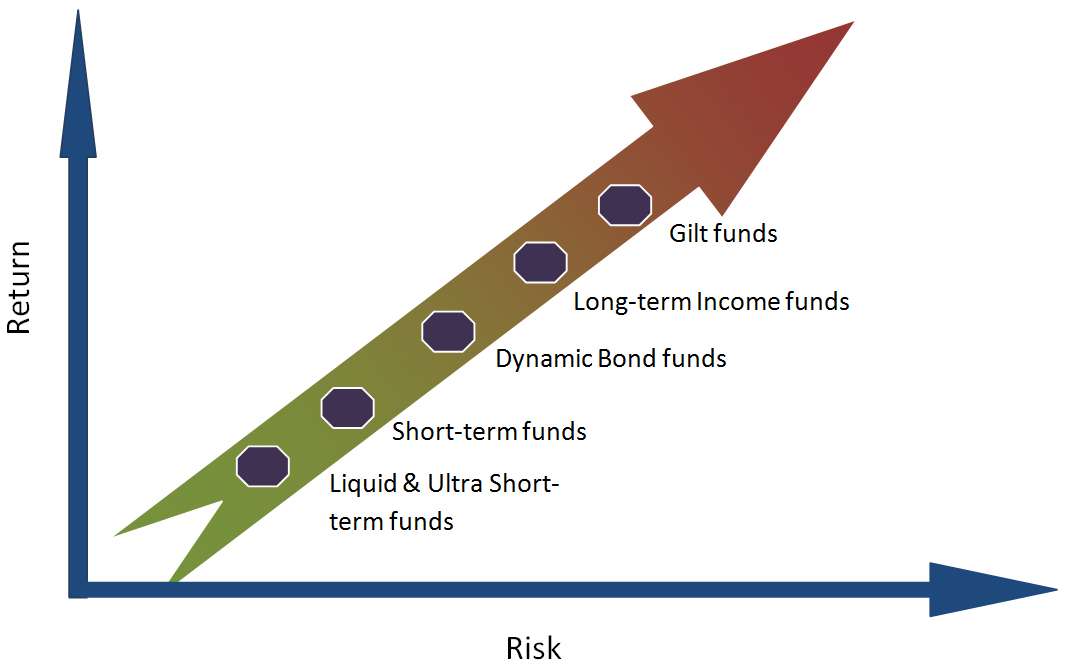

Then how can you gain from the falling interest rates scenario? The answer, especially for retail investors, is debt mutual funds. Debt mutual funds invest in various fixed income instruments like bank Certificates of Deposits (CDs), Commercial Papers (CPs), treasury bills, government bonds (G-secs), PSU bonds and corporate bonds/debentures, cash and call instruments, and so on. These funds are classified based on varying time frames. That means you choose a different fund for short-term needs, and a very different one for long-term requirements. Needless to say, short-term funds tend to take low risk as you need your money in the near term, while longer-term funds take a bit of risk to generate returns over the long-term for you. These funds are classified based on the category and tenure of the underlying investment instruments.

As highlighted in the below chart, risk increases with the tenure of investment instruments. When there is a fall in the market’s interest rates, fixed income instruments with the longest tenure will gain more compared to the shortest tenure instruments. Hence, funds such as dynamic bond funds, long term income funds, and gilt funds are best placed to gain from the falling interest rate scenario as when rates fall, the price of their underlying instruments rise.

In terms of taxation, debt funds score better than Bank FDs. If you hold your investments for more than three years, you just need to pay only 20 per cent capital gains tax (with indexation benefits). Since you take indexation benefits (that means adjusting the cost of your investment for inflation), your ‘real’ tax outgo will be far lower than the 20 per cent. Be it in terms of liquidity, superior returns or tax benefits, debt mutual funds score over passive bank deposits. Diversify your traditional debt holding with these schemes, based on your time frame of investment to take advantage of them.

How did the Rs. 103 figure come about? Rs. 111 (and not Rs. 103) is the amount on which 9% will yield Rs. 10.

Also, why do long term funds gain more wrt short term funds in a falling interest rates environment (as explained) if both invest in the same underlying instruments?

Hi Vijay,

Please use the PV function in Xl sheet to find the bond valuation.

Select PV formula and enter the following data to find the bond price.

Rate=9%, Nper=4, Pmt=10, FV=100, Type=0

In the same formula, if the Nper is 14 years (15 Year bond just received one coupon payment) you will get 107.8. Hence, longer the tenure of the bond, higher the gains.

You can refer the following link to know more about bond valuation.

http://www.investopedia.com/calculator/bondprice.aspx

Thanks

Sathya

Hello,

There are some good information in the article..Thank you..

Can you tell me is there a way to get 1 lac per month fixed return or 12% return if i invest 1 crore. If you invest huge amount is there any way to get such return. (i am not looking for mutual funds, i means fixed guaranteed returns..) Is any retirement plan or fixed income return plans for big amount..

Thank you.

Hello sir,

In today’s return scenario, 12% fixed return is hard to come by in regulated products.

thanks, Vidya

Hi Vijay,

A long term fund may have invested in a 5 year bond @10% for 5 years, while a short term fund may have invested in a 1 year bond @10% for 1 year. So when the year ends, the short term fund’s investment matures, and they will have to reinvest it @9%, whereas the long term fund continues to generate 10% for the next 4 years.

Prabhu

Hi Sir,

I analyzed the return for Debt Funds, both for Long Term & Ultra Short Term for a span of 8 – 10 years. I observed that Ultra Short Term has the same potentiality of giving return as long term Debt Fund. If you see the graph of ultra short term the curve is ever increasing with constant slope, whereas the graph of Long Term Debt Fund some times come down or fluctuates(negative return).

More over in case of short term Debt fund exit load is not there where as for long term Debt fund at least 1 year exit load is there.

I analyzed for a period of 2004 to 2013. I compared between Birla SL Saving Fund and HDFC Income Fund.

Please tell me whether my analysis was correct or not?

Hi Gourab

Most of the UST funds invest in very short duration (3 to 9 months) papers such as bank CDs and CPs .Long-term funds invest in very long term (5 yrs to 10 yrs) papers such as corporate bonds and Government securities. As explained in the article, longer the tenure higher the risk -return potential.

Over the last few years, UST funds have given stable returns due to elevated interest rates in the economy.However during the falling interest rate environment long-term funds tend to perform better than the UST funds.

Dynamic bond funds are better alternative for the pure income funds. Dynamic bond funds intermittently book profits during the falling interest rate environment and take short-term positions during rising interest rate environment. If you want to analyse take the complete universe of funds in the each category and come to a conclusion.

We still believe, dynamic and long term bond funds could deliver superior returns in the long run.

Thanks

Sathya

How does a Debt fund vs FD work in terms of tax effeciency for a person in 10% tax bracket and holding period of over 3 years. While the LT rate for Debt comes to 20% with indexation the FD rate would be only 10%. Therefore FDs seem much better in this feasible scenario

Hello Sir,

If you talk of short term (less than 3 years now), the tax rates are the same but returns tend to be slightly higher in debt funds. If you talk of long term (over 3 years), 20% with indexation makes a HUGE difference, especially given how high inflation has been in the past few years. when you index the cost, you bring it to today’s value..so your taxable money is far far lower and therefore despite 20% rate, it is almost always lower than the 10% tax without indexation (for FD).

thanks, Vidya

Hi,

I am a newly joined investor in fundsindia. I was more inclined & hence, have already started an SIP in tax saver funds.

But I went across your article a few days back. This current article & https://blog.fundsindia.com/blog/mutual-funds/there-is-a-debt-fund-to-suit-every-time-frame/7750

Really good articles.

I have already invested in a normal short term debt fund & a ultra short-term debt fund. I understand, these are for different time-frames. I want to understand the following –

“If you hold your investments for more than three years, you just need to pay only 20 per cent capital gains tax (with indexation benefits). Since you take indexation benefits (that means adjusting the cost of your investment for inflation), your ‘real’ tax outgo will be far lower than the 20 per cent.”

I want to know, how a debt fund is taxed,

– If I redeem it fully before 3-years. (say after 1-yr)

– If I redeem it partially after 1-yr up to 3-yrs. (say 50% in 2nd yr & rest before completion of 3rd year)

Thanks & Regards,

Aniket Mohite

Hello Aniket,

Sorry for the delayed response. For debt funds less than 3 years, whenever you sell, the capital gain (sale – cost of that investment) is subject to tax in your usual slab rate..just like income from other sources. This is the case whether you sell in the 1st year or 2rd year ans whether you sell aprtly or fully. That part (the units sold) which is sold is taxed accordingly. If you sell any part of your holding after 3 years, then your cost is indexed. That is the cost is multiplied by the cost inflation index (check here for the indices http://cadiary.org/cost-inflation-index-capital-gain/) of the year of sale and divided by the inflation index in the year od purchase. That way your cost is brought to present value. The capital gain so calculated after such indexed cost is taxed at 20%. Because of indexation, your gain appears lower and hence the tax is also lower as opposed regular tax without indexation.

Hi Vidya,

Thanks a lot for the answer. Thanks for the indexation link as well.

Wont be selling anything soon. But will keep this info in mind going forward.

Regards,

Aniket

Hi,

I am a newly joined investor in fundsindia. I was more inclined & hence, have already started an SIP in tax saver funds.

But I went across your article a few days back. This current article & https://blog.fundsindia.com/blog/mutual-funds/there-is-a-debt-fund-to-suit-every-time-frame/7750

Really good articles.

I have already invested in a normal short term debt fund & a ultra short-term debt fund. I understand, these are for different time-frames. I want to understand the following –

“If you hold your investments for more than three years, you just need to pay only 20 per cent capital gains tax (with indexation benefits). Since you take indexation benefits (that means adjusting the cost of your investment for inflation), your ‘real’ tax outgo will be far lower than the 20 per cent.”

I want to know, how a debt fund is taxed,

– If I redeem it fully before 3-years. (say after 1-yr)

– If I redeem it partially after 1-yr up to 3-yrs. (say 50% in 2nd yr & rest before completion of 3rd year)

Thanks & Regards,

Aniket Mohite

Hello Aniket,

Sorry for the delayed response. For debt funds less than 3 years, whenever you sell, the capital gain (sale – cost of that investment) is subject to tax in your usual slab rate..just like income from other sources. This is the case whether you sell in the 1st year or 2rd year ans whether you sell aprtly or fully. That part (the units sold) which is sold is taxed accordingly. If you sell any part of your holding after 3 years, then your cost is indexed. That is the cost is multiplied by the cost inflation index (check here for the indices http://cadiary.org/cost-inflation-index-capital-gain/) of the year of sale and divided by the inflation index in the year od purchase. That way your cost is brought to present value. The capital gain so calculated after such indexed cost is taxed at 20%. Because of indexation, your gain appears lower and hence the tax is also lower as opposed regular tax without indexation.

Hi Vidya,

Thanks a lot for the answer. Thanks for the indexation link as well.

Wont be selling anything soon. But will keep this info in mind going forward.

Regards,

Aniket

Hi,

Can anyone guide me whether investing in 5 years tax saving F.D. would be better OR investing in the scheme of Guaranteed plans for 5 years which ICICI bank is offering. In Guaranteed plans of ICICI Bank, ICICI bank will invest 70% in equity and 30% in debt funds but lock in period is 5 years.

Which option would be better either in investing in 5 years tax saving F.D or aforesaid guaranteed plans of ICICI bank for the purpose of tax saving?

Regards,

Jagdish

REg

Hello Jagdish, we answer queries on mutual funds. From what you say, there can be no guaranteed plan from a bank..it must be an insurance product. No product with equity can have guaranteed returns. Please verify the facts correctly and ensure your relationship manager is disclosing facts properly. Ask them to send you brochures of the products they are talking about and do not accept anything orally. Vidya

Hi I want to Invest some money in form of monthly investments(as you call SIP in mutual fund parlance or an RD in banks FD parlance) for a tenure of around 12-13 yrs but idea is to generate a fixed return of around 8-10% and as indicated in above article and by reading above comments it also gave an indication that sometimes these debt funds also give negative returns .is it true? Also it seems that debt mutual fund is a better option as compared to FD looking at indexation benefits …..would you suggest any particular fund and could you also pl throw some light on past return history of Debt mutual funds in India…Is it completely isolated from ups and downs of equity market (say if i invest in 100% debt fund with no exposure in Equities) .Also I want to play safe and would not like to take any risk as its my hard earned money and its my stretched savings which i will be putting every month in this…also let me tell you that its for my sons education requirements after around 13 yrs that i am planning this investment. I can also consider FD as an option if there is any risk associated in expected return of at least 8% p.a….Can you please advise.

Hello Mitul, Sorry for the delayed response. if you are planning for your son’s education expenses (13 years from now), then you should have some sizeable exposure to equity. That is the only way to beat the rising cost of inflation in education. An FD of 8% (which you will not get today as rates are lower) will deliver post-tax returns of 5.6-7.2% post-tax returns. Debt funds will deliver slightly higher true. But if you do not have equity, you miss out big time in building a sufficient corpus. If you wish to own debt funds, you write to us from your account if you are a FundsIndia investor (using advisor appointment feature under help) and we will provide you with suitable funds. thanks, Vidya

How does a Debt fund vs FD work in terms of tax effeciency for a person in 10% tax bracket and holding period of over 3 years. While the LT rate for Debt comes to 20% with indexation the FD rate would be only 10%. Therefore FDs seem much better in this feasible scenario

Hi, My Query is on Recurring Deposit Vs Debt Funds. I invest in RDs monthly to fund my son’s yearly school fees (yes! i pay over 1 Lakh, thats why the RD). Can you suggest a Debt fund that would give a better return compared to RD ?

Hello Sunil,

For inevstor-specific recommendations, you may please login through your FundsIndia account if you are a FundsIndia investor and send your query through advisor appointment. We will answer them. We are constrained from responding in this forum.

thanks,

Vidya

Please suggest that if I invest Rs 10lac in long term debt fund every year for 3yrs and withdraw profit of 1st year investment after 3rd yrs and after 4th year 2nd year profit and after 5th yrs 3rd yrs profit and repeat this after 6yrs onward what is my tax liabilities after 3rd year onwards

Avneesh, you may think of withdrawing the amount to the extent of profit but for mutual fund and tax purpsoes, every withdrawl is partly principal and partly capital gain. And any gain after 3 years of holding will have indexation benefit – that is cost can be indexed and then gain calculated. On such gain a 20% tax will be applicable. thanks, Vidya

Please suggest that if I invest Rs 10lac in long term debt fund every year for 3yrs and withdraw profit of 1st year investment after 3rd yrs and after 4th year 2nd year profit and after 5th yrs 3rd yrs profit and repeat this after 6yrs onward what is my tax liabilities after 3rd year onwards

Avneesh, you may think of withdrawing the amount to the extent of profit but for mutual fund and tax purpsoes, every withdrawl is partly principal and partly capital gain. And any gain after 3 years of holding will have indexation benefit – that is cost can be indexed and then gain calculated. On such gain a 20% tax will be applicable. thanks, Vidya

How does a Debt fund vs FD work in terms of tax effeciency for a person in 10% tax bracket and holding period of over 3 years. While the LT rate for Debt comes to 20% with indexation the FD rate would be only 10%. Therefore FDs seem much better in this feasible scenario

That is a yearly 10% tax that you are talking about in FDs but in case of Debt MFs it is a long term capital gain only once when the MF units are sold. So, effectively that 20% with indexation is for 3 year’s return.

I want to invest HDFC Dyanamic plan Growth, for two year but I am little concern about that fund will give negative return or I will try other other fund

Sumit, For individual recommendations, please talk to your advisor, if you are on the FundsIndia platform. thanks, Vidya

I wants to invest some money.

Please give me head of department contact no.

Thanks

Ahmed, Thanks for your interest. we are an online platform. Please register on the website with details and you will hear from us. Thanks, Vidya

WIth debt funds, you get superior returns post-tax, high level of liquidity, and safety of capital compared to FDs. These make debt funds an Excellent alternative to keeping your money in Bank FDs.

I was wondering about how do short term debt funds decide on their portfolio. What is the background or metric they use to finalize that they will invest x% of their money in CPs or maybe CDs and y% of money in treasury bills or maybe Government Securities. I wanted to know how do they decide on their portfolio and proportions.

Vihang, Such bifurcation depends on the the rate cycle, the credit scenario, the availability of papers with good yields in these segments and the fund’s own internal restrictions. There is no cookie cutter approach to this. Thanks, Vidya

How does a Debt fund vs FD work in terms of tax effeciency for a person in 10% tax bracket and holding period of over 3 years. While the LT rate for Debt comes to 20% with indexation the FD rate would be only 10%. Therefore FDs seem much better in this feasible scenario

Hello Sir,

If you talk of short term (less than 3 years now), the tax rates are the same but returns tend to be slightly higher in debt funds. If you talk of long term (over 3 years), 20% with indexation makes a HUGE difference, especially given how high inflation has been in the past few years. when you index the cost, you bring it to today’s value..so your taxable money is far far lower and therefore despite 20% rate, it is almost always lower than the 10% tax without indexation (for FD).

thanks, Vidya

Hi Sir,

I analyzed the return for Debt Funds, both for Long Term & Ultra Short Term for a span of 8 – 10 years. I observed that Ultra Short Term has the same potentiality of giving return as long term Debt Fund. If you see the graph of ultra short term the curve is ever increasing with constant slope, whereas the graph of Long Term Debt Fund some times come down or fluctuates(negative return).

More over in case of short term Debt fund exit load is not there where as for long term Debt fund at least 1 year exit load is there.

I analyzed for a period of 2004 to 2013. I compared between Birla SL Saving Fund and HDFC Income Fund.

Please tell me whether my analysis was correct or not?

Hi Gourab

Most of the UST funds invest in very short duration (3 to 9 months) papers such as bank CDs and CPs .Long-term funds invest in very long term (5 yrs to 10 yrs) papers such as corporate bonds and Government securities. As explained in the article, longer the tenure higher the risk -return potential.

Over the last few years, UST funds have given stable returns due to elevated interest rates in the economy.However during the falling interest rate environment long-term funds tend to perform better than the UST funds.

Dynamic bond funds are better alternative for the pure income funds. Dynamic bond funds intermittently book profits during the falling interest rate environment and take short-term positions during rising interest rate environment. If you want to analyse take the complete universe of funds in the each category and come to a conclusion.

We still believe, dynamic and long term bond funds could deliver superior returns in the long run.

Thanks

Sathya

Hi, My Query is on Recurring Deposit Vs Debt Funds. I invest in RDs monthly to fund my son’s yearly school fees (yes! i pay over 1 Lakh, thats why the RD). Can you suggest a Debt fund that would give a better return compared to RD ?

Hello Sunil,

For inevstor-specific recommendations, you may please login through your FundsIndia account if you are a FundsIndia investor and send your query through advisor appointment. We will answer them. We are constrained from responding in this forum.

thanks,

Vidya

How does a Debt fund vs FD work in terms of tax effeciency for a person in 10% tax bracket and holding period of over 3 years. While the LT rate for Debt comes to 20% with indexation the FD rate would be only 10%. Therefore FDs seem much better in this feasible scenario

I was wondering about how do short term debt funds decide on their portfolio. What is the background or metric they use to finalize that they will invest x% of their money in CPs or maybe CDs and y% of money in treasury bills or maybe Government Securities. I wanted to know how do they decide on their portfolio and proportions.

Vihang, Such bifurcation depends on the the rate cycle, the credit scenario, the availability of papers with good yields in these segments and the fund’s own internal restrictions. There is no cookie cutter approach to this. Thanks, Vidya

Hi,

Can anyone guide me whether investing in 5 years tax saving F.D. would be better OR investing in the scheme of Guaranteed plans for 5 years which ICICI bank is offering. In Guaranteed plans of ICICI Bank, ICICI bank will invest 70% in equity and 30% in debt funds but lock in period is 5 years.

Which option would be better either in investing in 5 years tax saving F.D or aforesaid guaranteed plans of ICICI bank for the purpose of tax saving?

Regards,

Jagdish

REg

Hello Jagdish, we answer queries on mutual funds. From what you say, there can be no guaranteed plan from a bank..it must be an insurance product. No product with equity can have guaranteed returns. Please verify the facts correctly and ensure your relationship manager is disclosing facts properly. Ask them to send you brochures of the products they are talking about and do not accept anything orally. Vidya

Hi I want to Invest some money in form of monthly investments(as you call SIP in mutual fund parlance or an RD in banks FD parlance) for a tenure of around 12-13 yrs but idea is to generate a fixed return of around 8-10% and as indicated in above article and by reading above comments it also gave an indication that sometimes these debt funds also give negative returns .is it true? Also it seems that debt mutual fund is a better option as compared to FD looking at indexation benefits …..would you suggest any particular fund and could you also pl throw some light on past return history of Debt mutual funds in India…Is it completely isolated from ups and downs of equity market (say if i invest in 100% debt fund with no exposure in Equities) .Also I want to play safe and would not like to take any risk as its my hard earned money and its my stretched savings which i will be putting every month in this…also let me tell you that its for my sons education requirements after around 13 yrs that i am planning this investment. I can also consider FD as an option if there is any risk associated in expected return of at least 8% p.a….Can you please advise.

Hello Mitul, Sorry for the delayed response. if you are planning for your son’s education expenses (13 years from now), then you should have some sizeable exposure to equity. That is the only way to beat the rising cost of inflation in education. An FD of 8% (which you will not get today as rates are lower) will deliver post-tax returns of 5.6-7.2% post-tax returns. Debt funds will deliver slightly higher true. But if you do not have equity, you miss out big time in building a sufficient corpus. If you wish to own debt funds, you write to us from your account if you are a FundsIndia investor (using advisor appointment feature under help) and we will provide you with suitable funds. thanks, Vidya

I wants to invest some money.

Please give me head of department contact no.

Thanks

Ahmed, Thanks for your interest. we are an online platform. Please register on the website with details and you will hear from us. Thanks, Vidya

How did the Rs. 103 figure come about? Rs. 111 (and not Rs. 103) is the amount on which 9% will yield Rs. 10.

Also, why do long term funds gain more wrt short term funds in a falling interest rates environment (as explained) if both invest in the same underlying instruments?

Hi Vijay,

Please use the PV function in Xl sheet to find the bond valuation.

Select PV formula and enter the following data to find the bond price.

Rate=9%, Nper=4, Pmt=10, FV=100, Type=0

In the same formula, if the Nper is 14 years (15 Year bond just received one coupon payment) you will get 107.8. Hence, longer the tenure of the bond, higher the gains.

You can refer the following link to know more about bond valuation.

http://www.investopedia.com/calculator/bondprice.aspx

Thanks

Sathya

Hello,

There are some good information in the article..Thank you..

Can you tell me is there a way to get 1 lac per month fixed return or 12% return if i invest 1 crore. If you invest huge amount is there any way to get such return. (i am not looking for mutual funds, i means fixed guaranteed returns..) Is any retirement plan or fixed income return plans for big amount..

Thank you.

Hello sir,

In today’s return scenario, 12% fixed return is hard to come by in regulated products.

thanks, Vidya

Hi Vijay,

A long term fund may have invested in a 5 year bond @10% for 5 years, while a short term fund may have invested in a 1 year bond @10% for 1 year. So when the year ends, the short term fund’s investment matures, and they will have to reinvest it @9%, whereas the long term fund continues to generate 10% for the next 4 years.

Prabhu

How does a Debt fund vs FD work in terms of tax effeciency for a person in 10% tax bracket and holding period of over 3 years. While the LT rate for Debt comes to 20% with indexation the FD rate would be only 10%. Therefore FDs seem much better in this feasible scenario

That is a yearly 10% tax that you are talking about in FDs but in case of Debt MFs it is a long term capital gain only once when the MF units are sold. So, effectively that 20% with indexation is for 3 year’s return.

I want to invest HDFC Dyanamic plan Growth, for two year but I am little concern about that fund will give negative return or I will try other other fund

Sumit, For individual recommendations, please talk to your advisor, if you are on the FundsIndia platform. thanks, Vidya

WIth debt funds, you get superior returns post-tax, high level of liquidity, and safety of capital compared to FDs. These make debt funds an Excellent alternative to keeping your money in Bank FDs.