Even as all eyes are glued to the debt market, the equity market has its own story to tell, if we care to listen; what with forward valuations (price earnings ratio) lower than long-term averages (at about 15 times), seen since 2001.

Yes, there are enough near-term concerns for equities. Besides the shape and health of the economy and certain sectors, the recent tightening of liquidity could make it harder for companies to meet their funding needs, whether working capital or capital expenditure. Then there are the elections, providing uncertainty to development work in the country. That means a good part of FY-14 may be reeling under uncertainty.

But then, equity was never meant to be a short-term game.

Still, somehow, most retail investors think otherwise. Result? Jumping in to the equity market euphoria just as markets turn expensive and then exiting when markets topple thereafter and look cheap.

The majority ill time it

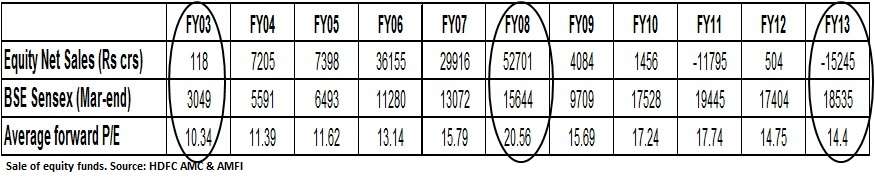

Here’s some interesting statistics on how investors put more money in equity funds at the peak and then stop the flow altogether later. The table below clearly illustrates the poor response to equity funds in down markets, such as the ones in FY-03 or FY-13, when valuations were very attractive.

Conversely, money flowed in to equity funds rapidly in peak markets such as FY-08, when price earnings ratio was upward of 20 times.

Now the question is: how would you know that it was a peak market? Fair enough, unless you follow markets/valuations, it may be tough. But then, why did investors stop investing when they knew the markets fell? This happens simply because people either invested in lump sums during market euphoria and did not bother to revisit in down markets or stopped their SIPs in panic, when the markets fell.

Now this is where pure investment discipline, if nothing else, rules.

The bounce back

Okay, let us suppose, your risk appetite would not let you throw, what may seem to you then as, good money after bad. But had you held on to what you had invested, chances are that you would still have made money. Given below is the Sensex data on the fall in down markets and returns 2 years after such down market.

Clearly, barring the years after the Y2K fall, markets have mostly compensated in the 2 years following the years’ of bear market. And we are simply looking at the Sensex. A basket of well diversified equity funds coudl have fetched much more in the above periods. Hence to say that your investments never made money may not be entirely true.

The no-loss territory

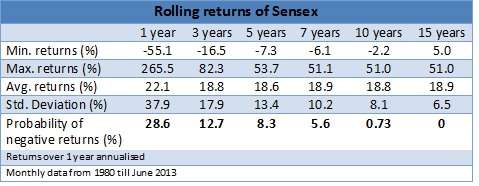

Agreed, again, that your skepticism in equities may be justified if you compare the returns of this asset class, in recent years, to other asset classes, including debt and gold. But then, that’s how equity markets have been earlier and will continue to be. Equities are simply for the long haul. Just take a look at the data below for the Sensex since 1980.

The rolling returns across various holding periods are given. Returns were rolled on monthly basis. The data shows that the probability of getting negative returns was as high as 30% for a 1-year period and 0% for a 15-year period. The probability keeps diminishing with time. In other words, the longer the holding period, the better the chances of not losing any money. And the average returns look good enough too.

What it all means

So does that mean you should never be holding equities if you had goals over shorter periods of say 3 years or 5 years? Not so. Its about the proportion you hold. It’s that proportion which would gently prop up portfolio returns if markets do rally and not actually harm your portfolio in case things take a turn for the worse. This is why a proper asset allocation becomes the determining factor when you have short- to medium-term goals.

Asset allocation to suit your time frame and systematic investing could be the only way out to play the equity game.

Else? Staying invested in pure guaranteed traditional debt products could be the only option. But then, you can be reasonably sure that they would lag behind rising prices, whether it is education or retirement.

If your parents managed it, they did so at a time when post offices and deposits gave a 12-13% interest and most of them drew pensions. So just how do you propose to manage with an average 6-8% post tax return on your fixed return products and no pension to think of?

Dear Vidya, Great article. Wonderful…and thanks for deep analysis.

Vidya,

very nice article.

One reason all mutual funds and all advisers blindly recommend equity for long term is it could beat inflation but not fixed income securities. But they fail to mention the probability of the outcome over certain period of time. Assuming 7% inflation, even for longer period of 10 years holding, ( for average Indian investor 1 year is long term ! ), 100% equity portfolio does not have 100% probability to beat inflation. No one mentions this.

Investment planners talk about returns as though it is sure thing with longer holding period but not probability of getting it. This mislead average investor to believe return is the only thing to worry about. It is nice to see that you covered the probability along with return numbers.

Since equity are recommended as the only instrument to beat inflation, it could have been better if you published the probability of an equity portfolio beating inflation over 3 years period, 5 years and 10 years period. I guess it will be much lower than what average investors are lead to believe as “magic of the stock market”.

Hello sir,

Thanks!

Since this data s from 1980 and the average returns over various buckets are about 18% and inflation was way below that, I did not mention the inflation. But if we do take a shorter time frame say from 2000, it would certainly make a case for equity not being invincible. Tks, Vidya

Thanks for your valuable inputs on investments. But, the amount I invested in 2007 in MFs is giving only 3% returns as on today. If i had redeemed the amount when the Index was at its peak and re-invested again when it reached the bottom, I would have earned more returns. The main point is after seeing the peak and bottom, now, I can think of doing it in a better way. But, while the index is going up or down, we cannot identify whether it is a peak or bottom. Could you suggest me a solution for this ?. Thanks.

Hello Saravanan, the simplest way out for this is doing portfolio rebalancing. Pl. read this for mroe info: https://blog.fundsindia.com/blog/mutual-funds/buying-low-and-selling-high-made-possible/2849

tks

I kind of agree with Mr. Saravanan. I had also done investments in late 2007 in MF and as on today the net gain is around 5 percent. Can we get net consolidated PE values for all the equity funds viz -a-viz their respective benchmarks on fundsindia? This will help us in identifying that are we buying/selling cheap or expensive.

Hello Jaspreet, Good funds delivered well even from the peak. I am myself an investor and can vouch for that! End of day – only 2 things matter – a regular review to weed our underperformers and rebalance the portfolio automatically as I pointed to Mr Saravanan. This strategy does not require you to time markets and make entries and exits. An inflated portfolio will automatically be pushed to its original allocation. It is simple and effective. Do pl. read: https://blog.fundsindia.com/blog/mutual-funds/buying-low-and-selling-high-made-possible/2849

Thanks.

Dear Vidya, Great article. Wonderful…and thanks for deep analysis.

Vidya,

very nice article.

One reason all mutual funds and all advisers blindly recommend equity for long term is it could beat inflation but not fixed income securities. But they fail to mention the probability of the outcome over certain period of time. Assuming 7% inflation, even for longer period of 10 years holding, ( for average Indian investor 1 year is long term ! ), 100% equity portfolio does not have 100% probability to beat inflation. No one mentions this.

Investment planners talk about returns as though it is sure thing with longer holding period but not probability of getting it. This mislead average investor to believe return is the only thing to worry about. It is nice to see that you covered the probability along with return numbers.

Since equity are recommended as the only instrument to beat inflation, it could have been better if you published the probability of an equity portfolio beating inflation over 3 years period, 5 years and 10 years period. I guess it will be much lower than what average investors are lead to believe as “magic of the stock market”.

Hello sir,

Thanks!

Since this data s from 1980 and the average returns over various buckets are about 18% and inflation was way below that, I did not mention the inflation. But if we do take a shorter time frame say from 2000, it would certainly make a case for equity not being invincible. Tks, Vidya

Thanks for your valuable inputs on investments. But, the amount I invested in 2007 in MFs is giving only 3% returns as on today. If i had redeemed the amount when the Index was at its peak and re-invested again when it reached the bottom, I would have earned more returns. The main point is after seeing the peak and bottom, now, I can think of doing it in a better way. But, while the index is going up or down, we cannot identify whether it is a peak or bottom. Could you suggest me a solution for this ?. Thanks.

Hello Saravanan, the simplest way out for this is doing portfolio rebalancing. Pl. read this for mroe info: https://blog.fundsindia.com/blog/mutual-funds/buying-low-and-selling-high-made-possible/2849

tks

I kind of agree with Mr. Saravanan. I had also done investments in late 2007 in MF and as on today the net gain is around 5 percent. Can we get net consolidated PE values for all the equity funds viz -a-viz their respective benchmarks on fundsindia? This will help us in identifying that are we buying/selling cheap or expensive.

Hello Jaspreet, Good funds delivered well even from the peak. I am myself an investor and can vouch for that! End of day – only 2 things matter – a regular review to weed our underperformers and rebalance the portfolio automatically as I pointed to Mr Saravanan. This strategy does not require you to time markets and make entries and exits. An inflated portfolio will automatically be pushed to its original allocation. It is simple and effective. Do pl. read: https://blog.fundsindia.com/blog/mutual-funds/buying-low-and-selling-high-made-possible/2849

Thanks.

Are the figures given in the rolling returns table are compounded or simple?

Hello sir,

Returns over one year are compounded in the rolling return table. tks

Are the figures given in the rolling returns table are compounded or simple?

Hello sir,

Returns over one year are compounded in the rolling return table. tks

There are funds like ‘Franklin India Opportunities’ where the returns are less than 4% / year – less than the returns one would have got from simple saving bank account. For this type of fund , as the fund house replied to me, 7 years period is not enough. By the way what does a fund managers job ?

Hello Rajiv, Yes, it is rather unfortunate. But That is the opportunity loss of not reviewing a fund. If all fund managers performed well and all analysts got their calls well, the Indian markets would not be delivering long-term returns of 12-18%. it would be low single digits because there would be no undiscovered opportunity or arbitrage opportunity. Thanks.

The article is worth reading for any type of investors. I have a question here for you is it better to redeem the profits in the mutual fund when the index is at peak and re-invest in same mf or different mf even before the goals are reached or just stay intact with the fund. Will this have any impact on power of compounding

Hello Satish, Clearly one cannot time one’s exit or profit booking. this is what rebalancing is an ideal startegy. Pl. read this if you need more inputs on rebalancing: https://blog.fundsindia.com/blog/mutual-funds/buying-low-and-selling-high-made-possible/2849

Thanks.

There are funds like ‘Franklin India Opportunities’ where the returns are less than 4% / year – less than the returns one would have got from simple saving bank account. For this type of fund , as the fund house replied to me, 7 years period is not enough. By the way what does a fund managers job ?

Hello Rajiv, Yes, it is rather unfortunate. But That is the opportunity loss of not reviewing a fund. If all fund managers performed well and all analysts got their calls well, the Indian markets would not be delivering long-term returns of 12-18%. it would be low single digits because there would be no undiscovered opportunity or arbitrage opportunity. Thanks.

The article is worth reading for any type of investors. I have a question here for you is it better to redeem the profits in the mutual fund when the index is at peak and re-invest in same mf or different mf even before the goals are reached or just stay intact with the fund. Will this have any impact on power of compounding

Hello Satish, Clearly one cannot time one’s exit or profit booking. this is what rebalancing is an ideal startegy. Pl. read this if you need more inputs on rebalancing: https://blog.fundsindia.com/blog/mutual-funds/buying-low-and-selling-high-made-possible/2849

Thanks.

Hi Vidya

There is a churn in the Nifty / Sensex constituents over a period of 10 years. So close to 50% of the constituents that formed part of the index 10 years agao are now no longer part of the index. So would it be reasonable to compare forward vauations now vis-a-vis forward valuations in 2001?

Hello ramkumar, that is true of all indices across markets. The fact is that a benchmark index has reasonable exposure to key companies and sectors and it is the valuation of those that matter at any point in time . Forward valuations in 2001 was a reflection of how the earnings of the then bluechips were expected to grow and the forward P/E now is an expectation from current bluechips. End of day, they represent the market and that is why they are in the index. A stock that is no longer believed to adequately represent the market is removed and rightly so. Hence, index valuations at any time offer good comparables. Thanks.

Hi Vidya

There is a churn in the Nifty / Sensex constituents over a period of 10 years. So close to 50% of the constituents that formed part of the index 10 years agao are now no longer part of the index. So would it be reasonable to compare forward vauations now vis-a-vis forward valuations in 2001?

Hello ramkumar, that is true of all indices across markets. The fact is that a benchmark index has reasonable exposure to key companies and sectors and it is the valuation of those that matter at any point in time . Forward valuations in 2001 was a reflection of how the earnings of the then bluechips were expected to grow and the forward P/E now is an expectation from current bluechips. End of day, they represent the market and that is why they are in the index. A stock that is no longer believed to adequately represent the market is removed and rightly so. Hence, index valuations at any time offer good comparables. Thanks.

Hi Vidya,

Well explained. Thanks for your research in equity markets.

I have lost more than 2 lacs in trading.

Now I am planning to invest only in MFs.

Is it good time to start investing in SIP?

If yes, can you please suggest me two funds.

And now PSU Banks are at 50% discounted price compared to one year before. So is it good to invest in banking funds now?

Hello Mani, This is certainly a good time to start SIPs if you have an atleast 3-5 year view. Portfolio suggestions can be sought using the ‘Ask advisor’ feature available for all FundsIndia account holders.

As for banking, you would have to take your own call as more volatility is expected in banking sector with NPA provisions of public sector banks seeming high.Staggered exposures with a 5-year term may be a better way of investing, if you are looking at banking funds. Tks.

Hi Vidya,

Well explained. Thanks for your research in equity markets.

I have lost more than 2 lacs in trading.

Now I am planning to invest only in MFs.

Is it good time to start investing in SIP?

If yes, can you please suggest me two funds.

And now PSU Banks are at 50% discounted price compared to one year before. So is it good to invest in banking funds now?

Hello Mani, This is certainly a good time to start SIPs if you have an atleast 3-5 year view. Portfolio suggestions can be sought using the ‘Ask advisor’ feature available for all FundsIndia account holders.

As for banking, you would have to take your own call as more volatility is expected in banking sector with NPA provisions of public sector banks seeming high.Staggered exposures with a 5-year term may be a better way of investing, if you are looking at banking funds. Tks.

Hi Vidya

Can you comment of UTI Opportuntines fund- does this comes under large cap or Large and mid cap sector. Am planning to do SIP in this fund after comparing the ratings and other stats from the websites and for me these fund seem to be doing good in all markets. Am planning to replace this fund with DSPBR top 100, which am holding since 2 yrs in SIP. Whats opinion on these.

Hello satish, UTI Opportunities is a diversified fund with a large-cap bias currently. It has a steady record. Tks, Vidya

Hi Vidya

Can you comment of UTI Opportuntines fund- does this comes under large cap or Large and mid cap sector. Am planning to do SIP in this fund after comparing the ratings and other stats from the websites and for me these fund seem to be doing good in all markets. Am planning to replace this fund with DSPBR top 100, which am holding since 2 yrs in SIP. Whats opinion on these.

Hello satish, UTI Opportunities is a diversified fund with a large-cap bias currently. It has a steady record. Tks, Vidya

Hi My name is Vijay. Recently I came to know about this through my friend and seeing this very informative. As I am new to SIP, I learnt a lot of things from this. I need a advice from you. As I want to start a SIP below are my options. Please give me your expert advice. My age is 29 married and I am some risk taker for good returns.

Generally my savings would be monthly Rs.5,500

Large cap Funds – 40% Approx.

Birla Sun Life Frontline Equity – Rs. 1000

HDFC top 200 – Rs. 1000

Large & Mid cap Funds – 15% Approx.

Quantum long term equity – Rs. 1000

Mid & Small cap Funds – 15% Approx.

HDFC Midcap opportunities fund – Rs. 1000

Diversified Equity funds – 20% Approx.

PPFAS long term value fund – Rs. 1000

Sector Funds – 10 %

ICICI Prudential FMCG – Rs. 500

Thanks in Advance

Hello Vijaya Kumar, thank you for writing to us. You have largely allocated well. But you need to keep in mind a few points:

1. have you done the allocation based on your risk profile as well as the time frame/investment goal?

2. Did you not find the need for some debt component because you already have sufficient exposure to debt? Debt is important to add stability to a portfolio.

3. Did you choose the sector fund because you believe the them holds promise?

4. Did you go for a new fund like PPFAS because you know how Parag Parikh’s strategy works or simply went because it was an NFO?

5. Do you need 6 funds for a Rs 5500 SIP?. You may add lot more funds when your SIP amt increases. Would you end up having one too many later, if you start with 6 funds now?

Do reassess in light of these questions. If you wish us to do a portfolio or review the same, or simply have a chat with our advisors to make a start, kindly use the ‘Ask Advisor’ feature in Fundsndia once your account is activated. This service is free of cost for all our investors. Thanks, Vidya

Hi My name is Vijay. Recently I came to know about this through my friend and seeing this very informative. As I am new to SIP, I learnt a lot of things from this. I need a advice from you. As I want to start a SIP below are my options. Please give me your expert advice. My age is 29 married and I am some risk taker for good returns.

Generally my savings would be monthly Rs.5,500

Large cap Funds – 40% Approx.

Birla Sun Life Frontline Equity – Rs. 1000

HDFC top 200 – Rs. 1000

Large & Mid cap Funds – 15% Approx.

Quantum long term equity – Rs. 1000

Mid & Small cap Funds – 15% Approx.

HDFC Midcap opportunities fund – Rs. 1000

Diversified Equity funds – 20% Approx.

PPFAS long term value fund – Rs. 1000

Sector Funds – 10 %

ICICI Prudential FMCG – Rs. 500

Thanks in Advance

Hello Vijaya Kumar, thank you for writing to us. You have largely allocated well. But you need to keep in mind a few points:

1. have you done the allocation based on your risk profile as well as the time frame/investment goal?

2. Did you not find the need for some debt component because you already have sufficient exposure to debt? Debt is important to add stability to a portfolio.

3. Did you choose the sector fund because you believe the them holds promise?

4. Did you go for a new fund like PPFAS because you know how Parag Parikh’s strategy works or simply went because it was an NFO?

5. Do you need 6 funds for a Rs 5500 SIP?. You may add lot more funds when your SIP amt increases. Would you end up having one too many later, if you start with 6 funds now?

Do reassess in light of these questions. If you wish us to do a portfolio or review the same, or simply have a chat with our advisors to make a start, kindly use the ‘Ask Advisor’ feature in Fundsndia once your account is activated. This service is free of cost for all our investors. Thanks, Vidya

Hi Vidya, Thank you for your elaborated reply.

1. This is the minimum amount I want to invest monthly. So My salary increases yearly. So Excess of Rs.5500 I will invest in others for my short term goals.

2. Right now I dont want to invest in debt funds. May be Excess of Rs.5500 I will invest.

3.I do beleive in FMCG / Health Care will grow in long run in a developing country like India. So I selected FMCG. If you know any good Health Care MF let me know.

4. I am a big fan of Parag Parikh. I liked his strategy to concentrate on single MF.

5.If I want to increase my SIP amount I will adjust it in the above mentioned funds and after 10yrs I will re-access my SIP.

I already applied for the account in Fundsindia. I need to send the documents.

Fine Vijay.Once you have an activated account, we would be able to respond to portfolio queries or do portfolio review as well using Ask Advisor. Thanks, Vidya

Hi Vidya, Thank you for your elaborated reply.

1. This is the minimum amount I want to invest monthly. So My salary increases yearly. So Excess of Rs.5500 I will invest in others for my short term goals.

2. Right now I dont want to invest in debt funds. May be Excess of Rs.5500 I will invest.

3.I do beleive in FMCG / Health Care will grow in long run in a developing country like India. So I selected FMCG. If you know any good Health Care MF let me know.

4. I am a big fan of Parag Parikh. I liked his strategy to concentrate on single MF.

5.If I want to increase my SIP amount I will adjust it in the above mentioned funds and after 10yrs I will re-access my SIP.

I already applied for the account in Fundsindia. I need to send the documents.

Fine Vijay.Once you have an activated account, we would be able to respond to portfolio queries or do portfolio review as well using Ask Advisor. Thanks, Vidya