Fear and rationality are often thrown with reckless abandon in equity market rallies. 2003-07 did see investors do this; but they paid quite a heavy price in the ensuing fall. While we are already well into over 52 weeks without any meaningful correction (historically, on an average, a rally corrects itself after 34 weeks), many investors may be tempted to make bolder moves in their quest for higher returns over a short span.

Lest you join the bandwagon, here are a few simple rules that may keep you from going overboard.

Mistake #1 – Changing your asset allocation to suit market movements

Your asset allocation, which is the proportion of equity, debt or gold that you own is dependent on your goals, your time frame, and your risk appetite. It does not have anything to do with market movements. Going overboard on equity in the euphoric markets of 2007, or loading up on gold and debt in 2012, would not have done you any good even as the same asset classes fell in the respective year that followed.

This happens when you try to participate in an asset class after it is already overheated. But then, how will you ever know that an asset class is overheated? Well, not until the bubble bursts. Then how do you participate in asset classes at the right time? A much simpler way out would be to look inward – into your own portfolio.

What to do: If you had an asset allocation of say 60:40 or 70:30 in equity and debt, your task is to maintain it around that level with a leeway of 5-8 percentage points, higher or lower. Here’s how asset rebalancing will actually help you go low on overheated asset classes and up your exposure to an underweight asset class:

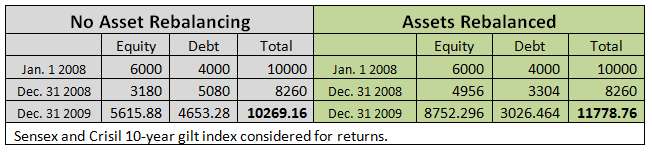

The table below shows the change that a Rs. 10,000 portfolio with the above asset allocation would have undergone, without rebalancing, and with rebalancing done at the end of the year. Let us suppose you had a 60:40 equity:debt asset allocation and in a year such as 2008, your allocation in equity may have fallen to about 38% while debt, which rallied well, would have gone up to 62%.

Now, had you done an annual asset rebalancing, you would have simply upped your exposure in equity back to 60% by booking profits in debt and bringing the latter to 40%. By doing this, you would have bought equities in their lows and actually sold debt in their highs. Irrespective of whether you had an equity rally in the next year, that is in 2009, or not, you managed to buy equities at their lows. That would eventually help you gain more, whenever the markets pick up. You can see the result in the above table in December 2009. The portfolio that was rebalanced gained more.

The same would be true in a year such as 2007, when you would have cut down your exposure in equities and increased it in debt. Hence, instead of trying to second guess the markets, read into what your portfolio is trying to tell you – annually. That’s all it takes.

Mistake #2 – Looking at short-term performance

Almost 90% of your portfolio is bound to become error-free if you avoid the above mistake. But then fund returns may tempt you to choose the ‘in’ funds, instead of time-tested, seemingly sober ones. That is where you need to tread carefully.

First, one-year returns of 100% or more will never repeat itself. Hence, to choose funds that delivered so, while believing a repeat century is possible, would be imprudent. Second, invariably, in a market upswing, especially in the ones after prolonged volatility or weakness, funds that are loaded with beaten-down stocks tend to go up. This is because cheap stocks tend to rise with the market in a momentum rally.

That does not mean a fund has started outperforming. For all you know, it may simply mean an opportunity for investors stuck with such a fund to exit it.

Third, the above 2 points are especially true when it comes to mid-cap funds. These funds will tend to outperform by a mile in a market recovery, showcasing impressive one-year returns that cannot repeat. Besides, when such returns woo investors into determinedly going after a few such funds, it may suddenly cause a hike in assets under management, causing the fund to struggle to deploy the same in opportune mid and small-cap stocks.

Stick to funds with established long-term record and do not unnecessarily switch them because they have lagged peers for 6 months or 1 year. As long as the fund has beaten the benchmark, its underperformance, if any, over other established peers is not over 5 percentage points, and its strategy is convincing to you, you have little reason to disturb your portfolio.

To go for ‘in’ funds based on short-term performance may turn out to be a ‘not so cool’ decision over the long run.

Mistake #3 – Going for hot themes

If you are not doing any of the above cool mistakes, then you are probably going after ‘hot’ themes. Infrastructure was hot in 2007. FMCG was hot until 2012. US-focused funds were hot in 2012. European funds were hot in 2013. We could go on.

The simple truth here is that – they have already become hot. That means there could well be a bubble. Hence, if you choose to enter them now, you may well burn your fingers!

No doubt, themes can play a part in either providing kicker returns to your portfolio, or to provide diversification. But then, you need to be doing three things to add them to your portfolio – one, you should be willing to track them; two, you should not load more than 10% of your portfolio with such themes, and three, you should be willing to exit when you see money and not wait for the last bubble in the theme to burst.

If all these are not easy for you, then remember, most of the local themes (and in some cases even international stocks (PPFAS Equity, Templeton India Equity Income are examples) are available in diversified equity funds. Diversified funds help you ride the sector at reasonably opportune times, while dynamically shifting allocation when they seen the trends turn.

Following these simple rules will more or less shock-proof your portfolio from market inanity, as well as your own mistakes. If the above piece of suggestion makes you doubt where equities stand now, here’s some data to cheer you:

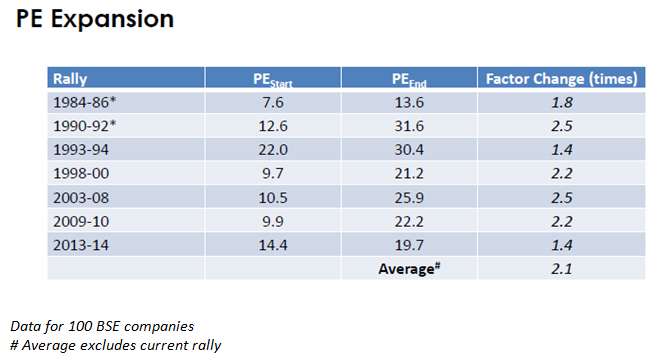

The data above shows how the number of times the price earnings ratio rises between the beginning and peak of a rally. The good news is that the current rally has not driven the P/E to the average levels seen before, suggesting scope for expansion. Besides, earnings growth has just picked up, providing scope for P/Es to remain less pricey. That means, we are unlikely to be in a bubble territory.

Happy investing!

Disclaimer: Returns mentioned are past returns and are not indicative of future performance.

To know how to read our weekly fund reviews, please click here.

Timely one.

Hi,

Thanks for the wonderfully articulated write-up and to be honest I’m quite impressed to note and also take the opportunity to appreciate the quality and balanced approach advised by you as against the general notion of hard-sell.

Please keep up the good work.

Regards,

Prem.

Thanks, Prem. Vidya

Timely one.

Hi,

Thanks for the wonderfully articulated write-up and to be honest I’m quite impressed to note and also take the opportunity to appreciate the quality and balanced approach advised by you as against the general notion of hard-sell.

Please keep up the good work.

Regards,

Prem.

Thanks, Prem. Vidya