Well, my answer is ‘it depends’. Don’t be disappointed. If you knew the factors that determine the number of funds you need to hold, you will likely have the answer yourself. So here’s what you need to take into account before choosing the number of funds to hold in a portfolio.

The amount

While this is not the first thing to really influence your decision, it is the most practical point to consider when investing, especially by small, retail investors. If you had Rs. 1,000 or Rs. 2,000 to invest every month, you can’t possibly have an asset balanced, category allocated, and style-diversified portfolio of funds. It leaves you with an option of one or two funds at best.

When you have a single-fund portfolio, it is a good idea to get these right: one, the choice (debt or equity fund) of asset class based on your time frame; two, if it is an equity fund, do not hold a mid/small cap, theme, or international fund as the one fund you hold.

Often times, this is one reason why many first-time investors are disenchanted with mutual fund investing. They would have chosen a risky fund to begin with, and would have probably burnt their fingers in a down market.

If you have a higher sum to invest – say Rs. 5,000 or above, then arises the question of asset allocation and diversification.

Asset allocation

If you need to allocate across asset classes, then you may need 2 or more funds, unless you think a balanced fund would suffice. If you are investing in a portfolio with a specific goal in mind, then ensure you have a proper asset allocation based on the goal and time frame.

If you are clear that you have already allocated certain sums outside of mutual funds for certain asset classes like debt or gold (say deposits or physical gold) for the said goal, then this might be a less significant factor to consider. Otherwise, asset allocation helps capitalise the returns across various asset classes, while acting as a hedge against the other assets.

Once you decide the proportion of equity, debt or gold to hold – the next requirement would be to decide how many funds to hold within each asset class.

Diversification

Now, this is key. If you are an investor who does not think you need a portfolio diversified across market cap or different styles of investing, then holding one or two diversified equity funds, and perhaps an income fund for debt may suffice, provided you are a long-term investor.

Of course, when you have a concentrated portfolio, make sure you get the funds reviewed at least annually as the risk profile of your portfolio would be high as a result of taking fewer bets.

But if you like to diversify across higher risk and lower risk funds, and across fund houses and fund management styles, then you will need more funds. Here are some general tips that may help you in your choice:

Diversification across market-cap segments

1. You don’t need ‘diversification’ across large caps. This is because, given the restricted universe within which large-cap funds can operate, you are unlikely to get different sets of stocks, or markedly varying styles of investing. Hence, unless you want a portfolio of only large caps, holding one large-cap fund should do the job for you.

2. Diversified/multi-cap funds come in different forms and shape. But largely, most of them have a large-cap bias, and seldom go overboard on mid-cap stocks. Funds such as Mirae Asset India Opportunities, or UTI Opportunities are good examples. Hence, if the amount you can spare to invest is not high, and you have a moderate risk appetite, you can even skip a large-cap fund and choose a diversified fund with a good track record.

You can specifically ask your advisor to provide you with a relatively low-risk diversified fund if you are skipping the large cap category. This is one way to ensure your portfolio remains compact.

3. A mid-cap fund is a good addition if you are building wealth for the long term and can take some risk. But in general, given that it is not too prudent to hold over 30 per cent of your portfolio in mid-cap funds, you may not be able to accommodate too many funds within this segment.

If you are going for just one fund – choose one that invests in mid-caps, but not too much in small caps, and has at least a fifth or more in large caps as well. Just to illustrate, within FundsIndia’s Select Funds’ list, funds such as HDFC Mid-Cap Opportunities, BNP Paribas Mid Cap, or Franklin India Prima will fit this description well.

If you are the aggressive kind and need funds that explore lesser known stocks, then adding one more is fine, provided you have that much money to spare. Again, to illustrate, funds such as Franklin India Smaller Companies or UTI Mid Cap may fit this description.

4. While it is market-cap segment in equities, it is portfolio maturity and credit risk in debt. Here, too much diversification is not required as most funds follow the interest rate cycle and invest accordingly. As a thumb rule, if your time frame is short, go for funds with low portfolio maturities (short-term debt funds). You don’t need too many funds in this category.

If you are looking for long-term investing in debt, the simplest option to avoid crowding is to choose a fund that will invest across instruments (gilt, corporate bond, commercial paper, deposits), and also vary its portfolio maturity based on the interest rate cycle. 1-2 funds should suffice.

Funds that will take exposure to credit, and specifically have corporate bonds as a theme, etc., are only for risk takers. View these as equivalent to holding theme funds in equity.

If you have done your diversification across market-cap segments (that roughly provides a diversified risk profile), do not bother too much to diversify across styles such as growth, value, contra, dividend yield, etc., unless, you really understand them and see merit in such diversification.

Why am I saying this? Because most of the time, you would have already got mixed styles when you attempted the earlier point we discussed. Besides, many funds have a thin line of differentiation across these styles; in other words, most funds mix and match these styles. A growth fund may take a value form in some markets too!

If you have these as a part of pre-packaged portfolios, good for you. If you are choosing on your own, then make sure that you know what style of investing suits certain market conditions before you invest.

In our opinion, this stage is something you can skip unless you keenly follow certain schools of investing (like you are a hard core ‘value’s seeker).

Other diversity

Theme funds, international funds, and so on are all add-ons to your portfolio. The allocation you can give to them is best restricted to 10-15 per cent; and that means the number of funds you can hold in this space cannot exceed one or two.

Again, unless you have some conviction in this diversification – either for the sake of seeing some high returns, or for true geographic diversification/hedge – this is also something that you can skip in your endeavour to keep your portfolio compact.

Same funds for different purposes

All that we are talking of here is the number of funds for a single portfolio that is built towards a specific goal. So, you may have 3 funds for your child’s education and 4 funds for your retirement. Treat each portfolio as a unit. In this, no harm in having the same funds earmarked for different goals. After all, if a fund performs well, it is only good to have them for your goals, albeit different ones.

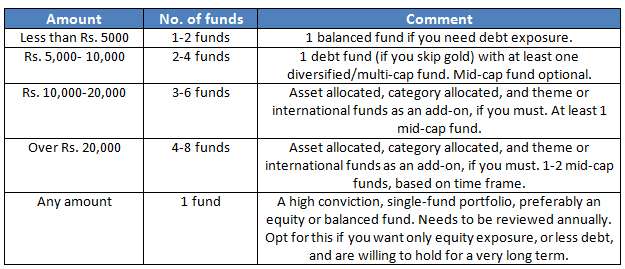

No one size, but…

Here’s a table just to give you an idea of how to decide the number of funds in a portfolio.

The above is merely suggestive and assumes a long-term 5-year holding at least. As discussed above, those who love diversification may choose more, and those who like to keep it compact may keep it less within the categories.

In my experience if you want to invest 20000 per month we have to choose 10 funds each 2000 sip in different dates which will absorb market volatility. The funds are multi cap, midcap, large cap , balanced each2 funds and micro cap , small cap each one.

Hello Venkat, not necessarily. some times just one diversified fund/large-cap fund, one midcap and one debt fund can also do the job for you 🙂 It depends on the choice of funds. thanks, Vidya

Hi,

Can you advice on the my below portfolio of 13000 PM SIP for 15 years.

SBI Bluechip Direct Growth : 2000

Kotak Select Focus Direct Growth : 2000

ADBSL Equity Direct Growth Fund : 2000

HDFC Balanced Direct Growth :2000

DSP black rock microcap Direct Growth : 2000

Mirae Asset Emerging Bluechip : 1000

DSP black Rock Tax Saver Direct Growth : 2000

thanks

Hello,

We don’t provide portfolio-specific reviews or queries on this forum. Queries are routed through our platform. This blog is meant primarily for discussion and informative articles. Please talk to your advisor on your portfolio.

Thanks,

Bhavana

Nice Article. Enjoyed it.

Great article clears most of my doubts. i invest 23k per month in sips of 5 equity mutual funds-1 elss and 4 large and midcap equity.

What is the maximum sip amount for a scheme?

Since i want to exhaust my 80c limit I am investing 8k in elss , is it risky? But when i wanted to split to 2 elss funds then they are very much co-related.

Hello Arun – The maximum per scheme is purely dependent on the overall allocation and the nature (risk profile) of the fund. For example: If you have a single mid-cap fund then the max can be 20-30%. and so on. Same holds good for max SIP per scheme. Rs 8000 in one ELSS fund is fine provided it is not a risky fund. For further fund-specific queries if any, please use the advisor appointment feature if you have a FundsIndia account to provide any specific advice. thanks, Vidya

One of the best articles that I’ve read on this topic. I would like some actual fund recommendations for this point that you make: “If you are looking for long-term investing in debt, the simplest option to avoid crowding is to choose a fund that will invest across instruments (gilt, corporate bond, commercial paper, deposits), and also vary its portfolio maturity based on the interest rate cycle. 1-2 funds should suffice.”. I’m building my debt portfolio and am confused by the inconsistent categories used by various websites – each has their own name for different debt categories.

Hello Pavan, thanks. Look for income funds/dynamic bond funds if you have a long-term time frame of 3-plus years. As for fund recommendations, we would be constrained from giving it in this forum. the blog is a general discussion forum. If you are a FundsIndia inevstor, please use the ‘advisor appointment’ feature in the help tab and post your query. We will understand your requirement and call or mail you as you need. This will also help us keep track fo queries and respond efficiently. thanks, Vidya

Hi,

I am a senior citizen having an account under National Savings Scheme, 1987. I would like to withdraw full amount with least Tax implication.Please suggest best option available to me.

Thanks,

Sathyamurthy G

Hello Sir, NSS is subject to tax unlike NSC. So you can’t do much there. You can withdraw and invest in Post Office Senior citizens’ scheme and get 80C benefit (if you wish to save tax) and if you need regular interest income. Mutual funds are suitable if you do not expect imemdiate regualr income from the corpus. thanks,Vidya

Hi,

Thanks for your suggestion and prompt response.

Regards,

Sathyamurthy G

I have never understood the logic of midcap funds? can you please explain it to me

Hello Prijesh, This ppt will tell all you about mid caps. It id dated but relevant in terms of its explanation. thanks, Vidya

Hi Bala,

I want to invest Rs10000 per month in ELSS fund.Please let me know how many funds should i choose and how it can be diversified.I am tracking few ELSS funds from Feb 2015 till now but i can see NAV increase when share market goes up and it went down when market goes down.IN last three years market goes very well but suppose market after 3 years is 30000 only then we have a loss in ELSS funds as NAV is based on market indices.

Hi Piyush, Sorry for the delay in reply.

As ELSS funds invest in equity markets, they will, naturally fall and grow with the market. You should not be put down by short-term falls. In the long term 5-10 years, the chances of negative returns (historically) in the market is nil unless something is terribly wrong with the economy. ELSS funds too need long time frame. The lock in may be 3 years but like any other equity fund you should consider 5 year holding to play out volatility. Plese read our article if you are a first time equity investor pl. read this: https://blog.fundsindia.com/blog/advisory/fundsindia-strategies-the-equity-fund-playbook-for-rookie-investors/7667

For the amount mentioned by you 2 funds should do. We will be able to provide you suggestions on funds if you ask your query through your activated fundsIndia account – using the advisor appointment feature. It is free for all our investors. The blog is only a forum for discussion. thanks, Vidya

Please explain

Great article. I’m fundsindia investor. I’m investing with 20 year target. Portfolio funds are : ICICI FOC – 20%, BIRLA F/L EQ – 20%, UTI OPP – 10%, HDFC PRU – 10%, ICICI DISC -20%, FRANKLIN SM COS. -20%. My goal is wealth creation over long-term. Should I make any changes.

Hello Sir, I do not find all the said funds in your portfolio under this current email (only some are there). It is easier for us to know your entire investments before recommending anything. If you have some of your investments offline, bring them in and consolidate so that you can manage them easily. IF you already have them, pl mention the email ids of your accounts when you write to us using the below feature. Our advisors will help you review your portfolios if you request using the ‘Advisor appointment’ feature when you click help tab. The funds you mentioned here are all good but remember Franklin Smaller Cos is a risky bet and a 20% exposure can be high. Also you do not have debt. If you wish to reallocate, as suggested pl use the feature mentioned above. The blog is merely a discussion forum. thanks, Vidya

Could you please review my portfolio

Birla SL Frontline Equity Direct-G 1,000 per month

HDFC Equity-G 1,000 per month

HDFC Mid-Cap Opportunities- G 2,000 per month

ICICI Pru Balanced Direct-G 1,000 per month

ICICI Pru Focused Bluechip Equity Direct -G 2000

Kotak Select Focus Direct-G 1,000 per month

Reliance Equity Opportunities-G 1000 per month

Ashish, Kindly activate your FundsIndia account. If you are already an investor, please write to us using the ask advisor feature (in help tab). As a FundsIndia investor, we will help you review your portfolio and also consolidate them in one platform, online, with us. thanks. The blog is merely a discussion forum. We will be constrained from offering ortfolio specific comments here. Vidya

Hi Vidya,

I’m 30 Yrs old. Please review my portfolio and suggest me if any…

1-LIC Life insurance cum retired plan : 50K per year, need to pay next 20 yrs

2- Bank FD: 300000

3- SIP Details as below(Monthly Basis)

1)Franklin India Tax Shield – Growth(ELSS)

Rs.2000/-

2)Axis Long term equity fund – Growth(ELSS)

Rs.2000/-

3)BNP Paribas long term equity fund – Growth(ELSS)

Rs.1000/-

4)Franklin India Prima fund – Growth(Mid cap & Small cap)

Rs.1000/-

5)Franklin India Smaller companies fund – Growth(Mid cap & Small cap)

Rs.1000/-

6) ICICI Prudential value discovery fund – Growth(Diversified Equity)

Rs. 1000/-

7) HDFC Balanced Fund – Growth(Balanced Fund)

Rs. 2000/-

LumpSum…

1. Franklin India Tax shield(ELSS invested to save tax for last FY 15-16)

Rs.50000/-

2. Axis long term equity fund(ELSS invested to save tax for last FY 15-16)

Rs.50000/-

Is it good and safe decision to continue above mentioned SIPs for next 10 years?. I’m expecting 15% to 20% return for over all tenure.

Please suggest me if any changes required in my portfolio and kindly suggest me to buy some other safe mutual funds to balance risk if I would have taken high risk by opting above mentioned funds.

Thank you With Great anticipation!

Hello sir,

We’re constrained from providing portfolio-specific advice in this forum. It is meant as a public discussion platform only. So request you to log into your FundsIndia account and schedule an appointment with your advisor. I hope you realise that, however, a return expectation of 15-20% is high. You would have to take excessive risk.

Thanks,

Bhavana

Hi Vidya,

I’m 30 Yrs old. Please review my portfolio and suggest me if any…

1-LIC Life insurance cum retired plan : 50K per year, need to pay next 20 yrs

2- Bank FD: 300000

3- SIP Details as below(Monthly Basis)

1)Franklin India Tax Shield – Growth(ELSS)

Rs.2000/-

2)Axis Long term equity fund – Growth(ELSS)

Rs.2000/-

3)BNP Paribas long term equity fund – Growth(ELSS)

Rs.1000/-

4)Franklin India Prima fund – Growth(Mid cap & Small cap)

Rs.1000/-

5)Franklin India Smaller companies fund – Growth(Mid cap & Small cap)

Rs.1000/-

6) ICICI Prudential value discovery fund – Growth(Diversified Equity)

Rs. 1000/-

7) HDFC Balanced Fund – Growth(Balanced Fund)

Rs. 2000/-

LumpSum…

1. Franklin India Tax shield(ELSS invested to save tax for last FY 15-16)

Rs.50000/-

2. Axis long term equity fund(ELSS invested to save tax for last FY 15-16)

Rs.50000/-

Is it good and safe decision to continue above mentioned SIPs for next 10 years?. I’m expecting 15% to 20% return for over all tenure.

Please suggest me if any changes required in my portfolio and kindly suggest me to buy some other safe mutual funds to balance risk if I would have taken high risk by opting above mentioned funds.

Thank you With Great anticipation!

Hello sir,

We’re constrained from providing portfolio-specific advice in this forum. It is meant as a public discussion platform only. So request you to log into your FundsIndia account and schedule an appointment with your advisor. I hope you realise that, however, a return expectation of 15-20% is high. You would have to take excessive risk.

Thanks,

Bhavana

Hi, I am a recent investor through Fundsindia, & below are the recommendations made for a tenure of 5 years.

Please suggest if there be any changes i need to make within this portfolio.

Birla Sun Life Frontline Equity Fund – Growth – 1,000 per month

Birla Sun Life Dynamic Bond Fund – Retail Plan – Growth- 1,000 per month

Mirae Asset Emerging BlueChip Fund – Regular Growth – 1,000 per month.

Hello Shruthi, we do not respond through the blog for individual reviews. I will send you a response to your mail through our ticketing system. In future, kindly use your FundsIndia account , help tab and send you query through the advisor appointment tab and we will provide a review.thanks, Vidya

I am Saket , 35 years old investing in mutual fund from Sep 2016 for my child higher education after 15 years. I have invested in DSP Black Rock Micro Cap(Direct Plan) for Rs 2500. Franklin Smaller Co Growth (Direct Plan) Rs 4000 DSP Tax Saver fund for Rs 5500 L&T India Value Fund(Direct Plan) for Rs 1000 & ICICI prud balance Fund growth Plan for Rs 5000. My target to get Rs 1 crore after 15 years for my child higher studies. Please let me know shall i go with the same above plans with the same amount or I need to invest more in different fund. Please advise

Saket, Thank you for writing to us and sorry about the delayed response. Since you have a planning and portfolio query, please write to us or contact your FundsIndia advisor through your account. We are constrained from offering personal advice on the blog. Please use our child education calculator to know if your savings is sufficient. http://www.fundsindia.com/content/jsp/calculators/MutulfundSipCalcAction.do?method=sipCalcHome

Thanks,

Vidya

Hi, I am a recent investor through Fundsindia, & below are the recommendations made for a tenure of 5 years.

Please suggest if there be any changes i need to make within this portfolio.

Birla Sun Life Frontline Equity Fund – Growth – 1,000 per month

Birla Sun Life Dynamic Bond Fund – Retail Plan – Growth- 1,000 per month

Mirae Asset Emerging BlueChip Fund – Regular Growth – 1,000 per month.

Hello Shruthi, we do not respond through the blog for individual reviews. I will send you a response to your mail through our ticketing system. In future, kindly use your FundsIndia account , help tab and send you query through the advisor appointment tab and we will provide a review.thanks, Vidya

I am Saket , 35 years old investing in mutual fund from Sep 2016 for my child higher education after 15 years. I have invested in DSP Black Rock Micro Cap(Direct Plan) for Rs 2500. Franklin Smaller Co Growth (Direct Plan) Rs 4000 DSP Tax Saver fund for Rs 5500 L&T India Value Fund(Direct Plan) for Rs 1000 & ICICI prud balance Fund growth Plan for Rs 5000. My target to get Rs 1 crore after 15 years for my child higher studies. Please let me know shall i go with the same above plans with the same amount or I need to invest more in different fund. Please advise

Saket, Thank you for writing to us and sorry about the delayed response. Since you have a planning and portfolio query, please write to us or contact your FundsIndia advisor through your account. We are constrained from offering personal advice on the blog. Please use our child education calculator to know if your savings is sufficient. http://www.fundsindia.com/content/jsp/calculators/MutulfundSipCalcAction.do?method=sipCalcHome

Thanks,

Vidya

Mam,

Presently I spent 5000 in ELSS and 2000 in icici value discovery, 2000 in Hdfc mid cap opportunity, 2000 in canara robeco emerging equity,,,, I plan to continue up to 15 /20 years for my daughter education,,,, marriage plans… Is it right or should move towards PPF?????? Please guide….

Regards.. Janak brahmbhatt.. Gandhinagar. Gujarat..

Hello Sir, Sorry for the delayed reply. For portfolio specific queries please route through your FundsIndia account, if you are an investor. We are constrained from giving any advice in a public forum. Vidya

Mam,

Presently I spent 5000 in ELSS and 2000 in icici value discovery, 2000 in Hdfc mid cap opportunity, 2000 in canara robeco emerging equity,,,, I plan to continue up to 15 /20 years for my daughter education,,,, marriage plans… Is it right or should move towards PPF?????? Please guide….

Regards.. Janak brahmbhatt.. Gandhinagar. Gujarat..

Hello Sir, Sorry for the delayed reply. For portfolio specific queries please route through your FundsIndia account, if you are an investor. We are constrained from giving any advice in a public forum. Vidya

Hi,

I am a new investor. I invested – DSP BlackRock Micro Cap Fund (Growth) – 7K SIP

Mirae Asset Emerging Bluechip Fund (Growth) – 3K SIP

HDFC Balaced Fund (Growth) – 2K

I want to invest 3-5K more thru SIP, which one i should choose.

I can take some risk and looking for long term wealth creation.

Please suggest.

Thanks

M. Lal

Hello,

This blog is for general personal finance articles and discussions. We are constrained from providing portfolio-specific advice here. If you are a FundsIndia customer, request you to please log into your FundsIndia account and schedule an appointment with your advisor.

Thanks,

Bhavana

FundsIndia

Hi,

I am a new investor. I invested – DSP BlackRock Micro Cap Fund (Growth) – 7K SIP

Mirae Asset Emerging Bluechip Fund (Growth) – 3K SIP

HDFC Balaced Fund (Growth) – 2K

I want to invest 3-5K more thru SIP, which one i should choose.

I can take some risk and looking for long term wealth creation.

Please suggest.

Thanks

M. Lal

Hello,

This blog is for general personal finance articles and discussions. We are constrained from providing portfolio-specific advice here. If you are a FundsIndia customer, request you to please log into your FundsIndia account and schedule an appointment with your advisor.

Thanks,

Bhavana

FundsIndia

What about mutual funds–how many mutual funds do you need to have a diverse enough portfolio? The answer is—you guessed it—it depends. Some funds, such as target-date funds, can deliver a lot of diversification in one package, providing exposure to stocks and bonds as well as U.S. and foreign securities. Investors can arguably obtain adequate diversification by buying a single target-date fund and calling it a day.

Meanwhile, an investor could build a 10-fund portfolio and still not achieve adequate diversification, assuming all the funds focused on a similar part of the market. That may sound farfetched, but it was actually the case in the laste 1990s, when many investors amassed multi-fund portfolios with a strong bias toward growth stocks, especially technology names. Seven large-growth funds simply won’t diversify a portfolio the same way owning one large-blend fund and one small-value fund and one small-growth fund would. Read more at : http://assetmanagement.kotak.com

What about mutual funds–how many mutual funds do you need to have a diverse enough portfolio? The answer is—you guessed it—it depends. Some funds, such as target-date funds, can deliver a lot of diversification in one package, providing exposure to stocks and bonds as well as U.S. and foreign securities. Investors can arguably obtain adequate diversification by buying a single target-date fund and calling it a day.

Meanwhile, an investor could build a 10-fund portfolio and still not achieve adequate diversification, assuming all the funds focused on a similar part of the market. That may sound farfetched, but it was actually the case in the laste 1990s, when many investors amassed multi-fund portfolios with a strong bias toward growth stocks, especially technology names. Seven large-growth funds simply won’t diversify a portfolio the same way owning one large-blend fund and one small-value fund and one small-growth fund would. Read more at : http://assetmanagement.kotak.com

Is ELSS only for first time equity investors ?. if i already invested in funds, stocks then can i invest ?

If i have other avenues to fill 80c, is it advised to go for ELSS ?

Hi Sadha, ELSS is open for all investors and there are no restrictions. It doesn’t matter if you are invested in other funds and stocks. ELSS, compared to other Section 80C investments delivers better returns over the long-term. If you have 80C amounts left after your regular contributions like home loan, or children’s education, you can consider ELSS.

Thanks,

Bhavana

Is ELSS only for first time equity investors ?. if i already invested in funds, stocks then can i invest ?

If i have other avenues to fill 80c, is it advised to go for ELSS ?

Hi Sadha, ELSS is open for all investors and there are no restrictions. It doesn’t matter if you are invested in other funds and stocks. ELSS, compared to other Section 80C investments delivers better returns over the long-term. If you have 80C amounts left after your regular contributions like home loan, or children’s education, you can consider ELSS.

Thanks,

Bhavana

I am planning to invest around 1.5-2 lacs lumpsum amount in a debt fund. Should I invest it in a single debt fund or multiple debt fund?

Hello, you can invest in a couple of funds based on what your expectation is from the funds. Vidya

I am planning to invest around 1.5-2 lacs lumpsum amount in a debt fund. Should I invest it in a single debt fund or multiple debt fund?

Hello, you can invest in a couple of funds based on what your expectation is from the funds. Vidya

Dear Vidya, Your views on my portfolio. 1. Tata Balanced Fund-2lakhs 2. Franklin Prima Plus(Multicap) Fund-2lakhs 3. SBI Bluechip(Largecap) Fund- 2lakhs 4. Mirae Asset Emerging Bluechip(Midcap) Fund-1lakh 5. DSP Microcap(Smallcap) Fund-1lakh. Total – 8lakh. holding on to this portfolio.

Please evaluate.

Thanks.

Hello Reena,

Thank you for writing to us. If you are a FundsIndia investor, please write to us through your account and we will respond to your query. This is a public forum and we are constrained from giving individual advice through this.

thanks,

Vidya

Looks good to me as I am also an investor like you…. balanced portfolio

Dear Vidya, Your views on my portfolio. 1. Tata Balanced Fund-2lakhs 2. Franklin Prima Plus(Multicap) Fund-2lakhs 3. SBI Bluechip(Largecap) Fund- 2lakhs 4. Mirae Asset Emerging Bluechip(Midcap) Fund-1lakh 5. DSP Microcap(Smallcap) Fund-1lakh. Total – 8lakh. holding on to this portfolio.

Please evaluate.

Thanks.

Hello Reena,

Thank you for writing to us. If you are a FundsIndia investor, please write to us through your account and we will respond to your query. This is a public forum and we are constrained from giving individual advice through this.

thanks,

Vidya

Looks good to me as I am also an investor like you…. balanced portfolio

Dear Vidhya,

Nice article and explained in very easy and simple manner. I have a query. I have planned to invest 1Lakh per month through SIP. I have decided the allocation in the following manner.

Largecap/Large cap oriented low risk fund – 1 (30%)

Aggressive multicap fund – 1 (10%)

Midcap oriented Diversified Fund – 1 (15%)

Midcap Fund – 1 (15%)

Smallcap Fund – 1 (10%)

Now remaining 20%, I had initially planned for Dynamic bond. But I am thinking if one needs Debt Fund at all! Can I invest in Balanced Fund(Equity) and Balanced Fund(Debt)?

should Debt fund form part of one’s MF portfolio? Since My SIP amount is 1L and may increase to 1.5L, I am confused if I should go for Debt fund to balance my portfolio. Also I have made lumpsum investment(30L) in in the similar fashion. In that, I have on Long term Debt fund(5L). My next Financial goal is only after 5yrs(son’sedn). I can take more risk than moderate portfolio.

I request you to suggest if this allocation is okey or little adjustments need to be made? and advice on my Debt query.

Thank you.

Hello Yavika,

Yes you do need debt in your portfolio. How much of debt and whether through debt fund or balanced fund should be determined by your time frame and whether you can handle short-term falls. If you have longer time frame, debt allocation can be lower. Else it needs to be higher (50%-80% based on time frame). It is ok to have balanced fund to get some debt but remember that a 40% balanced fund holding will give you only 10% debt. Also, a balanced fund will fall in a down market; just that it will fall lesser than a regular equity fund. Would you be fine with it? I would say keep a equity:debt allocation with regular equity funds, some balanced fund and some debt funds. I will be unable to comment on your individual category allocation unless I know more details espcially on your holdings. If you are a FundsIndia investor, please use your FundsIndia account to write your query and our advisor will suitably help you. thanks, Vidya

Dear Vidhya,

Nice article and explained in very easy and simple manner. I have a query. I have planned to invest 1Lakh per month through SIP. I have decided the allocation in the following manner.

Largecap/Large cap oriented low risk fund – 1 (30%)

Aggressive multicap fund – 1 (10%)

Midcap oriented Diversified Fund – 1 (15%)

Midcap Fund – 1 (15%)

Smallcap Fund – 1 (10%)

Now remaining 20%, I had initially planned for Dynamic bond. But I am thinking if one needs Debt Fund at all! Can I invest in Balanced Fund(Equity) and Balanced Fund(Debt)?

should Debt fund form part of one’s MF portfolio? Since My SIP amount is 1L and may increase to 1.5L, I am confused if I should go for Debt fund to balance my portfolio. Also I have made lumpsum investment(30L) in in the similar fashion. In that, I have on Long term Debt fund(5L). My next Financial goal is only after 5yrs(son’sedn). I can take more risk than moderate portfolio.

I request you to suggest if this allocation is okey or little adjustments need to be made? and advice on my Debt query.

Thank you.

Hello Yavika,

Yes you do need debt in your portfolio. How much of debt and whether through debt fund or balanced fund should be determined by your time frame and whether you can handle short-term falls. If you have longer time frame, debt allocation can be lower. Else it needs to be higher (50%-80% based on time frame). It is ok to have balanced fund to get some debt but remember that a 40% balanced fund holding will give you only 10% debt. Also, a balanced fund will fall in a down market; just that it will fall lesser than a regular equity fund. Would you be fine with it? I would say keep a equity:debt allocation with regular equity funds, some balanced fund and some debt funds. I will be unable to comment on your individual category allocation unless I know more details espcially on your holdings. If you are a FundsIndia investor, please use your FundsIndia account to write your query and our advisor will suitably help you. thanks, Vidya

I’m Fundsindia customer pls review about my fund selection

Hi Arun,

Your advisor will be the best person to review your portfolio. You can ask for a review by directly contacting your advisor over call and email. You can also ask for a review through our ‘Advisor Appointment’ system (you can see this under the ‘Help’ section of your account).

Regards.

Team FundsIndia

Hi Vidya,

I am existing investor with Funds India, I have too many funds in my portfolio and I want to reduce that number to optimal value. As paying too much FMC doesn’t look good to me. So could you please review my portfolio and share me list of funds keeping in mind diversification for a long term(retirement) with least duplication/overlapping funds and FMC.

Thanks,

Shailesh

Hello Shailesh,

We’ve shared your request with your FundsIndia advisor, who will contact you shortly to review your portfolio.

Thanks,

Bhavana

I’m Fundsindia customer pls review about my fund selection

Hi Arun,

Your advisor will be the best person to review your portfolio. You can ask for a review by directly contacting your advisor over call and email. You can also ask for a review through our ‘Advisor Appointment’ system (you can see this under the ‘Help’ section of your account).

Regards.

Team FundsIndia

Hi Vidya,

I am existing investor with Funds India, I have too many funds in my portfolio and I want to reduce that number to optimal value. As paying too much FMC doesn’t look good to me. So could you please review my portfolio and share me list of funds keeping in mind diversification for a long term(retirement) with least duplication/overlapping funds and FMC.

Thanks,

Shailesh

Hello Shailesh,

We’ve shared your request with your FundsIndia advisor, who will contact you shortly to review your portfolio.

Thanks,

Bhavana

Hello Madam,

I am 29, self-employed, married now. I am planning to invest in Mutual funds by doing some SIPs of Rs.20K every month for a time horizon of atleast 15 years. My target is maximum wealth generation to secure my children’s (max 2 kids) higher education and also save to plan for my early retirement. I am a moderate to aggressive investor.

I have sorted out few SIPs for my portfolio which are as follows:

1.SBI Bluechip Fund (G) – 5K,

2.ICICI Prudential Value Discovery Fund – 3K,

3.Mirae Asset Emerging Bluechip Fund – Regular Plan – 4K,

4.Birla SL Small and Midcap Fund (G) – 4k, and

5.DSP-BRTax Saver Fund (G) – 4K.

I request you to advice me and let me know if my portfolio will be ideal as per my requirement and time that I am willing to invest. And aso I wish to invest a lumpsum amount of Rs.5 lakhs and request for your suggest as to which funds I can invest this amount in for 15years time.

Thank you

Hello Sir,

Thanks for writing to us and sorry for the delay. From your picks, I see you have gone for more mid and small cap funds. Try to keep those to 20-30% of the portfolio. Also, try to introduce 20-30% in debt to provide some hedge to equity when it falls.

We are constrained from giving portfolio views through this forum. if you are a FundsIndia customer, please use the advisory support feature to ask your queries or for portfolio reviews. We will clarify them. thanks, Vidya

RESPECTED MAM,

MANY THANKS FOR YOUR VALUABLE RESEARCH ON MF. I AM 30 YEARS OLD AND WOULD LIKE TO INVEST IN THE FOLLOWING MID & SMALL CAP FUNDS FOR 5 YEARS THROUGH SIP FROM SEPT. 2017.

1. MIRAE ASSET EMERGING FUND

2. L&T INDIA VALUE FUND

3. BIRLA SUN LIFE VALUE FUND

4. L&T EMERGING BUSINESS FUND

NOW I NEED YOUR SUGGESTIONS & LOOKING FOR YOUR EARLY REPLY.

Hi,

Please note that putting all your investments into mid-cap and small-cap funds is highly risky, even if you can take it and have a long timeframe. Mid-caps and small-caps can be very volatile and over-investing here will open your portfolio to extreme vagaries. You should ideally have large-caps and debt in a portfolio. Coming to your funds, we won’t be able to provide specific advice here. It is a discussion forum only. If you’re a FundsIndia investor, you can book an appointment with your advisor who will guide you. You can also always sign up for an account, if you don’t have one!

Thanks,

Bhavana

RESPECTED MAM,

MANY THANKS FOR YOUR VALUABLE RESEARCH ON MF. I AM 30 YEARS OLD AND WOULD LIKE TO INVEST IN THE FOLLOWING MID & SMALL CAP FUNDS FOR 5 YEARS THROUGH SIP FROM SEPT. 2017.

1. MIRAE ASSET EMERGING FUND

2. L&T INDIA VALUE FUND

3. BIRLA SUN LIFE VALUE FUND

4. L&T EMERGING BUSINESS FUND

NOW I NEED YOUR SUGGESTIONS & LOOKING FOR YOUR EARLY REPLY.

Hi,

Please note that putting all your investments into mid-cap and small-cap funds is highly risky, even if you can take it and have a long timeframe. Mid-caps and small-caps can be very volatile and over-investing here will open your portfolio to extreme vagaries. You should ideally have large-caps and debt in a portfolio. Coming to your funds, we won’t be able to provide specific advice here. It is a discussion forum only. If you’re a FundsIndia investor, you can book an appointment with your advisor who will guide you. You can also always sign up for an account, if you don’t have one!

Thanks,

Bhavana

Dear Vidya,

I am 40 yr old having 2 kids. I am planning to invest 40~50 K in various Mutual Fund Sip for 7~8 yrs, and would withdraw money in 12~15 yrs for my kid’s education/marriage etc.

Please suggest the rough portfolio percentage in the various segment like Diversified, Small & Mid Cap, Large Cap, Thematic – Infrastructure, Balanced, Debt and Specific sectors like Banking, FMCG, Pharma etc.

I can take little more risk than a moderate portfolio.

Looking forward to your response.

Thanks,

Vikash

Vikash, I will be unable to provide an asset allocation without assessing your risk profile in a more methodical way. However, based on what you said you may look at a 70:30 equuity debt portfolio. with diversified fund, balanced fund, midcap fund and a debt fund. You really don’t need sector funds unless youa re adept in fllowing the sectors and timing your entry and exits in them. thanks, Vidya

Dear Vidya,

I need your valuable opinion on the mutual funds I have selected.

I am 34 year software engineer looking for financial freedom as soon as possible.I am going to invest in mutual fund with monthly SIP of 50 K for > 7 years in mutual fund. The target I want to reach is 2 crore(with indexation) for financial freedom within 7- 10 years. Consider me moderately aggressive investor.

Please go through my portfolio below and provide your valueable opinion on the funds selected. Help would be extremely appreciated.

LARGE CAP CATEGORY (40%)

Kotak Select focus – 20k

MID CAP CATEGORY(40%)

ABSL Pure Value – 7k

L &T midcap – 7 k

Mirae Asset Emerging Blue Chip – 6k

SMALL CAP CATEGORY(20%)

Reliance Small cap – 8k

HDFC Small cap – 8k

Franklin India small industries – 4k

The Portfolio aggregates(as analysed by valueresearchonline) for capital based category are: Giant (29.07%), Large Cap(14.60%), Midcap(34.03), Smallcap(20.90).

Sectorial division are : Financial(24%), Construction(11.7%), Energy(9%), Chemicals(8%), FMCG(8%), Automobile(7%), Energy(7%) …..

Thanks

Niraj

Dear Vidya,

I am 40 yr old having 2 kids. I am planning to invest 40~50 K in various Mutual Fund Sip for 7~8 yrs, and would withdraw money in 12~15 yrs for my kid’s education/marriage etc.

Please suggest the rough portfolio percentage in the various segment like Diversified, Small & Mid Cap, Large Cap, Thematic – Infrastructure, Balanced, Debt and Specific sectors like Banking, FMCG, Pharma etc.

I can take little more risk than a moderate portfolio.

Looking forward to your response.

Thanks,

Vikash

Vikash, I will be unable to provide an asset allocation without assessing your risk profile in a more methodical way. However, based on what you said you may look at a 70:30 equuity debt portfolio. with diversified fund, balanced fund, midcap fund and a debt fund. You really don’t need sector funds unless youa re adept in fllowing the sectors and timing your entry and exits in them. thanks, Vidya

Dear Vidya,

I need your valuable opinion on the mutual funds I have selected.

I am 34 year software engineer looking for financial freedom as soon as possible.I am going to invest in mutual fund with monthly SIP of 50 K for > 7 years in mutual fund. The target I want to reach is 2 crore(with indexation) for financial freedom within 7- 10 years. Consider me moderately aggressive investor.

Please go through my portfolio below and provide your valueable opinion on the funds selected. Help would be extremely appreciated.

LARGE CAP CATEGORY (40%)

Kotak Select focus – 20k

MID CAP CATEGORY(40%)

ABSL Pure Value – 7k

L &T midcap – 7 k

Mirae Asset Emerging Blue Chip – 6k

SMALL CAP CATEGORY(20%)

Reliance Small cap – 8k

HDFC Small cap – 8k

Franklin India small industries – 4k

The Portfolio aggregates(as analysed by valueresearchonline) for capital based category are: Giant (29.07%), Large Cap(14.60%), Midcap(34.03), Smallcap(20.90).

Sectorial division are : Financial(24%), Construction(11.7%), Energy(9%), Chemicals(8%), FMCG(8%), Automobile(7%), Energy(7%) …..

Thanks

Niraj

Nice Article. Enjoyed it.

In my experience if you want to invest 20000 per month we have to choose 10 funds each 2000 sip in different dates which will absorb market volatility. The funds are multi cap, midcap, large cap , balanced each2 funds and micro cap , small cap each one.

Hello Venkat, not necessarily. some times just one diversified fund/large-cap fund, one midcap and one debt fund can also do the job for you 🙂 It depends on the choice of funds. thanks, Vidya

Hi,

Can you advice on the my below portfolio of 13000 PM SIP for 15 years.

SBI Bluechip Direct Growth : 2000

Kotak Select Focus Direct Growth : 2000

ADBSL Equity Direct Growth Fund : 2000

HDFC Balanced Direct Growth :2000

DSP black rock microcap Direct Growth : 2000

Mirae Asset Emerging Bluechip : 1000

DSP black Rock Tax Saver Direct Growth : 2000

thanks

Hello,

We don’t provide portfolio-specific reviews or queries on this forum. Queries are routed through our platform. This blog is meant primarily for discussion and informative articles. Please talk to your advisor on your portfolio.

Thanks,

Bhavana

I have never understood the logic of midcap funds? can you please explain it to me

Hello Prijesh, This ppt will tell all you about mid caps. It id dated but relevant in terms of its explanation. thanks, Vidya

Please explain

Hi Bala,

I want to invest Rs10000 per month in ELSS fund.Please let me know how many funds should i choose and how it can be diversified.I am tracking few ELSS funds from Feb 2015 till now but i can see NAV increase when share market goes up and it went down when market goes down.IN last three years market goes very well but suppose market after 3 years is 30000 only then we have a loss in ELSS funds as NAV is based on market indices.

Hi Piyush, Sorry for the delay in reply.

As ELSS funds invest in equity markets, they will, naturally fall and grow with the market. You should not be put down by short-term falls. In the long term 5-10 years, the chances of negative returns (historically) in the market is nil unless something is terribly wrong with the economy. ELSS funds too need long time frame. The lock in may be 3 years but like any other equity fund you should consider 5 year holding to play out volatility. Plese read our article if you are a first time equity investor pl. read this: https://blog.fundsindia.com/blog/advisory/fundsindia-strategies-the-equity-fund-playbook-for-rookie-investors/7667

For the amount mentioned by you 2 funds should do. We will be able to provide you suggestions on funds if you ask your query through your activated fundsIndia account – using the advisor appointment feature. It is free for all our investors. The blog is only a forum for discussion. thanks, Vidya

Could you please review my portfolio

Birla SL Frontline Equity Direct-G 1,000 per month

HDFC Equity-G 1,000 per month

HDFC Mid-Cap Opportunities- G 2,000 per month

ICICI Pru Balanced Direct-G 1,000 per month

ICICI Pru Focused Bluechip Equity Direct -G 2000

Kotak Select Focus Direct-G 1,000 per month

Reliance Equity Opportunities-G 1000 per month

Ashish, Kindly activate your FundsIndia account. If you are already an investor, please write to us using the ask advisor feature (in help tab). As a FundsIndia investor, we will help you review your portfolio and also consolidate them in one platform, online, with us. thanks. The blog is merely a discussion forum. We will be constrained from offering ortfolio specific comments here. Vidya

Great article. I’m fundsindia investor. I’m investing with 20 year target. Portfolio funds are : ICICI FOC – 20%, BIRLA F/L EQ – 20%, UTI OPP – 10%, HDFC PRU – 10%, ICICI DISC -20%, FRANKLIN SM COS. -20%. My goal is wealth creation over long-term. Should I make any changes.

Hello Sir, I do not find all the said funds in your portfolio under this current email (only some are there). It is easier for us to know your entire investments before recommending anything. If you have some of your investments offline, bring them in and consolidate so that you can manage them easily. IF you already have them, pl mention the email ids of your accounts when you write to us using the below feature. Our advisors will help you review your portfolios if you request using the ‘Advisor appointment’ feature when you click help tab. The funds you mentioned here are all good but remember Franklin Smaller Cos is a risky bet and a 20% exposure can be high. Also you do not have debt. If you wish to reallocate, as suggested pl use the feature mentioned above. The blog is merely a discussion forum. thanks, Vidya

One of the best articles that I’ve read on this topic. I would like some actual fund recommendations for this point that you make: “If you are looking for long-term investing in debt, the simplest option to avoid crowding is to choose a fund that will invest across instruments (gilt, corporate bond, commercial paper, deposits), and also vary its portfolio maturity based on the interest rate cycle. 1-2 funds should suffice.”. I’m building my debt portfolio and am confused by the inconsistent categories used by various websites – each has their own name for different debt categories.

Hello Pavan, thanks. Look for income funds/dynamic bond funds if you have a long-term time frame of 3-plus years. As for fund recommendations, we would be constrained from giving it in this forum. the blog is a general discussion forum. If you are a FundsIndia inevstor, please use the ‘advisor appointment’ feature in the help tab and post your query. We will understand your requirement and call or mail you as you need. This will also help us keep track fo queries and respond efficiently. thanks, Vidya

Hi,

I am a senior citizen having an account under National Savings Scheme, 1987. I would like to withdraw full amount with least Tax implication.Please suggest best option available to me.

Thanks,

Sathyamurthy G

Hello Sir, NSS is subject to tax unlike NSC. So you can’t do much there. You can withdraw and invest in Post Office Senior citizens’ scheme and get 80C benefit (if you wish to save tax) and if you need regular interest income. Mutual funds are suitable if you do not expect imemdiate regualr income from the corpus. thanks,Vidya

Hi,

Thanks for your suggestion and prompt response.

Regards,

Sathyamurthy G

Great article clears most of my doubts. i invest 23k per month in sips of 5 equity mutual funds-1 elss and 4 large and midcap equity.

What is the maximum sip amount for a scheme?

Since i want to exhaust my 80c limit I am investing 8k in elss , is it risky? But when i wanted to split to 2 elss funds then they are very much co-related.

Hello Arun – The maximum per scheme is purely dependent on the overall allocation and the nature (risk profile) of the fund. For example: If you have a single mid-cap fund then the max can be 20-30%. and so on. Same holds good for max SIP per scheme. Rs 8000 in one ELSS fund is fine provided it is not a risky fund. For further fund-specific queries if any, please use the advisor appointment feature if you have a FundsIndia account to provide any specific advice. thanks, Vidya

Hello Madam,

I am 29, self-employed, married now. I am planning to invest in Mutual funds by doing some SIPs of Rs.20K every month for a time horizon of atleast 15 years. My target is maximum wealth generation to secure my children’s (max 2 kids) higher education and also save to plan for my early retirement. I am a moderate to aggressive investor.

I have sorted out few SIPs for my portfolio which are as follows:

1.SBI Bluechip Fund (G) – 5K,

2.ICICI Prudential Value Discovery Fund – 3K,

3.Mirae Asset Emerging Bluechip Fund – Regular Plan – 4K,

4.Birla SL Small and Midcap Fund (G) – 4k, and

5.DSP-BRTax Saver Fund (G) – 4K.

I request you to advice me and let me know if my portfolio will be ideal as per my requirement and time that I am willing to invest. And aso I wish to invest a lumpsum amount of Rs.5 lakhs and request for your suggest as to which funds I can invest this amount in for 15years time.

Thank you

Hello Sir,

Thanks for writing to us and sorry for the delay. From your picks, I see you have gone for more mid and small cap funds. Try to keep those to 20-30% of the portfolio. Also, try to introduce 20-30% in debt to provide some hedge to equity when it falls.

We are constrained from giving portfolio views through this forum. if you are a FundsIndia customer, please use the advisory support feature to ask your queries or for portfolio reviews. We will clarify them. thanks, Vidya